ID : MRU_ 431960 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

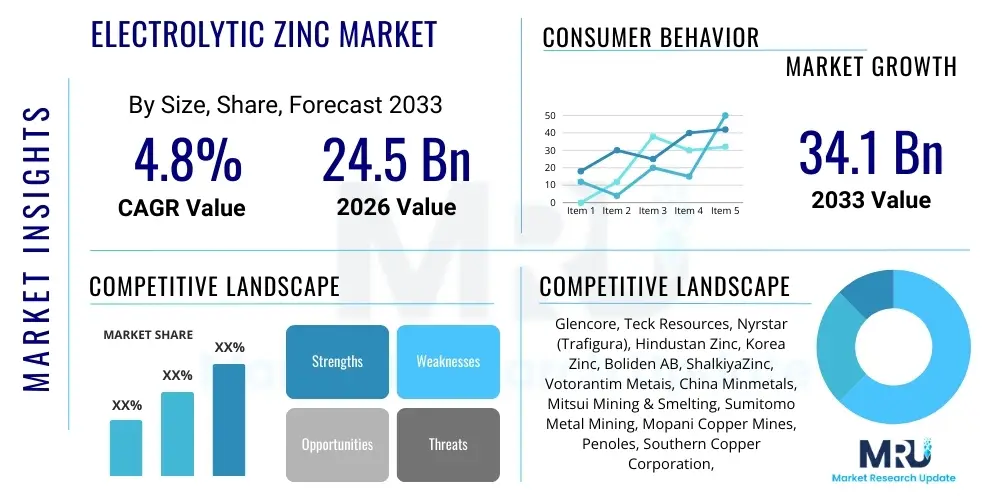

The Electrolytic Zinc Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at $24.5 Billion in 2026 and is projected to reach $34.1 Billion by the end of the forecast period in 2033.

The Electrolytic Zinc Market encompasses the production and trade of high-purity zinc metal derived primarily through the hydrometallurgical process, specifically electrowinning. This method, involving leaching zinc concentrates and subsequently depositing pure zinc onto cathodes using electrical current, accounts for the vast majority of global primary zinc production due to its ability to yield zinc metal with purities often exceeding 99.995%. Electrolytic zinc is the standard raw material required for applications demanding stringent quality control, such as high-grade die-casting alloys, specific chemical formulations, and, most critically, the galvanization process which protects steel structures from corrosion. The robust demand for galvanized steel in infrastructure development, automotive manufacturing, and renewable energy installations serves as the foundational driver for this market.

Product description highlights high-grade special high grade (SHG) zinc, which is the primary output of the electrolytic process. SHG zinc's superior characteristics, including minimal impurities like lead and cadmium, make it indispensable for galvanization and continuous hot-dip processes where alloy consistency is paramount. Major applications center around corrosion protection (galvanizing), where zinc forms a protective barrier and acts as a sacrificial anode, extending the lifespan of steel assets significantly. Secondary, yet vital, applications include its use in brass manufacturing, zinc oxide production (used in rubber, ceramics, and pharmaceuticals), and in zinc-air batteries, which are gaining traction in the energy storage sector.

The primary benefits of electrolytic zinc include its high purity, essential for manufacturing reliable end-products, and its consistent availability through standardized, large-scale industrial processes. Key driving factors include escalating global infrastructure spending, particularly in emerging economies of Asia Pacific, heightened environmental regulations pushing for longer-lasting materials, and the rapid expansion of the automotive sector, which utilizes galvanized steel for enhanced vehicle safety and longevity. Furthermore, technological advancements in the electrowinning process, focusing on energy efficiency and reduced operational costs, are continually supporting market expansion and competitiveness against alternative zinc production methods.

The global Electrolytic Zinc Market is characterized by steady growth driven by fundamental demands in infrastructure and corrosion protection, tempered by fluctuating energy costs and mineral supply chain stability. Business trends indicate a strong focus on sustainability, with major producers investing heavily in renewable energy integration to power the highly energy-intensive electrowinning process, aiming to achieve lower carbon footprints (Green Zinc). Vertical integration, especially among large mining conglomerates, remains a critical strategic approach to mitigate raw material price volatility (zinc concentrates) and secure long-term supply. Furthermore, there is a discernible trend towards digitalization in smelter operations, utilizing advanced analytics and automation to optimize current efficiency, reduce operational downtime, and enhance metal recovery rates, thus improving overall plant productivity and efficiency margins.

Regional trends demonstrate Asia Pacific (APAC) as the undisputed dominant region, fueled by massive steel production capacity and unprecedented urbanization driving demand for galvanized products in China, India, and Southeast Asia. North America and Europe, while mature, exhibit demand stability driven by stringent environmental standards necessitating high-purity zinc for complex alloys and specific chemical applications, alongside strategic investments in infrastructure renewal programs. Meanwhile, Latin America and the Middle East & Africa are emerging as significant regions, not only in terms of production capacity augmentation but also in localized consumption growth tied to expanding domestic construction and industrial sectors.

Segment trends reveal that the Galvanizing segment maintains the largest market share, but the Chemical Applications segment (especially zinc oxide and zinc sulfate) is projected to witness above-average growth, driven by expansion in pharmaceutical, agricultural, and specialized battery sectors. Furthermore, the Special High Grade (SHG) purity level dominates the product segment, reflecting the industry's continuous need for the highest purity electrolytic metal for critical, high-performance end-use applications. Innovations in secondary production techniques (recycling of zinc-containing residues) are also influencing supply dynamics, positioning recycled electrolytic zinc as an increasingly important complementary source of metal, though primary electrolytic production remains foundational.

User inquiries regarding the intersection of Artificial Intelligence (AI) and the Electrolytic Zinc Market frequently focus on two main areas: optimizing the energy-intensive electrowinning process and predicting volatile commodity prices and raw material availability. Users are keen to understand how AI-driven predictive maintenance can reduce operational risks in harsh smelting environments, minimize unplanned shutdowns, and maximize cathode quality and current efficiency—a direct measure of energy conversion effectiveness. Concerns also revolve around the capital investment required for implementing AI-driven sensor networks and proprietary algorithms capable of handling complex electrochemical parameters unique to each smelter’s electrolyte composition. Expectations are high that AI can provide real-time control adjustments previously unattainable, leading to significant reductions in the enormous electrical load required for zinc deposition, thereby dramatically improving the overall financial and environmental performance of production facilities.

The implementation of machine learning models in process control allows for the real-time adjustment of current density, electrolyte temperature, and impurity levels, which are critical variables in maximizing the yield and minimizing energy consumption during electrowinning. AI algorithms analyze vast datasets encompassing historical operational metrics, sensor readings, and external variables (like ambient temperature and grid stability) to predict optimal operating conditions and preemptively identify equipment failures, such as anode or cathode degradation or pump malfunctions, before they lead to catastrophic failure. This shift from reactive to predictive maintenance significantly enhances asset utilization and ensures sustained high-purity output required by premium customers.

Beyond operational efficiency, AI is revolutionizing supply chain management and strategic sourcing. Predictive analytics tools are employed to forecast short-term and long-term zinc concentrate prices, copper and sulfur by-product values, and associated logistical costs, enabling procurement managers to secure contracts under favorable terms. Furthermore, AI helps in simulating the impact of regulatory changes or geopolitical events on regional supply chains, providing producers with enhanced visibility and resilience. The ultimate impact of AI is transforming electrolytic zinc production from a traditional chemical engineering operation into a data-driven manufacturing process, ensuring sustainability and cost leadership in a competitive global commodity market.

The Electrolytic Zinc Market is propelled by robust global demand for corrosion protection (Driver), particularly from the construction and automotive sectors, yet faces significant challenges related to the energy-intensive nature of its production (Restraint). Opportunities lie in the transition towards green zinc and the expansion into niche high-tech applications like advanced batteries. The overall dynamics are strongly influenced by the Impact Force of fluctuating raw material and energy prices, coupled with stringent environmental regulations demanding high capital expenditure for compliance.

Key drivers include the global push for infrastructure development, especially in emerging economies requiring vast amounts of galvanized steel for bridges, roads, and utilities. The automotive sector's continuous shift towards lighter, more durable, and corrosion-resistant materials also sustains demand for high-purity electrolytic zinc alloys. Furthermore, the growing application of zinc in specialty chemicals and pharmaceuticals, along with the nascent but promising zinc-ion battery market, provides diversified growth avenues. Restraints primarily involve the high cost and volatility of electricity, which is the single largest operating expense in electrowinning, making sustained profitability sensitive to energy market instability. Additionally, the declining grade and increasing complexity of processing new zinc mineral reserves present technical challenges and elevated extraction costs, potentially limiting the accessible raw material supply.

Opportunities center on technological advancements that enhance energy efficiency, such as advanced cell design, pulsating current usage, and sophisticated electrolyte control systems. The industry's pursuit of "Green Zinc," certified using renewable energy sources, opens up premium market segments, especially in environmentally conscious regions like Europe. The primary impact forces shaping the competitive landscape are the stringent global environmental and safety regulations, particularly regarding sulfur dioxide emissions from the roasting process and hazardous waste management. These regulations require continuous investment in abatement technologies, increasing the barrier to entry and favoring established players with substantial capital. Geopolitical stability affecting major zinc mining regions also exerts a powerful influence on concentrate supply and price dynamics, necessitating robust risk management strategies across the value chain.

The Electrolytic Zinc Market is comprehensively segmented based on its Purity Level, Application, and Geographic Region, providing a detailed perspective on current consumption patterns and future growth trajectories. Purity segmentation is crucial as it directly determines the end-use suitability and pricing structure of the metal, with Special High Grade (SHG) dominating due to its requirement in continuous galvanizing lines. Application segmentation highlights the reliance on construction and automotive sectors, while regional segmentation underscores the shift of production and consumption dominance towards Asia Pacific, reflecting global industrialization trends and infrastructure development pace.

The value chain for electrolytic zinc is highly complex and integrated, starting with the upstream mining and concentration of zinc sulfide ores. Upstream activities involve exploration, extraction, and beneficiation processes to produce zinc concentrate (typically 50-60% zinc content). The profitability at this stage is highly dependent on ore body grade, extraction efficiency, and fluctuating base metal prices. Key players often pursue vertical integration to secure stable concentrate supply, as zinc smelting capacity globally often exceeds readily available high-quality concentrate, leading to significant tolling arrangements and market price sensitivity to mining output.

The midstream segment involves the energy-intensive processing, encompassing roasting (to convert sulfides to zinc oxide), leaching, purification, and the final electrowinning process, which defines the electrolytic zinc product. This stage is dominated by large-scale smelters, many located geographically close to major energy sources or ports. Distribution channels are essential for moving the final product (zinc ingots/jumbos) to downstream consumers. Direct distribution involves long-term contracts between large producers and major galvanizers or die-casters, ensuring consistent supply volumes and quality specifications. Indirect distribution utilizes LME-registered warehouses and metal traders, providing necessary liquidity and market access for smaller or regional buyers, particularly important for managing immediate inventory needs.

Downstream analysis focuses on the end-use industries, predominantly galvanizers who convert the pure zinc into protective coatings for steel, and specialized alloy manufacturers. The direct customer relationship provides stability, whereas the indirect market is impacted by global construction cycles and automotive production volumes. The chain emphasizes high quality; any impurity introduced at the electrowinning stage can compromise the downstream application, reinforcing the competitive advantage of producers maintaining ultra-high-purity standards. The efficiency of the distribution system, particularly in Asia Pacific, relies heavily on localized logistics networks to minimize transport costs and delivery times to highly dispersed manufacturing clusters.

The primary consumers of electrolytic zinc are large industrial entities whose operations fundamentally depend on the material's anti-corrosive properties and high purity characteristics. The largest segment of end-users is the steel industry, specifically companies operating hot-dip galvanizing lines, ranging from continuous strip galvanizers supplying automotive and construction coil, to general galvanizers handling structural steel components. These buyers prioritize consistency in SHG zinc quality, as minor impurities can severely impact the adherence and performance of the zinc coating, leading to substantial production losses.

Another crucial customer segment includes manufacturers of zinc-based alloys, particularly specialized die-casting companies. These firms produce components for the automotive, electronics, and appliance industries (e.g., door handles, carburetor parts, electronic housings). For die-casting, high purity is non-negotiable to achieve the necessary flow properties and mechanical strength of the cast parts. Furthermore, chemical manufacturers represent a growing potential customer base, utilizing electrolytic zinc to produce zinc oxide for tires, rubber, sunscreens, and pharmaceuticals, where metal contamination must be strictly avoided.

Emerging buyers include specialized battery manufacturers, particularly those developing and scaling zinc-air or next-generation zinc-ion battery technologies, leveraging zinc's high energy density and safety profile. These advanced applications demand exceptionally stringent purity specifications, often requiring customized metal grades. Ultimately, the market is driven by B2B transactions where long-term supplier relationships, guaranteed purity certificates, and reliable logistical frameworks are far more critical than short-term price fluctuations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $24.5 Billion |

| Market Forecast in 2033 | $34.1 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Glencore, Teck Resources, Nyrstar (Trafigura), Hindustan Zinc, Korea Zinc, Boliden AB, ShalkiyaZinc, Votorantim Metais, China Minmetals, Mitsui Mining & Smelting, Sumitomo Metal Mining, Mopani Copper Mines, Penoles, Southern Copper Corporation, Vedanta Resources, MMG Limited, Nexa Resources, Yunnan Metallurgical Group, Noranda, BMM Zinc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The electrolytic zinc production process is technologically mature, but continuous innovation focuses on two critical areas: improving energy efficiency and enhancing process control to handle increasingly complex and impure raw materials (zinc concentrates). The core technology remains the roast-leach-electrowin (R-L-E) process. Current R&D efforts center on optimizing the electrowinning cell house design, specifically moving towards larger cell sizes and automated cathode handling systems to reduce manual labor and improve safety. Furthermore, optimizing electrolyte purification methods, which use jarosite or goethite precipitation, is essential for maintaining the ultra-high purity required for SHG zinc, especially when processing secondary or complex feedstocks.

A key technological shift involves advanced digital control systems. Modern smelters utilize sophisticated sensors and data analytics, often integrated with AI and machine learning, to precisely manage variables like acid concentration, temperature, and current density in real-time. This dynamic control maximizes current efficiency, a measure of how effectively electrical energy is converted into deposited zinc, directly impacting profitability. Innovations in anode technology, particularly the development of dimensionally stable anodes (DSAs) or alternative materials, aim to reduce maintenance cycles and minimize the contamination risk posed by conventional lead-silver anodes.

Furthermore, significant technological investments are being channeled into improving environmental performance. The transition towards pressure leaching, rather than traditional roasting, for specific complex concentrates helps manage sulfur dioxide emissions more effectively and allows for higher metal recovery from challenging ores. Technologies focused on effluent treatment, specifically methods for stabilizing and safe disposal or beneficial reuse of jarosite/goethite residues, are vital for securing operational licenses and meeting escalating global sustainability standards. These technologies collectively aim to ensure the electrolytic zinc process remains the most viable and environmentally responsible method for primary zinc production.

The global electrolytic zinc market exhibits pronounced regional disparities in terms of production capacity, consumption intensity, and regulatory environment. These factors significantly influence localized market dynamics and supply chain strategies. Understanding the regional market landscape is crucial for strategic planning, especially concerning capital investment in new smelting capacity and securing long-term supply contracts.

APAC is the largest and fastest-growing regional market for electrolytic zinc, dominated heavily by China, which accounts for over half of the global consumption and production capacity. This supremacy is fueled by China’s immense capacity for steel production and its unparalleled infrastructural development boom, necessitating vast quantities of galvanized steel for construction, manufacturing, and automotive industries. Countries like India, South Korea, and Vietnam are also experiencing strong industrial growth, driving sustained regional demand. The key characteristic of the APAC market is its focus on high-volume production, often utilizing large, highly integrated smelters. While cost competitiveness is essential, increasing environmental scrutiny in China is forcing many older facilities to upgrade or close, favoring technologically advanced, efficient operations that specialize in SHG production. Logistics management across vast geographies remains a strategic challenge, though the proximity of major producers to end-users often provides a competitive edge.

The European market is mature and technologically advanced, characterized by stringent environmental regulations and a high premium placed on certified, sustainable production, often referred to as "Green Zinc." Electrolytic zinc producers in Europe, such as those in Belgium, Germany, and Scandinavia, focus heavily on energy efficiency and low-carbon operation, often utilizing renewable energy sources to power their smelters. Demand stability is driven by the European automotive sector and complex manufacturing industries that require SHG zinc for high-end alloys and brass. Operational profitability in this region is acutely sensitive to natural gas and electricity prices, compelling companies to invest continuously in process optimization and hedging strategies to mitigate volatility. Regulatory compliance regarding SO2 emissions and hazardous waste is a non-negotiable factor shaping capital expenditure decisions.

North America maintains significant production capacity and stable demand, predominantly driven by the robust construction sector, infrastructure repair, and durable goods manufacturing in the United States. Key producers benefit from strong vertical integration, owning both mining and smelting assets, which provides stability against concentrate price swings. The market prioritizes supply reliability and quality assurance for large domestic infrastructure projects. Recent governmental emphasis on revitalizing domestic manufacturing and securing critical mineral supply chains has stimulated interest in both primary and secondary (recycled) zinc production within the region. However, competition from high-volume imports, particularly from Canada and overseas, requires domestic producers to maintain competitive cost structures despite higher regulatory compliance costs.

Latin America is characterized by significant zinc mining activity, making it a crucial source of raw material (zinc concentrate) globally. Countries like Peru, Mexico, and Brazil host major integrated mining and smelting operations. While the region is a net exporter of concentrates, localized demand for electrolytic zinc is steadily rising, tied to internal economic growth, urbanization, and domestic construction projects. The market faces unique challenges related to infrastructure logistics and localized energy supply volatility. However, the abundance of mineral reserves ensures that the region will remain a key global production hub, focused on expanding smelting capacity to capture higher value-added steps within the domestic supply chain.

MEA is an emerging consumer of electrolytic zinc, driven primarily by ambitious infrastructure and construction projects in the GCC countries and industrialization initiatives in South Africa. While regional production capacity is limited compared to APAC, local demand is showing strong growth potential. The Gulf region's reliance on large-scale steel structures (e.g., ports, desalination plants) necessitates high-quality anti-corrosive coatings, ensuring stable demand for galvanized products. South Africa holds important mineral reserves and established mining infrastructure, supporting regional supply, but often faces energy supply constraints that challenge continuous high-volume production.

Electrolytic zinc (produced via electrowinning) is chemically purer, typically yielding Special High Grade (SHG) zinc (99.995% purity or higher). Thermal zinc (produced via distillation) usually has lower purity. Electrolytic zinc dominates because its superior purity is essential for continuous galvanizing lines and high-specification die-casting alloys where even minor impurities like lead or cadmium can compromise material performance and mechanical integrity. The electrolytic process allows for better control over contamination.

Energy, primarily electricity, represents the single largest operational expenditure (typically 30-40% of total smelting costs) in the electrowinning process. Consequently, global competitiveness is highly sensitive to regional power prices and grid stability. Facilities with access to cheaper, long-term power contracts or self-generated renewable energy (e.g., hydroelectric) gain a substantial cost advantage, directly impacting the final delivered price of the metal and regional trade flows.

The highest growth potential is anticipated in the Batteries segment, specifically for next-generation zinc-air and zinc-ion technologies. While still emerging, these applications demand stringent purity levels attainable only through the electrolytic process. The rapid scaling of the energy storage market, driven by renewables and electric vehicles, positions zinc-based battery chemistries as a promising, non-traditional source of high-volume demand.

The primary environmental challenges involve managing emissions and waste from the roasting and purification stages. Smelters must control sulfur dioxide (SO2) emissions, usually by converting it into sulfuric acid, and safely manage massive volumes of hazardous residues (like jarosite or goethite precipitates) generated during electrolyte purification. Compliance with increasingly stringent global regulations requires continuous, significant capital investment in advanced gas scrubbing and waste stabilization technologies.

The market is responding by launching "Green Zinc" initiatives, which involve certifying zinc produced using substantial inputs of renewable energy (hydro, solar, wind) to power the electrowinning process. Major producers are investing in long-term power purchase agreements (PPAs) for renewables and optimizing process efficiency through AI and digitization to reduce overall energy intensity, aiming to achieve a lower carbon footprint to meet demand from environmentally conscious buyers in regions like Europe.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.