ID : MRU_ 432958 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

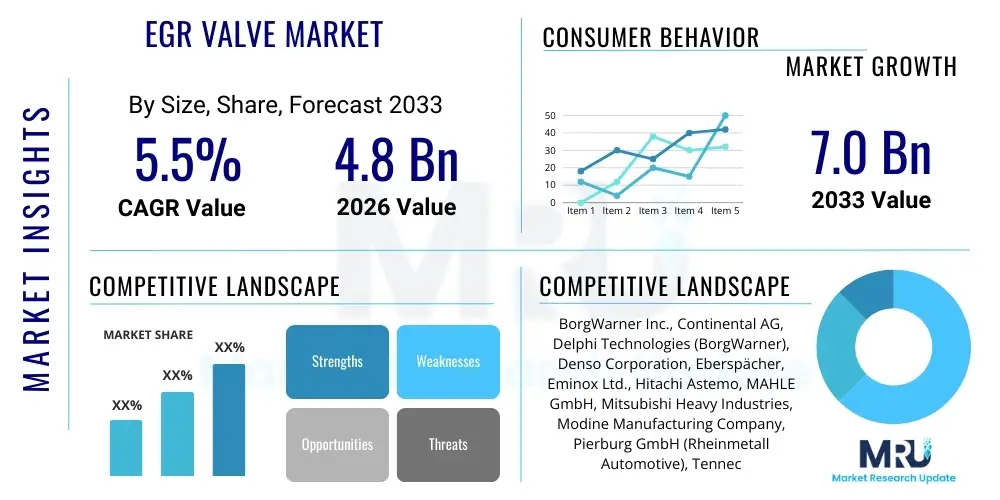

The EGR Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 7.0 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by the increasing complexity of emission control systems required globally, offsetting the eventual transition to electric propulsion in certain light-duty segments. The valuation reflects the high cost associated with advanced electronic and cooled EGR systems necessary for modern high-efficiency internal combustion engines.

The Exhaust Gas Recirculation (EGR) Valve Market serves as a critical nexus within the global automotive industry’s ongoing effort to mitigate environmental pollution stemming from internal combustion engine (ICE) operations. EGR technology functions as a primary, in-cylinder NOx reduction strategy by introducing cooled exhaust gas back into the intake air charge. This deliberate recirculation effectively reduces the concentration of oxygen and absorbs heat during combustion, consequently lowering peak cylinder temperatures below the threshold required for the substantial formation of Nitrogen Oxides (NOx). The increasing stringency of global regulatory frameworks, including the phased implementation of Euro 6d, EPA Tier 3 standards, and equivalent protocols in Asia Pacific, establishes the mandatory foundation for sustained market demand. EGR systems are now fundamental components in both Compression Ignition (Diesel) and increasingly in Spark Ignition (Gasoline Direct Injection or GDI) engine platforms, reflecting the technology's versatile application in achieving multi-faceted performance and emission targets.

EGR valve systems are differentiated by their design, ranging from simple vacuum-operated mechanical valves, now largely obsolete in new vehicles, to sophisticated electronic solenoid and stepper motor-controlled units. Modern electronic valves offer unparalleled precision, allowing the engine control unit (ECU) to modulate exhaust gas flow with microsecond accuracy based on real-time parameters such as engine speed, load, air mass, and temperature. This precision is vital for maximizing NOx reduction while avoiding negative side effects like combustion instability or excessive particulate matter formation. Furthermore, the market encompasses the ancillary components crucial for system efficacy, most notably the EGR cooler, which is integral to the process, ensuring the recirculated gas is sufficiently cooled before re-entry, thereby maximizing the density of the charge and enhancing the temperature reduction effect in the combustion chamber. The demand for robust, highly efficient coolers designed to withstand extreme thermal gradients and corrosive condensates significantly influences market valuation.

Major applications of EGR systems are concentrated in high-volume vehicle segments: light-duty passenger vehicles (especially those employing GDI technology or diesel powertrains), heavy-duty commercial trucks and buses, and off-highway machinery utilized in construction, agriculture, and marine sectors. Key benefits include the achievement of mandatory NOx limits, which is non-negotiable for vehicle certification and sale, along with indirect advantages such as minor improvements in specific fuel consumption under certain cruising conditions. The market's driving factors extend beyond mere regulation; they include advancements in turbocharging and engine downsizing, which inherently increase combustion pressures and temperatures, necessitating more aggressive and reliable EGR solutions. The expanding global vehicle parc and the corresponding growth in the aftermarket for replacement components further reinforce the market’s stability against the backdrop of long-term automotive evolution.

The global EGR Valve Market demonstrates a resilient growth pattern, primarily navigating the short-term mandates of rigorous emission standards against the long-term threat of vehicle electrification. Business trends reveal a concentrated effort by leading Tier 1 automotive suppliers to consolidate expertise in mechatronics, focusing on developing fully integrated EGR modules that incorporate the valve, cooler, and associated sensing and control electronics into a single, optimized package. There is a perceptible move toward standardizing modular components for global platforms to achieve economies of scale, even as regional regulatory variations require specific calibration adjustments. Strategic investments are heavily directed towards material science research aimed at developing corrosion-resistant alloys for coolers and anti-fouling coatings for valves, directly addressing the key reliability concerns that drive aftermarket failure rates and warranty claims for OEMs.

Geographically, the market presents a dichotomy of mature, highly technologically advanced markets (Europe and North America) and rapidly expanding, high-growth volume markets (Asia Pacific). Europe continues to dictate the pace of technological development, particularly for diesel engine solutions, owing to the stringent Euro 7 preparatory measures which demand highly efficient and reliable low-pressure EGR systems alongside robust thermal management capabilities. North America, while experiencing a slower transition in passenger vehicles, maintains a steady, substantial market driven by the heavy-duty truck segment, where compliance with EPA standards necessitates exceptionally durable, high-flow EGR assemblies. This region also contributes significantly to the aftermarket sector due to the long operational lifespan of commercial vehicles.

In terms of segmentation, the shift in focus towards Gasoline EGR (G-EGR) technology represents a crucial trend. Historically dominated by diesel applications, the passenger vehicle segment is increasingly adopting G-EGR to meet evolving particulate matter and NOx standards for GDI engines. The commercial vehicle segment (Heavy-Duty Vehicles or HCVs) remains the most critical revenue stream in terms of value, as these components are larger, more complex, and subject to higher operational demands, resulting in premium pricing and specialized component design. The aftermarket segment is expanding due to the increasing mechanical and thermal stress placed on modern EGR systems, leading to more frequent failure and replacement cycles, thereby providing a vital secondary revenue channel for component manufacturers.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) techniques is poised to fundamentally transform the functionality and service lifecycle of EGR valve systems, addressing historical pain points related to reliability and real-time control. User inquiries frequently explore how AI can move beyond simple threshold monitoring to implement true predictive maintenance, allowing vehicle owners and fleet managers to replace components based on degradation probability rather than reactive failure. There is a high interest in understanding how advanced ML models can leverage massive datasets of operational parameters—covering driving cycles, altitude, temperature extremes, fuel quality, and engine behavior—to develop highly optimized control maps. These maps could instantaneously adjust EGR flow rates to maintain the most efficient balance between NOx reduction and fuel economy under dynamic, real-world driving conditions, a capability far exceeding static, map-based ECU programming.

A central expectation among industry stakeholders is that AI will significantly mitigate the persistent problem of EGR system fouling caused by carbon and oil residue. By analyzing sensor drift and correlation patterns, AI algorithms can identify the onset of material buildup well before flow restriction becomes significant, prompting the engine management system to initiate preventive actions, such as temporary flow adjustments or thermal cycling strategies designed to burn off deposits. Furthermore, AI tools are accelerating the research and development pipeline. Generative design and optimization algorithms are being utilized to simulate thousands of potential valve geometries and cooler matrix designs, quickly identifying the most thermally efficient, weight-optimized, and durable solutions that would be prohibitively time-consuming to achieve through traditional iterative engineering methods. This ensures that the next generation of EGR components meets the ultra-tight tolerances mandated by future Euro 7 and equivalent regulations.

The overall impact of AI is highly strategic, moving EGR components from standard mechanical devices with electronic control to smart, self-monitoring, and self-optimizing subsystems within the powertrain. This capability reduces warranty costs for OEMs, improves engine longevity for end-users, and maximizes the environmental performance required for stringent emissions certification. Fleet managers are particularly interested in the telematics integration, where AI-processed EGR data can be aggregated across an entire fleet to identify systemic component weaknesses or fuel/operational dependencies affecting reliability, thus improving procurement and operational planning significantly.

The EGR Valve Market is fundamentally propelled by powerful legislative drivers that ensure the technology remains integral to the automotive ecosystem for the foreseeable future, despite electrification trends. The most critical driver is the continuous tightening of global emission standards, particularly the move towards stricter limits on NOx emissions under Real Driving Emissions (RDE) testing protocols. Regulatory bodies are demanding that vehicles maintain low emissions not just under standardized laboratory conditions, but across a wide range of operational and environmental variables (e.g., varying altitude, load, and temperature). This legislative pressure compels OEMs to invest heavily in highly robust, quick-acting, and thermally efficient electronic EGR systems capable of maintaining precise control under transient conditions, thereby escalating the complexity and consequently the market value of the components.

However, the market faces two primary, formidable restraints. Firstly, the exponential investment and policy push toward battery electric vehicles (BEVs) represents a structural long-term threat, as EVs entirely eliminate the need for EGR components. Although the ICE phase-out timeline varies significantly by region and vehicle segment (with heavy-duty remaining ICE-reliant longer), the overall reduction in the addressable market for new installations beyond 2035 poses a significant long-term constraint. Secondly, the intrinsic operational reliability issues of EGR systems, primarily stemming from carbon fouling, corrosion, and associated high maintenance costs, restrain market growth. These reliability concerns often lead to adverse consumer perception and drive manufacturers to seek alternative, potentially more expensive, non-EGR based NOx reduction strategies (e.g., highly optimized Selective Catalytic Reduction (SCR) systems or advanced catalyst technology).

Opportunities for market players are concentrated around technological differentiation and strategic service provision. The most significant opportunity lies in the burgeoning global aftermarket for replacement components, driven by the sheer volume of aging vehicles equipped with first- and second-generation EGR systems that are now failing due to operational stress or mileage accumulation. Manufacturers specializing in durable, high-quality replacement units that offer superior resistance to fouling and corrosion are well-positioned. Another key opportunity involves capitalizing on the need for Gasoline EGR (G-EGR) technology, developing bespoke solutions optimized for GDI engines to meet combined NOx and Particulate Matter (PM) reduction targets. The primary impact forces influencing the market are regulatory mandates (acting as a consistent upward pressure), technological innovation focused on component durability (a stabilizing force), and the disruptive impact of electrification (a long-term downward pressure).

A detailed segmentation of the EGR Valve Market provides essential insights into the diverse demands and varying technological requirements across different automotive applications globally. Segmenting by Vehicle Type reveals that while passenger cars constitute the highest volume of installations, the Commercial Vehicle (HCV) segment offers the highest value per unit due to the necessity for larger, more complex, and heavily cooled EGR modules designed for sustained, high-load operation. The rapid implementation of emission standards in previously under-regulated commercial sectors, particularly in emerging markets, ensures that HCVs remain a critical focal point for EGR innovation and revenue generation, demanding specialized product lines that emphasize robustness and thermal resilience over compactness.

Analyzing the market by Component highlights the shift towards integrated modules, which often include both the electronic valve and the water-cooled heat exchanger, optimizing system performance and reducing assembly complexity for OEMs. The segment dedicated to EGR Coolers is growing notably, driven by the fact that cooling efficiency is paramount for NOx reduction, and the coolers themselves are prone to failure due to thermal cycling stress and corrosive exhaust condensate. Furthermore, the segmentation by Fuel Type underscores the market's evolution, with the Diesel segment historically dominating due to high NOx formation, but the Gasoline segment (G-EGR) demonstrating the highest proportional growth as GDI engines become standard and face new NOx and PM regulatory pressures, requiring specialized EGR architectures compatible with gasoline combustion characteristics.

The EGR Valve Value Chain commences with highly specialized upstream suppliers providing critical raw materials and sub-components. This includes sophisticated metallurgical companies that supply specialized stainless steel alloys (such as high-nickel content variants) crucial for the EGR cooler's heat exchanger core, which must resist high-temperature oxidation and acid corrosion prevalent in diesel exhaust. Concurrently, electronic component manufacturers supply the high-precision actuators (stepper motors or solenoids) and robust sensors required for electronic valve control. The emphasis at this stage is on material quality and consistency, as component failure is often traceable back to micro-structural deficiencies in the raw materials used in critical sealing and heat exchange surfaces. Strong collaborative relationships between Tier 1 manufacturers and material suppliers are essential for achieving continuous improvements in thermal performance and durability.

The core manufacturing stage is dominated by Tier 1 suppliers who perform high-precision assembly, welding (especially vacuum or laser welding for cooler cores), and rigorous calibration and testing. Due to the component's critical role in meeting regulatory standards, quality control is exceptionally strict. Products are then distributed predominantly through direct channels to automotive OEMs globally. This direct channel requires complex logistics and highly coordinated Just-In-Time (JIT) supply chain management to feed high-volume engine assembly lines. The specifications for OEM supply are bespoke, tied to individual engine model requirements, making the entry barrier high and favoring established global players with extensive R&D capabilities and existing supply contracts.

The indirect channel, comprising the aftermarket, handles the distribution of replacement parts. This channel flows from Tier 1 manufacturers or specialized aftermarket distributors to wholesale parts providers, authorized service networks, and independent garages. Profit margins can often be higher in the aftermarket, incentivizing manufacturers to develop robust aftermarket strategies, including packaging, branding, and comprehensive parts catalogs. Downstream, the value chain focuses on maintenance and repair, driven by the operational lifecycle of vehicles. Effective service and diagnostic tools are essential, as incorrect installation or failure to address underlying causes (e.g., turbocharger oil consumption) can lead to immediate recurrence of EGR system issues. The overall chain is characterized by high technical barriers, stringent quality requirements, and complexity driven by the need to cater simultaneously to high-volume OEM demand and high-variety aftermarket needs.

The primary customer base for the EGR Valve Market is fundamentally segmented into organizations that purchase the product for new vehicle production (OEMs) and organizations responsible for vehicle maintenance and repair (Aftermarket channels). Global Automotive and Engine Original Equipment Manufacturers (OEMs)—including major passenger vehicle manufacturers (e.g., Volkswagen Group, Ford, Toyota) and heavy-duty engine makers (e.g., Cummins, Daimler Trucks)—represent the largest volume purchasers. Their procurement strategies prioritize technical integration, global quality assurance, and the supplier's ability to demonstrate compliance with the most recent and future emission regulations, making long-term supply agreements the norm. OEMs require valves and coolers that are optimized for their specific engine architecture to pass stringent certification tests, driving customization and technical partnerships with Tier 1 suppliers.

The second major category involves large Fleet Operators and Managers, particularly those running substantial fleets of commercial vehicles (freight haulage, municipal transit, waste management). For these operators, the EGR system is a critical operational component; its failure results in vehicle downtime and potential regulatory fines. They are key purchasers in the aftermarket, seeking high-durability replacement parts and often favoring components supplied directly by the original Tier 1 manufacturer or certified alternatives. Their purchasing criteria heavily emphasize Mean Time Between Failures (MTBF) and overall TCO, requiring parts that withstand continuous, high-mileage operation and challenging duty cycles, such as constant stop-start urban driving that exacerbates fouling issues.

Finally, the broad network of Independent Aftermarket Service Providers, authorized dealerships, and spare parts wholesalers forms the tertiary but highly profitable customer base. These entities require immediate availability of a wide variety of EGR components covering different model years and regulatory standards across various vehicle brands. Their success depends on accurate diagnostics and reliable parts supply. The increasing complexity of electronic EGR systems also necessitates specialized diagnostic equipment and training for technicians within this service sector, which manufacturers often provide as part of their value-added offering, cementing customer loyalty and ensuring correct installation procedures are followed.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 7.0 Billion |

| Growth Rate | CAGR 5.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BorgWarner Inc., Continental AG, Delphi Technologies (BorgWarner), Denso Corporation, Eberspächer, Eminox Ltd., Hitachi Astemo, MAHLE GmbH, Mitsubishi Heavy Industries, Modine Manufacturing Company, Pierburg GmbH (Rheinmetall Automotive), Tenneco Inc., Sogefi Group, Weifu High-Technology Group, Cummins Inc., Valeo, Schaeffler AG, Faurecia (FORVIA), Hanon Systems, Korens Co., Ltd., Calsonic Kansei (Marelli), Keihin Corporation, IHI Corporation, Mikuni Corporation, Standard Motor Products, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The contemporary technological landscape within the EGR Valve Market is defined by the necessity for extreme precision, integration, and resistance to environmental degradation. The core technology centers on fully electronic control, utilizing high-speed stepper motors or Pulse Width Modulated (PWM) solenoid actuators to achieve near-instantaneous and continuous modulation of exhaust flow, which is non-negotiable for meeting RDE (Real Driving Emissions) requirements. These electronic controls rely heavily on sophisticated embedded software and sensor technology, including high-accuracy flow meters and rapid-response temperature and position sensors, which provide the essential feedback loop to the ECU for maintaining target NOx levels across fluctuating engine loads and temperatures. The trend is moving away from simple on/off mechanical operation towards continuous, highly controlled flow proportional to engine demand.

Advanced thermal management solutions represent another pivotal technological focus. With modern turbocharged engines operating at increasingly higher exhaust gas temperatures (EGT), the effectiveness and durability of the EGR Cooler are paramount. Leading manufacturers are deploying proprietary heat exchanger designs, often featuring highly convoluted micro-channel structures made from specialized stainless steel or exotic alloys, specifically designed to maximize heat transfer efficiency within a constrained physical volume. Critical advancements include anti-corrosion coatings and improved welding techniques to prevent leaks caused by thermal cycling stress and the highly corrosive acidic condensate generated during cooling. Furthermore, the integration of by-pass valves within the cooler module allows the ECU to intentionally reduce cooling under cold-start conditions, accelerating catalyst warm-up and improving system efficiency before full cooling is required.

Looking forward, key technology development is concentrated on mitigation strategies for component fouling. This includes researching and deploying catalytic coatings on the internal surfaces of both the valve and cooler to inhibit carbon and soot adhesion. Furthermore, the increasing adoption of Low-Pressure EGR (LP-EGR), which draws cleaner exhaust gas downstream of filtration devices (like the Diesel Particulate Filter or Gasoline Particulate Filter), is a major technological shift. LP-EGR requires complex piping and sometimes a dedicated compressor or pump to overcome pressure differentials, but its benefits—reduced fouling, improved fuel economy, and better thermal efficiency—make it the preferred route for high-compliance engine architectures. The entire system is becoming increasingly networked, relying on high-speed CAN bus communication to integrate seamlessly with turbochargers, variable valve timing, and post-treatment systems.

Regional market consumption and technological trends in the EGR Valve Market are highly variable, directly mirroring local regulatory implementation and the structure of the local vehicle fleet. This geographic variance necessitates tailored manufacturing and supply strategies for global vendors.

The primary function of the Exhaust Gas Recirculation (EGR) valve is to reduce harmful Nitrogen Oxide (NOx) emissions. It achieves this by routing a measured portion of inert exhaust gas back into the combustion chamber, which lowers the peak combustion temperature. Regulatory bodies worldwide mandate EGR systems in internal combustion engines (ICE) to comply with stringent emission standards like Euro 6 and EPA Tier 3, making it a critical component for environmental compliance and vehicle certification.

The long-term outlook for the EGR Valve Market faces structural restraint from the accelerating global policy shift towards Battery Electric Vehicles (BEVs), which completely eliminate the need for EGR systems. However, in the mid-term (2026-2033), the market remains robust, sustained by continuous growth in the commercial vehicle, heavy-duty truck, and hybrid vehicle (HEV) segments, all of which continue to rely on complex, highly regulated ICEs, ensuring stable OEM and aftermarket demand.

The persistent issue of fouling caused by soot and carbon is being addressed through several technological advancements. Key solutions include the increased adoption of Low-Pressure EGR (LP-EGR) which utilizes cleaner exhaust gas, development of anti-fouling coatings (such as ceramic or specialized polymer coatings) on internal valve surfaces, and the implementation of advanced AI-based diagnostic algorithms that predict and attempt to mitigate buildup before system blockage occurs.

The Gasoline Engines segment (G-EGR) is experiencing the highest proportional growth. Historically dominated by diesel applications, the rise of Gasoline Direct Injection (GDI) engines requires G-EGR systems to comply with modern particulate matter (PM) and NOx standards. This expansion into high-volume passenger car platforms represents a significant new revenue stream for component manufacturers, expanding the overall addressable market.

The EGR Cooler is becoming critical because modern engines run at higher efficiencies and thus generate hotter exhaust gases. For EGR to be effective in reducing NOx, the recirculated gas must be cooled significantly. The cooler must be extremely efficient and robust, utilizing high-grade materials to withstand immense thermal stress and corrosive acidic condensate, making it a high-value, high-failure-rate component driving significant R&D investment and replacement demand.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.