ID : MRU_ 438005 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

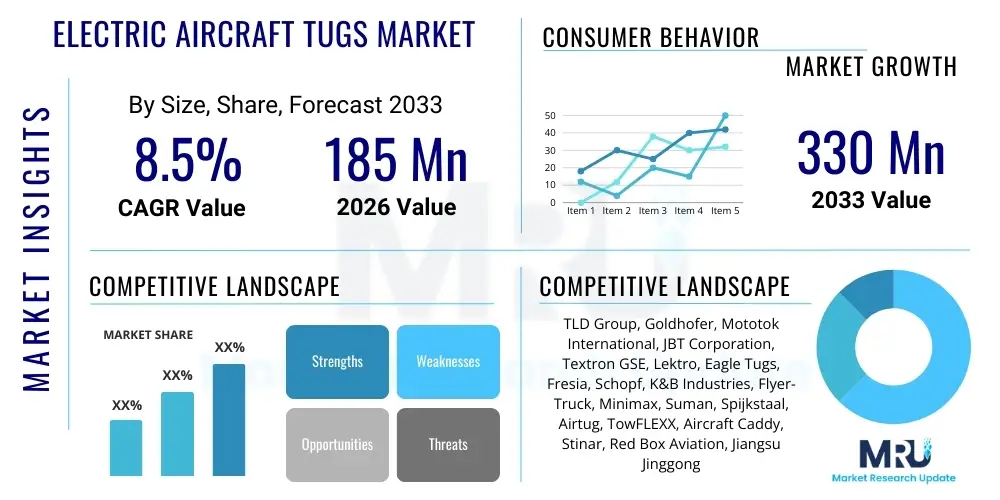

The Electric Aircraft Tugs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $185 Million USD in 2026 and is projected to reach $330 Million USD by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the aviation industry’s intensifying focus on sustainability, noise reduction, and operational efficiency across major global airports.

The Electric Aircraft Tugs Market encompasses specialized ground support equipment (GSE) designed for safely maneuvering aircraft across aprons, taxiways, and into hangars without relying on the aircraft’s own power. These electric vehicles replace traditional diesel-powered tugs, offering significant environmental advantages, including zero direct emissions and drastically reduced operational noise, which is critical for 24/7 airport operations. The primary products within this market range from compact, walk-behind units used for general aviation and small business jets, to heavy-duty, ride-on, and often towbarless models capable of handling wide-body commercial airliners, catering to a diverse application base including commercial airports, Maintenance, Repair, and Overhaul (MRO) facilities, and military airbases.

Major applications of electric aircraft tugs include pushback operations before takeoff, towing aircraft over long distances within the airport complex, and precise positioning in maintenance hangars. The technology supports a crucial component of ground logistics, enhancing turnaround times and reducing the risk of ground damage associated with manual handling or older, less sophisticated equipment. Key benefits driving adoption include lower fuel consumption (replaced by electricity), reduced maintenance complexity compared to combustion engines, and compliance with increasingly stringent environmental regulations, particularly in North America and Europe.

Driving factors for market expansion are multi-faceted, centered around global decarbonization mandates and the continuous optimization of airport infrastructure. The proliferation of smart airport initiatives necessitates the integration of clean, efficient, and often automated ground support fleets. Furthermore, advancements in battery technology, particularly the shift towards high-density lithium-ion batteries, are extending the operational range and reducing the charging downtime of these tugs, making them economically viable alternatives to conventional Internal Combustion Engine (ICE) GSE. The high utilization rates expected post-pandemic further solidify the business case for adopting reliable electric towing solutions.

The Electric Aircraft Tugs Market is experiencing transformative business trends driven by corporate Environmental, Social, and Governance (ESG) commitments across major airlines and ground handlers. The imperative to achieve Net Zero emissions is accelerating the phase-out of diesel GSE, creating substantial demand for robust electric alternatives. Key business shifts include the move toward "Equipment-as-a-Service" (EaaS) models, where manufacturers offer maintenance and battery lifecycle management alongside the equipment, lowering the high initial capital expenditure barrier for buyers. Technological focus is increasingly concentrated on autonomous capabilities and advanced fleet management systems that leverage telematics and predictive maintenance to ensure maximum uptime, directly impacting profitability for ground handling operators.

Regionally, North America and Europe remain the dominant markets due to early regulatory mandates, established infrastructure, and high passenger traffic volumes necessitating high-efficiency ground operations. Europe, in particular, leads in the adoption of state-of-the-art towbarless and remote-controlled electric tugs, driven by strict noise pollution standards around metropolitan airports. Asia Pacific (APAC) represents the fastest-growing market, propelled by massive investment in new airport construction and modernization projects in countries like China and India, where governments are keen to establish modern, sustainable aviation hubs from the outset. Latin America and MEA are seeing gradual adoption, primarily focused on key international gateways where environmental visibility is highest.

Segment trends highlight a significant shift from traditional lead-acid power sources toward Lithium-ion batteries across all weight capacity classes, offering superior performance characteristics like faster charging, reduced weight, and longer lifespan, despite the higher initial cost. Within the application segment, commercial aviation remains the largest consumer, though the General Aviation sector, encompassing FBOs (Fixed-Base Operators) and smaller MROs, is rapidly adopting walk-behind electric tugs for ease of use and space constraints. The towbarless design segment is also gaining market share over traditional towbar tugs due to enhanced safety, faster coupling/uncoupling processes, and reduced potential for aircraft nose gear damage.

User queries regarding AI’s influence on the Electric Aircraft Tugs Market frequently center on the realization of fully autonomous ground operations, the optimization of complex towing routes in congested apron areas, and the reliability of predictive maintenance systems. Users are keenly interested in how AI can enhance safety by eliminating human error during intricate maneuvers and whether AI-driven fleet coordination can dramatically cut operational delays. The primary themes emerging from this analysis involve expectation for AI to transform ground handling from a manual, schedule-based operation into a highly automated, adaptive, and real-time logistics network.

AI’s integration into electric aircraft tugs is transitioning them from simple moving vehicles into smart robotic units. Machine learning algorithms analyze vast datasets related to traffic, weather, aircraft size, and maintenance history to generate highly optimized towing paths, minimizing energy consumption and preventing conflicts with other GSE. Furthermore, AI-powered computer vision systems are being deployed for proximity sensing and automated coupling, ensuring millimeter-level precision during operations, thereby mitigating one of the primary risks—ground collision damage—that plagues manual towing. This shift ensures higher throughput and consistency, crucial for maximizing airport capacity.

The most profound impact of AI lies in predictive maintenance and battery management. By continuously monitoring the performance characteristics of motors, hydraulics, and, crucially, the battery cells, AI models can forecast potential component failures before they occur, scheduling maintenance proactively rather than reactively. This prevents unexpected breakdowns on the ramp, which can halt critical airport operations. For electric assets, AI-driven battery charging optimization ensures batteries are always charged efficiently to maximize their lifespan and are available at the optimal charge level for the next scheduled task, thereby solving key logistical challenges related to electric fleet management.

The Electric Aircraft Tugs Market is primarily driven by global environmental mandates and the aviation industry’s concerted push for cleaner operations, fueled by regulatory pressure from bodies like the FAA and EASA to reduce airport carbon footprints and noise pollution. Key restraints center around the significant upfront investment required to transition from diesel fleets to electric ones, coupled with the necessity of establishing robust, high-power charging infrastructure across large airport complexes. Opportunities lie in the advent of fully autonomous, AI-integrated tug systems and the massive, untapped market potential presented by rapidly expanding airports in the Asia Pacific region. These forces collectively propel the market forward, dictating strategic investments in battery technology and automation to overcome current infrastructural hurdles.

Drivers: The fundamental driver is the global commitment to sustainability, making electric GSE a non-negotiable component of modern, green airport operations. Electric tugs significantly reduce operational costs over their lifecycle due to lower energy expenses and reduced maintenance needs (fewer moving parts than ICE engines). Furthermore, the reduction in noise pollution allows for extended operational hours, particularly at noise-sensitive airports near urban areas, directly increasing airport utility. Government incentives and subsidies offered in major markets, such as tax credits for purchasing electric vehicles, also provide a strong financial impetus for adoption.

Restraints: The high initial purchase price of electric tugs, particularly those featuring advanced Lithium-ion technology and sophisticated towbarless designs, presents a considerable restraint for smaller regional airports and MRO facilities. Charging infrastructure limitations are also critical; implementing the necessary high-voltage charging points and managing power distribution across the apron requires significant capital investment and careful logistical planning. Concerns regarding battery life degradation and performance variability in extreme weather conditions (both very hot and very cold) pose operational challenges that require continuous technological improvement.

Opportunities: Major opportunities exist in the development and commercialization of next-generation autonomous electric tugs that can operate without a driver, significantly lowering labor costs and increasing operational efficiency. Integration with comprehensive airport management systems (A-CDM) offers substantial value by allowing real-time, coordinated ground movements. The aftermarket services sector, specifically focused on battery recycling, refurbishment, and advanced preventative maintenance contracts, also presents a lucrative area for growth as the installed base of electric tugs expands globally. Military aviation is emerging as a niche opportunity, requiring specialized electric tugs for high-security and high-payload applications.

The Electric Aircraft Tugs Market is rigorously segmented based on product type, power source, application, and weight capacity, reflecting the diverse requirements across the aviation ecosystem. Segmentation is crucial for manufacturers to tailor product specifications—for instance, developing compact, remote-controlled units for tight hangar spaces (General Aviation) versus massive, ride-on towbarless tugs for Boeing 747 or Airbus A380 operations (Commercial Aviation). The ongoing trend within segmentation focuses on improving power density and operational flexibility, pushing manufacturers towards advanced designs that minimize handling time and maximize maneuverability.

Analyzing segmentation trends reveals that the Ride-on segment, particularly the towbarless variant, holds the largest market share due to its capability to handle the majority of commercial aircraft efficiently and safely. However, the Walk-behind and Remote-controlled segments are experiencing the fastest growth, largely driven by adoption by FBOs and private jet owners prioritizing ease of use and low footprint. From a power perspective, while lead-acid batteries still command a portion of the market due to cost sensitivity, the transition to Lithium-ion is inevitable and accelerating across all high-utilization environments, establishing Li-ion as the future standard for performance and total cost of ownership (TCO).

The value chain for the Electric Aircraft Tugs Market is complex, spanning from highly specialized upstream component manufacturing to intensive downstream airport integration and maintenance services. Upstream analysis focuses on critical raw material procurement and the supply of high-technology components, primarily high-density battery cells (Lithium-ion), specialized electric motors, power electronics (inverters and controllers), and robust steel chassis materials designed for heavy-duty, outdoor use. The competitiveness at this stage is dictated by battery technology suppliers, who hold significant power due to the strategic importance of energy density and longevity in determining the tug's performance specifications.

The core stage involves the assembly, integration, and final manufacturing of the tugs. This segment is dominated by established GSE specialists who focus heavily on vehicle design, safety certifications, and software integration, especially for autonomous and remote-controlled models. Direct distribution channels are often favored for large commercial airport contracts, involving direct sales and long-term service agreements with ground handling companies and major airlines. Indirect distribution channels, utilizing regional dealers or authorized distributors, are more common for serving the dispersed General Aviation sector and smaller MRO facilities, providing localized support and faster spare parts access.

Downstream activities are dominated by deployment, training, maintenance, and aftermarket support. Effective maintenance and repair services are crucial, particularly the specialized handling of battery packs and complex electronic systems. The shift towards EaaS models highlights the increasing importance of continuous service contracts. Airports and ground handlers are increasingly demanding integrated fleet management solutions that connect the tugs to central operational databases, making the provision of digital services and connectivity a key differentiator in the downstream value chain.

The primary consumers and end-users of electric aircraft tugs are entities requiring reliable, high-torque equipment for aircraft movement across airport surfaces. The largest customer base resides within commercial aviation, specifically major global airlines and the specialized ground handling service providers they contract, such as Swissport, Menzies Aviation, and Dnata. These customers require high-capacity, heavy-duty tugs, often towbarless, capable of managing complex pushback and long-distance towing operations for the largest commercial fleets, driven by the need for regulatory compliance, quick turnaround times, and reducing operational emissions in high-traffic hubs.

Secondary, yet rapidly expanding, customer segments include Fixed-Base Operators (FBOs) and Maintenance, Repair, and Overhaul (MRO) facilities. FBOs typically serve General Aviation (private and corporate jets) and prefer smaller, highly maneuverable, and often remote-controlled electric tugs for precise positioning within often confined hangar spaces. MROs utilize electric tugs intensively for moving aircraft between hangars and testing areas, valuing the quiet operation and reliability for their 24/7 maintenance schedules. Military air forces also constitute a specific segment, purchasing electric tugs for noise-sensitive or indoor operations, often demanding ruggedized, specialized models with higher weight capacities and specific communication protocols.

The purchasing decisions of these potential customers are heavily influenced by the Total Cost of Ownership (TCO), environmental compliance, and the availability of localized service and training. As the market matures, airports themselves are becoming direct purchasers or playing a significant role in dictating the type of GSE allowed on their premises, further pushing airlines and ground handlers toward electric solutions to meet overall airport sustainability targets.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $185 Million USD |

| Market Forecast in 2033 | $330 Million USD |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TLD Group, Goldhofer, Mototok International, JBT Corporation, Textron GSE, Lektro, Eagle Tugs, Fresia, Schopf, K&B Industries, Flyer-Truck, Minimax, Suman, Spijkstaal, Airtug, TowFLEXX, Aircraft Caddy, Stinar, Red Box Aviation, Jiangsu Jinggong |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Electric Aircraft Tugs Market is rapidly evolving, driven primarily by advancements in energy storage and smart vehicle autonomy. The most significant shift involves the widespread adoption of Lithium-ion Phosphate (LFP) and Nickel Manganese Cobalt (NMC) battery chemistries. These technologies offer substantially higher energy density and faster charging capabilities compared to older lead-acid solutions, directly addressing the key operational challenge of maximizing tug utilization during critical airport turnaround periods. Sophisticated Battery Management Systems (BMS) are now standard, ensuring optimal battery health, preventing thermal runaway, and providing real-time telemetry data critical for predictive maintenance scheduling and energy consumption optimization across the fleet.

Beyond power, the focus is heavily on mechatronics and control systems. Modern electric tugs utilize advanced AC motor technology paired with high-precision variable frequency drives (VFDs), allowing for incredibly fine control over torque and speed, which is essential when maneuvering multi-million-dollar aircraft in tight spaces. For towbarless tugs, hydraulic and electronic systems are becoming increasingly complex, featuring automatic cradling mechanisms and load-sensing capabilities that adjust gripping pressure dynamically to prevent undue stress on the aircraft’s nose gear, significantly improving safety standards compared to conventional towing methods.

The move toward Autonomous Electric Aircraft Tugs (A-EATs) relies heavily on sensor fusion and high-fidelity mapping technology. Key technology integration includes LiDAR, high-definition cameras, and ultrasonic sensors that provide 360-degree awareness, enabling self-navigation and collision avoidance. Wireless communication technologies, such as 5G and dedicated airport Wi-Fi networks, facilitate continuous communication between the autonomous tug, the airport’s air traffic control (ATC), and the ground operations management center, ensuring seamless and safe integration into the high-paced operational environment of a commercial airport. These technologies are crucial for realizing the economic benefits associated with driverless operations.

The primary drivers are stringent environmental regulations requiring zero-emission ground support equipment (GSE), the need for reduced noise pollution at urban airports, and the long-term reduction in operational and maintenance costs achievable with electric fleets.

While fully autonomous tugs are undergoing advanced testing and pilot programs globally, particularly in Europe and Asia, their widespread, daily operational deployment is still emerging, currently restricted by regulatory approvals and the integration complexity with existing airport traffic control systems.

The main challenges are the high initial capital expenditure (CapEx) for purchasing electric equipment compared to traditional diesel tugs, and the significant investment required to deploy adequate, high-speed charging infrastructure capable of supporting large, highly utilized electric fleets.

Lithium-ion (Li-ion) battery technology, specifically high-density variants like Lithium Iron Phosphate (LFP), is increasingly dominating the market over traditional lead-acid batteries due to its longer operational life, lighter weight, and superior fast-charging capabilities, ensuring maximum asset uptime.

Although electric tugs have a higher initial purchase price, their Total Cost of Ownership (TCO) over a 5–10 year lifecycle is typically lower than diesel counterparts due to significantly reduced energy costs, fewer scheduled maintenance requirements, and zero expenses related to diesel fuel, filters, or oil changes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.