ID : MRU_ 437646 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

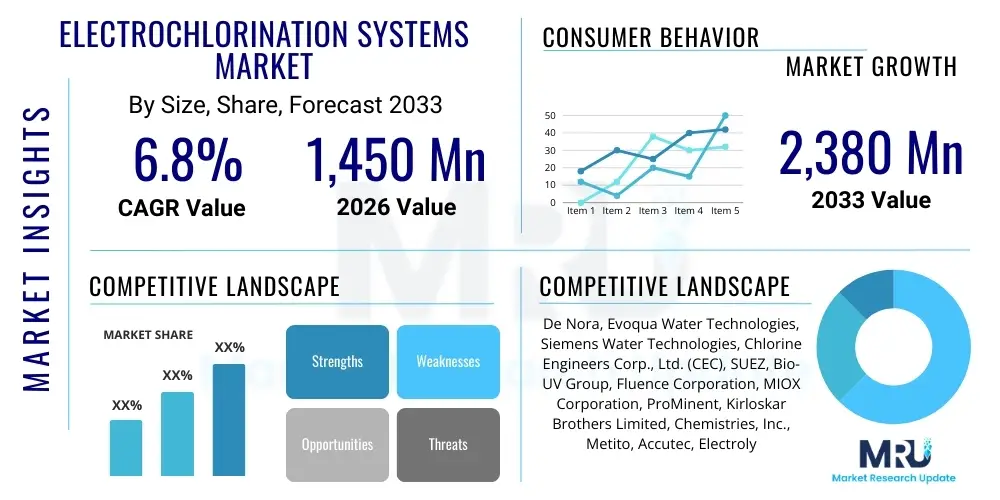

The Electrochlorination Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $1,450 Million in 2026 and is projected to reach $2,380 Million by the end of the forecast period in 2033. This robust expansion is fueled primarily by escalating global demand for effective biofouling control in industrial settings, particularly within power generation, marine ballast water treatment, and the burgeoning desalination industry. The intrinsic safety benefits and the operational efficiencies associated with on-site chlorine generation, eliminating the risks tied to transporting and storing hazardous gaseous chlorine, are key factors driving market adoption across regulated sectors worldwide.

The Electrochlorination Systems Market encompasses the provision of equipment and services for generating hypochlorite solutions through the electrolysis of natural seawater or brine (salt solution). These systems produce chlorine derivatives in situ, offering a safer and more manageable alternative to traditional bulk chlorination methods for disinfection and biofouling mitigation. Major applications span municipal water treatment, large-scale industrial cooling circuits, oil and gas operations, and maritime applications, where effective microbiological control is paramount for operational integrity and public health safety. The inherent safety of producing chlorine on demand, coupled with increasing environmental regulations mandating efficient water management, underscores the market’s positive trajectory. Key benefits include lower chemical costs over time, enhanced worker safety, and consistent disinfection efficacy, making electrochlorination a preferred solution for critical infrastructure globally.

The global Electrochlorination Systems Market is characterized by intense technological competition focused on improving cell efficiency, reducing energy consumption, and enhancing system automation capabilities. Business trends highlight a significant shift towards modular, skid-mounted systems that facilitate easier installation and deployment in remote or space-constrained environments, particularly relevant for offshore oil rigs and smaller municipal plants. Regionally, the Asia Pacific (APAC) stands out as the primary growth engine, driven by rapid industrialization, massive investments in coastal power generation, and critical needs for municipal water infrastructure development in countries like China and India. Segment trends indicate a strong preference for Seawater-based Electrochlorination Systems in coastal industrial applications due to cost efficiency, while Brine-based systems maintain dominance in inland municipal water facilities requiring precise dosage control. The convergence of strict environmental directives regarding effluent quality and the imperative for industrial asset protection against microbial induced corrosion (MIC) and biofouling are solidifying the market's long-term commercial viability.

User queries regarding the intersection of Artificial Intelligence (AI) and electrochlorination systems commonly revolve around three major themes: how AI enhances predictive maintenance to maximize uptime; the role of machine learning in optimizing electrolyte dosing and power consumption based on real-time water quality; and the integration of AI-powered diagnostics for regulatory compliance monitoring. Users seek assurance that AI integration will lead to tangible reductions in operational expenditure (OPEX) and proactive failure identification. The synthesis of these concerns suggests that the market expects AI to transition electrochlorination systems from reactive maintenance schedules to highly efficient, autonomous disinfection platforms, where variables such as temperature, salinity, and flow rates are instantly correlated to ideal current densities, maximizing efficiency and minimizing reagent consumption.

The Electrochlorination Systems Market growth is fundamentally driven by the critical need to control biofouling in large-scale cooling water systems, coupled with stringent environmental regulations worldwide that favor safer, on-site chemical generation over hazardous bulk transport. Restraints primarily involve the high initial capital expenditure required for installing these sophisticated systems, particularly large-capacity seawater units, and the persistent challenge of managing scale formation and electrode lifespan, which can elevate maintenance costs. Significant opportunities exist in the emerging sectors of green hydrogen production plants, which require substantial volumes of highly purified cooling water, and the proliferation of modular, containerized systems designed for rapid deployment in remote locations or disaster relief scenarios. These forces collectively shape the market's trajectory, emphasizing innovation in catalyst technology and modular design to overcome cost barriers and maintenance complexities, thereby facilitating wider adoption across diverse industrial landscapes.

The Electrochlorination Systems Market segmentation provides critical insights into diverse application areas and technological preferences shaping purchasing decisions across global industries. The market is primarily divided based on the Source of the Feedwater (Seawater-based or Brine-based), the Electrolytic Cell Type (Mixed Oxidant Generation or Hypochlorite Generation), and the specific Application where the disinfection or antifouling agent is utilized. Understanding these segments is vital for manufacturers to tailor system capacity, material composition, and automation features to meet the unique operational demands and regulatory environments encountered in high-salinity marine environments versus low-salinity municipal water treatment settings. The complexity inherent in managing differing feed water qualities dictates distinct technological pathways and system configurations for each identified market vertical.

The value chain for Electrochlorination Systems begins with the upstream sourcing of specialized raw materials, dominated by the procurement of high-purity titanium for manufacturing dimensionally stable anodes (DSAs), and specialized polymers for cell membranes and system piping. Key upstream activities involve intensive research and development to enhance catalytic coatings for prolonged electrode life and reduced energy consumption. Midstream activities center around the precision manufacturing, assembly, and integration of the core system components, including rectifiers, electrolytic cells, dosing pumps, and highly automated control panels. This phase requires rigorous quality control and customization based on client specifications, such as capacity requirements and feed water composition, particularly salinity and hardness levels.

Downstream analysis focuses heavily on system deployment, commissioning, and long-term maintenance and service contracts. Distribution channels are typically a mix of direct sales to large, strategic end-users (like national power utilities or major EPC firms for desalination projects) and indirect channels utilizing specialized regional distributors or system integrators who possess expertise in local regulatory compliance and installation protocols. The complexity of the technology necessitates strong technical support and spare parts availability throughout the operational life cycle, making post-sales service a crucial differentiator and a significant revenue stream within the value chain.

The most substantial value addition occurs during the integration and installation phase, where specialized engineering expertise ensures seamless operational efficiency within the client’s existing infrastructure. Direct channels ensure maximum margin capture and control over customer relationships, which is essential for customized large-scale projects. Conversely, indirect channels allow manufacturers to penetrate geographically diverse or niche markets rapidly, utilizing partners who can provide localized engineering support and meet specific regional environmental certifications.

The primary end-users and buyers of electrochlorination systems are organizations operating large-scale water-dependent infrastructure that face severe consequences from uncontrolled biofouling or require continuous, reliable disinfection. This demographic includes governmental entities managing municipal water supply, large utilities responsible for power generation, and multinational corporations in capital-intensive industries such as petrochemicals and offshore exploration. Decisions are often driven by stringent regulatory mandates concerning discharge limits and public health standards, coupled with the critical economic need to safeguard multi-million dollar assets, such as heat exchangers and cooling tower components, from degradation.

Specifically, potential customers are characterized by high volume water usage, operational criticality where downtime is prohibitively expensive, and a preference for safer chemical handling solutions compared to traditional gaseous chlorine or bulk hypochlorite delivery. These buyers prioritize systems offering longevity, minimal maintenance intervention, high energy efficiency (measured in kWh per kg of available chlorine), and advanced automation features that reduce required operator interaction. Their procurement processes typically involve detailed technical evaluations, life-cycle cost analysis (LCCA), and compliance with complex international engineering and safety standards, favoring established vendors with proven track records in high-stress industrial environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1,450 Million |

| Market Forecast in 2033 | $2,380 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | De Nora, Evoqua Water Technologies, Siemens Water Technologies, Chlorine Engineers Corp., Ltd. (CEC), SUEZ, Bio-UV Group, Fluence Corporation, MIOX Corporation, ProMinent, Kirloskar Brothers Limited, Chemistries, Inc., Metito, Accutec, Electrolytic Technologies Systems, LLC, Alfa Laval, Trojan Technologies, Ltd., Wuxi ROPV Industrial Co., Ltd., Hydro Instruments, Ltd., Sanicon AS, Cathodic Protection Co. Ltd. (CPCL) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological core of the electrochlorination market resides in the design and performance of the electrolytic cells, specifically the Dimensionally Stable Anodes (DSAs), which are critical for maximizing current efficiency and minimizing parasitic side reactions that degrade electrode performance. Advances are heavily concentrated on optimizing the composition of the catalytic coatings, typically based on platinum group metals (e.g., Ruthenium and Iridium oxide), to enhance tolerance to varying salinity levels and high temperatures while achieving lower operating voltages. Furthermore, the development of specialized cell designs, such as proprietary flow-through or tubular configurations, is aimed at reducing energy consumption (kilowatt-hours per kilogram of chlorine generated) and simplifying cleaning procedures to manage scale and hardness deposits effectively.

Beyond the core cell technology, the market landscape is being rapidly transformed by the integration of sophisticated monitoring and control systems. Modern electrochlorination units increasingly feature Supervisory Control and Data Acquisition (SCADA) systems and Programmable Logic Controllers (PLCs) that allow for precise, automated dosing adjustments based on real-time process inputs. This level of automation ensures consistent residual chlorine levels and contributes to significant cost savings by optimizing salt/brine usage and power consumption, particularly important in remote or unmanned installations. Furthermore, modularization technology, allowing for containerized, plug-and-play installation, represents a key manufacturing trend, addressing the need for rapid deployment and scalability across diverse project sizes.

The long-term technological trajectory is focused on moving towards zero-waste systems and integrating smart sensor technology to predict membrane and electrode exhaustion. Innovations in membrane materials for separating anolyte and catholyte streams, though more common in high-end hypochlorite production, are also being explored to potentially enhance overall system longevity and broaden the system’s effective operating range under challenging water conditions. The successful deployment of next-generation technology hinges on balancing CAPEX associated with premium materials (like specialized titanium alloys and catalysts) against the OPEX savings derived from higher energy efficiency and extended maintenance cycles.

The regional analysis reveals distinct market dynamics driven by varied regulatory landscapes, industrial development rates, and geographical access to seawater resources.

The primary advantage is enhanced safety. Electrochlorination generates chlorine solutions (hypochlorite) on-site and on-demand using non-hazardous feedstocks (salt or seawater), eliminating the need for the transportation, storage, and handling of highly corrosive and toxic gaseous chlorine or bulk liquid hypochlorite, thus drastically reducing chemical risk and improving worker safety compliance.

AI integration significantly lowers OPEX by enabling real-time optimization of energy consumption and feed water usage. Machine learning models adjust current density based on immediate water quality parameters, preventing over-chlorination, extending the lifespan of expensive electrolytic cells, and maximizing the efficiency of salt or seawater input.

While Brine-based systems dominate inland municipal and small industrial applications, Seawater-based electrochlorination systems are experiencing faster growth rates, primarily driven by large-scale coastal infrastructure projects, including major desalination plants, large power stations, and mandatory compliance in marine ballast water treatment, particularly in the rapidly industrializing APAC region.

The two main restraints are the high initial Capital Expenditure (CAPEX) required for procurement and installation of large, customized systems, and the ongoing maintenance challenge related to electrode fouling, scaling, and the periodic replacement of expensive Dimensionally Stable Anodes (DSAs) due to wear and tear.

MOG systems generate a complex mix of oxidizing agents, offering potentially superior disinfectant properties and residual efficacy compared to HGC systems, which produce only sodium hypochlorite. MOG is often preferred in specialized applications, such as certain industrial wastewater treatments, where higher potency against resistant microorganisms or complex organic loads is required.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.