ID : MRU_ 435024 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

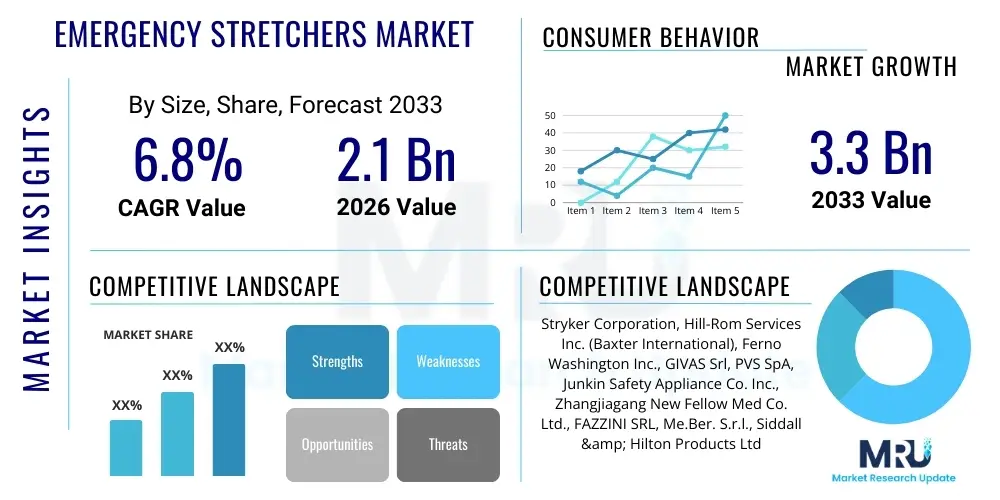

The Emergency Stretchers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 2.1 Billion in 2026 and is projected to reach USD 3.3 Billion by the end of the forecast period in 2033.

The Emergency Stretchers Market encompasses the manufacturing, distribution, and sale of specialized medical devices designed for the safe and efficient transport of injured or critically ill patients in pre-hospital and hospital settings. These essential medical transport solutions range from basic foldable stretchers used in routine patient transfer to highly sophisticated ambulance stretchers featuring advanced loading systems, power-operated height adjustments, and integrated monitoring capabilities. The primary function of these products is to stabilize the patient during movement, minimize secondary injury, and provide immediate access to life-saving interventions en route to definitive care. Market growth is fundamentally driven by the escalating global incidence of road accidents, natural disasters, and the expanding geriatric population requiring specialized medical mobility aids, thereby increasing the demand for reliable and ergonomic patient handling equipment across emergency medical services (EMS) infrastructure globally.

Product descriptions within this market segment are diverse, covering various materials such as aluminum, carbon fiber composites, and robust polymers, all chosen for their balance of lightweight properties, durability, and radiolucency. Major applications span critical care transport, military field operations, mass casualty incident (MCI) management, and routine inter-hospital transfers. Modern stretchers integrate features like adjustable backrests, Trendelenburg positioning, and comprehensive restraint systems, ensuring both patient comfort and provider safety during high-stress scenarios. The inherent benefit of advanced emergency stretchers lies in their ability to significantly reduce the physical strain on EMS personnel, comply with stringent patient safety regulations, and improve the speed and quality of trauma care delivery, directly impacting patient outcomes and operational efficiency within healthcare systems worldwide.

The driving factors propelling the Emergency Stretchers Market include significant investments in upgrading aging ambulance fleets, particularly in developing economies, and the continuous technological advancements leading to the development of powered and automated stretchers. Furthermore, regulatory mandates focusing on worker safety (preventing back injuries among paramedics) and patient transport standards are compelling healthcare providers and EMS agencies to replace outdated manual equipment with next-generation solutions. The convergence of these factors—enhanced safety regulations, technological innovation, and heightened global awareness regarding immediate and professional emergency response—establishes a robust environment for sustained market expansion throughout the forecast period, positioning emergency stretchers as indispensable components of the global emergency medical ecosystem.

The Emergency Stretchers Market is undergoing a significant transformation, characterized by rapid technological integration and increasing standardization requirements across major healthcare economies. Current business trends indicate a strong move toward automation, with powered stretchers gaining substantial market share due to their superior ergonomic benefits and efficiency gains in patient handling, directly addressing workforce health concerns in EMS. Furthermore, consolidation among key manufacturers is driving innovation in material science, focusing on lighter, stronger, and more infection-resistant materials, especially in response to heightened hygiene protocols post-pandemic. Strategic partnerships between stretcher manufacturers and ambulance conversion specialists are becoming prevalent, aiming to provide fully integrated and optimized patient transport solutions, rather than selling components in isolation, thereby enhancing the overall value proposition for emergency service providers globally.

Regional trends highlight North America and Europe as dominant markets, primarily driven by well-established EMS systems, high disposable incomes allocated to healthcare infrastructure, and early adoption of premium, technology-intensive products like bariatric and specialized evacuation stretchers. However, the Asia Pacific (APAC) region is poised for the fastest growth, propelled by massive governmental initiatives to modernize public health infrastructure, increasing urbanization leading to complex trauma incidents, and the rapid expansion of private ambulance services in countries like India and China. Latin America and the Middle East and Africa (MEA) present burgeoning opportunities, characterized by investments stimulated by large-scale public health programs and the critical need to enhance disaster preparedness capabilities, resulting in a steady uptake of reliable, albeit often less automated, basic and foldable stretcher models.

Segmentation trends reveal that the fixed/wheeled stretchers segment holds the largest revenue share due to their ubiquitous use in both pre-hospital and inpatient care. Nevertheless, the specialized stretchers segment, including scoop stretchers, basket stretchers (Stokes baskets), and orthopedic stretchers, is projected to exhibit the highest growth rate, driven by their necessity in complex rescue environments such as water rescue, mountainous terrain, and confined spaces. Based on end-user, the hospital segment remains the primary consumer, but the Emergency Medical Services (EMS) segment is rapidly increasing its procurement power, fueled by government contracts and the continuous expansion of dedicated ambulance fleets. These intertwined segment trends underscore the market’s responsiveness to both routine operational efficiency demands and highly specialized critical rescue requirements.

Common user questions regarding AI's impact on the Emergency Stretchers Market typically revolve around whether AI could automate patient loading, how predictive maintenance affects equipment lifespan, and if intelligent systems can optimize stretcher deployment and inventory management across large ambulance networks. Users are primarily concerned about the integration of AI-driven sensors for real-time patient status monitoring while in transit, questioning the reliability and regulatory clearance of such intelligent systems. There is also significant interest in AI's role in optimizing the design process itself, using simulation to create lighter, stronger, and more ergonomic stretcher geometries that minimize stress points and maximize stability. The overarching consensus is that AI will not replace the physical stretcher but rather serve as a powerful enhancement tool, transforming traditional transport equipment into smart, connected medical platforms capable of feeding crucial data back to emergency departments before arrival, thus significantly streamlining the continuum of care.

The core theme summarizing user expectations is focused on efficiency and predictive capability. Users anticipate AI integrating into stretcher systems via embedded sensors that continuously track equipment status (e.g., battery life, wheel integrity, structural stress) to predict maintenance needs, thereby ensuring maximum operational readiness and minimizing downtime for critical equipment. Furthermore, AI algorithms are expected to analyze route data and patient physiological inputs gathered during transport. For instance, an intelligent stretcher could autonomously adjust its posture (e.g., slight elevation change) based on real-time readings combined with AI assessments of optimal cardiac or respiratory positioning for the specific patient condition, requiring minimal manual intervention from the paramedic, thus freeing up providers to focus on clinical interventions.

The implementation of AI also extends deeply into logistical and inventory management. Large regional EMS providers struggle with optimal distribution of specialized stretchers (e.g., bariatric units) across geographically dispersed stations. AI-powered predictive logistics platforms, utilizing incident data and demographic information, can forecast the likely need for specific types of stretchers in certain areas at particular times, optimizing asset allocation and reducing response times when critical resources are required. While the physical structure of the emergency stretcher remains core, AI integration elevates the product from a static transport device to an active data acquisition and decision support system within the modern emergency medical workflow, fundamentally redefining its utility and market value.

The Emergency Stretchers Market is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape the competitive landscape and growth trajectories. Key drivers include the global increase in trauma and geriatric populations, which necessitate safe and ergonomic patient transfer solutions. The continuous modernization of pre-hospital care infrastructure, particularly in emerging economies, alongside stringent regulatory requirements for patient handling and worker safety (e.g., mandatory use of powered stretchers to prevent caregiver back injuries) acts as a powerful catalyst for market expansion. Furthermore, continuous product innovation, incorporating lightweight materials like carbon fiber and advanced features such as integrated weighing scales and monitoring systems, enhances the utility and appeal of new generation stretchers, driving replacement cycles in mature markets.

However, the market faces notable restraints. The high initial capital expenditure required for advanced, powered ambulance stretchers presents a significant barrier to adoption, especially for smaller or publicly funded EMS organizations with limited budgets. Additionally, complexity in maintenance and the need for specialized training to operate highly automated systems can slow down implementation, particularly in regions facing skilled labor shortages. Another restraint involves the potential for product recalls or safety failures related to mechanical or electrical components in powered systems, leading to negative publicity and mandatory design modifications. The intense pricing pressure from regional, localized manufacturers offering basic, low-cost manual stretchers in price-sensitive markets also challenges the profitability margins of international premium brands.

Opportunities for growth are abundant and center on expanding niche market penetration and strategic geographical expansion. The growing demand for bariatric stretchers, specifically engineered to handle obese patients safely, represents a high-growth, high-value opportunity, given the rising prevalence of obesity worldwide. Furthermore, the development of specialized stretchers for extreme environments (e.g., hazardous material incidents, high-altitude rescue) and the integration of telehealth capabilities into transport platforms offer promising avenues for diversification. Leveraging public-private partnerships (PPPs) to finance the massive fleet upgrades required across governmental EMS agencies in developing nations represents a substantial long-term opportunity, enabling manufacturers to secure large-volume, multi-year contracts and establish a dominant market presence early in the infrastructure development cycle.

The market is further governed by five primary impact forces, commonly analyzed through the lens of Porter's framework, indicating the intensity of competition and external pressures. The threat of new entrants is moderate, balanced by high capital requirements (especially for producing high-tech powered systems) but countered by the relatively standardized technology required for basic stretchers. The bargaining power of buyers, particularly large hospital groups and government procurement agencies, is high due to volume purchasing and the standardized nature of product specifications. Supplier bargaining power is moderate; while raw materials like specialized aluminum and composite fibers are unique, multiple sourcing options generally exist. The threat of substitutes is low, as no other device can safely and effectively replace a dedicated emergency stretcher for patient transport. Finally, competitive rivalry is high, driven by established global players continuously investing in R&D and aggressive marketing strategies to differentiate their automated and specialized product lines.

The Emergency Stretchers Market segmentation provides a granular view of product utilization and demand distribution across various dimensions, including product type, technology, application, and end-user. This structural breakdown helps identify high-growth areas and specific consumer needs, crucial for tailored marketing and product development strategies. The market is primarily bifurcated based on the complexity and functionality offered, ranging from manual, simple stretchers to highly sophisticated electro-hydraulic systems. Analyzing these segments is essential as the purchasing criteria often differ significantly; hospitals might prioritize stability and easy cleaning, while EMS providers focus on maneuverability, load capacity, and rapid deployment capabilities under duress. The technological split reflects the ongoing shift from fully manual reliance to power-assisted and fully automated patient handling, a trend heavily influenced by global safety standards for medical personnel.

Key segments include the differentiation between wheeled (gurney) stretchers, which are standard for ambulance use, and specialized stretchers like scoop, basket, and spinal boards, designed for initial immobilization and extraction from confined or dangerous environments. The wheeled segment, while mature, is seeing significant innovation through battery-powered operation that automates lifting and lowering, thereby minimizing physical exertion for emergency staff. Furthermore, the application segmentation distinguishes between emergency room usage (high throughput, static environment) and ambulance transport (dynamic environment, critical speed requirements). This distinction directly impacts design specifications, such as suspension requirements, material durability, and the integration of vehicle-compatible interfaces, ensuring seamless transfer between the transport unit and the clinical setting.

End-user analysis further defines market consumption patterns, with hospitals, ambulatory surgical centers, and dedicated EMS providers forming the core customer base. Hospitals represent consistent demand for internal patient transfer and ER preparation, while EMS agencies drive the demand for rugged, high-performance equipment suited for the rigors of pre-hospital care. The growing importance of military and disaster relief organizations as end-users is also notable, creating a segment requiring ultra-durable, collapsible, and easily deployable stretchers compliant with international rescue standards. Understanding these varied needs across segmentation axes is vital for predicting future investment areas and ensuring product portfolios remain relevant to the evolving landscape of emergency medicine and patient logistics.

The Value Chain for the Emergency Stretchers Market begins with upstream activities focused on raw material sourcing and component manufacturing, which are critical determinants of the final product's quality and cost. Upstream suppliers primarily provide specialized high-grade aluminum, lightweight composite materials (like carbon fiber), steel alloys for structural integrity, and complex electronic and hydraulic components for powered systems (motors, batteries, sensors, and control systems). The quality and reliability of these components are paramount, driving relationships toward long-term contracts with certified material providers, particularly those compliant with medical device manufacturing standards (e.g., ISO 13485). Managing volatility in raw material prices, especially metals, is a crucial strategic consideration at this stage, requiring efficient supply chain optimization and inventory hedging strategies to maintain competitive pricing in the downstream market.

The subsequent core activity involves primary manufacturing, assembly, and rigorous quality assurance testing. Major manufacturers engage in precision engineering, designing stretchers for maximum load capacity, stability, and radiolucency. Modern manufacturing processes emphasize lean techniques and integration of advanced robotics to ensure consistency in complex assembly processes, particularly for powered stretchers where hydraulic or electric systems must interface flawlessly with the frame and patient platform. Strict adherence to international regulatory standards, such as those set by the FDA (U.S.) and CE (Europe), dictates the extensive documentation and testing required before market release, adding significant value and ensuring product credibility. Customization and specialized manufacturing, such as the production of bariatric or MRI-compatible models, represent high-value additions within the manufacturing stage.

Downstream activities center on distribution, sales, and post-sale service. Distribution channels are typically complex, utilizing both direct sales models for large governmental tenders and key hospital groups, and indirect models through specialized medical equipment distributors and regional resellers. Direct channels offer greater control over pricing and customer relationship management, crucial for high-margin, technologically advanced products. Indirect channels provide necessary geographical reach, especially in fragmented emerging markets. Post-sale activities, including maintenance, servicing, and provision of spare parts, constitute a substantial part of the long-term value chain, ensuring equipment longevity and reliability. Effective service networks are critical, as downtime for an ambulance stretcher directly impacts emergency response capabilities, establishing service excellence as a key differentiator in a highly competitive sales environment.

The primary consumers and end-users of emergency stretchers constitute a broad spectrum of institutions dedicated to trauma management, emergency response, and patient transport logistics. These customers are categorized by their operational environment and specific functional requirements, dictating the type and complexity of stretchers they procure. Hospitals represent a massive, constant demand base, particularly their Emergency Departments (EDs), Intensive Care Units (ICUs), and radiology suites. They require robust, easily maneuverable wheeled stretchers (gurneys) for internal transfers and specialized units like radiolucent stretchers for imaging procedures. The purchasing decisions in this segment are often centralized and guided by infection control policies, ease of sterilization, and compatibility with existing hospital beds and monitoring equipment, often favoring basic and mid-range powered stretchers that integrate seamlessly into the hospital workflow.

Emergency Medical Service (EMS) providers and dedicated ambulance services form the second most crucial segment, driving the demand for high-performance, resilient, pre-hospital equipment. This group includes both municipal/governmental ambulance fleets and private sector emergency transport companies. Their procurement focuses intensely on powered loading systems, superior suspension compatibility with ambulance interiors, heavy-duty construction for field use, and advanced safety features, such as integrated restraints and ruggedized data capture capabilities. Given the operational stress and regulatory mandates concerning paramedic safety, EMS providers are the earliest and most substantial adopters of high-end, fully automated stretchers, justifying the higher cost based on reduced injury rates, enhanced operational speed, and improved crew retention rates associated with ergonomic equipment.

A rapidly expanding customer base includes specialized response teams, such as search and rescue organizations, military medical units, and large industrial sites (e.g., mining, offshore platforms). These customers typically require non-wheeled, highly durable, and specialized stretchers capable of extraction from challenging terrains—specifically basket stretchers, scoop stretchers, and specialized spine boards made from lightweight, extremely resilient materials like carbon fiber. Furthermore, the rise of mass casualty incident (MCI) planning and disaster preparedness globally has positioned governmental agencies and NGOs, such as the Red Cross, as significant buyers of high-volume, cost-effective folding and portable stretchers. Their purchasing criteria prioritize durability, rapid deployment, minimal footprint when stored, and strict compliance with global humanitarian aid standards, resulting in diverse procurement needs across the entire product complexity spectrum.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.3 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Stryker Corporation, Hill-Rom Services Inc. (Baxter International), Ferno Washington Inc., GIVAS Srl, PVS SpA, Junkin Safety Appliance Co. Inc., Zhangjiagang New Fellow Med Co. Ltd., FAZZINI SRL, Me.Ber. S.r.l., Siddall & Hilton Products Ltd., Narang Medical Limited, Pelican Manufacturing, Byron, Jiangsu Saikang Medical Equipment Co., Ltd., Orient New Star Medical Equipment Co., Ltd., CEAB Srl, BE SAFE Sp. z o.o., Allied Healthcare Products Inc., Royax. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Emergency Stretchers Market is rapidly evolving, moving beyond simple mechanical function toward integrated smart systems designed to enhance patient safety, increase operational efficiency, and improve provider ergonomics. The most significant technological leap is the widespread adoption of battery-powered systems, particularly in wheeled ambulance stretchers, which automate the lifting and lowering process. These electro-hydraulic or electro-pneumatic systems are crucial for reducing the risk of musculoskeletal injuries among EMS personnel, a major occupational health concern. Advanced control systems utilize microprocessors and sensors to ensure smooth, controlled movement, even with heavy loads, and often incorporate safety features like anti-tip mechanisms and audible warnings for unsafe angles. Furthermore, manufacturers are increasingly using lightweight, high-strength materials such as aviation-grade aluminum alloys and advanced carbon fiber composites, which significantly reduce the overall weight of the stretcher without compromising its load capacity or structural integrity, thereby improving vehicle fuel efficiency and handling dynamics.

Another crucial area of technological advancement involves connectivity and data integration. Modern stretchers are transforming into mobile medical hubs, equipped with integrated weighing scales, patient physiological monitoring ports, and wireless communication capabilities (Bluetooth/Wi-Fi). This integration allows for the seamless, real-time transmission of patient data—including weight, estimated critical severity scores, and time stamps of interventions—to the receiving hospital's electronic health record (EHR) system while the patient is still en route. This critical feature dramatically enhances the continuity of care by allowing the emergency department to prepare resources and personnel before the ambulance arrives, drastically cutting down on patient transfer time and initiating definitive treatment sooner. Compatibility with standardized ambulance docking systems, such as universal latching mechanisms, also represents a key technical requirement ensuring quick, safe, and secure patient loading and unloading across diverse ambulance vehicle models.

Specialized technological innovations cater to niche market demands. For instance, bariatric stretchers utilize complex, reinforced mechanisms and wider platforms, often requiring dual-motor systems to safely lift and transport obese patients exceeding 600 pounds. Infection control technology is also a major focus; new models feature smooth, non-porous surfaces, antimicrobial coatings, and components designed for quick, thorough chemical cleaning and sterilization, directly addressing heightened awareness regarding healthcare-associated infections (HAIs). Future technological trends point toward further automation, including semi-autonomous patient loading/unloading sequences guided by smart sensors and potential integration with virtual reality (VR) training modules to enhance paramedic proficiency in operating complex powered systems, ensuring that technology not only improves the equipment but also the skill set of the user.

The Emergency Stretchers Market exhibits distinct regional dynamics shaped by healthcare spending, regulatory environments, and the maturity of emergency infrastructure.

Demand for powered stretchers is driven primarily by regulatory mandates and clinical necessity focused on occupational safety for EMS personnel, aiming to significantly reduce musculoskeletal injuries associated with manually lifting patients. Efficiency gains and the ability to safely handle bariatric patients are also critical drivers, enhancing operational throughput.

Technology integration provides benefits through predictive maintenance (minimizing downtime), continuous patient monitoring via embedded sensors, and optimized logistics for stretcher deployment. Smart stretchers act as mobile data hubs, streamlining data transfer to hospitals and improving preparation for patient arrival.

The Asia Pacific (APAC) region is forecasted to exhibit the fastest growth rate. This acceleration is attributed to massive investments in regional healthcare infrastructure modernization, urbanization-related trauma increases, and the rapid expansion of private ambulance services across countries like China and India.

The primary restraints are the high initial capital investment required for advanced, automated systems and the complex maintenance associated with powered components. Additionally, intense price competition from basic manual models, particularly in emerging markets, limits market penetration for premium products.

The current trend favors lightweight, high-strength materials, specifically aviation-grade aluminum alloys and carbon fiber composites. These materials reduce the overall weight, improving handling and vehicle fuel efficiency, while ensuring high load capacity and radiolucency for imaging compatibility.

The comprehensive analysis of the Emergency Stretchers Market reveals a sophisticated sector undergoing rapid technological advancement, pivoting significantly towards automated solutions and data connectivity. The sustained focus on global safety standards, coupled with demographic shifts like aging populations and rising obesity rates, ensures a continuous and escalating requirement for specialized patient transport solutions. Key players are aggressively innovating in material science and electronic integration to maintain competitive advantages. The market structure, while mature in North America and Europe, promises robust expansion in the developing regions of APAC and MEA, contingent upon infrastructure investment and successful navigation of local regulatory landscapes. Future growth hinges on successful product differentiation through smart features and improved ergonomics, transforming the stretcher from a simple transport device into an indispensable part of the critical care continuum.

Manufacturers are strategically aligning their product portfolios to address the diverse needs spanning routine hospital transfers to complex disaster relief scenarios. The manual and folding stretcher segments remain vital for resource-constrained environments and specialized rescue operations, confirming that market diversity is crucial for meeting global demand. Furthermore, the regulatory environment is increasingly shaping procurement decisions, mandating adherence to stricter safety and quality protocols which indirectly favors larger manufacturers capable of absorbing the high costs of compliance and certification. Investment in post-sales service networks is becoming a critical differentiating factor, ensuring the operational readiness of high-cost powered equipment, thereby reinforcing customer loyalty and generating predictable aftermarket revenue streams.

In summary, the Emergency Stretchers Market is stable yet dynamic, poised for steady growth driven by demographic pressures and technological imperative. Successful market players will be those who master the delicate balance between innovation (e.g., AI integration, lighter composites), regulatory compliance, and cost efficiency. The evolving competitive landscape necessitates strategic foresight regarding regional expansion, particularly in high-growth APAC markets, and continuous investment in systems that prioritize both patient safety and the occupational health of emergency medical providers worldwide. This trajectory positions emergency stretchers as critical technological investments rather than mere commodity items in the modern healthcare ecosystem.

The robust market size projections reinforce the confidence in sustained investment in this sector. The estimated market value of USD 2.1 Billion in 2026, climbing to USD 3.3 Billion by 2033 at a CAGR of 6.8%, highlights the essential nature of these medical devices. The steady adoption rates, driven by fleet replacement cycles in established economies and foundational infrastructure build-out in emerging regions, guarantee consistent revenue growth. Moreover, the increasing complexity of patient transport—including the requirement for specialty stretchers like those for bariatric patients or magnetic resonance imaging (MRI) compatibility—introduces higher average selling prices (ASPs), contributing disproportionately to market valuation expansion, cementing the market’s critical position within the global medical device sector.

To further understand the competitive dynamics, an analysis of key strategic developments among leading market participants reveals a pattern of continuous mergers, acquisitions, and strategic collaborations. Larger entities often acquire smaller specialized firms to integrate proprietary technology, such as specialized power loading mechanisms or unique composite material expertise, quickly diversifying their product offerings. Furthermore, intellectual property protection, particularly for battery management systems and hydraulic stability controls, is becoming paramount, leading to increased patenting activity. These actions demonstrate the high stakes involved in capturing market share, especially in the premium powered stretcher segment where profit margins are significantly higher than those associated with standardized manual products. This intensified competitive environment ultimately benefits end-users through accelerated innovation and improved product quality across the industry spectrum.

Technological advancement is not confined solely to the stretcher unit itself but extends to its interface with the ambulance vehicle structure. Standardization of vehicle docking systems, for example, allows for swift interchangeability and compliance with varying ambulance designs, increasing flexibility for EMS providers. Future R&D efforts are expected to focus on miniaturization of power systems, increasing battery life, and enhancing the durability of electronic components against extreme temperatures and vibration encountered during emergency transport. The intersection of lightweight design and robust connectivity solutions defines the next generation of emergency stretchers, ensuring they are prepared for increasingly complex and data-intensive modern rescue operations globally, upholding the highest standards of safety and efficiency.

The regulatory landscape is becoming increasingly harmonized across major markets, particularly concerning load testing and patient restraint standards, ensuring a baseline of safety and efficacy. Compliance with these evolving standards represents a significant entry barrier for smaller players but also validates the quality of products offered by established market leaders. For instance, new standards often mandate higher maximum load capacities and rigorous testing protocols for automated lifting mechanisms, driving older, non-compliant equipment out of service and stimulating replacement demand. This regulatory push is a powerful, non-cyclical driver of sales, particularly within publicly funded healthcare systems that must adhere strictly to codified safety guidelines for both patient and provider welfare.

In conclusion, while the core function of emergency stretchers remains constant—safe patient transport—the methods and technology employed are undergoing dramatic modernization. The market’s sustained growth rate and expanding valuation reflect its essential role in emergency medicine. Strategic focus on innovation in power systems, advanced materials, and seamless digital integration will define success for market leaders. Furthermore, geographical strategies must balance penetrating high-volume, cost-sensitive markets with maintaining dominance in premium segments driven by regulatory compliance and technological superiority, ensuring the continued resilience and expansion of the Emergency Stretchers Market throughout the forecast period.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.