ID : MRU_ 435594 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

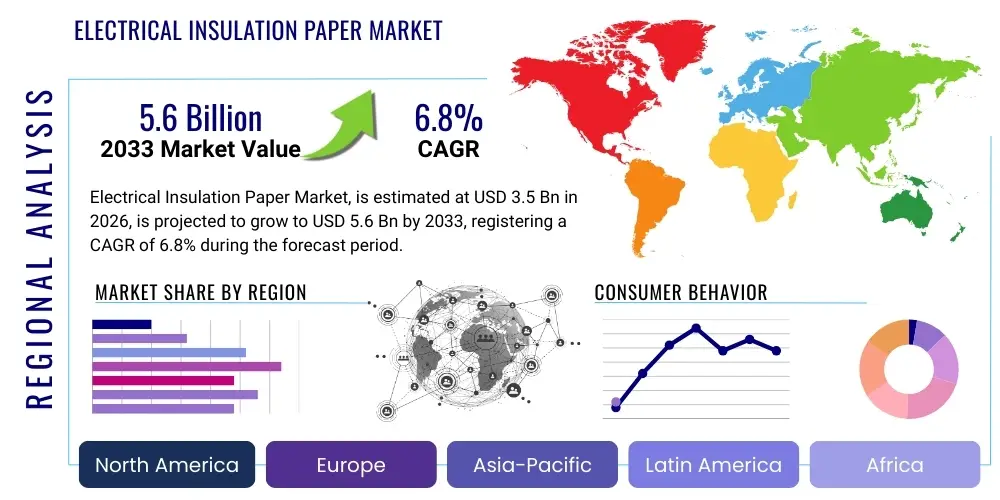

The Electrical Insulation Paper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.6 Billion by the end of the forecast period in 2033.

Electrical Insulation Paper, a critical component in electrical apparatus, is characterized by its superior dielectric strength, high thermal stability, and mechanical resilience, making it essential for preventing short circuits and ensuring the longevity of equipment. Primarily manufactured from highly refined cellulosic pulp, or synthetic fibers like aramid, this material serves as the main barrier against electrical discharge in high-voltage applications. Its fundamental role is to manage thermal stress while maintaining required insulation standards across a diverse range of operational environments, thereby upholding system reliability and safety standards within the electrical infrastructure. The efficacy of electrical insulation paper is directly linked to the purity of its raw materials and the precision of its manufacturing process, which includes specialized treatments like densification and impregnation.

The product portfolio encompasses various types, including standard Kraft paper for oil-filled transformers, thermally upgraded paper (TUP) for enhanced longevity, and advanced synthetic papers like aramid (meta- and para-aramid) for applications requiring exceptional thermal performance (Class H and above), such as traction motors and specialized aerospace components. Major applications driving demand include the construction and maintenance of power and distribution transformers, high-voltage cables, capacitors, and rotating machinery like generators and electric motors. These components require dependable insulation to handle increasing power loads and operate reliably under stringent environmental conditions, including elevated temperatures and moisture exposure. The performance metrics, such as partial discharge resistance and tensile strength, are crucial determinants of material selection.

Key benefits of utilizing specialized insulation papers include enhanced equipment lifespan, reduced maintenance costs, and improved energy efficiency due to lower dielectric losses. The primary driving factors currently influencing market trajectory include global initiatives toward smart grid implementation, rapid urbanization demanding expansion of Transmission and Distribution (T&D) infrastructure, and the accelerating proliferation of renewable energy sources which necessitate specialized transformer designs. Furthermore, the burgeoning demand from the electric vehicle (EV) sector, particularly for reliable high-voltage battery insulation and motor windings, is creating substantial new avenues for high-performance dielectric materials, pushing manufacturers toward innovation in thermal classes and material lightweighting.

The Electrical Insulation Paper Market is poised for robust expansion, driven primarily by significant investments in global power infrastructure modernization and the accelerating shift towards electrified transport. Key business trends indicate a strong move away from traditional cellulosic materials toward high-performance synthetic alternatives, such as aramid paper and specialized pressboard, driven by the need for higher thermal ratings (Class F, H, and C) required for compact, efficient, and higher-voltage apparatus. Manufacturers are strategically focusing on developing insulation solutions compatible with new eco-friendly ester fluids to meet stringent environmental regulations, particularly in developed economies. Supply chain optimization, driven by the volatile pricing of wood pulp, remains a crucial competitive differentiator, prompting vertical integration strategies among major market players to secure stable raw material input and manage operational costs effectively.

Regionally, the Asia Pacific (APAC) market sustains its dominance, largely attributable to massive infrastructure projects in China and India, focusing on grid expansion, electrification programs, and the establishment of large-scale manufacturing hubs for electrical components and automotive industries. While North America and Europe demonstrate mature market characteristics, growth is anchored in replacing aging equipment, implementing smart grid technologies, and substantial uptake in EV charging infrastructure, which mandates specialized dielectric materials. The Latin American and Middle East & Africa (MEA) markets, though smaller, are exhibiting promising growth trajectories fueled by urbanization and increasing access to reliable electricity, translating into stable demand for distribution transformers and industrial motors.

Segment trends highlight the critical role of the Transformer segment, which accounts for the largest share of market revenue, necessitating large volumes of high-quality Kraft and thermally upgraded papers. However, the fastest growth is anticipated in specialized segments like Electric Motors and Capacitors, particularly those catering to renewable energy inverters and high-efficiency industrial machinery, where synthetic papers offer a significant performance advantage. There is a discernible trend toward thinner papers and composite insulation systems that offer space savings without compromising dielectric integrity. Sustainability and recyclability are emerging segment criteria, influencing purchasing decisions among utilities and large Original Equipment Manufacturers (OEMs), thereby necessitating innovation in both product composition and end-of-life management.

Common user questions regarding AI's influence typically revolve around how artificial intelligence can enhance the reliability, quality control, and operational efficiency within the electrical insulation paper sector. Users frequently inquire about the feasibility of AI-driven predictive maintenance in high-voltage equipment, which relies heavily on the state of the insulation paper; they also seek clarity on how AI algorithms can optimize raw material blending and processing parameters to achieve consistent dielectric properties and reduce material waste. Furthermore, interest focuses on AI’s capacity to analyze large datasets from stress testing and real-world operational monitoring to predict insulation breakdown prematurely. The consensus themes reveal high expectations for AI to minimize human error in manufacturing, drastically improve quality assurance (QA) through automated defect detection, and fundamentally transform asset management by predicting the remaining useful life (RUL) of insulated components like power transformers, leading to optimized procurement cycles for insulation papers.

The Electrical Insulation Paper Market is significantly shaped by a confluence of market dynamics where robust drivers encounter structural restraints, yet numerous strategic opportunities remain prevalent. Key drivers include the global push for renewable energy integration (solar and wind farms), which requires specialized transformers and cables, and extensive grid modernization efforts, particularly the replacement of aging infrastructure in North America and Europe, demanding reliable, high-thermal-class insulation materials. Simultaneously, the rapid expansion of electrification in the automotive sector, focusing on high-voltage battery systems and efficient motor windings for electric vehicles (EVs), necessitates ultra-high performance aramid papers and flexible composites. These drivers provide sustained, high-volume demand, especially for synthetic and thermally upgraded cellulosic papers capable of operating under increasingly harsh thermal and electrical stress.

Conversely, the market faces notable restraints, chiefly the inherent volatility in the prices of critical raw materials, primarily wood pulp and specialized chemical additives, which directly impacts manufacturing costs and profit margins. Furthermore, strict environmental regulations concerning the use of conventional mineral oil coolants are pushing manufacturers toward expensive, specialized insulation papers compatible with bio-based ester fluids, creating a temporary cost barrier. The challenge of material purity and the complexity of ensuring zero defects in large-scale paper production also act as restraints, requiring significant capital investment in advanced quality control systems. Geopolitical risks affecting global trade routes for raw materials and finished electrical components also introduce supply chain friction and uncertainty.

Despite these challenges, substantial opportunities exist, particularly in the development and commercialization of next-generation nano-cellulose reinforced insulation papers offering superior dielectric performance and reduced thickness, enabling miniaturization of electrical apparatus. The increasing adoption of High-Voltage Direct Current (HVDC) transmission lines for long-distance power transfer presents a lucrative niche, as HVDC components require papers with specialized resistance to polarity reversals and space charge accumulation. Furthermore, manufacturers focusing on sustainable and easily recyclable paper formulations, coupled with backward integration into pulp processing, stand to gain significant market share by offering environmentally compliant and cost-effective solutions. The convergence of 5G infrastructure development and data center construction also fuels demand for specialized, thermally managed capacitor and circuit board insulation.

The segmentation of the Electrical Insulation Paper Market provides a detailed perspective on product consumption patterns and end-use demand across various electrical components. This market is primarily segmented based on the Product Type (cellulosic and synthetic), Application (transformers, cables, motors), and End-User Industry (power, electronics, automotive). The analysis highlights the fundamental bifurcation between traditional cellulosic papers, valued for their cost-effectiveness and proven reliability in oil-filled apparatus, and high-performance synthetic papers, which command premium pricing due to their ability to withstand extreme temperatures and environmental stresses inherent in modern, compact electrical designs. Understanding these segment dynamics is crucial for manufacturers to tailor their production capabilities and target specific high-growth application niches, such as high-efficiency motors and specialized distribution systems.

The largest volume consumption lies within the cellulosic segment, driven predominantly by Kraft paper and its thermally upgraded variants, which are standard for power and distribution transformers globally. However, the synthetic segment, encompassing materials like aramid paper and specialized composites, is experiencing the fastest revenue growth. This rapid expansion is directly linked to the burgeoning electric vehicle market and sophisticated aerospace/defense applications, where thermal stability (above 155°C) and lightweight construction are paramount. Furthermore, within the application segment, the shift towards higher operating voltages and reduced equipment footprints necessitates innovation in dielectric materials, creating sustained demand for premium insulating solutions that offer enhanced mechanical and electrical longevity without increasing overall component size.

Regional variations in infrastructure and regulatory frameworks heavily influence segment performance. For instance, countries heavily investing in urban rail and high-speed transit prioritize synthetic papers for traction motor insulation, while regions focusing on grid expansion prioritize cost-effective cellulosic options for distribution transformers. The increasing standardization of high-voltage components and the pressure to reduce equipment downtime globally underscore the critical nature of insulation paper purity and consistency. Consequently, market players are continuously refining manufacturing processes, investing in digitalization, and developing new composite materials that integrate the cost advantages of cellulose with the thermal superiority of synthetic polymers, thereby blurring the lines between traditional product categories and driving hybrid solutions.

The value chain for electrical insulation paper commences with the upstream analysis, focusing heavily on the sourcing and preparation of specialized raw materials. For cellulosic papers (Kraft and pressboard), this involves procuring high-purity wood pulp, typically bleached or unbleached sulfate pulp from specific softwoods known for long fibers, crucial for mechanical strength. The quality and consistency of this pulp are paramount, as impurities significantly degrade dielectric strength. For synthetic papers, the upstream stage involves the production of specialized polymers, such as aramid fibers and resins, which requires chemical synthesis and often involves complex proprietary processes. Managing the supply stability and cost efficiency of these primary inputs forms the core competitive challenge in the upstream segment, frequently leading to strategic long-term supply agreements or vertical integration by major paper manufacturers.

The core manufacturing process, or the midstream stage, transforms raw pulp or synthetic fibers into the finished paper product through highly controlled processes, including pulping, refining, paper formation (using specialized Fourdrinier machines), and crucial treatments like calendering, drying, and, for specific applications, diamond dot pattern (DDP) coating or chemical impregnation (e.g., thermally stabilizing agents). Quality assurance is a high-cost component, focusing on continuous monitoring of thickness, density, porosity, and critically, dielectric breakdown voltage. Distribution channels subsequently move these specialized, often large-format, rolls or sheets to end-users. Direct distribution is common for high-volume orders to large transformer and motor OEMs who require specific dimensions and tight quality specifications, facilitating technical dialogue and customized orders.

Indirect distribution involves specialized industrial distributors and agents who cater to smaller repair shops, maintenance companies, and regional component manufacturers, providing inventory management and localized technical support. The downstream analysis focuses on the integration of the insulation paper into final electrical apparatus (e.g., winding the paper around copper conductors, layering it within transformer cores, or using it as slot liners in motors). The end-users—primarily utilities, high-voltage equipment manufacturers, and large industrial original equipment manufacturers—demand materials that meet international standards (like IEC and ASTM) for thermal classes and purity. Effective collaboration between paper manufacturers and equipment designers is essential in the downstream segment to ensure the insulation solution is optimized for the specific operational environment, lifespan requirement, and coolant type (mineral or ester oil).

The primary customers for electrical insulation paper are entities involved in the design, manufacturing, operation, and maintenance of electrical power apparatus. These include major Original Equipment Manufacturers (OEMs) specializing in power and distribution transformers, such as ABB, Siemens Energy, and GE, who require vast quantities of Kraft paper and pressboard for internal insulation structures. Transformer manufacturers constitute the largest segment of buyers, driven by global electricity infrastructure needs and requiring materials that guarantee long service life, typically 25 to 40 years, under thermal and electrical stress. Their purchasing criteria are centered on thermal class rating (e.g., A, E, F), dielectric purity (low moisture content, low ash), and consistency in density and mechanical properties.

Another crucial customer group consists of manufacturers of rotating electrical machinery, specifically generators and electric motors, including those for industrial applications and, increasingly, specialized traction motors for high-speed rail and electric vehicles. These buyers typically demand higher-performance synthetic insulation papers, such as aramid or composites, capable of handling higher continuous operating temperatures (Class H or N) and severe vibration stress. Within the burgeoning automotive sector, EV battery system integrators and motor assembly lines are becoming significant high-growth customers, prioritizing lightweight, flame-retardant, and ultra-reliable thin insulation materials that maximize battery energy density while ensuring safety.

Finally, cable manufacturers, particularly those specializing in high-voltage and extra-high-voltage (EHV) cables, represent a steady customer base, utilizing insulation paper as part of the overall dielectric shield system, demanding extremely consistent thickness and purity to prevent partial discharge. Utilities and grid operators, although not direct purchasers of raw paper, heavily influence purchasing decisions through specifications and procurement tenders for new equipment. Their need for minimized downtime and maximum asset longevity directly dictates the quality and thermal performance specifications required by their equipment suppliers, thereby setting the standards for insulation paper manufacturers across the value chain. Specialized repair and maintenance companies also act as key downstream customers for aftermarket replacements and refurbishment projects.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.6 Billion |

| Growth Rate | CAGR 6.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Weidmann Holding AG, DuPont, ABB, ISOVOLTA Group, KREMPEL-GROUP, DSM, SAKURA KRAFT, Tervakoski Oy, Cottrell Paper Company, SHANDONG GUOLAN ELECTRIC CO., LTD., Yantai Metron New Materials, Von Roll Holding AG, Denso Corporation, Nippon Paper Industries Co. Ltd., Okawa Electrical Insulation, Fujian Senhong Electrical Insulation Materials Co., Ltd., Elantas PDG Inc., Micarta |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the electrical insulation paper market is evolving rapidly, driven by the need for enhanced thermal performance, reduced thickness, and greater environmental compatibility. A significant development is the refinement of thermally upgraded Kraft paper (TUK), where nitrogen-containing compounds (e.g., dicyandiamide) are used to modify the cellulose structure, significantly inhibiting cellulose degradation and extending the insulation life by up to five times compared to standard Kraft paper. This enables transformers to operate efficiently at higher temperatures (Class E, 120°C) without premature failure. Furthermore, manufacturing precision has advanced significantly, utilizing sophisticated control systems to ensure micron-level thickness uniformity, which is vital for high-voltage applications where localized imperfections can lead to catastrophic partial discharge, thereby enhancing the overall reliability of the final electrical apparatus.

A key area of innovation focuses on the integration of nano-materials, particularly nano-cellulose fibers (NCF) or cellulose nanofibrils (CNF), into traditional paper matrices. This technology significantly improves the dielectric strength, thermal conductivity, and mechanical properties of the paper while potentially reducing the overall material footprint. Nano-cellulose applications are currently being explored to create hybrid papers that combine the low-cost structure of traditional cellulose with near-synthetic performance characteristics, offering a bridge solution for applications requiring high-density energy storage or compact electrical motors. Concurrently, the processing technology for synthetic materials, such as aramid paper, is being optimized to produce thinner, more flexible films (e.g., polyimide-aramid composites) specifically tailored for demanding applications in aerospace and high-performance electric vehicle motor windings, where space and weight constraints are critical design parameters.

Furthermore, technology related to fluid compatibility is crucial, particularly the transition from mineral oil to natural or synthetic ester fluids for environmental and fire safety reasons. This requires insulation papers to be specially formulated or treated to ensure optimal compatibility, minimizing swelling or chemical reactions that could compromise the dielectric interface. Diamond Dot Pattern (DDP) paper technology, where a thermally stable adhesive (often epoxy resin) is applied in a specific pattern, remains essential for forming rigid, self-supporting insulation barriers within transformers, utilizing advanced automated application systems to ensure precise placement and curing. The focus on life cycle assessment and end-of-life management is also driving the development of recyclable or easily separable composite insulation systems, integrating sustainability as a core technological parameter alongside electrical performance.

The Asia Pacific (APAC) region currently dominates the Electrical Insulation Paper Market both in terms of consumption volume and market growth rate, primarily driven by large-scale infrastructure investments in power generation and transmission networks across China, India, and Southeast Asian nations. Rapid urbanization and industrialization mandate continuous expansion and upgrade of existing grids, generating significant demand for distribution and power transformers, which are the largest consumers of cellulosic insulation paper and pressboard. Moreover, APAC is the global manufacturing hub for electronics and electric vehicles, fueling high demand for premium, synthetic insulation papers (aramid) used in capacitors, high-efficiency motors, and battery packs. Regulatory efforts in these countries to minimize transmission losses and enhance grid stability further accelerate the adoption of higher-grade insulation materials.

North America and Europe represent mature markets characterized by steady replacement demand, driven largely by the necessity to overhaul aging electricity infrastructure and integrate decentralized renewable energy sources. In North America, the focus is on smart grid deployment and enhancing grid resilience against extreme weather events, necessitating specialized insulation solutions for compact, modern substations. European market growth is heavily influenced by stringent energy efficiency directives (e.g., Ecodesign requirements) and environmental regulations, leading to a high preference for insulation systems compatible with biodegradable ester fluids. Consequently, the demand here leans toward thermally upgraded cellulosic papers and complex synthetic composites, prioritizing long-term reliability and compliance over initial material cost.

The regions of Latin America (LATAM) and the Middle East & Africa (MEA) are experiencing emerging growth, linked to investments in new power plants, mining operations, and large oil and gas projects requiring robust electrical infrastructure. In MEA, massive government spending on utility infrastructure and diversification projects drives demand for standard and high-temperature-resistant insulation paper for industrial machinery and local T&D networks. While overall volumes are lower than APAC, these regions present significant untapped potential. However, market penetration is often constrained by local manufacturing capacity and dependence on imported high-end insulation materials, making them sensitive to global supply chain disruptions and currency volatility.

Aramid paper (e.g., Nomex) is a synthetic insulation material offering significantly superior thermal stability (up to Class C, 220°C) and inherent flame resistance, making it ideal for high-performance applications like traction motors and aerospace components. Traditional Kraft paper is cellulosic, cost-effective, and typically restricted to lower thermal classes (Class A/O, 105°C), primarily used in oil-filled transformers and standard industrial equipment.

The rapid growth of the electric vehicle (EV) sector is a major driver, shifting demand towards high-performance, thin, and lightweight insulation materials, predominantly aramid papers and specialized composites. These materials are essential for managing the high operating temperatures, voltages, and vibration stresses within EV battery packs, charging systems, and highly efficient traction motors, ensuring safety and optimizing vehicle range.

Nano-cellulose technology involves incorporating cellulose nanofibrils into paper matrices to significantly enhance key performance metrics. This integration improves the dielectric strength, thermal conductivity, and mechanical strength of the paper, enabling manufacturers to produce thinner, more resilient insulation layers that facilitate equipment miniaturization and higher operational efficiency.

The Asia Pacific (APAC) region, particularly China and India, holds the highest growth potential. This is driven by aggressive governmental infrastructure initiatives focused on expanding and modernizing power transmission and distribution grids, coupled with the region's massive industrialization and its role as the global manufacturing hub for electrical components and automotive systems.

The main sustainability challenges involve the high energy consumption during the paper manufacturing process, the volatility and environmental impact of raw material sourcing (wood pulp), and the transition towards eco-friendly coolants. Manufacturers are addressing this by developing insulation papers compatible with non-toxic, biodegradable ester fluids and focusing on life cycle assessments to improve the recyclability of composite insulation systems used in power equipment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.