ID : MRU_ 433223 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

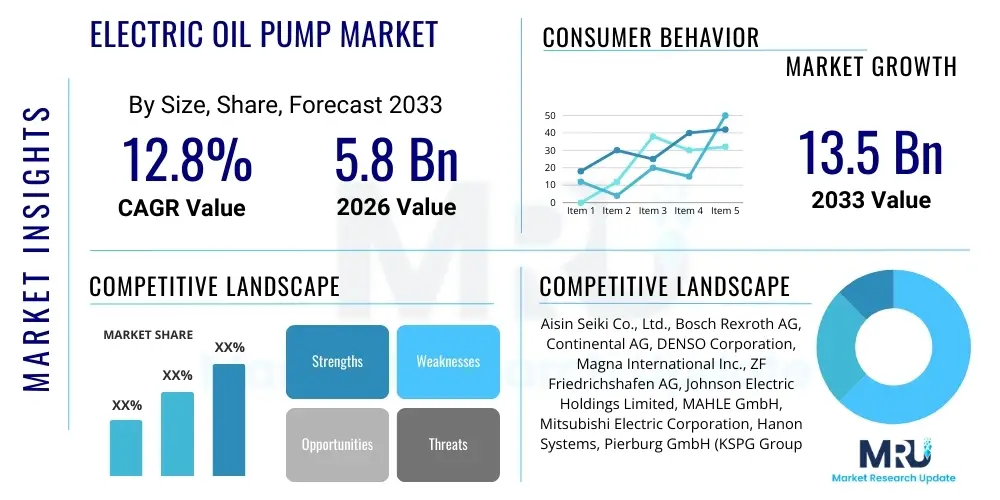

The Electric Oil Pump Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2026 and 2033. The market is estimated at USD 5.8 Billion in 2026 and is projected to reach USD 13.5 Billion by the end of the forecast period in 2033.

The Electric Oil Pump (EOP) Market encompasses advanced fluid management systems utilized primarily in modern automotive applications, including Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), and conventional Internal Combustion Engine (ICE) vehicles that require sophisticated auxiliary lubrication and thermal management. These pumps replace traditional mechanical pumps, offering variable flow rates independent of engine speed, which significantly enhances fuel efficiency, reduces parasitic losses, and improves overall thermal stability, especially in stop-start and hybrid operational modes. Products include wet-type and dry-type pumps, crucial for applications such as engine lubrication, transmission fluid circulation, and active battery cooling systems in electrified powertrains.

Major applications of EOPs span across powertrain components, including dedicated pumps for transmission lubrication (DCT/AT), engine oil delivery, and crucial auxiliary functions like turbocharger cooling post engine shutdown. The inherent ability of EOPs to operate on demand makes them indispensable for maximizing efficiency in complex systems like hybrid transmissions, where precise pressure and flow control are mandatory for clutch engagement and gear shifting. Furthermore, their deployment is critical in meeting stringent global emission regulations, as optimized lubrication reduces friction and subsequently lowers CO2 output and pollutant emissions from ICE vehicles.

The principal benefits driving market expansion include enhanced fuel economy through reduced engine load, superior thermal management for high-performance components (like batteries and power electronics), and improved vehicle reliability due to precise flow control under diverse operating conditions. Key driving factors accelerating market adoption are the accelerating global shift towards vehicle electrification, supportive governmental mandates promoting low-emission vehicles, and the increasing complexity of modern transmissions that necessitate highly responsive and efficient oil circulation solutions.

The Electric Oil Pump Market is experiencing transformative business trends dominated by strategic collaborations between Tier 1 suppliers and major automotive OEMs focused on developing integrated thermal and lubrication management modules. There is a discernible market shift towards higher voltage EOPs (48V and above) necessary for supporting larger battery packs and high-performance electric drive systems. Innovation is centered around compact design, noise reduction, and the integration of smart electronics for predictive maintenance capabilities, transforming EOPs from simple mechanical devices into essential electronic subsystems within the vehicle architecture. This transition is redefining traditional supply chains, demanding expertise in motor control, power electronics, and high-efficiency permanent magnet materials.

Regionally, Asia Pacific (APAC), led by China and Japan, maintains the largest market share due to its dominant position in electric vehicle manufacturing and adoption, coupled with favorable government policies promoting New Energy Vehicles (NEVs). Europe exhibits robust growth driven by stringent Euro 7 emission standards and ambitious decarbonization targets, propelling the adoption of EOPs in both mild-hybrid and full-electric architectures. North America is poised for accelerated growth, supported by massive investments in EV infrastructure and domestic manufacturing capabilities, particularly requiring high-performance EOPs for robust battery thermal management in diverse climatic conditions.

Segment trends reveal that the Transmission Oil Pump segment, vital for high-efficiency automatic and dual-clutch transmissions, holds a significant market share, while the Coolant Pump segment is projected to exhibit the highest Compound Annual Growth Rate (CAGR) driven overwhelmingly by the necessity for precise thermal regulation in EV battery packs and power inverter units. Furthermore, the OEM channel dominates sales, reflecting the primary demand stemming from new vehicle production lines, although the aftermarket is slowly gaining traction, fueled by the growing service and repair needs of the burgeoning hybrid and electric vehicle fleet globally.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Electric Oil Pump Market typically revolve around themes of predictive maintenance, optimized performance control, and supply chain efficiency. Users frequently question how AI algorithms can enhance the lifespan of EOPs, whether machine learning can optimize power consumption based on real-time driving patterns, and the feasibility of integrating smart diagnostics directly into the pump control unit. Concerns often focus on data security, the required infrastructure for complex analytics, and the necessity for standardized communication protocols to enable seamless interaction between the EOP ECU and the vehicle’s central AI management system. The overarching expectation is that AI will move EOP functionality beyond simple variable flow control toward truly adaptive, energy-saving, and self-diagnosing operation, significantly improving vehicle reliability and operational efficiency across diverse environmental stresses.

The Electric Oil Pump Market dynamics are fundamentally shaped by strong regulatory drivers and technological progression, offset by inherent cost barriers and standardization challenges within the automotive industry transition. Key drivers include the global push for vehicle electrification, which makes EOPs critical for battery and motor thermal management, and increasingly stringent emission standards (like CAFE and Euro 7), compelling OEMs to adopt efficient auxiliary systems to reduce parasitic engine loads. Significant opportunities arise from the expansive adoption of high-voltage architectures (800V systems) in premium EVs, requiring highly specialized, robust EOPs, and the potential application of EOPs in industrial machinery and renewable energy systems beyond traditional automotive use.

However, the market faces notable restraints, primarily the substantially higher initial cost of electric pumps compared to traditional mechanical pumps, which pressures cost-sensitive vehicle segments. Furthermore, the rapid evolution of EV architecture leads to a lack of standardization across voltage levels, mounting configurations, and communication protocols (CAN/LIN), complicating the manufacturing and interoperability for global Tier 1 suppliers. The necessity for advanced electronic control units (ECUs) and sophisticated software integration also increases complexity and potential points of failure, requiring rigorous validation protocols.

The primary impact forces propelling market growth are the regulatory mandate for efficiency improvements and the consumer demand for extended EV range and reliability. These forces ensure continuous investment in EOP research and development aimed at improving pump efficiency and reducing component footprint. The competitive landscape is intensely focused on material science to develop lighter, more durable pump housings, and power electronics expertise to maximize efficiency, thus positioning EOP technology as a critical enabler for the next generation of highly efficient and autonomous electric vehicles.

The Electric Oil Pump Market segmentation is crucial for understanding specific growth vectors, largely differentiated by product type, functional application, vehicle architecture, and distribution methodologies. Analysis by Type distinguishes between Wet Type EOPs, which are submerged in the fluid they pump, offering cooling and compactness but facing challenges related to fluid compatibility and seal integrity, and Dry Type EOPs, which are mounted externally, providing easier maintenance and superior thermal separation for the motor but often requiring additional installation space. Both types are optimized for distinct tasks, with wet-type pumps often preferred for transmission applications and dry-type pumps prevalent in battery cooling systems.

The Application segmentation highlights the diverse roles EOPs play across the modern vehicle ecosystem, ranging from primary Engine Oil lubrication (though less prominent in pure EVs), essential Transmission Oil circulation, high-growth Coolant circulation for thermal management, and specific Vacuum Pump functions crucial for brake boosting in EVs and hybrids. The rapid proliferation of electric vehicles has cemented the Coolant Pump and Transmission Oil Pump segments as the primary drivers of current and future market expansion. Vehicle segmentation, covering Passenger Vehicles and Commercial Vehicles, demonstrates that while Passenger Vehicles currently dominate volumes due to mass adoption of hybrids and EVs, Commercial Vehicles, particularly electric buses and heavy-duty trucks, represent a growing market due to the need for robust, high-capacity cooling systems for large battery packs.

Distribution segmentation between OEM (Original Equipment Manufacturer) and Aftermarket channels confirms the market's reliance on new vehicle production, with OEMs commanding the majority share due to the highly integrated nature of EOPs in vehicle design. However, as the global fleet of EOP-equipped vehicles ages, the Aftermarket is anticipated to grow steadily, requiring specialized suppliers capable of providing reliable, compatible replacement units that meet the complexity of modern vehicle control systems. Understanding these segment dynamics is paramount for manufacturers seeking targeted investment and strategic market entry.

The value chain for the Electric Oil Pump Market is characterized by highly specialized components and advanced manufacturing processes, beginning with the procurement of critical raw materials, specifically high-grade permanent magnets (such as Neodymium), specialized copper windings for motors, and high-performance engineering plastics and seals capable of withstanding extreme temperatures and chemical environments. Upstream analysis focuses intensely on securing stable supplies of these raw materials and developing reliable semiconductor components (power MOSFETs and microcontrollers) necessary for the integrated electronic control units. Key players in this phase are material suppliers and specialized electronic component manufacturers who significantly influence the cost and performance ceiling of the final EOP product.

The middle stage involves complex manufacturing, assembly, and rigorous testing conducted primarily by large Tier 1 automotive suppliers. This phase necessitates significant investment in high-precision machining, clean-room assembly, and sophisticated automated testing to ensure pumps meet strict hydraulic, electrical, and NVH (Noise, Vibration, Harshness) specifications mandated by OEMs. Strategic focus during manufacturing centers on optimizing motor efficiency, minimizing size and weight, and ensuring software reliability for real-time communication with the vehicle's master control unit. Quality assurance and compliance with ISO/TS standards are non-negotiable prerequisites for entry into the supply networks of major automotive manufacturers.

Downstream distribution channels are segmented primarily into Direct (OEM) and Indirect (Aftermarket). The Direct channel involves just-in-time delivery of finalized, validated EOP modules directly to vehicle assembly lines worldwide, demanding absolute reliability in logistics and zero-defect quality. The Indirect channel involves distribution through authorized parts dealers, independent service organizations, and specialized automotive repair shops. The Aftermarket requires robust inventory management and clear product identification to ensure correct part selection for a diverse range of vehicle models and years. The overall value chain emphasizes vertical integration, with leading suppliers often controlling key technology aspects from magnet production to final software calibration to maintain a competitive advantage in performance and cost.

The primary end-users and buyers of Electric Oil Pumps are large automotive Original Equipment Manufacturers (OEMs), who integrate these components into their new vehicle platforms, spanning passenger cars, SUVs, and commercial vehicles. OEMs demand EOPs that offer superior reliability, high energy efficiency, specific flow characteristics tailored to proprietary transmission and battery systems, and seamless integration with complex vehicle architectures, typically engaging in long-term procurement contracts with Tier 1 suppliers. The crucial decision-making factor for OEMs is the EOP's contribution to achieving mandated fuel economy targets, extended EV range, and superior component durability.

A rapidly growing segment of potential customers includes specialized manufacturers of electric powertrain components and battery systems, who require dedicated EOPs for their sub-systems before integration into a final vehicle chassis. This includes companies specializing in developing advanced dual-clutch transmissions (DCTs) for hybrid vehicles, high-performance battery pack manufacturers, and suppliers of power electronics (inverters and converters). These customers seek highly specialized, sometimes customized, EOP solutions that can handle specific thermal loads and fluid types unique to their high-performance systems.

Finally, the aftermarket customers, comprising automotive repair facilities, independent service garages, fleet operators, and authorized dealership service centers, constitute the secondary customer base. These buyers focus on purchasing high-quality replacement units that match or exceed OEM specifications. For fleet operators, durability and cost of ownership are paramount, driving demand for EOPs with proven long-term reliability and straightforward diagnostic capabilities. The aftermarket is increasingly reliant on digital cataloging and rapid distribution networks to meet the maintenance demands of the growing global fleet of electrified vehicles.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | CAGR 12.8 % |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Aisin Seiki Co., Ltd., Bosch Rexroth AG, Continental AG, DENSO Corporation, Magna International Inc., ZF Friedrichshafen AG, Johnson Electric Holdings Limited, MAHLE GmbH, Mitsubishi Electric Corporation, Hanon Systems, Pierburg GmbH (KSPG Group), Nidec Corporation, SHW AG, Concentric AB, Mikuni Corporation, Trelleborg AB, Kirloskar Brothers Limited, Eberspächer Group, GMB Corporation, Vitesco Technologies. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Electric Oil Pump Market is rapidly advancing, focusing intensely on miniaturization, enhanced electrical efficiency, and sophisticated control systems. Core innovations center around the motor technology utilized, with Brushless DC (BLDC) motors being the industry standard due to their high power density, long service life, and excellent controllability compared to traditional brushed motors. Current R&D efforts are heavily invested in optimizing magnet materials and winding techniques to maximize torque and reduce power consumption while maintaining a compact footprint, essential for integration into constrained vehicle spaces, especially near transmissions and battery packs. Furthermore, the development of integrated controllers (System-on-Chip solutions) that embed the motor drive electronics directly into the pump housing is crucial for reducing external wiring complexity and enhancing overall system reliability against environmental factors such as vibration and heat.

Advanced hydraulic design represents another critical area of technological focus, aiming to reduce internal fluid losses and improve volumetric efficiency across a wide range of operating temperatures and viscosities. Suppliers are leveraging Computational Fluid Dynamics (CFD) modeling to refine impellers and housing geometries, ensuring optimal flow characteristics for specific applications, such as high-pressure transmission lubrication or high-volume battery coolant circulation. The adoption of high-performance materials, including specialized polymers and ceramics for seals and bearings, is essential to prolong the operational life and ensure compatibility with modern synthetic oils and coolants, particularly those utilized in extreme temperature environments within high-power density electric powertrains and fast-charging cycles.

The most defining technological shift is the integration of sophisticated electronic control and communication capabilities. Modern EOPs are not standalone devices but networked components, communicating vital operational data via CAN bus or LIN protocols to the vehicle’s master ECU. This connectivity enables advanced functionalities such as on-demand operation, diagnostic feedback, and seamless integration with vehicle thermal management strategies. Future technologies are exploring the use of high-frequency switching for greater efficiency and reduced electromagnetic interference (EMI), alongside the incorporation of edge computing capabilities for real-time local monitoring and basic fault correction, further supporting the industry trend towards fully intelligent vehicle systems.

The primary function of an EOP in electrified vehicles is enabling independent fluid circulation for lubrication and thermal management, regardless of engine speed. This is crucial for optimizing efficiency in start-stop systems, cooling high-voltage batteries, and lubricating transmissions in hybrid and electric drive systems, maximizing component life and vehicle range.

The shift to 800V architectures necessitates more robust, higher-power-density EOPs capable of operating efficiently at higher voltages. This trend drives demand for technologically advanced pumps requiring specialized motor controls and enhanced insulation, contributing significantly to market value growth, particularly in the premium EV segment.

The Coolant Pump segment, critical for battery thermal management and power electronics cooling in Battery Electric Vehicles (BEVs), is projected to exhibit the highest CAGR. As EV production scales globally, the demand for precise, reliable thermal fluid circulation systems dictates the strong expansion of this segment.

Wet Type EOPs are typically more compact and offer inherent noise reduction as they are submerged in fluid. They are often favored for integrated transmission lubrication systems due to their simpler sealing and efficient cooling, contrasting with Dry Type pumps, which are mounted externally and provide easier access for maintenance and better thermal isolation.

The main restraints are the significantly higher initial manufacturing cost of EOPs compared to traditional mechanical pumps, primarily due to the inclusion of sophisticated electronics (BLDC motors and ECUs). Additionally, the lack of standardization across rapidly evolving EV platforms complicates mass production economies of scale, maintaining a high cost barrier.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.