ID : MRU_ 433446 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

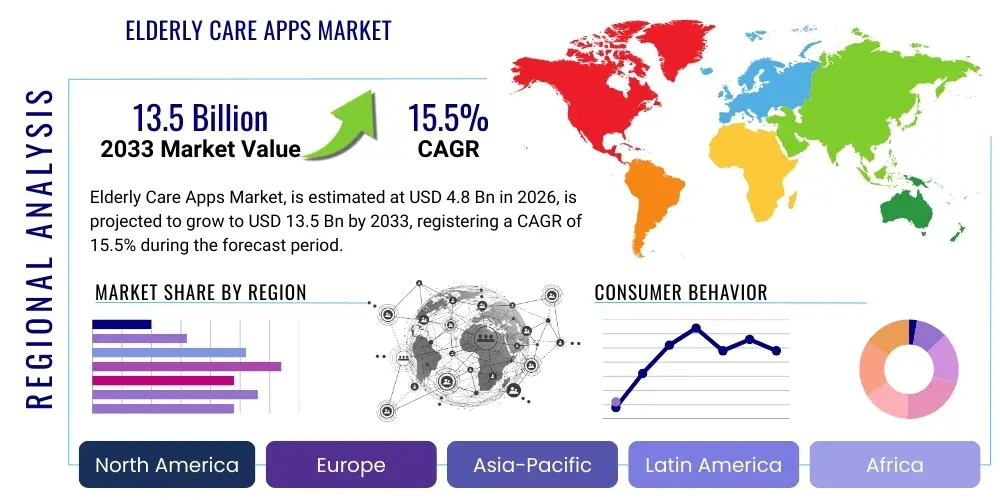

The Elderly Care Apps Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033.

The Elderly Care Apps Market encompasses a sophisticated and rapidly evolving ecosystem of mobile applications specifically engineered to support the physical, cognitive, and social well-being of the global geriatric population, concurrently providing indispensable tools for their formal and informal caregivers. These digital solutions represent a critical component of the emerging digital health paradigm, moving beyond simple health tracking to offer comprehensive platforms for remote patient monitoring (RPM), personalized medication management, proactive emergency response coordination, and virtual social engagement. The foundation of this market's growth lies in its ability to harness pervasive smart technology, enabling continuous, non-invasive data collection regarding the user's daily activities and physiological status, thereby significantly improving the feasibility and quality of home-based care. The market is fundamentally driven by the global imperative to manage the healthcare demands of an increasingly long-lived population while navigating persistent shortages of professional care staff and optimizing escalating institutional care expenses.

The product portfolio within the elderly care apps sector is remarkably diverse, spanning highly specialized clinical applications and general wellness tools. Key offerings include sophisticated telemonitoring apps capable of integrating data from various wearable sensors (such as ECG monitors, blood pressure cuffs, and oximeters) to provide real-time vital sign tracking and analysis. Another prominent category involves robust communication and logistical platforms that enable seamless coordination among dispersed care teams, utilizing secure messaging, shared calendars for appointments, and detailed reporting functions for physician review. Furthermore, specialized applications focusing on cognitive health, utilizing gamification and tailored exercises based on established neuroscience principles, are gaining traction as populations globally face rising incidences of dementia and Alzheimer's disease. The core function of these products transcends mere digitalization; they aim to restore autonomy and dignity to the elderly by placing control over health management directly into the hands of the individual or their immediate support structure, facilitating a preventative rather than reactive approach to chronic condition management and potential crises.

The principal market benefits driving the substantial projected growth stem from verifiable improvements in care efficiency and substantial cost reduction across the healthcare continuum. By enabling continuous preventative monitoring and timely alerts, these applications drastically decrease the likelihood of preventable emergency room visits and costly, prolonged hospital stays, thereby offering significant economic advantages to healthcare systems and individual payers. Major driving factors include the demographic tsunami of the aging Baby Boomer generation entering their senior years, leading to an unprecedented demand for flexible care models. This demand is met by continuous technological breakthroughs, particularly in miniaturized sensor accuracy and the development of highly intuitive user interfaces that lower the barrier to entry for older users. Favorable global regulatory shifts, such as increased governmental endorsement and reimbursement for telehealth services, further accelerate the commercial viability and large-scale deployment of these digitally integrated elderly care solutions across both developed and rapidly developing economies.

The Elderly Care Apps market is currently experiencing significant acceleration, driven by powerful demographic and technological tailwinds. Key business trends include a pronounced shift toward holistic wellness platforms that integrate physical health, medication management, and mental health support, moving beyond simple safety alerts. There is an observable consolidation trend, with major technology and healthcare conglomerates actively acquiring smaller, specialized app developers to rapidly integrate niche functionalities, such as advanced predictive analytics for fall risk or highly secured communication pathways compliant with international standards like GDPR and HIPAA. Furthermore, developers are increasingly leveraging Software as a Service (SaaS) models, offering tiered subscription packages that cater to a wide range of user needs, from basic free versions supported by advertisements to premium enterprise versions offering dedicated clinical support and full EHR integration for institutional clients.

Geographically, market expansion is heterogeneous yet robust. North America maintains its leadership, capitalizing on substantial venture capital funding and high rates of clinical acceptance for RPM technologies. However, the Asia Pacific (APAC) region is forecasted to be the primary engine of future growth, spurred by unprecedented demographic pressures in countries such as Japan and China, forcing immediate governmental investment in scaled digital care infrastructure. European markets are characterized by stringent privacy standards and a strong focus on seamless integration with public health services, ensuring equity of access. Regional strategies must therefore be highly localized: focusing on reimbursement maximization in North America, addressing scalability and infrastructure limitations in APAC, and ensuring regulatory compliance and interoperability across fragmented national health systems in Europe. This differential growth pattern necessitates highly adaptive investment and partnership strategies from global market participants to capture region-specific opportunities effectively.

Segmentation analysis highlights critical growth areas. By application type, the Chronic Disease Management segment within Health Management is showing the steepest growth trajectory, essential due to the high correlation between age and the prevalence of multiple co-morbidities. By end-user, the Caregivers and Family Members segment remains the dominant revenue driver, emphasizing the ongoing necessity for robust remote oversight and communication features within app design. Technology trends emphasize the transformative impact of AI and Machine Learning, which are essential for processing the massive influx of data generated by connected IoT devices, enabling highly accurate behavioral pattern analysis and personalized care path recommendations. This strategic focus on AI-driven prediction and personalization is crucial for maintaining competitive advantage and driving long-term value creation in the highly competitive ecosystem of digital elderly care solutions.

Common user inquiries concerning Artificial Intelligence (AI) in Elderly Care Apps frequently address the ethical implications, particularly regarding autonomy and the depersonalization of care. Users and caregivers commonly ask about the accuracy of AI-driven health risk assessments, questioning whether algorithms can reliably detect distress signals or impending health events better than human intuition, and what mechanisms are in place for minimizing false positives, especially concerning fall detection which can cause alarm and distress. There is substantial concern over algorithmic bias, specifically how AI models trained on certain demographic datasets might perform poorly when applied to diverse ethnic or geographic populations, potentially leading to care inequities. Moreover, users are deeply interested in the transparency, or 'explainability,' of AI recommendations, requiring assurance that they can understand the basis upon which critical health alerts or lifestyle changes are suggested by the application, moving beyond black-box decision-making processes.

The implementation of AI and Machine Learning (ML) is fundamentally transforming the value proposition of elderly care applications by introducing true predictive intelligence. AI engines process heterogeneous data sets—ranging from passively collected vital signs and sleep patterns to active input like mood trackers and medication logs—to construct a comprehensive, longitudinal profile of the senior’s health baseline. This capability allows the system to identify highly subtle deviations that precede significant health crises, such as changes in walking speed correlated with increased fall risk or slight fluctuations in heart rate variability indicative of potential cardiac issues. Consequently, AI enables applications to provide highly tailored, just-in-time interventions, moving the standard of care from responsive treatment following an event (like a fall) to proactive mitigation measures implemented before the event occurs. This shift enhances patient safety and significantly reduces the overall burden on emergency medical services and institutional care facilities.

Beyond clinical prediction, AI is crucial in enhancing the user experience and administrative efficiency within the ecosystem. NLP technologies are employed to create highly empathetic and context-aware virtual assistants, offering conversational support that aids in cognitive engagement and combats pervasive social isolation, serving as a non-judgmental presence that encourages routine adherence. Furthermore, AI optimizes the operational aspects for caregivers by automatically generating summarized, clinically relevant reports from voluminous raw data, streamlining communication with medical professionals, and efficiently managing complex scheduling across multi-person care teams. The integration of these intelligent systems ensures scalability and personalization simultaneously, confirming AI's role not just as a feature enhancer, but as the essential technological core driving market innovation, enabling applications to deliver more precise, individualized, and efficient care across a rapidly expanding user base.

The market dynamics of Elderly Care Apps are governed by a powerful interplay of propelling and restricting forces, synthesized into a set of core Drivers, Restraints, and Opportunities (DRO). The paramount Driver is the structural demographic shift globally, characterized by unprecedented growth in the population aged 65 and over. This burgeoning senior demographic creates an inherent, non-negotiable demand for scalable care solutions. Coupled with this is the dramatic escalation in traditional institutional care costs, making technologically mediated home care an economically superior and increasingly necessary alternative for families and payers alike. Furthermore, the exponential proliferation of affordable, high-fidelity personal smart devices and robust 5G infrastructure provides the technical backbone necessary for reliable data transmission and sophisticated application function, acting as a crucial enabling driver for mass market penetration.

Counterbalancing these drivers are significant Restraints that challenge the speed and breadth of adoption. A primary barrier remains the digital divide; a considerable segment of the elderly population lacks the requisite technical literacy or comfort level to utilize complex applications effectively, demanding substantial investment in intuitive UX/UI design and dedicated user training. Paramount concerns over data privacy and the security of highly sensitive personal health information (PHI) also restrict trust and adoption, necessitating continuous, costly compliance with evolving global regulations such as HIPAA, GDPR, and localized data residency laws. Moreover, the lack of standardized regulatory frameworks regarding the classification and approval of health apps across different countries complicates global market scaling and delays the introduction of clinically certified applications, particularly those seeking medical device status from regulatory bodies like the FDA or EMA.

The existing Restraints, however, simultaneously illuminate substantial Opportunities for innovative market players. The market offers rich potential in developing highly specialized applications targeting neglected areas, such as robust mental health support platforms utilizing remote teletherapy integrated with AI sentiment analysis, or highly tailored tools for specific complex conditions like Parkinson's or Multiple Sclerosis, leveraging motion tracking and personalized feedback loops. The expansion of governmental and private insurance reimbursement policies for Remote Patient Monitoring (RPM) services presents a crucial revenue stream opportunity, encouraging developers to invest in clinical validation and certification to qualify for these programs. Exploiting advanced integration capabilities, such as seamless connectivity with Electronic Health Record (EHR) systems used by institutional providers and integrating with smart home platforms, offers key pathways for establishing ecosystem dominance and achieving widespread, clinically validated deployment within the formal healthcare sector.

The Elderly Care Apps Market segmentation provides a strategic map of user needs and technological requirements, classified predominantly by the functional utility (Application Type), the delivery platform (Operating System and Deployment Model), and the primary beneficiary (End-User). The By Application Type segment is essential for understanding where consumer spending and clinical demand are focused, ranging from basic safety alerts to advanced holistic health management tools. This diversity requires developers to focus either on specialized excellence within a niche (e.g., dedicated medication adherence) or comprehensive platform development that integrates multiple functionalities to serve as an all-in-one care hub, reflecting a common strategic decision point in the market.

Analyzing the End-User segmentation reveals the purchasing power dynamics. While Seniors are the ultimate beneficiaries, the financial decision-making and daily operational interaction often reside with Informal Caregivers (family members), making robust communication, reporting, and ease-of-use critical features for this segment. Conversely, Institutional End-Users (Hospitals, Home Care Agencies) prioritize features related to enterprise management, regulatory compliance, scalability for large patient populations, and deep integration capabilities with existing clinical IT infrastructures. The Deployment Model segmentation, particularly the preference for Cloud-Based solutions, underscores the need for high availability, robust data security, and the ability to leverage central processing power for sophisticated AI analytics without relying solely on local device capacity, especially crucial for continuous remote monitoring services.

The comprehensive value chain for the Elderly Care Apps Market begins rigorously in the Upstream segment, dominated by key technology suppliers essential for the final product’s functionality. This phase involves the critical manufacturing and sourcing of high-precision biomedical sensors, microprocessors, and IoT hardware components that constitute wearable devices and smart home integration systems. Crucially, it also encompasses the development of operating system frameworks and specialized Software Development Kits (SDKs) provided by major tech players, alongside the provision of scalable and secure cloud infrastructure necessary for hosting voluminous Protected Health Information (PHI). Strategic decisions at this stage—such as selecting compliant cloud vendors (e.g., AWS, Azure with relevant health compliance certifications) and forming supply partnerships with reliable sensor manufacturers—directly influence the application’s potential for clinical accuracy and regulatory approval down the line.

The Midstream phase constitutes the core creation of value, focusing intensely on software engineering, application design, and clinical validation. Market participants invest heavily in developing proprietary algorithms, especially those leveraging AI/ML for predictive health scoring and pattern recognition, which constitute the intellectual property barrier to entry. This phase includes meticulous User Experience (UX) design focused on geriatric accessibility (large fonts, simple navigation, voice commands) and the critical process of regulatory compliance, ensuring the application adheres to global standards for medical software and data protection. Distribution channel optimization is also midstream activity, requiring nuanced strategies: Direct distribution through app stores relies on robust App Store Optimization (ASO) and digital marketing, while B2B distribution to hospitals mandates establishing sophisticated integration teams capable of linking the app platform seamlessly with complex Electronic Health Record (EHR) systems, often requiring high-level custom solutions and prolonged implementation periods.

The Downstream elements center on market reach, customer acquisition, deployment, and crucial post-sales support, determining long-term customer satisfaction and retention. This phase involves aggressive marketing campaigns targeted simultaneously at the elderly user and the key decision-makers—the caregivers and institutional purchasers. Deployment involves the physical installation and initial setup of connected devices in the home environment, often requiring specialized field support. Post-sales support is critical, involving 24/7 technical assistance and continuous software updates that introduce new features and maintain security integrity against evolving threats. The final stage of the value chain involves data feedback loops: capturing real-world usage data, clinical outcomes, and user feedback, which is then fed back into the upstream R&D segment, driving iterative product improvement and ensuring the application remains competitive, clinically relevant, and aligned with the shifting needs of the aging demographic and evolving healthcare regulatory landscape.

The identification of potential customers in the Elderly Care Apps market necessitates a layered approach, recognizing that the user (the senior) is often distinct from the economic purchaser and the primary operator (the caregiver or institution). The first core segment comprises the independent, tech-savvy senior—those who are comfortable with smartphones and proactively seek tools to maintain their active lifestyle, manage complex medication regimens, or engage in cognitive fitness programs. This segment demands high-quality, seamless application performance, and often opts for subscription models that include integrated wearable technology, focusing on applications that enhance their autonomy and provide immediate access to information without the need for constant family supervision.

The second, and commercially most influential, segment is the informal caregiver cohort, typically adult children managing the care of elderly parents or spouses. This group's purchasing decision is heavily influenced by reliability, robust emergency features (e.g., proven fall detection accuracy, GPS tracking), and comprehensive reporting capabilities. For these customers, the app serves as an essential oversight tool, offering peace of mind by providing real-time location data, adherence tracking, and secure communication channels to coordinate efforts with siblings or other extended family members. Applications marketed to this group must prioritize features that reduce caregiver burnout and streamline logistical complexities associated with decentralized care provision.

The third significant segment encompasses formal healthcare institutions, including large hospital networks, specialty geriatric centers, and vertically integrated Home Health Care (HHC) agencies. These institutional buyers acquire platform licenses to scale Remote Patient Monitoring (RPM) services, manage post-discharge care transitions, and satisfy regulatory requirements related to quality of care monitoring. Their focus is on enterprise-grade solutions that offer guaranteed interoperability with existing EHR systems, sophisticated data analytics for population health management, and verifiable clinical trial evidence demonstrating efficacy in reducing costly adverse events. Finally, government agencies and insurance payers represent an indirect yet critical customer group; while they may not directly download the app, their policies regarding telehealth reimbursement and preventative care funding heavily influence which apps are adopted and financially viable for mass deployment by providers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 15.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Koninklijke Philips N.V., Honor Technology, Inc., UnaliWear, Inc., CareZone, Inc., Rescu, Inc., Life360, Inc., AgeWell Global, Connective Touch, CuroGens, LLC, MedMinder Systems, Inc., Qardio, Inc., Wellthy, Inc., Silverline Technologies, Inc., K4Connect, Inc., True Link Financial, Inc., Birdsong, Inc., GrandPad, Inc., AARP, MobileHelp, AlertMe |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological framework supporting the Elderly Care Apps market is highly sophisticated, relying fundamentally on the seamless integration of miniaturized sensors, pervasive mobile connectivity, and advanced computational intelligence. Mobile Application Development remains the user interface cornerstone, demanding investment in universally accessible design principles (A11Y compliance), including simplified navigation, customizable text sizes, and comprehensive voice command functionality to accommodate varying levels of motor and cognitive decline typical in the user demographic. Crucially, the mobile app serves as the aggregator for data streams originating from the exponentially growing ecosystem of Internet of Things (IoT) devices, establishing a centralized, easy-to-interpret dashboard for both the senior and their care network.

The IoT and Wearables component is indispensable, encompassing medical-grade biosensors for continuous vital sign monitoring (e.g., continuous blood pressure, heart rate, oxygen saturation), non-contact environmental sensors (motion detection, bed occupancy sensors), and smart Personal Emergency Response Systems (PERS). These devices generate massive, continuous streams of raw data, necessitating reliable, low-latency transmission, increasingly facilitated by 5G wireless technology, which ensures real-time communication critical for emergency alerts and high-definition video consultations. This high volume of data is processed and stored exclusively in Cloud Computing environments, which must adhere to the highest international standards for healthcare data residency and compliance, providing the foundational scalability and remote access capabilities required for global deployment and multi-site institutional usage.

The cutting edge of the technology landscape is defined by the depth of integration of Artificial Intelligence (AI) and Machine Learning (ML). These analytical engines transform raw sensor data into actionable clinical intelligence, predicting potential health deterioration with far greater accuracy and speed than manual monitoring. AI algorithms analyze behavioral anomalies, predict adherence risks, and power advanced features like customized cognitive training programs and empathetic virtual companions utilizing Natural Language Processing (NLP). Finally, Cybersecurity must be treated as a primary technological necessity, not an afterthought. The reliance on end-to-end encryption, regular penetration testing, robust API security for EHR integration, and adherence to international regulatory frameworks (GDPR, HIPAA) ensures the confidentiality, integrity, and availability of sensitive patient data, maintaining the critical trust required for widespread clinical adoption.

Leading Elderly Care Apps utilize robust, multi-layered cybersecurity protocols essential for handling Protected Health Information (PHI). These include strict compliance with international regulations such as HIPAA (US) and GDPR (EU), mandatory end-to-end encryption for all data transmission, secure, access-controlled cloud storage, and deployment of multi-factor authentication methods. Furthermore, continuous security auditing and advanced anonymization techniques are standard practices to ensure maximum data privacy, integrity, and resilience against evolving cyber threats and data breaches.

AI is critically significant, acting as the primary technological differentiator by enabling true predictive and proactive care capabilities. AI algorithms analyze continuous, multi-source data streams from wearables and environmental sensors to establish individual health baselines, allowing them to detect subtle, statistically significant anomalies. This predictive capacity allows the apps to forecast risks such as falls, cardiac events, or potential medication non-adherence, thereby offering personalized, timely interventions that transition the app from a passive tracker to an essential, intelligent risk mitigation tool.

Coverage is expanding but highly variable based on geographic region and specific application functionality. In established markets like the US, Remote Patient Monitoring (RPM) and specific Chronic Care Management features integrated into these apps are increasingly eligible for coverage or reimbursement under Medicare and private insurance, provided the apps hold clinical certification and are utilized under a physician’s directive. Non-clinical applications focused on general wellness, communication, or cognitive games are usually accessed via direct, user-paid monthly or annual subscription fees.

The primary barriers to widespread adoption include the persistent digital literacy gap among older adults, significant technical apprehension, and resistance to adopting new technologies that are often perceived as complex or intrusive. Other constraints include the high initial cost of fully integrated smart home systems, lack of ubiquitous high-speed internet in certain demographics (particularly rural areas), and consumer mistrust related to the security and privacy of sensitive personal health data, necessitating simplified, highly accessible UX/UI design and targeted educational programs.

While the Monitoring and Safety segment currently holds the largest market share, the Health Management segment, particularly the sub-segment dedicated to Chronic Disease Management (CDM), is projected to drive the highest revenue growth. This acceleration is inevitable due to the global increase in age-related co-morbidities (e.g., cardiovascular disease, diabetes). Providers and payers prioritize CDM solutions that offer continuous vital sign tracking, medication optimization using AI, and automated reporting, proving their effectiveness in reducing expensive hospital readmissions and managing population health risks efficiently across large patient cohorts.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.