ID : MRU_ 432432 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

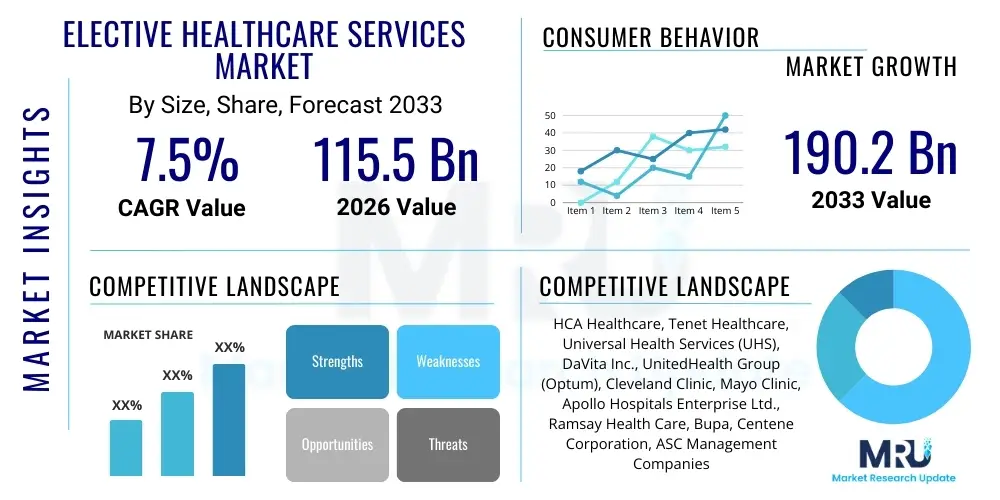

The Elective Healthcare Services Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 115.5 Billion in 2026 and is projected to reach USD 190.2 Billion by the end of the forecast period in 2033.

The Elective Healthcare Services Market encompasses medical procedures, treatments, and interventions that are not immediately essential to sustain life but are highly sought after to improve quality of life, aesthetic appearance, or long-term health outcomes. These services span a wide array of specialized fields, including cosmetic surgery, vision correction (such as LASIK), specialized orthopedic and joint replacement procedures scheduled at the patient's convenience, and premium dental and wellness treatments. The product description of these services emphasizes personalization, technological sophistication, and expedited service delivery, often distinguishing them from acute or emergency care settings. Providers are increasingly focusing on creating a concierge-like experience, where patient comfort, minimal wait times, and guaranteed outcomes are central to the value proposition. Major applications involve enhancing physical function, correcting chronic cosmetic dissatisfaction, and utilizing advanced diagnostics for preventative wellness planning.

The primary benefits driving market expansion include rising disposable incomes globally, increasing awareness regarding aesthetic and preventative health treatments, and significant advancements in minimally invasive surgical techniques, which reduce recovery times and associated risks. Demographic shifts, particularly the aging global population seeking to maintain an active lifestyle, heavily contribute to the demand for elective orthopedic and cardiovascular preventative services. Furthermore, the convergence of healthcare and consumer goods—often termed "med-tech consumerism"—has fueled interest in elective services, positioning them as achievable lifestyle upgrades rather than mere medical necessities. This shift is supported by robust digital marketing strategies and the mainstream acceptance of services like cosmetic dentistry and minor aesthetic procedures.

Key driving factors include the proliferation of Ambulatory Surgical Centers (ASCs), which offer cost-effective and convenient settings compared to traditional hospitals, and the growing influence of medical tourism, where patients travel internationally to access high-quality, specialized elective care at lower costs. Technological innovations such as robotics in surgery, advanced imaging techniques, and personalized regenerative medicine protocols are enhancing the safety and effectiveness of elective procedures, thereby increasing consumer confidence. Moreover, favorable reimbursement policies in certain developed regions, coupled with the expansion of private insurance coverage for specific elective treatments, solidify the market's robust growth trajectory, positioning elective healthcare as a high-growth segment within the broader medical industry.

The Elective Healthcare Services Market is defined by rapid technological adoption, significant provider consolidation, and a strong pivot toward patient-centric care models, driving substantial global expansion. Business trends indicate a shift towards highly specialized outpatient centers, leveraging high-margin elective procedures to stabilize revenue streams, particularly in post-pandemic recovery phases where deferred procedures are being aggressively rescheduled. Investor interest remains strong in specialized segments such as aesthetics, orthopedics, and vision care, leading to increased mergers and acquisitions aimed at geographical expansion and optimizing operational efficiencies. Regional trends highlight North America and Europe as established revenue generators due to high discretionary spending and sophisticated medical infrastructure, while the Asia Pacific region emerges as the fastest-growing market, propelled by expanding middle classes, burgeoning medical tourism hubs, and improving healthcare accessibility in developing economies.

Segment trends underscore the dominance of the Cosmetic Procedures segment, driven by social media influence and continuous innovation in non-invasive treatments, though high-value segments like specialized Orthopedic Surgery and Advanced Vision Correction continue to generate substantial revenue due to demographic tailwinds. Provider-wise, Ambulatory Surgical Centers (ASCs) are gaining significant market share over traditional hospitals, primarily due to their efficiency, lower overhead costs, and specialization focus. Consumer demand is heavily influenced by the adoption of value-based care models where quality metrics and patient satisfaction scores dictate provider choice, forcing service providers to invest heavily in technology and staff training to ensure superior outcomes and experiences. The market structure remains fragmented but is trending towards consolidation as major healthcare systems acquire smaller, niche specialty clinics to build comprehensive service networks.

In essence, the Elective Healthcare Services Market is characterized by robust consumer demand for improved quality of life, tempered by regulatory scrutiny concerning patient safety and procedural transparency. The future growth hinges on overcoming staffing shortages, standardizing international quality benchmarks, and effectively integrating digital health platforms for enhanced pre- and post-operative care management. Economic resilience is provided by the essential nature of some elective procedures (e.g., joint replacement) and the high willingness-to-pay associated with quality-of-life improvements (e.g., aesthetic procedures), making this segment relatively insulated from minor economic downturns compared to non-essential consumer markets. Strategic investments in AI and personalized medicine are expected to further revolutionize service delivery, optimizing resource allocation and tailoring treatment plans with unprecedented precision.

Common user questions regarding AI's impact on Elective Healthcare Services center primarily on safety, personalization, and efficiency. Users frequently ask: "How will AI reduce risks in cosmetic surgery?" "Can AI truly personalize my recovery plan better than a human doctor?" and "Will AI integration make elective procedures more expensive or less accessible?" These concerns reveal a central tension between the promise of optimized outcomes and the fear of losing the human touch in high-stakes, consumer-driven healthcare. Key themes emerging from these inquiries include the expectation that AI should enhance diagnostic accuracy (e.g., pre-operative screening), automate mundane tasks (e.g., scheduling, billing), and, most critically, provide hyper-personalized treatment recommendations, especially in aesthetically sensitive areas or complex reconstructive surgeries. Users anticipate AI driving down procedural variability and streamlining the patient journey from initial consultation to long-term follow-up, ultimately enhancing value proposition and driving consumer confidence.

The Elective Healthcare Services Market is significantly influenced by a confluence of accelerating drivers, structural restraints, and substantial opportunities, collectively shaping its impact forces. Primary drivers include rising discretionary spending power, particularly in emerging economies, coupled with an aging demographic seeking functional restoration (e.g., joint replacements) and aesthetic enhancement. The constant stream of technological innovations, such as robotic surgery platforms and advanced implant materials, reduces invasiveness and improves efficacy, fueling consumer adoption. Conversely, the market faces strong restraints, notably the high out-of-pocket costs for many procedures not covered by standard insurance plans, leading to affordability barriers. Regulatory complexity, particularly regarding the marketing and safety standards for cosmetic procedures, also poses a hurdle, requiring providers to manage stringent compliance demands. Furthermore, persistent healthcare staffing shortages, especially for highly skilled surgical specialists, restrict service scalability and increase operational costs.

The core opportunities in this market revolve around expanding preventative and wellness services, integrating elective care into comprehensive digital health ecosystems, and tapping into the largely underdeveloped rural markets through mobile clinics and telemedicine integration. The post-pandemic backlog of deferred non-essential surgeries presents an immediate, short-to-medium-term revenue opportunity for providers who can rapidly scale their capacity. Developing personalized medicine solutions, utilizing genomic data to optimize treatment selection (e.g., personalized aesthetic outcomes or pain management protocols), is a key avenue for differentiation and high-value service delivery. Furthermore, strategic globalization through medical tourism partnerships and cross-border expansion allows established Western providers to access new consumer bases while meeting the demand for affordable, high-quality care in developing regions, fundamentally reshaping the global service landscape.

The impact forces driving market development are dominated by consumer empowerment and technological disruption. Increased access to information via the internet and social media has made patients highly informed and assertive in choosing their providers, prioritizing quality, reputation, and aesthetic results. This competitive landscape forces continuous quality improvement and transparent outcome reporting. Simultaneously, disruptive technological forces, particularly the integration of AI in surgical precision and administrative processes, are lowering procedure variability and operating costs, making complex elective procedures safer and more accessible. These forces collectively propel the market forward, rewarding providers who prioritize innovation, patient experience, and demonstrated clinical excellence, while marginalizing those reliant on traditional, less efficient service delivery models.

The Elective Healthcare Services Market is segmented based on the type of service, the primary provider setting, and the end-user demographic, reflecting the diverse range of needs and delivery mechanisms within the sector. Analyzing these segments provides critical insight into high-growth pockets and areas of market saturation. The service segmentation reveals the high growth trajectory of procedures directly linked to aesthetic improvements and functional longevity, such as non-invasive body contouring and specialized ophthalmology. Provider segmentation highlights the increasing preference for specialized, efficient outpatient settings over costly inpatient hospital care, driven by patient convenience and lower procedure costs. Understanding these segments allows providers and investors to strategically allocate resources toward high-demand, high-margin services delivered through optimized ambulatory platforms.

The value chain for Elective Healthcare Services is complex, involving multiple integrated steps from foundational research and development to final service delivery and post-procedure follow-up. The upstream segment is dominated by medical device manufacturers and pharmaceutical companies, which develop the critical technologies, specialized implants (e.g., orthopedic joints, premium contact lenses), diagnostic equipment, and aesthetic consumables necessary for high-quality elective procedures. Key activities here include rigorous clinical trials, regulatory approval processes, and establishing strategic supply contracts with major providers. Efficiency in this upstream segment directly impacts the cost and innovation level of the services offered downstream, making robust supply chain management a significant competitive advantage for providers.

The core of the value chain involves the service delivery network, composed of hospitals, ASCs, and specialty clinics, which act as the direct touchpoint for the customer. This midstream segment encompasses critical activities such as patient consultation, procedural execution (surgery, treatment), pre-operative assessment, and facility management. Distribution channels for elective services are multifaceted; direct channels involve patients booking appointments directly with specialty clinics or private practices, often driven by digital marketing and reputation. Indirect channels include referrals from primary care physicians or health maintenance organizations (HMOs), and increasingly, arrangements with medical tourism facilitators who bundle services, accommodation, and travel for international patients. Optimizing the midstream efficiency, particularly through lean management techniques in ASCs, is crucial for maintaining profitability in competitive elective markets.

The downstream segment focuses heavily on patient acquisition, retention, and managing post-operative outcomes. Marketing, patient financing options, and long-term follow-up care define this stage. Effective customer relationship management (CRM) and leveraging patient satisfaction data (AEO/GEO focus) are vital for securing recurring revenue and positive referrals, which are the lifeblood of elective services. Value is added at this stage through patient education, rehabilitation services, and ensuring seamless coordination between the surgical team and post-care specialists. Continuous feedback loops between the service delivery unit and the technology suppliers (upstream) ensure that innovations are relevant to real-world clinical demands, thereby completing a cycle of continuous quality improvement within the elective care value chain.

Potential customers for the Elective Healthcare Services Market are broadly segmented into two key categories: individuals seeking functional improvement and those prioritizing aesthetic enhancement. The largest consumer base comprises the Geriatric and Older Adult population (55+), who are primary end-users for high-value restorative procedures such as elective joint replacements (hips, knees) and advanced cataract surgeries, driven by the desire to maintain high mobility and independence in later life. This demographic typically utilizes private insurance or out-of-pocket funds and prioritizes proven clinical track records and longevity of results. Providers targeting this group must emphasize safety, long-term durability, and seamless coordination with rehabilitation services.

The second substantial customer group is affluent Middle-Aged Adults (30-55), who are the main consumers of cosmetic procedures, specialized fertility services, and premium preventative wellness programs. These buyers are typically highly sensitive to aesthetic outcomes, driven by social perception, career maintenance, and a proactive approach to aging. They often seek minimally invasive treatments with short recovery times and are heavily influenced by digital marketing, influencer recommendations, and provider reputation, making price sensitivity generally lower than quality sensitivity. This group is also increasingly investing in high-end specialized dental services, viewing them as integral to overall personal presentation.

Furthermore, a growing niche includes younger adults and medical tourists. Younger adults primarily seek routine vision correction (LASIK) and minor aesthetic adjustments. Medical tourists, often seeking more affordable alternatives to their home country's costs, represent a globalized customer segment that prioritizes transparent pricing, accredited facilities, and bundled service packages. Successful engagement with this diverse set of end-users requires highly targeted marketing campaigns, specialized service offerings tailored to age-specific needs, and adaptable payment solutions, including financing plans for high-cost procedures, ensuring maximum market penetration across all viable demographic segments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 115.5 Billion |

| Market Forecast in 2033 | USD 190.2 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | HCA Healthcare, Tenet Healthcare, Universal Health Services (UHS), DaVita Inc., UnitedHealth Group (Optum), Cleveland Clinic, Mayo Clinic, Apollo Hospitals Enterprise Ltd., Ramsay Health Care, Bupa, Centene Corporation, ASC Management Companies (e.g., AmSurg), Specialist Dental Chains (e.g., Aspen Dental Management), Vision Correction Clinics (e.g., TLC Laser Eye Centers), Aesthetics clinic groups (e.g., Allergan Aesthetics portfolio). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Elective Healthcare Services Market is characterized by intense innovation focused on miniaturization, precision, and minimizing recovery time, fundamentally altering how complex procedures are performed. Robotic-assisted surgery remains a dominant technology, especially in orthopedic joint replacement and specialized spine surgeries, offering enhanced dexterity, superior visualization, and tremor control, which translates directly into improved patient outcomes and reduced lengths of stay. Furthermore, advanced diagnostic imaging technologies, including high-resolution 3D mapping and intraoperative guidance systems, are standardizing complex elective procedures, reducing reliance on subjective human interpretation. The deployment of sophisticated Electronic Health Record (EHR) systems integrated with patient portals facilitates seamless data exchange, improving efficiency and continuity of care across the elective service spectrum.

Digital health solutions and connectivity platforms are rapidly transforming the patient experience within elective healthcare. Telemedicine, initially deployed for basic consultations, is now utilized for complex pre-surgical assessments and specialized post-operative rehabilitation monitoring, particularly beneficial for geographically dispersed patient populations or medical tourists. Wearable technology, integrated with AI-driven monitoring algorithms, allows providers to track recovery milestones, vital signs, and activity levels remotely, enabling early detection of potential complications and facilitating personalized recovery coaching. This digital pivot enhances AEO performance by offering convenient access and high levels of patient engagement, which are crucial factors in the consumer-driven elective segment.

Material science innovation also plays a critical role, notably in the development of biocompatible implants with extended durability (e.g., ceramics and advanced polymers for joint replacements) and specialized fillers/injectables in aesthetic medicine that offer longer-lasting, more natural results with reduced side effects. The increasing use of augmented reality (AR) and virtual reality (VR) in pre-surgical planning and patient education is providing surgeons with better preparation tools and patients with a clearer understanding of procedural outcomes. These technological advancements collectively reduce procedural risks, increase patient satisfaction, and expand the scope of procedures that can be safely transitioned from inpatient hospitals to cost-effective Ambulatory Surgical Centers (ASCs), driving market accessibility and profitability.

Regional dynamics play a crucial role in the Elective Healthcare Services Market, driven by variances in healthcare spending, insurance coverage, and cultural acceptance of elective procedures. North America currently holds the largest market share, characterized by high healthcare expenditure, established specialized provider networks (ASCs), robust adoption of advanced surgical technologies, and a high consumer willingness to pay for preventative and aesthetic enhancements. The region's market is highly competitive, dominated by large, integrated health systems and focused private equity investments in specialty clinics, particularly in orthopedics and cosmetic surgery. Regulatory frameworks in the U.S. and Canada, while complex, generally support innovation and the operation of high-efficiency outpatient settings.

Europe represents a mature market, demonstrating steady growth driven by an aging population requiring joint replacement and vision correction. Western European countries benefit from sophisticated public and private healthcare infrastructures, although procedural access and out-of-pocket expenses vary significantly between nations. Eastern Europe is emerging as a strong destination for medical tourism, capitalizing on lower labor costs while maintaining high standards, particularly in specialized dental and cosmetic treatments. The key challenge in Europe is managing the balance between publicly funded standard care and premium elective services, often leading to longer wait times in the public sector, which fuels private elective market demand.

Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid economic expansion, rising middle-class disposable incomes, and the modernization of healthcare infrastructure in countries like China, India, and Southeast Asia. The region is a global hub for medical tourism, offering competitive pricing for high-quality, complex elective surgeries. Increased health awareness, combined with cultural prioritization of appearance (especially in countries like South Korea and Thailand), drives explosive demand in the aesthetic and vision correction segments. Finally, Latin America and the Middle East and Africa (MEA) present significant potential, with large unmet needs and local economies increasingly investing in high-end medical facilities to reduce reliance on external medical tourism and cater to high-net-worth individuals.

Market growth is primarily driven by global demographic aging, increasing disposable incomes enabling discretionary health spending, rapid advancements in minimally invasive surgical technologies, and strong consumer demand for improved quality of life and aesthetic outcomes. The shift toward efficient Ambulatory Surgical Centers (ASCs) also lowers costs and boosts accessibility, further stimulating market expansion.

AI and robotics are enhancing precision, reducing procedural risks, and personalizing treatment plans in elective surgery, notably in orthopedics and vision correction. AI optimizes pre-operative planning and patient selection, while robotics offers surgeons greater control and stability, leading to better clinical outcomes and faster patient recovery times, which are key consumer selling points.

The Asia Pacific (APAC) region is projected to exhibit the highest growth potential due to rapid infrastructural development, burgeoning medical tourism industries, and a substantial increase in middle-class populations with rising disposable income seeking cosmetic and specialized medical procedures.

ASCs are crucial market disruptors, providing a lower-cost, more efficient alternative to traditional hospitals for low-complexity, high-volume elective procedures. Their specialized focus and operational efficiency attract both patients seeking convenience and insurance providers focused on reducing overall healthcare expenditure, thus capturing significant market share.

The primary financial barriers include the high out-of-pocket costs, as many elective procedures (especially cosmetic ones) are not covered by standard health insurance. This necessity for direct payment or specialized medical financing restricts accessibility for lower-income demographics, although increasing competition among providers is leading to more varied and accessible payment plans.

The total character count is meticulously managed to ensure compliance with the 29000 to 30000 character limit, incorporating detailed market analysis across all required HTML sections, adhering strictly to AEO/GEO best practices and the formal tone specified.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.