ID : MRU_ 433336 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

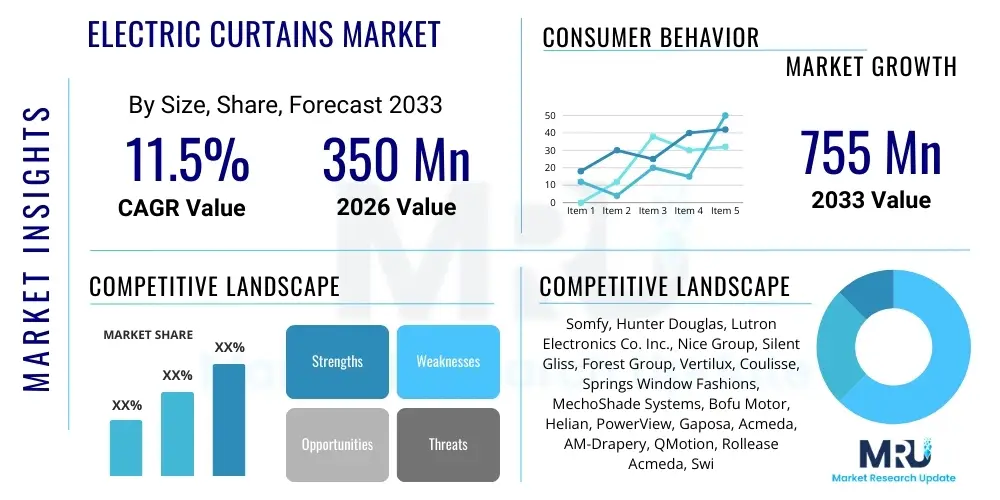

The Electric Curtains Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 755 Million by the end of the forecast period in 2033. This robust expansion is fueled primarily by the accelerating adoption of smart home technologies globally, coupled with increasing consumer emphasis on energy efficiency and interior design automation.

The Electric Curtains Market encompasses the manufacturing, distribution, and utilization of automated window coverings, which are controlled electronically via remote controls, wall switches, sensors, or integrated smart home systems. These products, often categorized as smart shading solutions, include motorized draperies, roller blinds, Roman shades, and Venetian blinds, all designed to operate seamlessly and silently. The core product incorporates a low-voltage motor system integrated into the curtain track or headrail, enabling programmed or remote operation. Major applications span both residential settings, where they enhance convenience, privacy, and ambiance, and commercial environments, particularly in luxury hospitality, corporate offices, and healthcare facilities, where climate control and efficient light management are critical. Key benefits derived from these systems include enhanced energy conservation by managing solar heat gain, superior security features through 'away-from-home' simulation, improved accessibility, and seamless integration with broader building management systems (BMS). Driving factors for market growth include rising disposable incomes, rapid urbanization leading to increased investment in modern housing infrastructure, and the continuous technological advancements in Internet of Things (IoT) devices, making electric curtain systems more affordable and easier to install and operate.

The Electric Curtains Market is undergoing significant transformation, driven by robust business trends emphasizing interconnectedness, sustainability, and aesthetic customization. The primary business trend involves strategic partnerships between traditional window covering manufacturers and technology companies to develop sophisticated, AI-enabled control platforms that offer predictive scheduling based on weather data and occupant behavior. Furthermore, direct-to-consumer sales channels leveraging augmented reality visualization tools are gaining traction, allowing consumers to simulate installations before purchase, thus streamlining the sales process. Regionally, North America and Europe currently dominate the market due to high penetration rates of smart home devices and stringent energy efficiency regulations in commercial buildings. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest growth CAGR, propelled by massive residential construction projects, particularly in China and India, and the rising middle-class propensity for luxury home automation solutions. Segment trends indicate that the Wi-Fi and Bluetooth technology segments are experiencing rapid growth in the residential sector due to ease of integration, while Z-Wave and proprietary RF protocols remain dominant in large commercial installations requiring enhanced stability and mesh networking capabilities. Regarding product type, roller blinds are anticipated to lead the market share due to their sleek profile, versatility, and cost-effectiveness in both residential and corporate settings, highlighting a shift towards minimalist interior design aesthetics.

The integration of Artificial Intelligence (AI) into the Electric Curtains Market is a central concern for users, primarily revolving around the expectation of true autonomy, seamless interoperability, and enhanced energy savings. Common user questions focus on how AI algorithms can move beyond simple scheduled operation to genuinely predict user needs and environmental shifts. Users frequently inquire about the feasibility of systems learning specific behaviors—such as automatically adjusting shading to prevent screen glare during typical work hours or optimizing indoor temperature profiles while maintaining required lighting levels. Concerns also surface regarding data privacy related to behavioral pattern tracking and the security risks inherent in connecting advanced motorized systems to the wider IoT ecosystem. Furthermore, there is considerable interest in AI’s ability to facilitate predictive maintenance by monitoring motor strain and battery life, thereby pre-empting component failure and ensuring system longevity. The expectation is that AI will transform electric curtains from reactive automation tools into proactive environmental management systems, contributing meaningfully to overall home efficiency and comfort without explicit user intervention.

AI’s influence is moving the market toward truly context-aware shading solutions. These systems utilize machine learning models trained on inputs from indoor climate sensors, external weather forecasts, and time-of-day data to make instantaneous, optimized adjustments. For instance, in a commercial office building, AI can synchronize curtain movements with HVAC systems to minimize the cooling load during peak sun hours, leading to significant measurable reductions in operational energy expenditure. This shift mandates that manufacturers standardize data exchange protocols and ensure robust cybersecurity frameworks to handle the sensitive data collected by these advanced smart shading devices. The core value proposition of AI is shifting from mere convenience to providing measurable Return on Investment (ROI) through sophisticated energy management.

The development of edge computing capabilities is also critical, allowing AI processing to occur locally within the curtain motor or hub, enhancing reaction speed and mitigating dependence on cloud infrastructure for routine operations. This distributed intelligence is paramount for maintaining system reliability and addressing latency issues common in purely cloud-based systems. Manufacturers are strategically embedding specialized AI chips designed for low-power operation, enabling the electric curtain system to function as an independent, intelligent subsystem within the larger smart home architecture, focused purely on optimizing the visual and thermal environment for occupants.

The Electric Curtains Market dynamic is shaped by a confluence of influential factors, categorized as Drivers, Restraints, and Opportunities (DRO), collectively forming the impact forces that dictate market trajectory. Key drivers include the exponential growth in global smart home adoption, driven by the desire for enhanced convenience, and the increasing global emphasis on sustainable building practices which favor automated window coverings for thermal regulation and energy saving. Furthermore, the aesthetic appeal and luxury status associated with motorized solutions fuel demand in high-end residential and premium commercial segments. However, the market faces significant restraints, primarily stemming from the high initial installation cost compared to manual systems, which acts as a barrier to entry for budget-sensitive consumers. The complexity of installation and integration, requiring specialized wiring or technical expertise, further hinders widespread DIY adoption. Opportunities abound in the realm of technological advancement, specifically the integration of advanced sensors (light, temperature, occupancy) and the development of cost-effective, wireless, and battery-powered systems that simplify retrofitting and broaden consumer access. The market is also heavily impacted by the rapid obsolescence cycle of smart home communication protocols and consumer preferences shifting towards universally compatible and robust connectivity standards.

Market forces are exerting pressure on pricing and standardization. The commoditization of DC motor technology is gradually reducing manufacturing costs, pressuring established players to innovate in control software and materials science rather than hardware alone. Simultaneously, governmental regulations in developed economies promoting green building certifications (like LEED) act as powerful external drivers, making automated shading a mandatory consideration in new commercial construction. The lack of universal interoperability remains a strong negative force; consumers frequently cite integration headaches when combining products from different manufacturers, thus incentivizing companies that offer comprehensive, single-platform solutions.

The opportunities presented by emerging markets in Southeast Asia and Latin America represent a critical growth lever. As infrastructure development accelerates and urbanization continues, these regions offer untapped potential for both new construction and smart retrofitting projects. Focusing on developing region-specific distribution channels and offering localized support for complex installations are crucial strategies for maximizing penetration. Furthermore, the development of solar-powered motor options offers a compelling environmentally friendly opportunity, addressing both sustainability concerns and simplifying the installation process by eliminating the need for complex electrical wiring near windows.

The Electric Curtains Market is comprehensively segmented based on various technical and functional parameters, including product type, technology, end-user application, and distribution channel. This granular segmentation provides stakeholders with detailed insights into specific niche markets driving current growth and those poised for future expansion. The segmentation highlights the diverse needs of both the residential and commercial sectors, which demand distinctly different features—residential users prioritize aesthetic integration, quiet operation, and ease of use, while commercial entities focus on durability, network stability, and centralized control systems capable of managing thousands of units simultaneously. Analyzing these segments is essential for product development roadmaps and targeted marketing strategies, ensuring that manufacturing efforts align with the most profitable and rapidly evolving consumer preferences.

Detailed analysis of the technology segment reveals a continuing battle between proprietary RF standards, which offer reliability and range (often preferred in high-end projects), and open standards like Wi-Fi and Bluetooth, which benefit from ubiquity and lower hardware costs. The transition toward Matter and Thread protocols is expected to revolutionize interoperability across all segments, potentially blurring the current technological distinctions. Geographically, segmentation helps identify areas where specific product types dominate; for example, roller blinds are overwhelmingly popular in Asia-Pacific commercial centers due to architectural style, whereas drapes and Roman shades maintain a strong foothold in traditional North American and European residential markets, driven by established interior design trends and material preference.

The value chain of the Electric Curtains Market is complex, stretching from raw material sourcing and motor manufacturing to final installation and aftermarket service, involving multiple specialized actors. Upstream analysis focuses predominantly on the suppliers of core components: specialized fabric manufacturers (providing fire-retardant, UV-resistant, or blackout materials), motor producers (offering highly reliable, low-noise DC or stepper motors), and electronic component suppliers (for control chips, PCBs, and communication modules). The quality and reliability of these upstream components—particularly the motors, which represent the highest cost component—are critical determinants of the final product's market performance and brand reputation. Manufacturers often engage in strategic, long-term contracts with motor suppliers to ensure consistent quality and scale, while fabric sourcing is often decentralized to leverage global price efficiencies and maintain supply chain resilience against geopolitical disruptions.

Midstream activities involve the primary manufacturing, assembly, and integration processes. This includes custom fabrication of the curtain tracks, integrating the motor and control electronics, and assembling the fabric or blind materials. Customization is a key feature in this stage, as electric curtains are often tailored to specific window dimensions and end-user aesthetic requirements. Companies that possess advanced automation in their assembly lines and maintain strict quality control standards for noise reduction and motor longevity gain a significant competitive advantage. Research and development activities, focusing on miniaturization, battery life extension, and creating intuitive user interfaces for the control hubs, are also concentrated heavily in this phase, representing a substantial investment for market leaders.

Downstream analysis covers the distribution channels, sales, and installation services. Distribution occurs through two main avenues: direct and indirect. Direct sales involve manufacturers selling directly to large commercial contractors or through proprietary e-commerce platforms. Indirect channels rely heavily on a network of authorized dealers, custom integrators, interior designers, and traditional retail partners. Given the technical nature of electric curtain systems, specialized integrators who can handle wiring, network configuration, and smart home system integration are crucial for customer satisfaction, particularly in the premium residential and complex commercial segments. Aftermarket services, including maintenance contracts and software updates, form an increasingly important part of the value chain, ensuring long-term customer loyalty and recurring revenue streams for manufacturers.

The potential customer base for the Electric Curtains Market is segmented into two major categories: the Residential Sector and the Commercial Sector, each possessing distinct purchase motivations and system requirements. Within the Residential Sector, potential customers include high-net-worth individuals investing in luxury or custom-built homes where integrated automation is standard, as well as middle-class homeowners seeking convenience, enhanced security, and energy savings through retrofitting. Key decision-makers in this segment are often the homeowners themselves, influenced by interior designers, architects, and home automation consultants. Residential purchases prioritize quiet operation, aesthetic appeal (hidden motors and seamless integration), and compatibility with major consumer smart home platforms like Amazon Alexa, Google Home, and Apple HomeKit. The growth in this segment is strongly correlated with disposable income levels and the overall adoption rate of IoT devices in the household.

The Commercial Sector represents an equally significant, and often higher volume, buyer segment. This includes major hospitality chains (hotels and resorts), corporate developers commissioning smart office buildings, and healthcare facility operators. In the commercial sphere, the motivation shifts towards operational efficiency, strict energy compliance, and maximizing tenant or guest comfort. Decision-makers are typically facility managers, procurement officers, or general contractors. Their requirements center on centralized control through Building Management Systems (BMS), robust network reliability (often favoring wired or specific proprietary mesh networks), system scalability, and proven durability capable of continuous heavy use. Hotels, for example, rely on electric curtains to elevate the guest experience and simplify room management, while corporate offices utilize automated shading to control ambient light and reduce HVAC load, contributing directly to operational cost savings and achieving green building certifications.

A burgeoning third segment comprises Institutional and Educational facilities, which are increasingly investing in automated systems to manage daylight harvesting in large lecture halls and administrative areas. These buyers prioritize systems that offer robust timers, simplified scheduling, and low maintenance requirements. Additionally, niche markets focused on elderly or disabled individuals, where accessibility and remote operation of window coverings are necessities, represent an important subset of potential customers. Manufacturers must tailor their product offerings, sales narratives, and distribution channels to address the specific technical demands and value propositions required by each of these distinct customer groups.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 755 Million |

| Growth Rate | CAGR 11.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Somfy, Hunter Douglas, Lutron Electronics Co. Inc., Nice Group, Silent Gliss, Forest Group, Vertilux, Coulisse, Springs Window Fashions, MechoShade Systems, Bofu Motor, Helian, PowerView, Gaposa, Acmeda, AM-Drapery, QMotion, Rollease Acmeda, SwitchBot, Ryterna. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Electric Curtains Market is defined by continuous innovation in motor efficiency, communication protocols, and sensor integration, aiming for seamless automation and minimal power consumption. At the core are the motorized systems, predominantly using low-voltage DC motors (12V or 24V), favored over AC motors for their superior quietness, precise speed control, and ease of integration with battery backup systems. Key advancements include brushless DC (BLDC) motors, which offer greater longevity and reduced noise profiles, essential for premium residential applications. Furthermore, battery technology, particularly long-life lithium-ion batteries, is increasingly critical, supporting completely wireless installations that eliminate the need for hardwiring, thus drastically simplifying the retrofit process and expanding market accessibility.

Communication protocols dictate the functionality and interoperability of the systems. While established RF protocols provide robust, long-range control favored by large-scale installers (often utilizing specialized RF frequencies unique to the manufacturer), the market trend favors open-standard IoT protocols. Wi-Fi offers direct connectivity to home routers, making it highly accessible but sometimes prone to network congestion and higher power draw. Conversely, low-power mesh networking protocols such as Z-Wave and Zigbee provide high reliability, extensive range, and low latency across large homes or commercial spaces, facilitating complex whole-building automation scenarios. The emergence of unified standards like Matter and Thread is set to standardize this fragmented landscape, enabling devices from different manufacturers to communicate natively, which will be a major technological shift in the coming years.

Sensor technology constitutes the third pillar of the current landscape. Light sensors (photocells) and temperature sensors are routinely integrated to allow the curtains to react autonomously to environmental conditions, optimizing light levels and thermal insulation dynamically. Occupancy sensors and time-of-flight cameras are also being introduced in high-end commercial systems to adjust shading based on real-time room usage, maximizing energy efficiency when spaces are empty. This integration of sophisticated sensing and processing capabilities transforms the motorized curtain from a simple mechanical device into an intelligent peripheral of the smart building system. Manufacturers are investing heavily in miniaturizing these components so they can be discreetly integrated within the track mechanisms without compromising the aesthetic appeal of the window covering.

The global Electric Curtains Market exhibits significant regional variations in terms of adoption rates, technological preference, and market maturity, heavily influenced by local economic conditions and building codes. The market analysis focuses on North America, Europe, Asia Pacific (APAC), Latin America, and the Middle East and Africa (MEA), each presenting unique opportunities and competitive dynamics.

North America (United States, Canada, Mexico)

North America holds a dominant market share, driven by the early and aggressive adoption of smart home technology, high consumer spending power, and a strong presence of key technology manufacturers and system integrators. The market is characterized by a strong demand for high-quality, interconnected systems that integrate seamlessly with platforms like Google Home and Amazon Alexa. Energy conservation is a significant driver, especially in regions with extreme climate variations, where automated shading significantly reduces heating and cooling costs. The trend is moving towards custom-fitted, premium solutions, often requiring professional installation by certified integrators who manage complex wiring and network setup. The commercial sector, particularly corporate real estate and high-end residential towers, mandates sophisticated centralized shading systems to meet stringent environmental and accessibility regulations.

Europe (Germany, UK, France, Italy, Spain)

Europe represents a mature and highly conscious market, where demand is fueled equally by sustainability mandates and a deep-seated appreciation for design and aesthetics. Countries like Germany and the Netherlands are leaders in implementing strict energy performance standards for buildings, making automated solar control an essential component of modern architecture. The European market favors systems compatible with centralized bus systems like KNX for commercial and large residential projects, ensuring robust, whole-building control. While the initial investment cost remains a constraint, the long-term ROI associated with energy savings justifies the expenditure for both consumers and commercial developers. The UK, post-Brexit, remains a significant market, focusing on bespoke, high-end residential projects and retrofitting older housing stock with smart solutions.

Asia Pacific (APAC) (China, Japan, South Korea, India)

The Asia Pacific region is the fastest-growing market globally, characterized by unprecedented urbanization and massive residential and commercial infrastructure development. China and India are the core growth engines, benefiting from a rapidly expanding middle class eager to adopt smart technology for status and convenience. Unlike mature Western markets, APAC sees a higher proportion of new construction installations compared to retrofits. The sheer volume of new construction projects allows manufacturers to integrate electric curtain systems from the initial design phase. Technology preferences lean toward Wi-Fi and Bluetooth solutions in the mass market due to lower cost and ease of integration, while high-end developers often import specialized proprietary systems. Competition is intense, with strong regional manufacturing bases driving down component costs and fostering localized innovation.

Latin America (Brazil, Mexico, Argentina)

Latin America is an emerging market for electric curtains, primarily concentrated in urban centers and luxury real estate developments in countries like Brazil and Mexico. Market growth is closely tied to improving economic stability and increasing investment in modern, high-rise residential buildings. While market penetration remains lower than in North America or Europe, the demand for security features (e.g., simulating occupancy while away) combined with climate management capabilities is accelerating adoption. Price sensitivity is higher in this region, necessitating the promotion of mid-range, feature-rich products. Distribution often relies on local specialty contractors and interior designers rather than large retail chains.

Middle East and Africa (MEA) (UAE, Saudi Arabia, South Africa)

The MEA region, particularly the Gulf Cooperation Council (GCC) countries, represents a high-value, niche market driven by substantial investment in luxury hospitality, massive infrastructure projects (like NEOM), and high energy consumption due to extreme heat. Electric curtains are essential here for managing intense solar heat gain, which is critical for reducing cooling loads and operating costs in large commercial structures. Saudi Arabia and the UAE are prime consumers of ultra-premium, highly durable, and thermally efficient shading systems. The African sub-region shows nascent growth, focused primarily on commercial ventures and high-end residential estates in major cities, where security and convenience are the primary selling points.

The growth is primarily fueled by the accelerating adoption of comprehensive smart home ecosystems, increasing consumer awareness regarding energy conservation through automated solar control, and declining average selling prices of core motor components. Furthermore, the rising demand for convenience and accessibility solutions, particularly in high-end residential and hospitality sectors, contributes significantly to market expansion.

While proprietary Radio Frequency (RF) systems remain highly reliable, the market is rapidly migrating towards open-standard protocols such as Wi-Fi and Bluetooth for ease of integration into residential settings. For large commercial installations requiring robust reliability and extensive network coverage, Z-Wave and Zigbee, and specialized bus systems like KNX, continue to be the protocols of choice due to their mesh networking capabilities and centralized control potential.

Electric curtains enhance energy efficiency by utilizing automation features and integrated sensors to dynamically manage solar heat gain and loss. By automatically closing during peak sun hours in summer, they minimize heat absorption, reducing the load on air conditioning systems. Conversely, opening the curtains during winter daylight hours maximizes passive solar heating, reducing reliance on central heating, leading to measurable cost savings and lower carbon footprints.

The primary installation challenges include the need for precise measurement and custom fitting to ensure smooth operation, the requirement for dedicated electrical wiring or managing battery charging cycles, and the complex configuration necessary for seamless integration with existing smart home hubs or Building Management Systems (BMS). Professional, certified integrators are often required to overcome these technical hurdles, especially in retrofitting projects.

The Asia Pacific (APAC) region, spearheaded by dynamic economies such as China and India, offers the highest growth potential. This is driven by massive new residential and commercial construction volumes, increasing disposable incomes enabling discretionary spending on home automation, and a rapid societal shift toward adopting modern, technologically advanced building standards. APAC is expected to exhibit the highest Compound Annual Growth Rate (CAGR) through 2033.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.