ID : MRU_ 431347 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

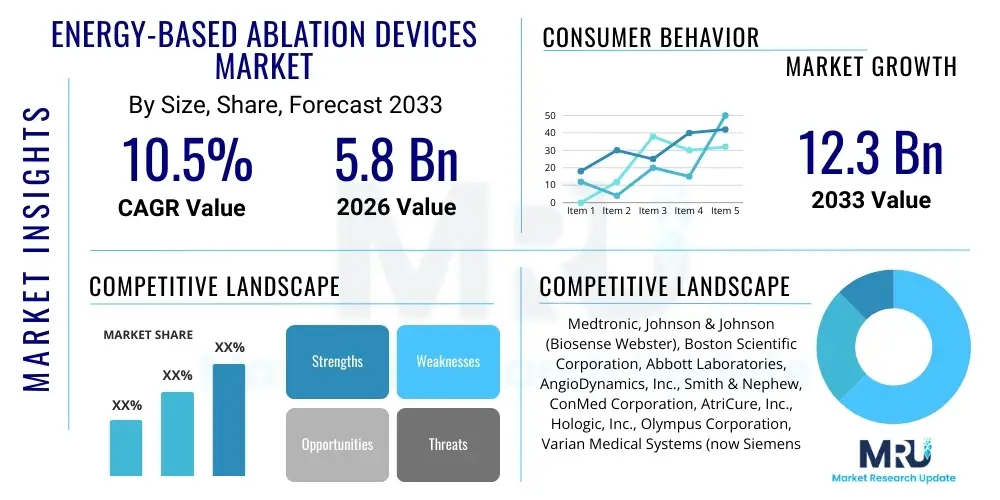

The Energy-Based Ablation Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2026 and 2033. The market is estimated at $5.8 Billion in 2026 and is projected to reach $12.3 Billion by the end of the forecast period in 2033.

The Energy-Based Ablation Devices Market encompasses specialized medical instruments utilizing various energy sources—such as radiofrequency (RF), microwave, cryoablation, laser, and high-intensity focused ultrasound (HIFU)—to precisely destroy or remove targeted tissues, often employed in minimally invasive surgical procedures. These devices facilitate the localized treatment of abnormal or diseased tissues without the need for extensive open surgery, significantly reducing patient recovery times, minimizing operative risk, and improving cosmetic outcomes. The primary product description includes generators, catheters, probes, needles, and control units, all engineered to deliver controlled thermal or non-thermal energy doses to specific anatomical locations, particularly vital in oncology, cardiology, pain management, and urology applications.

Major applications of these ablation systems span the treatment of complex cardiac arrhythmias, including atrial fibrillation (A-fib), the localized destruction of solid tumors in organs like the liver, lung, and kidney, and managing chronic pain conditions through nerve denervation. The fundamental benefits driving market adoption include the highly targeted nature of the treatment, which spares surrounding healthy tissue, the outpatient potential of many procedures, and the enhanced safety profile compared to traditional surgical resection. Furthermore, the increasing prevalence of lifestyle diseases leading to cancer and cardiac disorders, combined with a rising global geriatric population, accelerates the demand for less invasive therapeutic options provided by energy-based ablation technologies.

Key driving factors propelling market expansion are rooted in continuous technological advancements leading to smaller, more powerful, and more precise ablation systems, such as advanced navigation and imaging integration (e.g., fusion imaging and robotic assistance). Favorable reimbursement policies for minimally invasive procedures in developed healthcare economies, coupled with growing awareness among both clinicians and patients regarding the efficacy of these treatments, further solidify market growth. The shift from conventional surgery towards minimal access interventions across various surgical disciplines defines the current trajectory and long-term potential of the energy-based ablation devices sector.

The global Energy-Based Ablation Devices Market is witnessing robust expansion driven by the escalating demand for non-pharmacological, minimally invasive treatments across critical therapeutic areas like oncology and cardiac rhythm management. Business trends indicate a strong focus on integration—specifically combining ablation technologies with sophisticated 3D mapping and real-time imaging systems (like CT, MRI, and ultrasound) to ensure optimal procedural guidance and enhance efficacy rates. Furthermore, competitive strategies emphasize developing multi-modal systems, such as combining RF and cryoablation capabilities, to broaden the applicability of single-platform devices and capture diverse procedural volumes in hospitals and specialized clinics. Investment in disposable components, particularly specialized catheters and probes, represents a significant revenue stream and a core driver of technological innovation.

Regionally, North America maintains market dominance due to high healthcare expenditure, established clinical infrastructure, rapid adoption of advanced technologies, and favorable regulatory frameworks for novel medical devices. However, the Asia Pacific (APAC) region is projected to register the fastest growth, propelled by increasing medical tourism, improving healthcare access in emerging economies like China and India, and a rising prevalence of target diseases requiring interventional treatments. European markets demonstrate steady growth, supported by strong research and development activities and stringent quality standards, particularly concerning devices used in cardiac electrophysiology.

Segment trends highlight the technological segment dominance of Radiofrequency (RF) ablation due to its long history, versatility, and established clinical effectiveness, although Microwave (MW) ablation is rapidly gaining ground, particularly in liver and lung tumor ablation, owing to its ability to treat larger volumes faster and less susceptible to the heat-sink effect. Within the application segmentation, Oncology remains the most lucrative segment, driven by the expanding indications for treating small, localized tumors where ablation offers a curative option. End-user analysis confirms that hospitals remain the largest purchasers, yet the shift toward Ambulatory Surgical Centers (ASCs) is accelerating due to cost-efficiency and procedural efficiency advantages, reflecting broader healthcare decentralization trends.

User queries regarding AI's influence on the Energy-Based Ablation Devices Market predominantly revolve around three core themes: improving targeting precision, enhancing procedural safety through real-time feedback, and automating aspects of treatment planning. Users frequently ask how AI-driven algorithms can process complex imaging data (e.g., pre-operative CT/MRI scans combined with intra-operative electroanatomical mapping) to accurately delineate tumor margins or pathological tissue boundaries, which are critical for successful ablation. Concerns also focus on whether AI can predict treatment outcomes and personalize energy delivery profiles based on individual patient tissue characteristics, thereby minimizing complications and recurrence rates. The key expectation is that AI will transform ablation from an operator-dependent skill into a highly standardized, optimized, and predictive therapeutic process.

The integration of Artificial Intelligence and Machine Learning (ML) algorithms is set to revolutionize the efficiency and effectiveness of ablation procedures. In the planning phase, AI models analyze vast datasets to determine the optimal trajectory, probe placement, and required energy settings, significantly reducing procedural variability. During the intervention, real-time AI processing of thermal mapping, impedance data, or force sensing information provides immediate feedback to the clinician, adjusting energy delivery parameters automatically to maintain the desired lesion size and temperature, crucial for mitigating risks such as unintended damage to adjacent critical structures.

Furthermore, AI-powered predictive analytics are being developed to assess the risk of complications or recurrence post-ablation, guiding follow-up strategies and potentially personalizing subsequent treatment plans. This predictive capability optimizes patient care pathways, moving beyond simple procedural success rates to overall long-term patient survival and quality of life. As data volumes from ablation procedures increase, AI will become essential for pattern recognition, identifying subtle indicators of incomplete ablation, and ensuring the highest standard of minimal residual disease. This shift towards intelligent ablation platforms enhances the overall value proposition of energy-based devices.

The Energy-Based Ablation Devices Market is primarily driven by the increasing global incidence of chronic diseases, particularly cancer and cardiac arrhythmias, necessitating localized, less invasive treatment modalities. Restraints include the high initial capital expenditure associated with purchasing advanced ablation systems and the steep learning curve required for operating complex devices, potentially limiting adoption in resource-constrained environments. Opportunities are significantly focused on emerging economies, expanding indications for ablation (e.g., neurological disorders, benign prostatic hyperplasia), and the development of cost-effective, portable ablation solutions. The impact forces are generally positive, characterized by strong clinical validation and patient preference for minimally invasive procedures, exerting continuous pressure on manufacturers to innovate and lower procedure costs.

The core drivers include the undeniable success of minimally invasive surgical approaches, leading to reduced hospital stays and quicker patient recovery, which aligns perfectly with modern healthcare cost containment goals. Technological improvements, such as improved visualization techniques (e.g., fusion imaging combining pre-operative and intra-operative data) and the development of next-generation ablation energies like Pulsed Field Ablation (PFA), are expanding the safety window and effectiveness of the procedures. Restraints, conversely, center on regulatory hurdles, particularly in obtaining approvals for novel energy sources or new therapeutic indications, and the ongoing challenge of achieving complete tissue necrosis without compromising adjacent vital structures, which requires impeccable technique and advanced monitoring systems.

Opportunities lie in shifting geographical focus, as the immense, untapped patient pools in regions like APAC and Latin America present massive growth potential once infrastructure constraints are overcome and training standards are elevated. The successful integration of robotics and AI into existing ablation platforms offers high-impact potential by standardizing complex procedures like cardiac ablation and achieving higher success rates. Furthermore, the strong positive impact force stems from demographic trends—an aging population worldwide is inherently more susceptible to conditions requiring ablation, ensuring sustained long-term demand for these therapeutic tools across diverse clinical settings.

The Energy-Based Ablation Devices Market is comprehensively segmented based on the type of energy source utilized, the clinical application where the device is deployed, and the specific end-user settings procuring the equipment. This detailed segmentation allows for a precise understanding of market dynamics, distinguishing between established technologies like Radiofrequency (RF) and nascent, high-growth segments such as Pulsed Field Ablation (PFA) and High-Intensity Focused Ultrasound (HIFU). The interplay between technological precision and expanding clinical indications, particularly in complex tumor ablation and cardiac electrophysiology, dictates the growth trajectory of each segment. Understanding these segment contributions is crucial for stakeholders to align their R&D and market penetration strategies effectively.

The dominance of the Oncology application segment reflects the increasing utilization of localized ablation techniques as a viable alternative or adjunct therapy to traditional surgical resection, chemotherapy, and radiation, driven by improved clinical outcomes in small, localized tumors. Conversely, the growth rate within the Cardiology segment is fueled by the epidemic increase in atrial fibrillation incidence globally, demanding higher volumes of catheter-based electrophysiological interventions. Technological advancements are highly segmented, with RF ablation holding the largest revenue share due to maturity and widespread adoption, while microwave ablation is experiencing rapid growth due to its superior performance in certain high-volume ablation zones, particularly in the hepatic system.

Analyzing end-user segmentation reveals a significant reliance on Hospitals for complex, high-risk procedures involving intricate system setups. However, the rapidly growing adoption rate in Ambulatory Surgical Centers (ASCs) is driven by the movement of routine, less complex ablation procedures, such as pain management and minor orthopedic ablations, out of acute care settings, aiming for improved cost efficiency and patient throughput. This market segmentation highlights a dual structure: established, high-revenue segments providing stability, and specialized, high-growth segments driving technological innovation and market expansion into new clinical domains.

The value chain for the Energy-Based Ablation Devices Market is complex, beginning with the upstream analysis focusing on the procurement of specialized, high-purity raw materials such as proprietary metal alloys, advanced polymers, and complex microelectronic components crucial for generator and catheter manufacturing. Research and development (R&D) forms the most value-intensive stage, involving extensive collaboration with clinicians, physicists, and software engineers to develop safe, effective, and image-compatible devices. Key suppliers often specialize in high-precision manufacturing processes necessary for producing slender, flexible catheters and probes designed for minimally invasive access. Intellectual property surrounding energy delivery systems and specialized tips is a significant barrier to entry and a core source of competitive advantage in this upstream segment.

Midstream activities involve the actual manufacturing, assembly, rigorous quality control, and testing of the final ablation systems, including the complex generators and disposable accessories. Following manufacturing, the distribution channel plays a pivotal role in ensuring market access. Direct distribution, involving manufacturers selling directly to major hospital networks and large specialized clinics, is common for high-cost capital equipment like RF and HIFU generators, allowing manufacturers to maintain tight control over installation, training, and maintenance. Indirect distribution involves leveraging specialized medical device distributors or Group Purchasing Organizations (GPOs), particularly in fragmented markets or for distributing high-volume disposable components and accessories, providing wider reach and logistical efficiency.

Downstream analysis centers on the end-users—hospitals, ASCs, and clinics—where the value is realized through clinical application. Post-sales services, including system maintenance, technical support, clinician training, and software updates, constitute a critical, ongoing revenue stream and are essential for maximizing device uptime and user proficiency. Customer relationship management and continuous clinical evidence generation, often through post-market surveillance studies, complete the downstream value creation, ensuring sustained trust and adoption by the medical community. The efficiency and reliability of the service component directly influence the overall perceived value of the ablation platform.

The primary customers for Energy-Based Ablation Devices are specialized healthcare facilities equipped to perform complex interventional procedures requiring advanced imaging and monitoring capabilities. Hospitals, particularly large university hospitals and regional tertiary care centers, represent the largest customer segment. These institutions possess the necessary high capital budgets, a wide range of surgical specialties (cardiology, oncology, urology), and the complex infrastructure required for housing and operating sophisticated ablation systems such as integrated robotic navigation and high-intensity focused ultrasound units. Their procedural volumes for conditions like atrial fibrillation and solid tumor ablation are consistently high, necessitating continuous investment in modern equipment and disposable components.

Ambulatory Surgical Centers (ASCs) constitute a rapidly growing customer base, specifically for procedures that are migrating out of inpatient hospital settings due to their lower complexity and shorter recovery times. ASCs are key buyers of less invasive, higher-volume devices used in pain management (e.g., chronic back pain nerve ablation) and specific gynecological or urological procedures. The driving factor for ASC adoption is cost-effectiveness and increased operational efficiency, making them crucial targets for manufacturers offering streamlined, easy-to-use, and moderately priced ablation solutions that enhance patient throughput.

Specialty Clinics and Interventional Radiology Centers form the third significant customer segment. These facilities, often dedicated to a narrow range of treatments (e.g., vascular intervention or minimally invasive oncology), prioritize devices that offer high precision and specialized application focus, such as dedicated microwave or cryoablation systems for percutaneous tumor destruction. Research institutes and academic medical centers also serve as important, albeit smaller, customers, primarily procuring systems for clinical trials, technology validation, and training purposes, influencing future clinical standards and technology adoption.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $5.8 Billion |

| Market Forecast in 2033 | $12.3 Billion |

| Growth Rate | 10.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Johnson & Johnson (Biosense Webster), Boston Scientific Corporation, Abbott Laboratories, AngioDynamics, Inc., Smith & Nephew, ConMed Corporation, AtriCure, Inc., Hologic, Inc., Olympus Corporation, Varian Medical Systems (now Siemens Healthineers), EDAP TMS, Misonix, Inc., Teleflex Incorporated, MicroPort Scientific Corporation, Tandem Diabetes Care, Inc., CooperSurgical Inc., IMRIS, Elekta AB, St. Jude Medical (now part of Abbott) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Energy-Based Ablation Devices Market is characterized by intense innovation across multiple energy modalities aimed at improving precision, speed, and safety. Radiofrequency (RF) ablation remains the most mature technology, utilizing electromagnetic energy to generate heat through resistive heating of tissue surrounding an electrode, leading to coagulation necrosis. Advances in RF systems are focused on irrigated tip catheters, which prevent char formation and allow for the creation of deeper, larger lesions, critical for pulmonary vein isolation in cardiac ablation. Microwave (MW) ablation, a fast-growing competitor, utilizes higher frequency electromagnetic waves (typically 915 MHz or 2.45 GHz) that generate heat via molecular vibration, offering the advantages of faster procedure times, independence from the heat-sink effect (making it better for perivascular tumors), and the ability to create consistently larger spherical ablation zones, enhancing its utility in liver and lung tumor management.

Cryoablation, an alternative thermal modality, uses extreme cold (often via circulating argon or nitrogen gas) to induce cell death through freezing and thawing cycles. This technology is particularly valued for procedures near sensitive structures, such as in kidney tumor ablation, as the induced ice ball is visible under ultrasound or CT imaging, providing a clear safety margin. Furthermore, cryoablation minimizes pain due to its analgesic effect, making it suitable for certain pain management applications. Laser ablation (or interstitial laser photocoagulation) uses focused light energy delivered via optical fibers, favored for precise, small-volume tumor destruction in neurosurgery and breast oncology where precise targeting is paramount. High-Intensity Focused Ultrasound (HIFU) represents a non-invasive thermal technique, focusing high-intensity acoustic energy deep into the body without an incision, primarily used in treating uterine fibroids, prostate conditions, and bone metastases, although its complexity limits widespread adoption compared to percutaneous methods.

The most disruptive technology currently emerging is Pulsed Field Ablation (PFA), a non-thermal modality utilizing high-voltage, ultra-short electrical pulses to selectively create permanent pores in cell membranes (irreversible electroporation), leading to highly targeted cell death without thermal damage to adjacent connective tissues, nerves, or vasculature. PFA promises superior safety, particularly in cardiac ablation procedures where damage to the esophagus or phrenic nerve is a critical risk associated with thermal methods. The landscape is moving toward multi-modal platforms where different energies can be deployed interchangeably, and system integration with advanced imaging—including robotics and augmented reality overlays—is becoming standard, ensuring enhanced control and reduced procedural variability across all ablation techniques.

The primary driver is the significant shift in surgical standards towards minimally invasive procedures, coupled with the rising global incidence of treatable chronic diseases, particularly complex cardiac arrhythmias (like A-fib) and localized solid tumors (liver, lung, kidney), where ablation offers a less traumatic alternative to traditional surgery.

Pulsed Field Ablation (PFA) is projected to experience the fastest growth due to its non-thermal mechanism (irreversible electroporation), which offers superior safety margins by selectively destroying target cells while sparing critical adjacent structures like nerves and blood vessels, minimizing complications in complex areas like the heart.

AI enhances efficacy by integrating pre-operative and real-time imaging data to optimize treatment planning, guide precise catheter or probe placement, and automatically modulate energy delivery parameters based on instantaneous tissue response, ensuring complete ablation lesions and reducing procedural variance.

The main constraints include the substantial initial capital investment required for purchasing sophisticated generators and imaging platforms, the high cost of disposable specialized catheters/probes, and the necessity for extensive specialized training for clinical professionals to operate these complex systems effectively.

North America dominates the market revenue, driven by high per capita healthcare spending, advanced medical infrastructure, rapid uptake of innovative technologies, favorable reimbursement environments for complex interventions, and the presence of leading global medical device manufacturers.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.