ID : MRU_ 434943 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

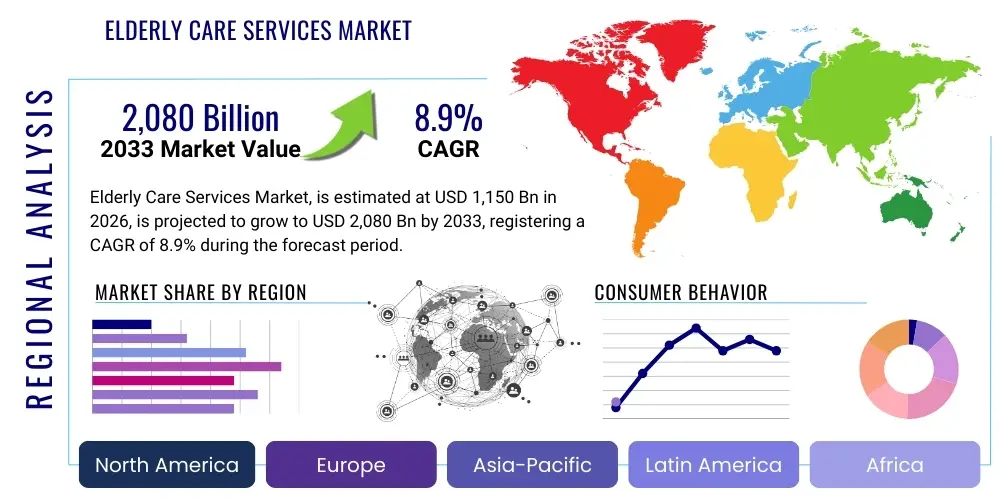

The Elderly Care Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2026 and 2033. This robust expansion is fueled primarily by the rapid aging of the global population, particularly in developed economies, coupled with significant advancements in healthcare technology that enable effective home-based care. The market is estimated at USD 1,150 Billion in 2026 and is projected to reach USD 2,080 Billion by the end of the forecast period in 2033, reflecting a sustained demand for personalized and high-quality geriatric care solutions.

The transition toward person-centered care models, emphasizing autonomy and quality of life for seniors, is a critical factor influencing market valuation. Increasing prevalence of chronic conditions, such as dementia, cardiovascular diseases, and diabetes, necessitates long-term specialized care, further driving service utilization. Furthermore, the rising awareness among families regarding the benefits of professional elderly care, including reduced caregiver burnout and better clinical outcomes, supports the sustained financial growth trajectory projected for the next decade.

The Elderly Care Services Market encompasses a wide array of support systems designed to meet the physical, emotional, and social needs of the aging population, generally defined as individuals aged 65 and above. This industry includes diverse service types, ranging from highly medicalized home health care and skilled nursing facilities to non-medical assistance such as adult daycare, custodial care, and respite services. The core objective of these services is to help seniors maintain independence, manage chronic illnesses effectively, and improve their overall quality of life, whether they reside in their own homes (aging in place) or in specialized institutional settings.

The major applications of elderly care services span across routine daily living assistance (ADLs) and complex clinical management. Key benefits include the provision of professional medical supervision, reduced hospitalization rates through preventative care, psychological support, and relief for family caregivers. The market is predominantly driven by the accelerating global demographic shift toward older populations, especially the 'oldest old' segment (80+), which requires intensive support. Additionally, increasing disposable incomes in emerging economies and favorable government policies promoting community-based care further propel market expansion. Technological integration, particularly telehealth and remote patient monitoring (RPM), is revolutionizing service delivery, enhancing efficiency, and expanding accessibility, thereby solidifying the market's long-term growth prospects.

Products within this sector are primarily services structured as bundled care packages, customized based on patient acuity and payer specifications. These packages often include medication management, physical therapy, nutritional support, and personal assistance. The shift towards value-based care models, which prioritize patient outcomes over volume of services, is significantly reshaping how these services are designed and delivered, placing a premium on integrated care coordination between various providers and technology platforms.

The Elderly Care Services Market is characterized by robust resilience and consistent expansion, largely insulated from typical economic volatility due to fundamental demographic imperatives. Key business trends indicate a definitive pivot toward technology-enabled services, with significant venture capital flowing into digital health platforms, remote monitoring solutions, and AI-driven predictive analytics that optimize staffing and patient safety. Consolidation among smaller, regional service providers by large national and international entities is accelerating, driven by the need for economies of scale, wider geographic coverage, and sophisticated IT infrastructure required for handling complex payer requirements and compliance standards. Furthermore, strategic partnerships between technology firms and traditional care providers are becoming essential for maintaining competitiveness and enhancing the service portfolio.

Regionally, North America maintains its dominance in terms of market value, primarily due to its highly sophisticated healthcare infrastructure, high prevalence of private insurance coverage, and early adoption of advanced geriatric technologies. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate, fueled by its immense and rapidly aging population base (particularly China and India), coupled with increasing public and private investments aimed at expanding essential care facilities and formalizing the previously fragmented caregiving structure. Europe presents a mixed landscape, characterized by strong government funding models but facing increasing strain due to escalating operational costs and acute workforce shortages, necessitating urgent shifts toward automated and efficiency-driven care models.

Segment trends highlight the sustained preference for Home Care Services (HCS), which consistently holds the largest market share. This preference is driven by lower cost compared to institutional settings, psychological benefits associated with ‘aging in place,’ and technological capabilities that make complex care delivery feasible at home. Within service type segmentation, the demand for non-medical assistance (e.g., companionship, help with daily activities) is growing rapidly alongside skilled nursing care, reflecting the multifaceted needs of the senior population. The increasing regulatory focus on quality metrics and patient satisfaction across all segments is compelling providers to invest heavily in staff training and continuous quality improvement programs to secure market viability.

User queries regarding AI's influence in the Elderly Care Services Market commonly revolve around the immediate benefits such as enhanced safety, personalized care plans, and reduced administrative burdens, contrasted with significant concerns regarding data privacy, technological equity across diverse socioeconomic groups, and the potential displacement of human caregivers. Users are intensely interested in how AI can provide predictive alerts for falls or sudden health deterioration (proactive care), thereby ensuring continuous monitoring without invading privacy. A core thematic expectation is that AI systems must act as effective force multipliers for scarce human staff, managing routine tasks like scheduling and data entry, rather than replacing the essential empathy and emotional support provided by caregivers. Furthermore, there is considerable skepticism regarding the feasibility and affordability of implementing complex AI solutions uniformly across residential and in-home care settings.

AI is profoundly transforming the Elderly Care Services market by automating administrative processes, enhancing clinical decision support, and enabling highly personalized preventative care. Machine learning algorithms analyze vast datasets—including vital signs, activity patterns, and electronic health records—to predict health crises, such as sepsis or imminent falls, allowing caregivers to intervene before emergencies occur. This shift from reactive to proactive care significantly improves patient outcomes and reduces overall healthcare expenditure, making services more sustainable. AI-powered diagnostic tools also assist geriatric specialists in accurately assessing cognitive decline and tailoring individualized therapy programs.

The integration of conversational AI (chatbots and voice assistants) is crucial for addressing the social isolation frequently experienced by seniors, providing interactive companionship, and managing medication reminders with high adherence rates. However, successful AI adoption relies on overcoming infrastructure challenges, particularly ensuring reliable internet connectivity in remote care settings, and addressing ethical concerns related to algorithmic bias and consent. Strategic investments are necessary to train the existing workforce on utilizing these tools effectively, ensuring AI acts as a complementary partner rather than a replacement for human interaction, thereby maintaining the quality and compassionate nature of elderly care.

The Elderly Care Services Market dynamics are heavily influenced by a potent blend of demographic pressures (Drivers), economic constraints (Restraints), and technological advancements (Opportunities), all interacting to shape the competitive and operational landscape. The foremost driver is the inexorable demographic shift, where the global 65+ population is expanding at an unprecedented rate, creating a baseline demand that far outstrips existing supply capacity. This is compounded by the increasing incidence of complex chronic diseases requiring continuous management, often favoring specialized elderly care settings over general hospitals. Economic factors like rising healthcare consumer expenditure, particularly in high-income nations, and expanding private insurance coverage are providing the necessary financial impetus for market growth and innovation.

However, market expansion is significantly restrained by acute, systemic challenges. The most critical constraint is the persistent global shortage of qualified caregivers (nurses, geriatric aides, and home health professionals), exacerbated by high turnover rates and intense physical/emotional demands of the profession. Furthermore, the high cost of institutional care, particularly in major urban centers, renders quality services inaccessible to large segments of the population, often leading to reliance on unpaid family care which strains the support system. Regulatory complexities, including varied licensing requirements and reimbursement uncertainties across different geographies and service types, also impose substantial operational barriers and limit cross-regional scalability for major providers.

Opportunities for market players are primarily concentrated in technological innovation and new service models. The proliferation of Telehealth and remote diagnostics offers a scalable solution to address geographical barriers and staff shortages, enabling remote monitoring and virtual consultations. The development of specialized niche services, such as palliative care, dementia care units, and geriatric mental health services, caters to specific high-need patient populations, yielding premium margins. Crucially, the move toward integrated care networks, where elderly care providers collaborate with primary care physicians and hospitals, enhances continuity of care, improves outcomes, and aligns with emerging value-based reimbursement frameworks, representing a significant long-term growth avenue.

The Elderly Care Services Market is segmented primarily based on Type of Service Delivery, Service Type, and Service Payment Method, offering a granular view of consumer preferences and operational structures. The dominance of the Home Care segment reflects the strong global trend toward ‘aging in place,’ where seniors prefer receiving personalized care in familiar settings, which is often more cost-effective than facility-based options. The segmentation highlights the critical division between skilled clinical services, which require licensed professionals (e.g., physical therapy, chronic disease management), and non-medical services, which focus on daily living assistance and emotional support. Analyzing these segments is crucial for providers to strategically allocate resources, design targeted service bundles, and align offerings with the most profitable payer channels.

The value chain for Elderly Care Services is complex, spanning from upstream technology development and staffing recruitment to downstream service delivery and final reimbursement. Upstream activities involve the procurement of critical resources, including medical equipment, IT infrastructure, and recruitment of qualified personnel. Technology developers, particularly those specializing in telehealth, RPM devices, and AI platforms, are vital upstream partners, supplying the tools necessary for efficient and scalable care delivery. Staffing agencies and educational institutions form the human resource base, constantly struggling to meet the escalating demand for skilled geriatric professionals, influencing operational capacity.

Core service delivery activities (midstream) include the assessment of patient needs, development of personalized care plans, and the physical execution of care (e.g., medication administration, ADL assistance). Effective care coordination and quality assurance protocols are central to maximizing value capture in this stage. Distribution channels are predominantly direct, involving providers interacting directly with patients and families (for home care) or managing facility operations (for institutional care). Indirect channels involve collaboration with intermediaries such as hospitals (referral networks), physician groups, and specialized case management firms that facilitate patient placement and transition between care settings.

Downstream value realization focuses on the payer entities—governments, insurance companies, and private individuals—who determine reimbursement rates and service utilization metrics. Efficiency in claims processing, coupled with demonstrating superior patient outcomes (value-based metrics), dictates financial success downstream. The market benefits significantly from robust integrated supply chain management that links technology vendors, staffing agencies, and service delivery points, ensuring continuous, high-quality care that meets stringent regulatory and consumer expectations.

The primary consumers and beneficiaries of the Elderly Care Services Market are highly segmented, including the elderly individuals themselves, their immediate family members who act as decision-makers and financial guarantors, and large institutional payers. Elderly individuals, particularly those over 80 requiring assistance with activities of daily living (ADLs) or suffering from cognitive decline, are the direct end-users. Their purchasing decisions are heavily influenced by the desire for autonomy, comfort, and clinical quality, often preferring customized in-home care over institutional settings when financially viable.

Family caregivers represent a crucial customer segment, often initiating the service search, managing logistics, and contributing financially. They seek services that provide reliability, professional expertise, and, critically, respite from the intense emotional and physical demands of caregiving. For this segment, ease of communication, transparency in care reporting, and flexible scheduling are paramount purchasing criteria. The third major group comprises the institutional buyers, specifically governmental health programs (like Medicare/Medicaid or NHS equivalents) and private long-term care insurance companies, which utilize these services to manage costs associated with acute care, reduce readmission rates, and improve population health outcomes, operating within stringent budget and quality constraints.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1,150 Billion |

| Market Forecast in 2033 | USD 2,080 Billion |

| Growth Rate | 8.9% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | LHC Group, Inc., Kindred Healthcare, LLC, Brookdale Senior Living Inc., Genesis HealthCare, Extendicare Inc., Senior Care Centers of America, Home Instead, Inc., Benesse Style Care Co., Ltd., Right at Home, LLC, Sunrise Senior Living, Atria Senior Living, Inc., Econ Healthcare Group, Healthcare at Home, Service Corporation International, The Ensign Group, Inc., Five Star Senior Living Inc., Senior Helpers, Comfort Keepers, Visiting Angels, ResCare, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Elderly Care Services market is undergoing a profound technological transformation, driven by the need to enhance efficiency, overcome staffing limitations, and improve remote oversight. The key technology landscape is dominated by the adoption of interconnected digital platforms. Telehealth and telemedicine solutions, including secure video consultation portals and remote diagnostic tools, enable geriatric specialists to monitor patients and conduct virtual visits, significantly reducing the need for non-essential travel and expanding access to specialized care, particularly in rural or remote areas. The integration of Internet of Things (IoT) sensors and wearable devices forms the backbone of remote patient monitoring (RPM), collecting continuous data on vital signs, mobility, and environmental factors, alerting caregivers to potential risks like dehydration or changes in routine.

Robotics and automation are emerging as vital components, primarily deployed for physical assistance (e.g., lift support, mobility aids) and companionship roles. Service robots can assist with medication dispensing, basic cleaning tasks, and provide social interaction to mitigate loneliness, though their penetration remains higher in institutional settings compared to home environments. Furthermore, Artificial Intelligence (AI) and Machine Learning (ML) are utilized not just for predictive risk analysis but also for optimizing operational logistics, such as sophisticated shift scheduling that matches caregiver skills to patient needs and geo-optimization of routes, resulting in significant cost efficiencies and improved resource allocation across large provider networks.

Finally, Electronic Health Records (EHR) and centralized care management software platforms are indispensable, ensuring seamless data exchange between the elderly care provider, primary care physicians, hospitals, and payers. These integrated systems are critical for maintaining compliance, facilitating complex billing requirements, and enabling data-driven decision-making regarding care quality and resource management. The convergence of these technologies—IoT, AI, and comprehensive digital platforms—is instrumental in supporting the complex operational requirements of value-based elderly care delivery.

The global Elderly Care Services market exhibits distinct regional dynamics driven by demographic factors, healthcare policies, and economic development levels. North America, encompassing the United States and Canada, currently holds the largest market share by value. This dominance is attributable to high per capita healthcare spending, advanced infrastructure supporting complex medical care, and strong consumer acceptance of private long-term care insurance. The U.S. market is highly fragmented but sophisticated, characterized by early adoption of technology like AI and telehealth, stringent regulatory oversight, and a robust private sector providing a spectrum of specialized services, particularly in assisted living and high-acuity home health care. The region faces escalating labor costs, driving aggressive investment in automation to mitigate wage pressure.

Europe represents a mature market, distinguished by diverse national healthcare systems, many of which are publicly funded. Countries in Western Europe, such as Germany, France, and the UK, have well-established, though increasingly strained, systems facing demographic pressure and sustainability issues due to rising pension and social care costs. The emphasis is heavily placed on subsidized home and community-based care to reduce dependence on expensive institutional services. Scandinavian countries often lead in integrating welfare services and utilizing technology for monitoring and independent living. Eastern Europe is generally catching up, constrained by lower public expenditure but rapidly growing private care offerings targeting affluent segments.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally, driven by the sheer scale and speed of its demographic transition—particularly the aging populations in Japan, China, and South Korea. Japan leads globally in addressing senior care needs through technology, especially robotics, due to its critical labor shortage. China and India are experiencing massive urbanization and the erosion of traditional, informal family care structures, necessitating rapid formalization and commercialization of elderly care. Government initiatives and massive infrastructural investment in developing dedicated senior living communities and expanding access to foundational services are key growth catalysts in APAC, despite pervasive challenges related to affordability and the quality gap between urban and rural services.

Latin America and the Middle East & Africa (MEA) are emerging markets characterized by lower current penetration rates but significant long-term potential. In Latin America, economic variability and limited public funding restrict wide-scale formal service adoption, leading to reliance on fragmented family care. However, private care services are expanding in metropolitan areas targeting expatriate communities and the rapidly growing middle class. In the MEA region, the market is highly nascent, with demand concentrated in wealthy Gulf Cooperation Council (GCC) states where specialized services are often imported to meet the needs of a small, high-net-worth senior population. Political stability and economic development are crucial prerequisites for the scalable formalization of elderly care services in these regions.

The primary driver is the accelerating global demographic transition, characterized by the exponential growth of the population segment aged 65 and above, which necessitates specialized long-term medical and non-medical support services.

Technology, particularly Telehealth and Remote Patient Monitoring (RPM), is highly significant as it enhances operational efficiency, mitigates the impact of staff shortages, expands geographic access to specialized care, and improves patient safety through proactive health monitoring.

The Home Care Services segment holds the largest market share. This dominance is driven by consumer preference for aging in place, coupled with the comparative cost-effectiveness and increasing technological capabilities of delivering complex care outside institutional settings.

The key restraints include severe, persistent shortages of qualified caregivers, resulting in increased labor costs and high staff turnover, alongside the substantial financial burden placed on families due to the rising costs of high-quality specialized care.

The Asia Pacific (APAC) region is projected to exhibit the fastest growth rate, fueled by its enormous aging population base, rapid urbanization dissolving traditional care models, and increasing governmental investment in formal elderly care infrastructure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.