ID : MRU_ 434308 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

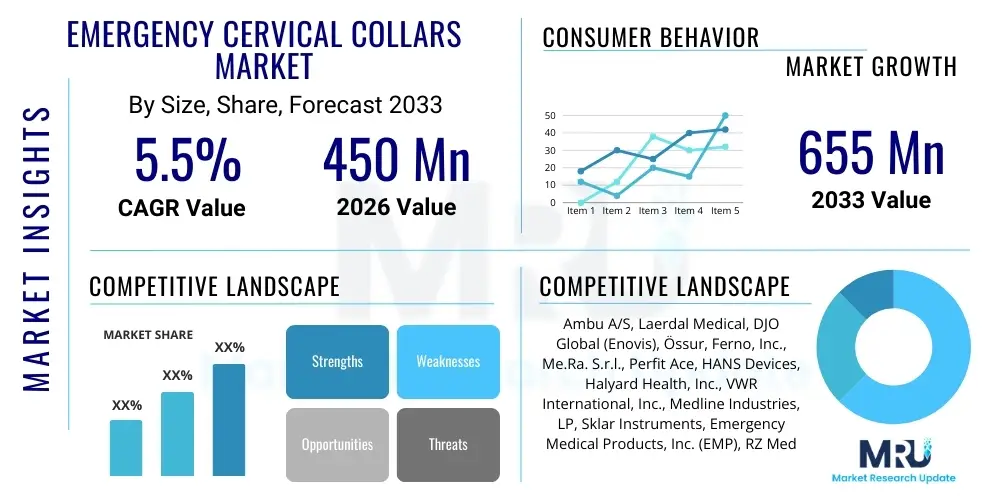

The Emergency Cervical Collars Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 655 Million by the end of the forecast period in 2033.

The Emergency Cervical Collars Market encompasses the manufacturing and distribution of specialized medical devices designed for the immediate immobilization and stabilization of the cervical spine in trauma patients. These devices are critical in pre-hospital and emergency department settings to prevent secondary spinal cord injury following accidents, falls, or sudden forceful impacts. The primary function of an emergency cervical collar, often referred to as a C-collar, is to limit flexion, extension, lateral bending, and rotation of the neck, maintaining the neck in a neutral, inline position until definitive medical imaging and diagnosis can be achieved. Products range from rigid, adjustable, and semi-rigid designs, tailored to fit diverse patient anatomies and trauma scenarios, ensuring optimal patient safety during transport and initial assessment. The fundamental necessity for reliable spinal immobilization in potential cervical trauma cases serves as the foundational demand driver for this critical medical device market.

The widespread application of emergency cervical collars spans critical care transport, sports medicine, military field operations, and routine hospital emergency services. Major applications include stabilization following motor vehicle accidents, pedestrian collisions, severe falls, and blunt force trauma to the head or neck area. The benefits of using these devices are paramount, primarily focusing on reducing the risk of neurological damage by minimizing movement of potentially fractured or unstable vertebrae. Key advantages include ease of application by first responders, standardized sizing mechanisms that reduce inventory complexity, and radiolucent materials allowing for uninterrupted diagnostic imaging like X-rays and CT scans without the need for device removal, thereby streamlining critical care pathways. Innovations focused on patient comfort and minimizing pressure ulcers are also increasingly integrated into modern designs.

The market growth is primarily driven by the increasing global incidence of road traffic accidents and sports-related head and neck injuries, particularly in rapidly urbanizing regions. Furthermore, enhanced public awareness and stricter adherence to advanced trauma life support (ATLS) protocols among emergency medical service (EMS) providers worldwide mandate the routine use of cervical immobilization devices, even when spinal injury is only suspected. Technological advancements, such as the introduction of lightweight, adjustable, and disposable collars, are also significantly contributing to market expansion by improving efficiency and reducing the potential for cross-contamination. Government initiatives aimed at upgrading emergency healthcare infrastructure and increasing investments in trauma centers further solidify the market's positive growth trajectory throughout the forecast period.

The Emergency Cervical Collars Market demonstrates robust expansion driven by stringent safety protocols and the rising global burden of traumatic injuries. Business trends reveal a strong emphasis on product differentiation through material science, focusing on creating lighter, more hygienic, and easier-to-apply designs that accommodate various clinical needs, particularly adjustable models dominating the pre-hospital care segment. Strategic collaborations between manufacturers and major EMS providers are streamlining procurement and standardization processes. Companies are also heavily investing in automation and sterilization technologies within manufacturing to meet high regulatory standards imposed by bodies like the FDA and CE. Furthermore, the shift towards disposable options is gaining traction, prompted by concerns related to infection control, particularly in high-volume trauma settings, influencing supply chain adjustments towards high-throughput production lines.

Regionally, North America maintains the leading position due to its highly developed emergency medical infrastructure, standardized trauma care guidelines, and significant expenditure on advanced medical devices. However, the Asia Pacific region is forecast to exhibit the highest CAGR, propelled by rapid infrastructure development, increasing urbanization leading to higher accident rates, and substantial governmental investments in improving access to basic and advanced emergency services in countries like China and India. Europe also represents a mature market, characterized by stable demand and a focus on integrating ergonomic and sustainable designs into their healthcare systems. The market dynamics in Latin America and MEA are largely dictated by imports and non-governmental organization (NGO) activities supporting trauma management training and equipment donation.

Segmentation trends indicate that hospitals and trauma centers remain the largest end-users, driving demand for inventory stability and high-quality, reusable products, while EMS and military segments favor lightweight, robust, and often single-use adjustable collars that minimize inventory complexity on site. By product type, adjustable collars are replacing fixed-size models due to their versatility and ability to provide a precise fit, which is crucial for effective stabilization and patient compliance. The material segment sees continued dominance by durable plastics and high-density foam combinations, though the use of advanced polymer composites for better radiolucency and reduced skin irritation represents a key area of future material innovation and differentiation among leading market players seeking competitive advantage.

User queries regarding AI's influence on the Emergency Cervical Collars Market primarily center on three areas: how AI can enhance the diagnostic speed and accuracy leading to quicker deployment decisions, the role of AI in optimizing collar design for personalized fit and injury type, and how AI can improve logistics and inventory management for emergency services. Users are keen to understand if AI-powered trauma assessment tools, potentially integrated into ambulance telemedicine systems, could automate the initial decision to apply or adjust a cervical collar, reducing human error under pressure. There is also significant interest in AI applications in predicting material stress and failure points, leading to ultra-reliable designs, as well as optimizing the supply chain to ensure critical stock availability during mass casualty incidents, reflecting expectations for greater efficiency and reliability in high-stakes clinical environments.

While AI does not directly interact with the physical application of the collar, its indirect impact on the market value chain and clinical decision-making is substantial. AI algorithms are increasingly being used in conjunction with imaging diagnostics (CT scans, X-rays) to rapidly detect subtle cervical spine injuries, providing crucial guidance to attending physicians on the need for continued immobilization or safe removal of the collar. This reduces the time a patient remains potentially uncomfortable or restricted unnecessarily. Furthermore, predictive modeling, utilizing machine learning on vast datasets of trauma kinetics and patient outcomes, is informing the next generation of collar biomechanics. Manufacturers are leveraging these insights to fine-tune energy absorption rates and pressure distribution points, moving towards designs that offer maximum protection while minimizing negative side effects like restricted venous return or skin breakdown.

In the realm of operations and logistics, AI algorithms are vital for demand forecasting within emergency medical supply chains. By analyzing historical trauma rates, geographic accident hotspots, and seasonal variations, AI tools help hospitals and regional EMS providers maintain optimized inventory levels of various collar types, preventing stockouts during peak trauma seasons or unexpected events. This operational efficiency ensures that the necessary stabilization equipment is always immediately available, a key performance indicator in emergency care. The application of AI in analyzing post-market surveillance data also allows manufacturers to quickly identify and rectify design flaws or usage errors, leading to faster iteration cycles and overall product quality improvement, thereby enhancing trust and reliability in the product line.

The Emergency Cervical Collars Market is fundamentally shaped by a dynamic interplay of driving forces (D), restrictive challenges (R), and latent opportunities (O), all magnified by high-impact forces that define emergency medical protocols. The primary drivers include the escalating global prevalence of traumatic incidents, specifically high-velocity vehicular accidents and increasing participation in extreme sports, necessitating immediate, standardized spinal protection. Alongside this, the continuous strengthening of clinical guidelines globally, especially those originating from bodies like the National Association of Emergency Medical Technicians (NAEMT), mandates specific protocols for cervical spine assessment and immobilization. These regulatory and protocol drivers ensure consistent market demand irrespective of economic fluctuations. Furthermore, continuous innovation in device materials and ergonomics, making collars lighter and easier to use, further accelerates adoption.

Restraints impeding optimal market penetration include the challenge of improper application and sizing, which, if incorrect, can exacerbate rather than prevent injury, leading to significant liability concerns and resistance among some advanced practitioners. The cost differential between basic foam collars and highly specialized, adjustable rigid collars poses an economic barrier, particularly in low and middle-income countries (LMICs) where resource allocation for advanced medical devices is severely constrained. Moreover, growing clinical debates regarding the necessity of routine immobilization for all minor trauma cases—prompted by concerns over complications such as elevated intracranial pressure (ICP) and difficulty in airway management—create market uncertainty and demand for more sophisticated, context-aware screening tools that might reduce reliance on universal collar application.

Opportunities for future growth are significant, centered on the development of smart cervical collars incorporating integrated sensors for real-time monitoring of spinal alignment and patient physiology, providing critical feedback to clinicians during transport. The shift towards sustainable and biodegradable material options addresses growing environmental concerns within healthcare systems, offering a distinct marketing advantage. Furthermore, the immense untapped market potential in developing nations, coupled with increasing international aid and training focused on establishing robust trauma care systems, presents a long-term commercial opportunity. The impact forces defining the market are heavily focused on product liability, regulatory oversight, and the rapid pace of technological integration in pre-hospital care, making adherence to ISO standards and clinical evidence paramount for market sustainability and success.

The Emergency Cervical Collars Market is comprehensively segmented based on product type, material, application, and end-user, allowing for precise market analysis tailored to specific healthcare environments and clinical needs. The segmentation by product type—including adjustable, non-adjustable, and specialty traction collars—is crucial, as product flexibility dictates suitability for diverse logistical scenarios, with adjustable collars commanding a premium due to their inventory efficiency. Material segmentation reflects the trade-off between cost, durability, and radiolucency, typically comprising foam, rigid plastic, and composite materials. Application segmentation distinguishes between usage in high-trauma environments like emergency medical services (EMS) and stable clinical settings such as hospitals or specialty clinics, where the requirements for portability and robustness vary significantly, driving distinct demand patterns across these segments.

The end-user segmentation is critical, delineating demand from institutional buyers such as hospitals and trauma centers versus specialized external service providers like EMS agencies, military units, and sports medical teams. Hospitals generally purchase in large volumes, focusing on standardized, reusable devices that fit strict budget requirements and infection control protocols. Conversely, EMS and military procurement prioritizes lightweight, rapid-deployment, and often disposable devices that ensure readiness in unpredictable field conditions. Understanding these buyer characteristics is essential for manufacturers to tailor their marketing and distribution strategies effectively, recognizing that the clinical environment dictates the primary features sought in an emergency collar, influencing factors such as radiolucency, quick-release mechanisms, and overall ease of cleaning or disposal.

The value chain for the Emergency Cervical Collars Market initiates with upstream activities heavily focused on sourcing raw materials, primarily specialized polymers, medical-grade plastics (HDPE), and high-density foam, along with advanced components for adjustable mechanisms and fastening systems. Upstream analysis involves rigorous quality control over materials to ensure biocompatibility, radiolucency, and structural integrity under trauma stress. Key activities include material procurement, polymerization processes, and initial component molding. The efficiency and cost-effectiveness at this stage are critical, directly influencing the final product margin, with major manufacturers often vertically integrating some component production or maintaining strong, long-term contracts with specialized raw material suppliers to mitigate volatility in commodity prices and guarantee supply chain robustness required for constant emergency readiness.

Midstream activities encompass the core manufacturing process, involving injection molding, assembly, sterilization, and rigorous quality assurance testing, ensuring compliance with stringent medical device regulations (e.g., ISO 13485). This stage sees significant investment in automated assembly lines, particularly for high-volume adjustable collars. Downstream activities focus intensely on distribution channels. Distribution is predominantly indirect, utilizing specialized medical device distributors and regional healthcare supply chain aggregators who handle warehousing and logistics to ensure prompt delivery to dispersed end-users like rural EMS stations and large urban hospitals. Direct distribution is typically reserved for major government tenders (military/national health systems) or highly specialized, customized products, although a small percentage of sales are handled directly by manufacturers through dedicated sales teams to maintain closer client relationships and control branding.

The final element involves marketing, sales, and post-sales support, emphasizing comprehensive training for end-users (first responders, nurses, physicians) on proper application techniques to maximize device effectiveness and minimize patient risk. The distribution channel selection hinges on geographical reach and the required speed of delivery, acknowledging that emergency collars are critical, often life-saving devices requiring rapid replenishment capabilities. Indirect channels offer wider market access and localized inventory management, crucial for emergency preparedness, while direct channels allow for better margin control and focused relationship building with key institutional customers who demand high levels of technical support and customized inventory solutions.

Potential customers for the Emergency Cervical Collars Market are diverse institutions and specialized personnel who operate within the trauma care ecosystem, necessitating immediate and reliable spinal immobilization capabilities. The largest segment of end-users comprises major hospitals and dedicated trauma centers, which require large inventories of both reusable and disposable collars across various sizes and types to manage the continuous influx of emergency patients. These institutions serve as the primary purchasing decision-makers, prioritizing quality, compatibility with existing imaging equipment, and stringent infection control features. Their buying decisions are influenced by clinical consensus, procurement contracts, and long-term cost of ownership, making them key targets for large-volume contract sales and bundled purchasing agreements for comprehensive medical supplies.

A second major customer segment includes Emergency Medical Service (EMS) agencies, both public and private, who are responsible for initial patient assessment and transport. EMS providers prioritize ease of use, quick application mechanisms, and durability in challenging field environments. They are heavy consumers of adjustable and disposable collars due to the need for rapid deployment and minimizing contamination risks associated with multi-patient use. Furthermore, military and defense medical units represent another high-priority customer base, requiring rugged, lightweight collars suitable for deployment in austere and remote settings. Their procurement cycles are often driven by specific tender requirements focusing on durability, low profile, and operational suitability, distinguishing their needs significantly from standard civilian healthcare providers, requiring specialized product lines and distribution logistics tailored to defense supply chains.

Finally, niche end-users such as specialized sports medicine clinics, athletic training facilities, and industrial safety departments also constitute important buyers, particularly for situations involving potential concussions or workplace accidents where neck stabilization is a standard precautionary measure. These buyers often seek lighter, more comfortable designs suitable for prophylactic use or immediate sideline management before definitive transfer to a hospital. Training academies and simulation centers also purchase collars for educational purposes. Overall, the buying behavior across these segments reflects a shared need for products that are clinically effective, easily stored, and compliant with the highest standards of trauma protocol adherence, underlining the market’s reliance on trust and proven reliability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 655 Million |

| Growth Rate | 5.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Ambu A/S, Laerdal Medical, DJO Global (Enovis), Össur, Ferno, Inc., Me.Ra. S.r.l., Perfit Ace, HANS Devices, Halyard Health, Inc., VWR International, Inc., Medline Industries, LP, Sklar Instruments, Emergency Medical Products, Inc. (EMP), RZ Medizintechnik GmbH, Stifneck Select. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Emergency Cervical Collars Market is rapidly evolving, moving beyond simple foam and plastic constructs towards integrated, high-performance devices. A core focus lies in material science, utilizing advanced polymer composites that offer superior strength-to-weight ratios while ensuring complete radiolucency. This innovation is crucial, as it allows for clear diagnostic imaging (MRI, CT scans) without the need for collar removal, adhering to the principle of "image before movement." Furthermore, the development of specialized hypoallergenic and breathable padding materials is addressing the long-standing clinical concern of pressure ulcer formation and skin breakdown, particularly during prolonged immobilization or transport times, thereby directly impacting patient comfort and outcomes.

Another significant technological shift involves the integration of rapid prototyping techniques, primarily additive manufacturing (3D printing). While 3D printing is not yet widely used for high-volume standard collar production, it is increasingly being leveraged in the design phase for quick iteration of ergonomic features and specialized sizing options. This technology offers the potential for true customization, allowing for patient-specific collar fabrication in complex trauma scenarios where standard sizing fails. Coupled with sophisticated biomechanical modeling software, manufacturers are able to simulate various impact forces and adjust material thickness and geometry precisely, ensuring optimal stabilization performance across a wide range of patient body types and injury patterns, resulting in greater clinical trust in the device.

The emerging frontier involves "smart" collars, which represent the convergence of medical devices and IoT technology. These devices incorporate micro-sensors, such as gyroscopes or accelerometers, capable of monitoring the patient’s head and neck movements in real-time. This feedback mechanism alerts medical staff if the stabilization is compromised during transport, ensuring continuous cervical alignment. While still in nascent stages, this technology promises to revolutionize spinal immobilization protocols by providing objective data rather than relying solely on visual assessment. Additionally, improved fastening and adjustment systems, utilizing ratcheting mechanisms or standardized color-coding, enhance the speed and reliability of application by minimally trained first responders, significantly reducing the potential for user error and improving critical response times in high-stress emergency scenarios.

Regional dynamics are critical in defining the Emergency Cervical Collars Market, with distinct requirements and growth drivers across major geographic zones.

Emergency Cervical Collars are primarily indicated for patients suspected of having an acute cervical spine injury resulting from significant trauma, such as motor vehicle accidents, falls from height, diving incidents, or blunt force trauma to the head, neck, or trunk. The collar is used to maintain neutral spine alignment and prevent secondary neurological damage during initial assessment and transport until radiological clearance is obtained.

Adjustable collars offer significant clinical utility by allowing first responders to quickly customize the collar fit to various patient neck sizes using a single device, reducing the inventory required and minimizing the risk of applying an ill-fitting collar. Fixed-size collars, while potentially cheaper, require pre-sizing based on patient measurements, increasing the potential for error and logistical complexity in high-stress, dynamic emergency environments.

Radiolucency is crucial because it allows clinicians to perform necessary diagnostic imaging, such as X-rays and CT scans, without removing the collar. Removing the collar before radiological clearance risks exacerbating a potential spinal injury. Modern designs use advanced polymers that are transparent to imaging radiation, ensuring continuous stabilization throughout the diagnostic process, which is fundamental to efficient trauma protocols.

The primary driver is infection control, particularly minimizing the risk of cross-contamination between patients in environments where rapid decontamination is challenging. Disposable collars also eliminate the need for costly and time-consuming sterilization procedures, simplifying logistics for high-volume users like EMS agencies, thereby increasing overall operational efficiency and adherence to hygiene standards in pre-hospital care settings.

The Asia Pacific (APAC) region is projected to exhibit the fastest growth rate. This accelerated expansion is attributed to large-scale infrastructure investments, increasing incidence of road traffic accidents associated with rapid urbanization, and significant governmental efforts to modernize and improve access to standardized, high-quality emergency and trauma healthcare services across densely populated nations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.