ID : MRU_ 439175 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

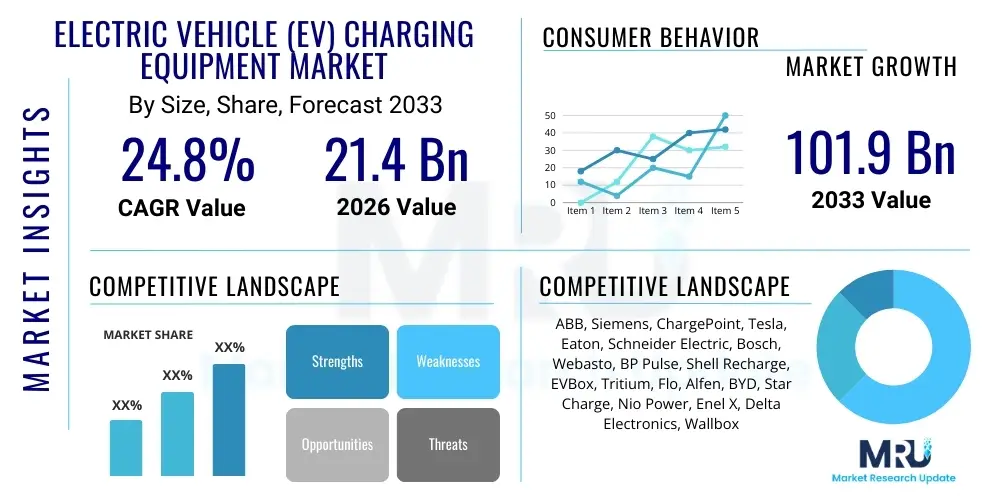

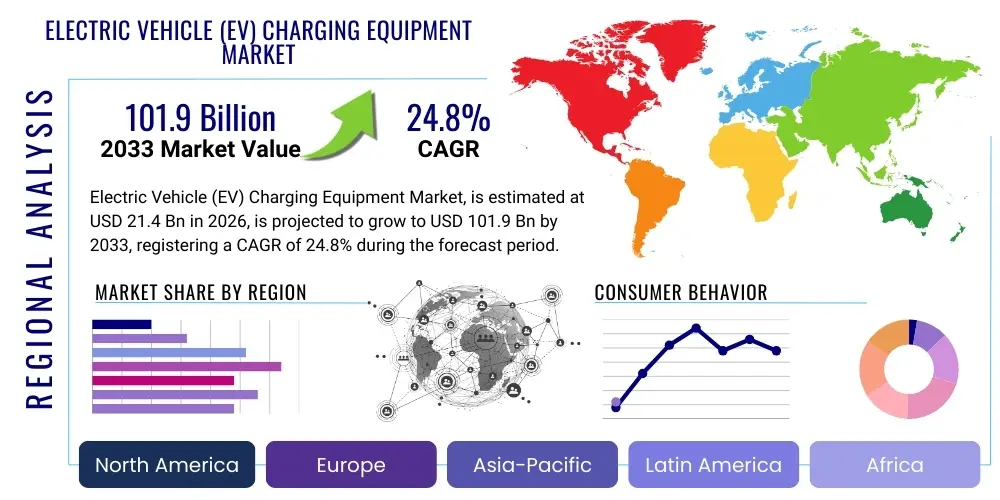

The Electric Vehicle (EV) Charging Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 24.8% between 2026 and 2033. The market is estimated at USD 21.4 Billion in 2026 and is projected to reach USD 101.9 Billion by the end of the forecast period in 2033.

The substantial growth trajectory is underpinned by aggressive global electrification goals and mandatory regulatory shifts phasing out Internal Combustion Engine (ICE) vehicles. Increasing consumer adoption of EVs, driven by environmental concerns and decreasing battery costs, necessitates a robust, widespread charging infrastructure. This rapid expansion demands significant investment in both public charging networks, particularly DC fast charging stations along major transit routes, and residential charging solutions, solidifying the market’s high growth potential through the forecast period.

The Electric Vehicle (EV) Charging Equipment Market encompasses the essential hardware, software, and services required to replenish the batteries of electric vehicles. This infrastructure is critical for the mass adoption of EVs, providing connectivity between the power grid and the vehicle's battery management system. Key products include AC chargers (Level 1 and Level 2) predominantly used in residential and workplace settings, and DC fast chargers (Level 3) crucial for public, high-speed charging requirements, mitigating range anxiety and enabling long-distance travel. The development and deployment of this equipment are vital for supporting governmental mandates and achieving net-zero emission targets globally.

Major applications of EV charging equipment span residential homes, commercial parking facilities, public charging stations managed by Charging Point Operators (CPOs), and dedicated fleet depots for logistics and public transport vehicles. The core benefits include enabling sustainable transportation, reducing reliance on fossil fuels, improving air quality in urban centers, and creating new opportunities for utility grid management and smart city integration. The rapid technological advancements in power electronics and communication protocols (such as OCPP and ISO 15118) are making charging solutions more efficient, interoperable, and secure.

Driving factors for this market include supportive governmental incentives, such as tax credits and subsidies for both EV purchases and charging infrastructure installation, coupled with mandates for zero-emission vehicle sales. Furthermore, significant investments by automotive OEMs in establishing proprietary charging networks and the standardization efforts across North America, Europe, and Asia Pacific are fueling market expansion. The integration of smart grid features, dynamic load management, and Vehicle-to-Grid (V2G) capabilities further enhances the value proposition of modern charging equipment, ensuring sustainable scaling of the infrastructure in line with grid capacity.

The EV Charging Equipment Market is experiencing transformative growth, characterized by significant business model diversification and technological acceleration, predominantly centered on high-power DC fast charging and advanced software integration. Business trends highlight a strong shift toward comprehensive Energy-as-a-Service (EaaS) models, where Charging Point Operators (CPOs) collaborate with utilities and fleet operators to provide optimized charging solutions, leveraging smart charging and dynamic pricing. Consolidation and strategic partnerships among hardware manufacturers, software providers, and major energy companies are defining the competitive landscape, focused on achieving standardization and scale across different geographies.

Regionally, Asia Pacific maintains market dominance due to aggressive electrification targets in China and burgeoning demand in India and South Korea, driving massive installations of public Level 2 and DC fast chargers. North America is poised for high growth, fueled by substantial federal funding (such as the NEVI program) aimed at building a robust national corridor charging network. Europe emphasizes interoperability and sustainable sourcing, with countries like Germany and the Nordics leading the push for smart grid integration and V2G technologies, ensuring charging infrastructure complements renewable energy sources.

Segment trends underscore the rising importance of DC fast chargers (Level 3) for commercial and public applications, significantly outpacing the growth rate of slower AC chargers, reflecting the need for expedited charging times. Within the component segment, software and services are growing fastest, driven by the need for advanced Charging Station Management Systems (CSMS), sophisticated billing solutions, and predictive maintenance services. The residential segment remains foundational but increasingly incorporates smart features, while commercial fleets represent the most lucrative near-term opportunity for high-utilization charging solutions and integrated fleet management software.

User inquiries regarding AI's influence on the EV charging sector frequently revolve around optimization, efficiency, and predictive capabilities. Common questions focus on how AI can manage grid load during peak EV charging events, improve charging reliability through predictive maintenance, and personalize charging experiences based on driver behavior and energy costs. Users are particularly concerned about the transition to smarter infrastructure, querying the role of AI in Vehicle-to-Grid (V2G) implementation and the security implications of autonomous charging systems. The central expectation is that AI will be the key enabler for scaling charging infrastructure without destabilizing existing electrical grids, ensuring optimal energy flow and minimizing operational downtime.

The integration of Artificial Intelligence and Machine Learning (ML) is fundamentally transforming the operational efficiency of EV charging networks. AI algorithms are deployed for sophisticated dynamic load balancing, optimizing the distribution of available power across multiple charging stations based on real-time grid constraints, forecasted renewable energy availability, and prioritized charging needs of specific vehicles (e.g., high-priority fleet vehicles). This intelligence minimizes infrastructure upgrade costs for CPOs and prevents localized grid overload, making the network inherently scalable and resilient against energy price fluctuations.

Furthermore, AI is crucial for enhancing the user experience and improving system reliability. Predictive maintenance models, driven by ML analysis of operational data (temperature, voltage anomalies, usage patterns), allow CPOs to anticipate hardware failures before they occur, drastically reducing out-of-service time and improving customer satisfaction. AI-driven recommendation engines can also personalize charging schedules and suggest the most cost-effective and convenient charging locations based on traffic, battery state of charge, and utility tariffs, moving the industry toward truly autonomous and highly efficient energy management.

The EV Charging Equipment Market is shaped by powerful Drivers (D) such as stringent global emission regulations and supportive governmental subsidies, countered by significant Restraints (R) including the high initial capital expenditure for DC fast charging deployment and persistent concerns regarding grid infrastructure readiness. Opportunities (O) abound in the development of Vehicle-to-Everything (V2X) technologies, particularly V2G integration, and the expansion into emerging markets requiring rapid infrastructure deployment. These forces collectively dictate the pace and direction of market growth, prioritizing scalable and smart charging solutions to overcome inherent infrastructure challenges.

The primary drivers include the massive commitments by major automotive manufacturers to fully electrify their fleets, creating guaranteed demand for charging solutions. This is amplified by consumer preference shifts toward sustainability and the declining total cost of ownership (TCO) for EVs. However, the market faces significant restraints related to standardization fragmentation (different connector types like CCS, CHAdeMO, NACS, and regional variations in regulatory compliance) and the complexity associated with acquiring permits and integrating charging stations with localized utility infrastructure, which often causes project delays.

Opportunities are largely focused on innovation in ultra-fast charging technology (350kW+) and the penetration of charging solutions into previously underserved sectors, such as heavy-duty trucking and marine transport. Furthermore, the convergence of charging infrastructure with renewable energy generation (solar canopies, battery storage) presents an opportunity for CPOs to create sustainable, off-grid or grid-independent charging hubs. The impact forces indicate a strong positive market momentum driven by sustained policy support and technological convergence, though profitability is still highly sensitive to utility costs and utilization rates.

The EV Charging Equipment Market is comprehensively segmented across several key dimensions including the type of charger (AC vs. DC), the application environment (commercial vs. residential), the components offered (hardware, software, services), and the connector standard. This segmentation provides a granular view of market dynamics, revealing that growth is disproportionately driven by commercial applications requiring high-power DC charging, which necessitates advanced software management for utilization optimization and billing efficiency. Understanding these segments is crucial for stakeholders to tailor investment strategies towards the highest-growth areas, particularly smart charging and public access networks.

The segmentation by charging level is fundamental, differentiating between Level 1/Level 2 AC charging (slower, typically <22kW) and Level 3 DC fast charging (rapid, often 50kW to 350kW+). While AC charging dominates installation volume in residential settings, DC fast charging commands higher market revenue due to its complexity, capital intensity, and critical role in public charging infrastructure. The component segmentation highlights the increasing value contribution of software, moving the industry beyond simple hardware sales toward subscription-based, recurring revenue models centered on Charging Station Management Systems (CSMS) and energy data analytics.

The value chain for EV charging equipment is complex and involves multiple highly specialized stages, beginning with upstream raw material suppliers and power component manufacturers. Upstream activities include the production of power semiconductors (IGBTs, MOSFETs), specialized cables, smart meter components, and enclosures. This stage is crucial as the quality and efficiency of these components directly impact the charger's reliability and charging speed. Key challenges upstream involve securing stable supply chains for semiconductor chips and ensuring compliance with rapidly evolving safety and electrical standards.

Midstream activities involve the core manufacturing, integration, and software development. Manufacturers assemble power modules, integrate communication hardware, and develop proprietary Charging Station Management Software (CSMS). This stage requires significant R&D investment to enhance power density, thermal management, and connectivity features (OCPP compliance, V2G capabilities). The integration of robust cybersecurity features is paramount here, given the system's connection to both the vehicle and the smart grid.

Downstream analysis focuses on distribution, installation, operation, and maintenance. Distribution channels are highly varied, involving direct sales to fleet operators and utilities, and indirect sales through authorized electrical distributors, CPOs, and specialized system integrators. The final installation and activation process, often handled by certified electricians, must be tightly coordinated with local utilities. The ongoing operation and maintenance (O&M) and provision of cloud-based services generate long-term recurring revenue for CPOs and software providers, marking the highest value-added activity in the downstream segment.

Potential customers for EV charging equipment are broadly categorized into entities responsible for vehicle ownership, energy management, and public access provision. Charging Point Operators (CPOs), such as ChargePoint or BP Pulse, are primary high-volume buyers, investing in large networks of public charging stations and requiring robust hardware and comprehensive, scalable management software. Utilities and grid operators constitute another major customer segment, purchasing equipment for grid integration, load balancing projects, and sometimes operating their own charging assets to manage local power distribution and implement V2G pilot programs.

Automotive Original Equipment Manufacturers (OEMs), including Tesla, Ford, and VW, are significant customers, either establishing proprietary charging networks to support their vehicle sales or partnering with CPOs to ensure customer access. Fleet operators, encompassing last-mile delivery, taxi services, and municipal bus agencies, represent a fast-growing segment requiring bespoke, high-utilization charging depots with advanced energy management software to minimize operational costs and ensure optimal route scheduling. Lastly, residential homeowners and multi-unit dwelling (MUD) owners form the base customer segment for Level 1 and Level 2 AC chargers, prioritizing ease of use, smart connectivity, and installation simplicity.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 21.4 Billion |

| Market Forecast in 2033 | USD 101.9 Billion |

| Growth Rate | 24.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens, ChargePoint, Tesla, Eaton, Schneider Electric, Bosch, Webasto, BP Pulse, Shell Recharge, EVBox, Tritium, Flo, Alfen, BYD, Star Charge, Nio Power, Enel X, Delta Electronics, Wallbox |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the EV charging market is rapidly evolving, driven primarily by the need for faster, more efficient, and smarter power delivery. A major area of innovation is in power electronics, specifically the transition from silicon-based semiconductors to wide bandgap materials like Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials enable the creation of smaller, lighter, and significantly more efficient power conversion modules for DC fast chargers, allowing for ultra-high power output (350kW and above) while minimizing energy loss and improving thermal management, crucial for high-utilization environments.

Another pivotal technology is the development of advanced communication and standardization protocols. ISO 15118 is becoming the standard for Plug and Charge functionality, enabling automated authentication and billing simply by plugging the vehicle in, significantly enhancing the user experience and security. Concurrently, the growth of the Open Charge Point Protocol (OCPP), particularly OCPP 2.0.1, is essential for enabling smart charging capabilities, including sophisticated remote management, detailed transaction logging, and crucial support for V2G communication and smart energy grid interactions, fostering interoperability across different vendor hardware and software.

Inductive (wireless) charging technology, although still nascent, is gaining traction, particularly for fleet applications like autonomous shuttles and buses where manual plug-in is inefficient. Furthermore, the integration of energy storage systems (BESS) directly into charging hubs is a growing trend. BESS allows charging stations to draw power from the grid slowly during off-peak hours and deliver it quickly to EVs during peak times, effectively decoupling the fast charging demand from instantaneous grid capacity, thereby enabling the deployment of ultra-fast chargers in locations with weak grid connections and optimizing operational costs.

Regional dynamics heavily influence the type and scale of EV charging deployment, with Asia Pacific (APAC) maintaining the largest market share, driven overwhelmingly by China's aggressive national electrification strategy. China has established the world’s most extensive public charging network, focusing heavily on both high-volume public Level 2 chargers and dense deployments of DC fast chargers to support its massive domestic EV production. Other significant APAC growth markets include South Korea and Japan, focusing on technological innovation (like high-power CHAdeMO and CCS integration), and India, which is rapidly scaling up its infrastructure to support its nascent but explosive two and three-wheeler EV segments.

North America is characterized by robust regulatory support and unprecedented federal investment, notably through the Infrastructure Investment and Jobs Act (IIJA) and the NEVI program, which mandate a standardized, interoperable network across major highway corridors. This region is focused on deploying reliable DC fast charging to address range anxiety, with a critical emphasis on high reliability and seamless payment systems. The recent adoption of the North American Charging Standard (NACS) by major OEMs is simplifying the future infrastructure rollout, though harmonization with existing CCS infrastructure remains a critical short-term challenge.

Europe stands out for its strong emphasis on sustainability, interoperability, and smart grid integration. The region is governed by the Alternative Fuels Infrastructure Regulation (AFIR), pushing for denser public charging infrastructure and mandatory minimum power outputs. European markets, particularly in Nordic countries and Germany, lead in V2G pilot projects, positioning charging equipment not just as a consumer necessity but as an active component of the future energy grid, supporting renewable energy penetration and ensuring energy security.

The explosive growth is primarily driven by massive governmental mandates worldwide focused on phasing out fossil fuel vehicles and substantial subsidies for both EV purchases and infrastructure development. Technological advancements leading to faster, more reliable DC charging, coupled with major automotive OEM investments in electrification, are also core accelerators.

V2G (Vehicle-to-Grid) technology transforms charging equipment from a passive energy consumer to an active grid resource. V2G-enabled equipment allows parked EVs to feed excess stored energy back into the power grid during peak demand, stabilizing the grid, minimizing reliance on fossil-fuel peaking plants, and potentially offering revenue streams for EV owners and CPOs.

DC Fast Charging (Level 3) dominates market revenue despite lower unit volumes compared to AC Level 2. This is because DC fast chargers require significantly higher capital investment due to complex power electronics (rectifiers, transformers), robust thermal management systems, and high-power grid connections, resulting in a much higher average selling price (ASP) per unit.

AI is crucial for enhancing efficiency through dynamic load management, optimizing power distribution in real-time based on grid constraints and demand forecasts. For reliability, AI utilizes predictive maintenance algorithms, analyzing operational data to anticipate component failures, thereby reducing station downtime and improving overall network utilization rates.

The main regional challenges involve the coexistence and competition among various connector standards: CCS in North America and Europe, CHAdeMO (prevalent in older Japanese models), and GB/T in China. North America is currently undergoing a significant transition toward the Tesla-developed North American Charging Standard (NACS), creating a short-term challenge for CPOs needing to rapidly adapt hardware to support multiple connection types.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.