ID : MRU_ 433211 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

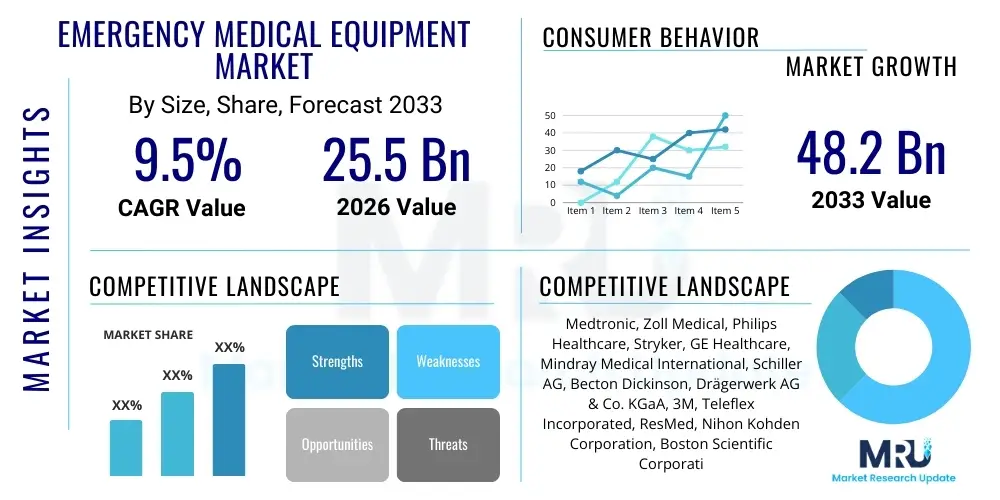

The Emergency Medical Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at $25.5 Billion in 2026 and is projected to reach $48.2 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by the increasing prevalence of chronic conditions requiring immediate stabilization, coupled with significant advancements in portable and connected medical technologies designed for pre-hospital care and rapid trauma response. Global investment in strengthening Emergency Medical Services (EMS) infrastructure, particularly in developing economies, further contributes to this expansion, creating substantial demand for advanced and reliable emergency devices capable of operating effectively outside traditional clinical settings.

The Emergency Medical Equipment Market encompasses a wide range of specialized devices and tools crucial for diagnosing, monitoring, and treating patients in critical, life-threatening situations, particularly during pre-hospital care or initial stabilization phases within emergency departments. Key products include defibrillators (manual, semi-automatic, and automated external defibrillators or AEDs), patient monitoring systems, emergency ventilators and respiration equipment, trauma management kits, and various disposable supplies necessary for immediate intervention. These products are engineered for portability, durability, rapid deployment, and intuitive operation, ensuring effective treatment delivery under demanding, time-sensitive circumstances where seconds often determine patient outcomes.

Major applications of emergency medical equipment span various critical scenarios, including cardiac arrest, severe respiratory distress, major trauma resulting from accidents, strokes, and environmental emergencies. The inherent benefits derived from these devices are numerous, focusing predominantly on improving survivability rates and minimizing long-term damage through immediate intervention. For instance, rapid deployment of AEDs significantly increases the likelihood of survival from sudden cardiac arrest, while portable ventilators maintain critical oxygenation during transport. Technological integration, such as telemonitoring capabilities, further enhances their utility by allowing EMS personnel to transmit vital data to receiving hospitals, thereby streamlining in-hospital treatment protocols before patient arrival.

Driving factors propelling market growth are multi-faceted. The global rise in chronic diseases, especially cardiovascular and respiratory disorders, necessitates readily available emergency solutions. Furthermore, an aging population worldwide is more susceptible to medical emergencies. Regulatory emphasis on public access to defibrillation (PAD) programs, coupled with continuous technological innovation resulting in smaller, lighter, and more sophisticated devices with improved battery life and connectivity, are foundational drivers ensuring sustained market expansion. Increased awareness and mandatory training requirements for first responders and laypersons also contribute significantly to the broader adoption of user-friendly emergency devices.

The global Emergency Medical Equipment Market is characterized by accelerating integration of digital health solutions and a strong focus on device portability and user interface simplification. Current business trends highlight significant merger and acquisition activities among key players aiming to consolidate technological expertise, particularly in areas involving remote patient monitoring and decision support systems enhanced by artificial intelligence. The shift towards disposable and automated devices designed for ease of use by non-specialized personnel—such as those involved in public access environments—represents a crucial commercial pivot, broadening the market beyond traditional institutional procurement.

Regionally, North America remains the dominant revenue contributor, largely due to well-established EMS infrastructure, high healthcare spending, and rapid adoption of advanced medical technologies supported by favorable reimbursement policies. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. This rapid growth in APAC is driven by substantial government investments in improving emergency response capabilities, modernization of hospital infrastructure, and the expansion of medical tourism, creating massive demand for reliable, standardized emergency equipment.

Segment trends indicate that the Defibrillator segment, particularly Automated External Defibrillators (AEDs), continues to hold a significant market share, fueled by mandates for public access and the increasing incidence of sudden cardiac death. The Monitoring Devices segment is expected to show robust growth, attributed to the demand for multi-parameter monitors capable of tracking vital signs during transport. Among end-users, Emergency Medical Services (EMS) and hospitals maintain primary market consumption, though the increasing use of personal and home-care emergency kits represents an emerging high-growth niche, driven by decentralized healthcare models and tele-health adoption. Successful market players are focusing heavily on developing robust, internet-of-things (IoT) enabled devices that can transmit real-time data securely, optimizing immediate patient care decisions.

Users frequently inquire about how Artificial Intelligence (AI) can enhance the speed and accuracy of critical care decisions, asking specifically if AI-driven diagnostics will reduce response times and improve patient outcomes in high-stress emergency environments. Key concerns revolve around the reliability and validation of AI algorithms in pre-hospital settings where data quality might be compromised, and the necessary integration standards required for seamless communication between diverse emergency medical devices. Users also express strong interest in how AI can be utilized for predictive maintenance of life-support equipment, ensuring device reliability, and for optimizing EMS resource allocation and route planning. The overarching expectation is that AI will transform emergency response from reactive to predictive, enabling highly customized and evidence-based interventions before definitive care is reached.

AI's influence is rapidly extending across the spectrum of emergency medical equipment, promising enhanced operational efficiency and superior clinical precision. By integrating machine learning models into portable monitoring devices, AI facilitates real-time interpretation of complex physiological data, allowing EMS personnel to receive immediate, actionable clinical decision support regarding conditions like sepsis, acute respiratory failure, or cardiac rhythm abnormalities. This acceleration of diagnosis initiation is particularly vital in rural or remote areas where access to specialist physician consultation is limited, enabling frontline responders to initiate standardized, evidence-based treatment protocols more effectively and minimizing crucial time delays. Moreover, the application of AI in analyzing historical emergency response data, including geographical, temporal, and demographic factors, is instrumental in optimizing the strategic placement of emergency vehicles and equipment, thereby drastically reducing median response times and enhancing overall system readiness.

The development of next-generation emergency ventilators and infusion pumps heavily leverages AI for adaptive therapy delivery. For instance, AI algorithms can dynamically adjust ventilator settings based on continuous patient feedback parameters such as lung compliance and gas exchange efficiency, moving beyond static protocols to highly personalized respiratory support. This sophisticated level of automation not only improves the efficacy of life support during transport but also reduces the cognitive burden on emergency personnel, allowing them to focus on immediate hands-on care and stabilization. Regulatory pathways are evolving to address the unique challenges of certifying AI-embedded medical devices, focusing on robustness, algorithmic transparency, and mitigating risks associated with data bias, ensuring that these innovations meet the stringent safety and performance requirements expected in critical care environments.

The Emergency Medical Equipment Market is fundamentally shaped by a dynamic interplay of factors encapsulated by Drivers, Restraints, and Opportunities (DRO). Significant market drivers include the global escalation in road accidents, natural disasters, and the increasing incidence of cardiovascular and respiratory emergencies necessitating immediate care outside traditional hospital settings. This is strongly coupled with technological progress focused on creating compact, robust, and highly functional portable equipment. However, the market faces constraints related to the high initial capital investment required for advanced equipment and ongoing challenges in ensuring standardized training across diverse user groups. Opportunities lie primarily in penetrating underserved emerging markets, developing integrated IoT-enabled emergency ecosystems, and leveraging public-private partnerships to expand public access to critical devices like AEDs.

The primary drivers are anchored in demographics and technology. The demographic shift towards an older population inherently increases the pool of individuals requiring emergency medical attention. Technologically, the shift from bulky, complex machines to lightweight, battery-powered, and connected devices (leveraging 5G and secure cloud platforms) makes advanced care feasible in mobile environments. These forces collectively enhance the capacity and efficiency of emergency response networks worldwide. Conversely, major restraints include stringent regulatory approval processes, which can delay the introduction of innovative products, and the complexity of ensuring interoperability among disparate systems used by various emergency service providers. Furthermore, the limited budget allocations for healthcare infrastructure, particularly in low and middle-income countries, often restrict the large-scale adoption of cutting-edge, expensive emergency equipment, forcing reliance on older or less advanced technologies.

Impact forces within this market demonstrate a profound influence on patient outcomes and industry investment. The imperative for better patient outcomes drives continuous innovation in device accuracy and deployment speed. For instance, the rapid success of thrombolytic therapy relies directly on swift diagnosis and transport facilitated by advanced emergency equipment. Secondly, the societal cost associated with preventable mortality and morbidity exerts immense pressure on governments and healthcare organizations to invest heavily in comprehensive, well-equipped emergency infrastructure. Opportunities manifest through the creation of specialized market niches, such as disaster preparedness equipment and military field care solutions, demanding highly ruggedized and versatile devices. The ongoing transition towards preventative care and predictive diagnostics, supported by connectivity and data analysis capabilities, further solidifies the long-term growth potential and resilience of this vital medical equipment sector.

The Emergency Medical Equipment Market is extensively segmented based on the type of product, the specific application or medical condition being addressed, and the primary end-user setting where the equipment is deployed. This segmentation provides a crucial framework for understanding purchasing behavior, regional consumption patterns, and technological focus areas within the industry. Product segmentation typically reflects the functional categories essential for emergency stabilization, ranging from airway management to circulatory support. Application segmentation highlights the increasing specialization required to manage distinct trauma and medical emergencies, while end-user analysis provides insight into infrastructure needs, distinguishing between high-volume users like hospitals and rapid-deployment units like EMS providers.

The Product Type segment includes high-value, complex equipment such as patient monitoring systems capable of continuous vital sign tracking during transport, and advanced resuscitation devices like mechanical CPR systems. Furthermore, consumables and disposables, while individually lower in value, constitute a massive volume segment critical for infection control and immediate care. The Application segments often see cardiac emergencies and trauma stabilization as the largest revenue generators due to their high prevalence globally. Understanding these segments is vital for manufacturers developing targeted marketing strategies, allowing them to optimize device features for specific user environments, such as ruggedization for field use or advanced data integration capabilities for hospital settings, ultimately driving overall market penetration and adoption.

The value chain for the Emergency Medical Equipment Market begins with the upstream procurement of highly specialized components, including advanced sensor technology, high-capacity battery systems, durable and lightweight materials, and complex microprocessors necessary for advanced monitoring and computational functions. Manufacturers engage in rigorous design and assembly processes, often requiring specialized cleanroom environments, to produce devices that meet stringent safety and regulatory standards (such as ISO certifications and FDA approvals). Key considerations at this stage include minimizing device size, maximizing battery life, and ensuring extreme ruggedness to withstand harsh operational environments, which dictates the complexity and cost of the upstream supply inputs.

The downstream segment is dominated by distribution and after-sales service, which are critical differentiators in this market. The distribution channel is complex, involving direct sales forces for major hospital and government contracts, specialized medical device distributors for regional markets, and third-party logistics providers (3PLs) for inventory management and rapid deployment. Given the life-critical nature of the equipment, effective post-sales support—including mandatory training for emergency personnel, calibration services, and timely repairs—is paramount to maintaining market reputation and securing recurring revenue. Direct distribution is often preferred for high-value capital equipment like advanced ventilators, allowing manufacturers greater control over installation and ongoing maintenance, whereas disposables and consumables are typically managed through broad, indirect distribution networks.

The success of the value chain relies heavily on maintaining a balance between innovative technology development and robust regulatory compliance. Effective channel management, including optimizing inventory levels for rapid replacement of critical supplies, is essential for EMS providers. Indirect channels often utilize e-commerce platforms and specialized medical procurement agencies, particularly for smaller, standardized products like AED pads or basic trauma kits. The overall value extraction is maximized when manufacturers integrate software solutions (for data management and predictive maintenance) directly into the sales offering, transforming the product from a one-time capital purchase into a recurring service model, thus strengthening long-term customer relationships and ensuring optimal device performance throughout its lifecycle.

The primary customers for emergency medical equipment are institutions and services dedicated to rapid response and critical stabilization, dominated by the Hospital and Emergency Medical Services (EMS) segments. Hospitals, particularly those designated as Level I and II Trauma Centers, require extensive inventories of high-specification equipment, including transport ventilators, advanced patient monitors, and sophisticated resuscitation systems, catering to a continuous influx of severe cases. EMS providers, encompassing both public and private ambulance services, constitute a critical customer base, demanding ultra-portable, durable, and highly integrated devices that function reliably under extreme conditions, where device weight, battery longevity, and real-time connectivity are non-negotiable performance metrics.

Beyond the core institutional users, a rapidly growing customer segment includes Public Access Defibrillation (PAD) programs and various non-traditional emergency preparedness organizations. This encompasses corporate offices, educational institutions, airlines, sporting venues, and public transportation hubs, all mandated or encouraged to install user-friendly Automated External Defibrillators (AEDs). This demographic represents a high-volume market for simpler, highly automated, and low-maintenance equipment. Furthermore, the increasing trend of telemedicine and decentralized care positions home healthcare providers and individual patients managing chronic conditions (e.g., severe asthma or cardiac risks) as emerging potential customers for personal emergency kits and monitoring devices designed for layperson use.

The purchasing decisions across these diverse customer groups are influenced by differing factors. Hospitals prioritize clinical efficacy, integration with Electronic Health Records (EHRs), and total cost of ownership, including service contracts. EMS agencies prioritize ruggedness, size, and compatibility across their fleet, often adhering to strict governmental procurement cycles and specifications. Public access buyers, conversely, focus on simplicity, minimal training requirements, and compliance with local public health regulations. Therefore, successful market players must tailor their product features, distribution strategies, and support services to meet the highly specific operational and budgetary needs of each distinct potential customer category.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $25.5 Billion |

| Market Forecast in 2033 | $48.2 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Zoll Medical, Philips Healthcare, Stryker, GE Healthcare, Mindray Medical International, Schiller AG, Becton Dickinson, Drägerwerk AG & Co. KGaA, 3M, Teleflex Incorporated, ResMed, Nihon Kohden Corporation, Boston Scientific Corporation, Smiths Medical (ICU Medical), B. Braun Melsungen AG, Asahi Kasei Corporation, Johnson & Johnson, Masimo Corporation, Allied Healthcare Products Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Emergency Medical Equipment Market is currently defined by three critical pillars: miniaturization, advanced connectivity, and integration of sophisticated decision-support algorithms. Miniaturization allows for the development of highly portable, rugged devices that maintain the comprehensive functionality previously associated only with large, stationary hospital machines. This trend is crucial for optimizing space and weight in ambulances and enabling rapid deployment by first responders in challenging environments. Significant investments are being made in developing high-density, long-lasting battery technologies (e.g., lithium-ion improvements) to ensure continuous operation of critical life support systems during extended transport or disaster scenarios, minimizing the risk of equipment failure when it is needed most.

Advanced connectivity, primarily leveraging 4G/5G networks and secure Internet of Things (IoT) protocols, is transforming patient monitoring from simple data collection to continuous remote patient management. Connected devices facilitate seamless, real-time data transfer of vital signs, waveforms, and treatment logs directly from the scene to the receiving hospital's emergency department and electronic health records (EHRs). This Pre-Hospital Telemonitoring capability enables physicians to anticipate patient needs, activate specialized teams (e.g., Cath Lab or Stroke Team), and prepare resources well before the patient's arrival. Interoperability standards, ensuring that data can be shared seamlessly across devices from different manufacturers and integrating securely with centralized EMS platforms, remain a key technological focus for the industry.

Furthermore, sensor technology improvements and the integration of Artificial Intelligence (AI) are enhancing the diagnostic capabilities of frontline equipment. Next-generation patient monitors incorporate non-invasive sensors capable of measuring complex physiological parameters with greater accuracy, such as continuous blood pressure measurement without cuff inflation. AI and machine learning algorithms are embedded within defibrillators and ventilators to offer intelligent, adaptive therapy. For instance, AI can analyze ECG signals for subtle irregularities often missed by human eyes or automatically modulate oxygen delivery based on patient saturation trends. This technological evolution increases the efficacy of field interventions, elevates the standard of care delivered by non-physician personnel, and fundamentally shifts emergency medicine towards highly data-driven, predictive response models, representing a massive leap forward in ensuring positive outcomes for critical patients.

The global distribution and growth rates of the Emergency Medical Equipment Market vary significantly by region, driven by differences in healthcare infrastructure maturity, regulatory environment, and public health spending.

The market growth is fundamentally driven by the rising global incidence of sudden chronic conditions such as cardiovascular disease and respiratory failure, coupled with an increasing aging population requiring immediate stabilization. Technological innovation, specifically the development of portable, rugged, and IoT-enabled devices that facilitate seamless pre-hospital data exchange and enhance rapid intervention capabilities, is a core accelerator. Furthermore, regulatory mandates supporting Public Access Defibrillation (PAD) programs significantly expand the installed base for automated external defibrillators (AEDs), contributing substantially to overall market expansion and revenue generation.

AI is increasingly integrated into emergency equipment to provide advanced clinical decision support and optimize operational efficiency. For instance, AI algorithms are used in patient monitors for real-time interpretation of complex physiological data, enabling earlier detection of conditions like sepsis or shock, thereby reducing diagnostic delays. In defibrillators, AI refines rhythm analysis, and in ventilators, it facilitates adaptive therapy adjustments based on instantaneous patient feedback. Operationally, AI is vital for EMS resource allocation, predicting high-demand areas to minimize critical response times, transforming the delivery of critical care.

The Defibrillators segment historically holds one of the largest market shares, driven by the critical need for immediate response to sudden cardiac arrests and strong government initiatives promoting broad public access and mandatory installation in key public venues. The proliferation of Automated External Defibrillators (AEDs) in non-clinical settings, along with continuous upgrades in advanced manual and semi-automatic hospital-grade units, ensures persistent dominance. However, the Patient Monitoring Devices segment is expected to show the fastest growth rate, fueled by the demand for sophisticated multi-parameter monitors capable of sustaining functionality and data fidelity during patient transport and transfer.

Manufacturers primarily face challenges related to achieving robust interoperability across diverse device ecosystems and ensuring data security in connected emergency systems. Developing compact devices that do not compromise on battery life or clinical accuracy remains a technological hurdle. Additionally, the regulatory environment is increasingly complex, especially concerning software as a medical device (SaMD) and AI-enabled diagnostics, requiring significant investment in validation and certification processes. Balancing the need for advanced features with the imperative for affordability, particularly in emerging markets, also poses a significant competitive challenge.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) from 2026 to 2033. This accelerating growth is primarily attributed to substantial government investments aimed at modernizing outdated healthcare infrastructure, the expansion of emergency medical services in populous urban centers, and increasing disposable income leading to higher demand for quality healthcare. Countries like China, India, and Southeast Asian nations are actively standardizing and expanding their trauma and emergency response systems, driving high volume procurement of new and sophisticated emergency medical equipment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.