ID : MRU_ 436329 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

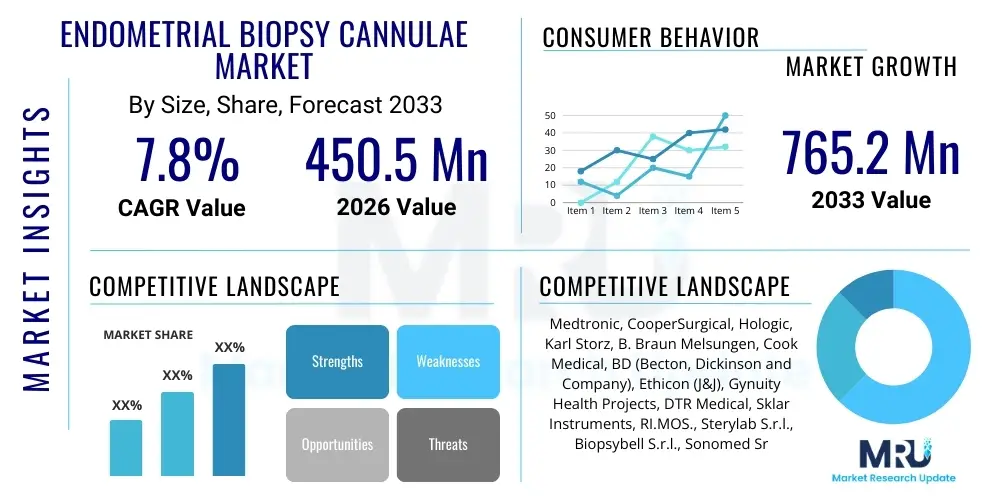

The Endometrial Biopsy Cannulae Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 450.5 Million in 2026 and is projected to reach USD 765.2 Million by the end of the forecast period in 2033.

The Endometrial Biopsy Cannulae Market encompasses the specialized medical devices utilized to safely and effectively obtain tissue samples from the endometrium, the lining of the uterus, for diagnostic purposes. These devices, crucial for identifying various uterine pathologies, including endometrial cancer, polyps, hyperplasia, and infertility causes, offer a minimally invasive alternative to traditional dilation and curettage (D&C) procedures. The cannulae are typically sterile, thin, flexible, or semi-rigid tubes designed for easy insertion through the cervix, often employing suction mechanisms to collect adequate tissue. The design focus is on patient comfort, minimizing procedural complications, and ensuring high diagnostic accuracy. The market landscape is characterized by continuous innovation aimed at improving sample yield and reducing procedural pain, positioning these devices as indispensable tools in gynecological diagnostics and women’s health management globally.

The primary applications of endometrial biopsy cannulae revolve around diagnostic screening and monitoring. They are extensively used in gynecology and oncology settings when unexplained uterine bleeding occurs, postmenopausal bleeding is present, or when abnormalities are detected via ultrasound. Furthermore, these cannulae play a critical role in fertility workups, assessing the endometrial response to hormonal therapies, and monitoring high-risk patients for precancerous lesions. The inherent benefits of using these devices—such as being outpatient procedures, requiring minimal or no anesthesia, reducing hospital stays, and providing quick results—have significantly accelerated their adoption across different healthcare settings. This procedural efficiency and lower cost profile compared to operative procedures drive demand across established and emerging healthcare infrastructures.

Major driving factors fueling the expansion of this market include the global increase in the incidence and prevalence of gynecological cancers, particularly endometrial cancer, which necessitates early and accurate detection. Furthermore, the rising awareness among women regarding routine health screenings and the growing geriatric female population, which is more susceptible to uterine disorders, contribute substantially to market growth. Technological advancements leading to the development of cannulae that offer enhanced flexibility, smaller diameters, and superior vacuum capabilities are making procedures more accessible and less traumatic for patients. Favorable reimbursement policies in developed economies and increasing investments in women's healthcare infrastructure in developing regions further solidify the positive trajectory of the Endometrial Biopsy Cannulae Market.

The Endometrial Biopsy Cannulae Market is experiencing robust growth driven by favorable business trends focused on disposable solutions and integration with advanced imaging technologies. Business strategies across major manufacturers emphasize geographical expansion, particularly into high-growth APAC and Latin American markets, and securing long-term contracts with large hospital networks and specialty clinics. The trend toward outpatient and ambulatory surgical centers (ASCs) is creating a significant demand shift toward disposable, easy-to-use cannulae kits, optimizing procedural throughput and minimizing sterilization costs. Furthermore, strategic acquisitions aimed at consolidating specialized product portfolios and enhancing supply chain resilience are defining the competitive dynamics. Innovation is centered on materials science to improve flexibility and ergonomic design for clinicians, ensuring the overall market structure remains highly dynamic and focused on quality diagnostics.

Regionally, North America maintains market leadership due to high healthcare expenditure, sophisticated diagnostic infrastructure, and high rates of awareness and screening protocols for gynecological malignancies. However, the Asia Pacific region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by substantial investments in healthcare facilities, expanding medical tourism, and a rapidly increasing patient pool requiring diagnostic intervention. Europe follows closely, benefiting from established public healthcare systems that prioritize cancer screening and detection, although regulatory harmonization presents a moderate challenge. The overall global trend reflects a strong correlation between economic development, healthcare accessibility, and the adoption rate of modern diagnostic cannulae, with emerging economies rapidly closing the gap in procedural volume.

Segmentation trends highlight the dominance of the disposable cannulae segment, attributed to enhanced safety protocols, reduced risk of cross-contamination, and ease of use. Within the application segment, oncology diagnostic procedures constitute the largest market share, driven by the necessity for definitive tissue diagnosis in suspected endometrial carcinoma cases. The end-user analysis indicates that hospitals, due to their capacity for high-volume procedures and complex case management, remain the primary consumption point, although specialty clinics and independent diagnostic labs are rapidly increasing their market penetration by offering convenient, focused gynecological care. Material-wise, flexible plastic cannulae are preferred over rigid metallic options due to improved patient tolerance and ease of navigation through anatomical structures, thereby shaping future product development pipelines.

Common user questions regarding AI's impact on the Endometrial Biopsy Cannulae Market frequently center on whether AI can replace the physical biopsy procedure, how AI assists in slide analysis post-biopsy, and if AI integration will lead to entirely non-invasive diagnostic tools that render cannulae obsolete. Users are keen to understand the synergy between physical sampling tools and sophisticated digital diagnostics. The consensus summarized is that while AI will not replace the necessity of obtaining the physical tissue sample (the function of the cannulae), it profoundly impacts the subsequent diagnostic workflow. AI algorithms are increasingly employed for rapid, high-throughput analysis of the collected endometrial tissue, enhancing pathologist efficiency, improving diagnostic consistency, and potentially flagging subtle precancerous lesions that might be missed by the human eye. This integration drives demand for higher quality, better preserved tissue samples, thus indirectly influencing the design requirements for cannulae (e.g., enhanced suction mechanisms to maintain cellular integrity). AI serves as a powerful accelerator in the diagnostic phase, making the biopsy procedure itself more valuable.

The Endometrial Biopsy Cannulae Market is propelled by strong drivers, primarily the rising global burden of endometrial cancer and the increasing emphasis on early detection through minimally invasive procedures. However, the market faces significant restraints, chiefly stemming from patient discomfort associated with the procedure and the inherent risk of inadequate sampling, which necessitates repeat biopsies. Opportunities abound in the development of specialized, highly flexible cannulae integrated with vacuum regulation systems and the strategic expansion into developing economies with improving healthcare infrastructures. These forces create a dynamic environment where technological innovation acts as the primary impact force, mitigating restraints and amplifying drivers.

The key drivers include the demographic shift toward an aging global population, where women over 50 face a higher risk of uterine pathologies, thus increasing screening volumes. Furthermore, substantial technological advancements, such as the introduction of smaller diameter cannulae and specialized tip designs (e.g., Pipelle-type devices), have significantly improved patient compliance and reduced procedural failure rates. Government initiatives and increased funding for cancer screening programs in regions like North America and Western Europe also serve as major market catalysts. These drivers ensure a steady increase in procedural volume, positioning the cannulae as standard first-line diagnostic tools before resorting to more invasive surgical interventions.

Restraints are primarily linked to clinical challenges. Despite being minimally invasive, the procedure can cause cramping and pain, discouraging some women from follow-up screenings. Moreover, a critical restraint is the possibility of obtaining insufficient or non-diagnostic tissue samples, which requires rescheduling the procedure and increases healthcare costs. Regulatory hurdles and stringent approval processes for new medical devices, particularly in highly controlled markets, also act as constraints, delaying the introduction of advanced products. Overcoming these restraints necessitates sustained investment in clinical training for practitioners to maximize sample yield and in developing next-generation cannulae focused on pain reduction through smoother insertion profiles and superior vacuum control.

Opportunities for growth are concentrated in untapped geographical markets, particularly in populous regions of Asia where cancer awareness and access to gynecological screening are rapidly increasing. Furthermore, manufacturers have a significant opportunity to develop hybrid devices that combine sampling with simultaneous hysteroscopic visualization, enhancing targeting accuracy and reducing the incidence of non-diagnostic samples. Strategic partnerships with training institutions to standardize biopsy techniques and integrate cannulae with telemedicine platforms for remote consultation and diagnostic review present viable avenues for market penetration and expansion. Impact forces are overwhelmingly positive, driven by the ethical imperative for early cancer detection and technological breakthroughs that continuously improve the device performance and patient experience.

The Endometrial Biopsy Cannulae Market segmentation is analyzed primarily based on Type, Usage, and End-User, reflecting the diverse clinical requirements and preferences across global healthcare systems. The market is fundamentally segmented by the structural design of the device (flexible versus rigid), which dictates suitability for different anatomical challenges and physician preferences. Crucially, the segmentation by usage (disposable versus reusable) holds significant weight, driven by infection control mandates and the trade-off between procedural convenience and long-term cost efficiency. Understanding these segments is vital for manufacturers focusing their R&D efforts and marketing strategies toward the most rapidly expanding and profitable niches within women's health diagnostics, particularly catering to the shift toward outpatient settings.

The Disposable segment dominates the market due to the prevailing emphasis on sterility and minimizing the risk of cross-contamination, particularly in high-volume settings like hospitals and ASCs. Although reusable cannulae offer cost savings per use, the comprehensive costs associated with sterilization, tracking, and potential damage often render disposable options more practical and compliant with strict hospital protocols. Furthermore, the End-User segment shows high consumption rates in Hospitals, which handle the most complex cases and maintain large gynecological departments. However, the rapidly expanding network of Specialty Clinics, offering focused and timely gynecological care, is expected to exhibit the fastest growth rate, leveraging the convenience and minimally invasive nature of modern cannulae.

Segmentation by Type reveals that Flexible Cannulae, such as the popular Pipelle endometrial sampler, command a larger share. Their inherent design allows for easier navigation through a potentially curved cervical canal, reducing patient discomfort and the risk of uterine perforation compared to older, more rigid designs. Rigid cannulae, while less popular, still maintain a niche role in specific diagnostic procedures where maximum control over the sample collection trajectory is required, often employed under hysteroscopic guidance. This nuanced segmentation underscores the market's maturity and its capability to cater to a broad spectrum of clinical situations, ensuring appropriate tooling is available for diverse patient populations and clinical settings globally.

The value chain for the Endometrial Biopsy Cannulae Market starts with raw material procurement, primarily medical-grade plastics (polyethylene, polypropylene) and specialty metals (stainless steel) for rigid components. Upstream analysis involves optimizing the procurement of these high-quality materials, which must meet stringent biocompatibility and sterilization standards. Manufacturers focus on strategic sourcing to ensure material quality consistency and cost efficiency. The subsequent manufacturing phase involves precision molding, assembly, sterilization (often using Ethylene Oxide or gamma radiation), and rigorous quality control testing to comply with international regulatory standards like FDA and CE marking. This upstream process determines the final product's performance characteristics, flexibility, and safety profile, driving manufacturing expertise as a key competitive factor.

The downstream segment focuses on distribution and logistics. Cannulae are distributed through several channels: direct sales forces, specialized medical device distributors, and large-scale procurement organizations (GPOs) that service extensive hospital networks. Direct channels are common for large multinational players serving major medical centers, allowing for better margin control and direct customer feedback. Indirect channels, utilizing specialized distributors, are essential for reaching smaller clinics, rural hospitals, and international markets where local regulatory expertise is necessary. The distribution channel must ensure the sterile integrity and timely delivery of these critical diagnostic tools, making inventory management and robust supply chain logistics essential components of the downstream value proposition.

Potential customers, including hospitals, specialty clinics, and ASCs, represent the final stage of the value chain. Their purchasing decisions are heavily influenced by clinical efficacy, procedural convenience, pricing structure (especially for disposable items), and brand reputation. Successful market penetration relies on effective training and support provided by manufacturers or distributors to ensure proper clinical usage, minimizing sample inadequacy rates. The shift towards bulk procurement through GPOs necessitates competitive pricing and demonstrable clinical outcomes. The value chain is constantly optimized to reduce the time from production to patient usage while maintaining the highest possible quality and regulatory compliance throughout the procurement, manufacturing, and distribution processes.

The primary and largest segment of potential customers for Endometrial Biopsy Cannulae is comprehensive healthcare facilities, particularly large, multi-specialty Hospitals. These institutions serve as high-volume end-users due to their extensive gynecology and oncology departments, access to sophisticated imaging technologies for guidance, and the capability to manage complex diagnostic and therapeutic pathways. Hospitals require bulk purchasing of both disposable and specialized rigid cannulae and prioritize products that integrate seamlessly into their infection control and procedural workflows, often making purchasing decisions through centralized committees and GPO contracts based on cost-effectiveness and clinical evidence.

A rapidly expanding customer base includes Specialty Clinics and dedicated Women’s Health Centers. These centers focus exclusively on gynecological and obstetrics care, prioritizing efficiency, patient comfort, and rapid turnaround times for diagnostic results. They typically favor user-friendly, highly flexible, disposable cannulae, such as the Pipelle sampler, because they enable quick, outpatient procedures without the need for extensive surgical setups. This customer group places a high value on product ergonomics and minimal patient discomfort, making device features that support office-based procedures a significant purchasing determinant.

Ambulatory Surgical Centers (ASCs) and Independent Diagnostic Laboratories also represent crucial potential customers. ASCs utilize cannulae for scheduled, minor diagnostic procedures performed under light sedation, valuing streamlined processes and cost containment, favoring economical, high-quality disposable options. Diagnostic laboratories, while not directly performing the biopsy, often influence purchasing decisions by providing feedback to referring physicians regarding sample quality and adequacy, indirectly promoting cannulae brands known for superior tissue yields and sample preservation capabilities. This diverse customer base requires manufacturers to maintain a varied product portfolio catering to differing needs regarding volume, budget, and procedural setting.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450.5 Million |

| Market Forecast in 2033 | USD 765.2 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, CooperSurgical, Hologic, Karl Storz, B. Braun Melsungen, Cook Medical, BD (Becton, Dickinson and Company), Ethicon (J&J), Gynuity Health Projects, DTR Medical, Sklar Instruments, RI.MOS., Sterylab S.r.l., Biopsybell S.r.l., Sonomed Srl, Ziemer Group, PBN Medicals, J. SISKO LTD, Precision Medical, Advin Health Care. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for Endometrial Biopsy Cannulae is dominated by minimally invasive design principles centered on improving patient experience and diagnostic yield. The most pervasive technology is the simple, high-vacuum suction cannula, famously embodied by the Pipelle sampler, which utilizes a plunger mechanism or external vacuum source to draw tissue into the barrel. Recent advancements focus on material science, employing advanced polymers that provide optimal flexibility and strength, allowing the cannula to conform to the uterine anatomy while maintaining structural integrity during insertion and suction. Furthermore, innovations in tip design, including specialized atraumatic profiles and side-port openings, are engineered to maximize the collection of contiguous tissue strips while minimizing trauma and bleeding, thereby enhancing the quality of the pathological sample.

A critical area of technological advancement involves integrating these cannulae with auxiliary diagnostic technologies. While cannulae remain fundamentally mechanical devices, their utility is significantly boosted when used in conjunction with high-resolution ultrasound or hysteroscopy. The development of cannulae compatible with these visualization techniques allows physicians to precisely target areas of suspicion, moving from blind sampling to targeted biopsies. This integration minimizes the risk of non-diagnostic results and increases the procedure's overall efficacy, particularly in cases of focal lesions or small polyps. The focus on improved vacuum technology, utilizing controlled negative pressure systems, ensures uniform and sufficient sample aspiration, crucial for definitive diagnosis and differentiation between benign and malignant conditions.

Future technology is moving towards smart cannulae and enhanced sterility assurance. Research is ongoing into incorporating microscopic sensing capabilities within the cannula tip to provide real-time feedback on tissue capture quality, although this remains nascent. However, more immediate trends involve advanced coating technologies to reduce friction during insertion and antimicrobial treatments for reusable devices, enhancing safety. Furthermore, standardization in sterile packaging and manufacturing processes, utilizing automation and advanced cleanroom technologies, ensures that the high volume of disposable cannulae produced meets increasingly stringent global regulatory requirements, confirming that safety and efficacy remain paramount technological considerations in this sector.

North America currently holds the largest share of the Endometrial Biopsy Cannulae Market, driven by high adoption rates of advanced diagnostic procedures, extensive healthcare infrastructure, and favorable reimbursement policies covering women's cancer screening programs. The United States, in particular, contributes significantly due to its well-established clinical guidelines recommending prompt endometrial sampling for abnormal uterine bleeding (AUB), coupled with high public awareness of gynecological cancer risks. The presence of major market players and a robust technological innovation ecosystem ensures early access and rapid uptake of the latest cannula designs, maintaining North America's dominance despite the high procedural costs compared to other regions.

Europe represents the second-largest market, characterized by mature healthcare systems in Western countries (Germany, UK, France) that emphasize early cancer detection through national screening protocols. The market growth in Europe is steady, supported by standardized clinical practices and a high reliance on minimally invasive diagnostic tools. However, economic disparities and varied regulatory frameworks across Eastern European countries provide both challenges and opportunities for market penetration. The adoption of disposable cannulae is particularly strong in this region, driven by strict EU directives on cross-contamination control and patient safety, ensuring a steady demand flow within both public and private health sectors.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally throughout the forecast period. This rapid expansion is attributable to several factors: massive population size, increasing healthcare expenditure, improving access to gynecological specialists, and rising prevalence of lifestyle-related cancers. Countries like China, India, and Japan are investing heavily in modernizing hospital infrastructure and promoting women's health initiatives. The APAC market shows a strong preference for cost-effective solutions, initially driving demand for reusable cannulae, though the trend is shifting towards disposable models as economic stability improves and infection control awareness heightens. This region offers immense untapped potential for manufacturers willing to navigate complex local regulatory environments and adapt pricing strategies.

Latin America and the Middle East & Africa (MEA) represent emerging markets with substantial growth potential. In Latin America, improving economic conditions and expansion of private healthcare services are boosting the adoption of advanced diagnostic tools. Brazil and Mexico are key contributors. The MEA region faces challenges related to fragmented healthcare systems and lower per capita healthcare spending, yet urbanization and growing initiatives focusing on women's cancer screening, particularly in the UAE and Saudi Arabia, are generating measurable demand. Market penetration here requires focused efforts on distribution logistics and training programs to ensure the appropriate use of cannulae, making strategic partnerships with local distributors critical for long-term success.

The primary function of an endometrial biopsy cannula is to obtain a sample of uterine lining tissue (endometrium) for diagnostic pathological examination, crucial for detecting conditions like cancer or hyperplasia. Its key benefit lies in providing a minimally invasive, outpatient alternative to surgical procedures like D&C, ensuring quick results and minimal recovery time.

Disposable endometrial biopsy cannulae currently dominate the market share. This preference is driven by stringent infection control mandates, the elimination of sterilization costs and logistical complexities associated with reusable devices, and the guaranteed sterility and high quality offered by single-use products, particularly in high-volume hospital settings.

Technological advancements address inadequate sampling risk through improved vacuum generation systems, enabling stronger and more controlled suction. Furthermore, specialized tip designs (e.g., side ports and atraumatic profiles) and the increasing use of cannulae under visualization technologies like hysteroscopy allow for more targeted and comprehensive tissue collection, significantly reducing the need for repeat procedures.

The main drivers include the escalating global incidence of endometrial and gynecological cancers requiring definitive tissue diagnosis, the aging female population susceptible to uterine disorders, and continuous product innovations focused on enhanced patient comfort and clinical efficacy, propelling the shift towards minimally invasive diagnostic procedures globally.

The Asia Pacific (APAC) region is anticipated to exhibit the fastest growth rate. This is due to massive government and private sector investments in modernizing healthcare infrastructure, rising awareness about women's health and cancer screening, and the sheer size of the target patient population across major developing economies like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.