ID : MRU_ 432433 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

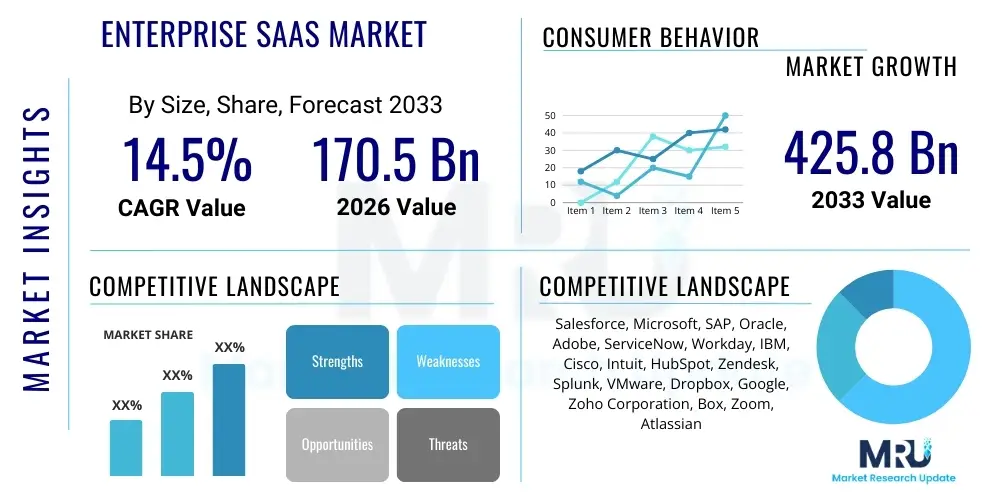

The Enterprise SaaS Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% (CAGR) between 2026 and 2033. The market is estimated at USD 170.5 Billion in 2026 and is projected to reach USD 425.8 Billion by the end of the forecast period in 2033.

The Enterprise Software as a Service (SaaS) market encompasses a diverse range of cloud-based applications designed to support mission-critical business processes within large organizations. These solutions, which include Customer Relationship Management (CRM), Enterprise Resource Planning (ERP), Human Capital Management (HCM), and specialized industry applications, are delivered over the internet on a subscription basis, eliminating the need for extensive on-premise hardware and maintenance. The fundamental shift driving this market is the pursuit of operational agility, scalability, and cost efficiency, allowing enterprises to allocate IT budgets toward innovation rather than infrastructure upkeep. The mature integration capabilities of modern SaaS platforms further enable seamless data flow across different functional departments, creating unified and actionable views of business operations.

Product descriptions within the Enterprise SaaS landscape often emphasize modularity and deep vertical specialization. For instance, advanced ERP SaaS solutions now integrate AI/ML capabilities for predictive analytics in supply chain management, while next-generation HCM platforms leverage behavioral science to optimize employee engagement and talent acquisition. Major applications span core business functions, including finance, sales, marketing, operations, and IT service management. The critical benefits derived from adopting these platforms include faster deployment cycles, automatic updates ensuring compliance and feature parity, inherent elasticity to handle fluctuating workloads, and predictable operational expenditure models replacing large capital outlays.

Key driving factors accelerating market expansion include the global push for digital transformation across all industries, the imperative for remote work enablement demanding secure and accessible cloud solutions, and the continuous innovation cycles delivered by leading vendors. Furthermore, the increasing complexity of regulatory environments worldwide necessitates flexible software solutions capable of rapid adaptation, which SaaS models inherently provide. The ongoing need for robust data security and resilience against cyber threats is also being addressed effectively by hyper-scale cloud providers underpinning Enterprise SaaS, reinforcing confidence among large corporations regarding data governance and risk mitigation.

The Enterprise SaaS market is currently characterized by intense competition focused on platform consolidation, deep integration of generative AI features, and a pronounced shift toward verticalized offerings designed for specific industry needs, moving beyond generalized horizontal applications. Business trends show a strong prioritization of core system migration (especially ERP and core banking) to the cloud, driven by the end-of-life cycles of legacy systems and the demand for real-time transactional capabilities. Mergers and acquisitions remain a central theme as large players seek to acquire niche capabilities, particularly in low-code/no-code development and specialized data analytics, aiming to create comprehensive, end-to-end digital transformation suites for their clients.

Regional trends highlight North America maintaining market dominance, propelled by high technological adoption rates and the presence of major SaaS providers and early-stage innovators; however, the Asia Pacific (APAC) region is demonstrating the highest growth trajectory. This APAC surge is fueled by rapid industrialization, increasing digitalization investments in emerging economies like India and Southeast Asia, and robust government initiatives promoting cloud infrastructure development. Europe continues steady growth, heavily focused on data sovereignty and compliance requirements such as GDPR, driving demand for localized cloud solutions and specialized SaaS platforms that ensure regulatory adherence.

Segments trends indicate that Large Enterprises remain the primary revenue generator, yet the Small and Medium-sized Enterprises (SMEs) segment is poised for accelerated growth, supported by accessible, scalable, and affordable entry-level SaaS subscriptions. Functionally, CRM and ERP segments retain the largest market share, but niche areas like cybersecurity management SaaS (CSMS) and specialized industry clouds (e.g., healthcare technology, fin-tech) are experiencing explosive growth rates. Deployment preference is strongly trending towards Hybrid Cloud models for organizations maintaining sensitive on-premise data, though Public Cloud remains the foundational backbone for most new applications due to its unparalleled elasticity and cost-effectiveness.

Users frequently inquire about the practical implementation and return on investment (ROI) of generative AI within their existing Enterprise SaaS stacks, particularly regarding data privacy risks, job displacement fears, and the challenge of integrating nascent AI features with complex, established workflows. Common concerns revolve around ensuring AI outputs are accurate, bias-free, and compliant with industry regulations, especially when deployed in customer-facing applications or decision-support systems. Furthermore, organizations are seeking clear strategies from vendors on how AI can fundamentally transform labor-intensive processes—such as automated report generation, personalized customer interactions, and predictive maintenance—without requiring a complete overhaul of their infrastructure. The consensus expectation is that AI must deliver tangible efficiency gains and unlock novel business insights that traditional analytics tools cannot provide.

The immediate impact of Artificial Intelligence, particularly Generative AI (GenAI), on the Enterprise SaaS market is transformative, shifting the focus from automation of routine tasks to augmentation of high-value professional functions. Vendors are rapidly embedding AI capabilities directly into their platform interfaces, enabling functionalities like automated code generation for developers, personalized sales content creation for CRM users, and sophisticated anomaly detection in financial systems. This integration minimizes the friction associated with deploying AI, allowing end-users to leverage advanced machine learning models without requiring specialized data science expertise. The long-term effect will be the convergence of traditional application software with intelligent platforms that continuously learn and optimize business processes in real-time, thereby resetting competitive benchmarks in operational excellence.

This integration drives increased stickiness for SaaS platforms, as the proprietary data collected and analyzed by the platform becomes an increasingly valuable asset, enhancing the accuracy and utility of the embedded AI models. For enterprises, the adoption of AI-enhanced SaaS translates into significant productivity gains, reduced time-to-market for new services, and superior customer experience management. However, this also necessitates substantial investment in data governance and security frameworks to manage the voluminous and sensitive data streams powering these AI engines, emphasizing the need for robust, trustworthy AI (TAI) components within the SaaS offerings.

The Enterprise SaaS market is propelled by powerful macro-economic and technological drivers, balanced by significant restraining factors centered primarily around security and legacy system inertia, all while numerous opportunities emerge from specialized technological adoption. Primary drivers include the necessity for remote and hybrid work environments, the inherent scalability and flexibility offered by cloud solutions, and the continuous decline in total cost of ownership (TCO) compared to traditional on-premise solutions over the long term. These forces collectively push enterprises toward cloud migration. Restraints typically involve the high initial costs and complexities associated with migrating large, intricate datasets from legacy on-premise systems, concerns over data sovereignty and compliance requirements unique to highly regulated sectors (like BFSI and Healthcare), and vendor lock-in risks associated with proprietary cloud ecosystems.

Opportunities in the market are abundant, notably focusing on the proliferation of vertical SaaS (VSaaS) solutions tailored to highly specific industry processes, such as pharmaceuticals R&D or advanced manufacturing operations, which command higher average contract values. Furthermore, the integration of cutting-edge technologies like blockchain for secure supply chain tracking, edge computing for localized processing power, and quantum-safe cryptography represents significant future growth avenues. The impact forces acting upon the market ensure continuous evolution, demanding that vendors not only innovate in core functional areas but also establish superior security and regulatory compliance records to build enterprise trust.

The overall impact of these forces results in a highly dynamic and fragmented competitive landscape. Technological forces mandate constant investment in R&D to incorporate AI/ML and advanced analytics, while regulatory forces dictate platform design, particularly regarding data residency and privacy controls. Economic forces favor subscription models, driving predictable recurring revenue for vendors and manageable operational expenditure for customers. The prevailing impact is a sustained, high-growth environment where differentiation increasingly relies on integration depth, industry specificity, and demonstrable security superiority, moving beyond simple cost advantages.

The Enterprise SaaS market is meticulously segmented across deployment type, enterprise size, functional application, and industry vertical, reflecting the varied technological requirements and budgetary constraints of different organizational types. This segmentation is crucial for market participants to tailor their go-to-market strategies and product development roadmaps. The deployment segment, for instance, highlights the ongoing strategic decisions enterprises face regarding data governance—choosing between the elasticity of the Public Cloud, the control of the Private Cloud, or the balanced approach of a Hybrid model. Understanding these segments provides clarity on where capital expenditure is being prioritized for digital transformation initiatives.

The Value Chain for the Enterprise SaaS market begins with the upstream activities of core infrastructure providers, namely the hyper-scale Public Cloud vendors (e.g., AWS, Microsoft Azure, Google Cloud Platform). These entities provide the foundational computing, storage, networking, and security layers that SaaS applications utilize. Upstream analysis also includes the developers of fundamental software technologies, open-source communities, and specialized AI/ML model providers, who contribute essential components to the overall SaaS product architecture. The efficiency and pricing of these upstream services critically influence the operational costs and scalability of the final SaaS product, making strategic partnerships with infrastructure providers paramount for SaaS firms.

Mid-stream activities are dominated by the core SaaS vendors themselves, involving product development, continuous feature updates (CI/CD pipelines), data management, security infrastructure maintenance, and application hosting. These vendors are responsible for translating core technology into user-centric, industry-specific solutions. Distribution channels are varied, incorporating both Direct Sales models, where large enterprise contracts are handled by dedicated sales teams for complex, customized deployments, and Indirect Channels, which include Value-Added Resellers (VARs), Managed Service Providers (MSPs), and system integrators. Indirect channels are particularly important for reaching SMEs and facilitating regional market entry and complex integrations with existing enterprise ecosystems.

The downstream analysis focuses on the end-user deployment, customization, and continuous utilization phases. This involves implementation consultants, training providers, and ongoing customer success support. Direct distribution ensures close customer feedback loops, allowing vendors to rapidly iterate product features based on enterprise needs. Indirect distribution, leveraging partners, allows for localized support and expertise necessary for complex global rollouts. A well-optimized value chain minimizes latency, ensures data security across all touchpoints, and maximizes the customer lifetime value (CLV) by providing consistent and high-quality service throughout the subscription lifecycle.

Potential customers for Enterprise SaaS solutions are broadly defined as organizations across all major industry verticals that possess complex operational requirements, significant employee bases, and a strategic mandate for digital transformation and technological modernization. These potential buyers typically fall into the Large Enterprise category, where the investment in integrated cloud platforms like ERP and HCM yields the highest operational efficiency gains and ROI. Specifically, multinational corporations seeking centralized control over global operations and highly regulated entities requiring auditable, secure, and compliant software platforms are prime targets. The increasing prevalence of modern IT infrastructure within SMEs, however, is rapidly expanding the potential customer base in this segment, particularly for specialized, lower-cost SaaS solutions.

End-user profiles vary significantly depending on the functional segment being targeted. For CRM SaaS, the key buyers are sales, marketing, and customer service departments, prioritizing platforms that enhance customer experience (CX) and streamline the sales funnel. For ERP and SCM SaaS, the buyers are typically the Chief Financial Officer (CFO) and Chief Operating Officer (COO) or their respective VPs, who focus on optimizing supply chain efficiency, financial reporting accuracy, and global resource allocation. HCM solutions target the Chief Human Resources Officer (CHRO), focusing on talent management, employee experience, and core HR functions.

The growing necessity for robust security and compliance in the face of escalating cyber threats means that the Chief Information Security Officer (CISO) and Chief Information Officer (CIO) are now critical buyers across all SaaS categories, ensuring that cloud vendor solutions meet stringent internal and external security standards. The most attractive potential customers are those undergoing significant business restructuring or geographical expansion, as these periods often necessitate the replacement of outdated software infrastructure with flexible, cloud-native Enterprise SaaS platforms capable of supporting rapid scaling and organizational change.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 170.5 Billion |

| Market Forecast in 2033 | USD 425.8 Billion |

| Growth Rate | 14.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Salesforce, Microsoft, SAP, Oracle, Adobe, ServiceNow, Workday, IBM, Cisco, Intuit, HubSpot, Zendesk, Splunk, VMware, Dropbox, Google, Zoho Corporation, Box, Zoom, Atlassian |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Enterprise SaaS market is underpinned by a dynamic technological landscape defined by the increasing sophistication of cloud-native architectures, the pervasive integration of Artificial Intelligence, and the adoption of modern development methodologies. Core technology relies on multi-tenant cloud architectures to achieve scale and resource pooling, primarily leveraging containers (Docker, Kubernetes) for application portability and rapid deployment across diverse cloud environments. This shift towards microservices architecture allows vendors to update and iterate components independently, significantly improving system resilience and reducing downtime for enterprise clients. Furthermore, the deployment of robust Application Programming Interfaces (APIs) is critical, enabling seamless interoperability between different enterprise systems, both internal and external to the SaaS platform, which is a key requirement for modern digital ecosystems.

A major technological inflection point is the aggressive incorporation of advanced analytics and Machine Learning (ML) engines. These technologies are no longer confined to specialized BI tools but are embedded directly into functional applications—for instance, predictive maintenance models in SCM or fraud detection algorithms in BFSI-specific SaaS. More recently, Generative AI (GenAI) models, often running on specialized GPU instances provided by hyper-scalers, are becoming foundational, enabling features that create personalized content, summarize vast amounts of unstructured data, and assist in automating complex decision-making processes, thereby fundamentally changing user interaction with enterprise software.

Security technologies remain paramount, driving innovation in areas such as Zero Trust Architecture (ZTA), enhanced identity and access management (IAM) solutions, and decentralized data encryption mechanisms to address growing data governance and compliance demands, especially concerning GDPR, CCPA, and HIPAA. Low-code/No-code (LCNC) platforms are also essential components of the current technology landscape, empowering business users to customize and extend SaaS applications without relying heavily on IT developers, accelerating time-to-value and fostering greater organizational agility in adapting the software to unique business requirements. This convergence of advanced AI, robust security, and agile development tools defines the modern competitive advantage in the Enterprise SaaS space.

Regional dynamics play a crucial role in shaping the Enterprise SaaS market, reflecting varying degrees of digitalization maturity, regulatory frameworks, and economic priorities. North America maintains its leadership position, driven by early and aggressive adoption of cloud technologies, significant R&D spending by tech giants, and a highly mature ecosystem of Venture Capital funding supporting continuous innovation in specialized SaaS. Key countries like the United States and Canada continue to be pioneers, focusing on large-scale platform migrations and incorporating cutting-edge AI features, especially within the financial and IT sectors.

Europe represents a large and complex market characterized by strong regulatory influence, particularly concerning data privacy and sovereignty (GDPR). Countries like Germany and the UK are major adopters, but there is a distinct preference for cloud solutions that offer localized data centers and certified compliance frameworks. The market growth in Europe is steady, driven primarily by manufacturing sector modernization (Industry 4.0) and public sector digitalization efforts, leading to strong demand for secure, hybrid cloud deployments.

The Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate globally. This expansion is powered by the rapid digitalization of economies in China, India, Japan, and Australia. Key factors include the massive growth of the SME segment seeking scalable solutions, increasing internet penetration, and supportive government policies pushing cloud adoption. While competition is intense, the sheer volume of potential new enterprise users and the high growth in e-commerce and manufacturing are positioning APAC as the most critical growth vector for global SaaS providers. Latin America (LATAM) and the Middle East and Africa (MEA) are emerging markets focusing heavily on adopting core SaaS functions (CRM, ERP) to modernize their BFSI and resource-based industries, often leapfrogging older on-premise generations directly to cloud-native solutions.

The Enterprise SaaS market is projected to experience robust expansion, achieving a Compound Annual Growth Rate (CAGR) of 14.5% between the forecast years of 2026 and 2033, driven by continuous digital transformation initiatives globally.

AI, particularly Generative AI, is shifting SaaS from simple automation to cognitive augmentation by embedding intelligent features like predictive analytics, automated content generation, and sophisticated anomaly detection directly into core business applications (e.g., ERP, CRM, HCM).

The Asia Pacific (APAC) region is anticipated to exhibit the fastest growth, fueled by accelerated SME digitalization, increasing government support for cloud infrastructure, and rapid expansion across manufacturing and e-commerce sectors.

Key restraints include pervasive concerns over data sovereignty and regulatory compliance (especially in Europe), the high complexity and cost associated with migrating large, intricate legacy systems, and the risk of vendor lock-in associated with proprietary cloud ecosystems.

The largest functional segments contributing significantly to market revenue are Customer Relationship Management (CRM) and Enterprise Resource Planning (ERP), as these systems form the core operational and transactional backbone for large organizations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.