ID : MRU_ 433177 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

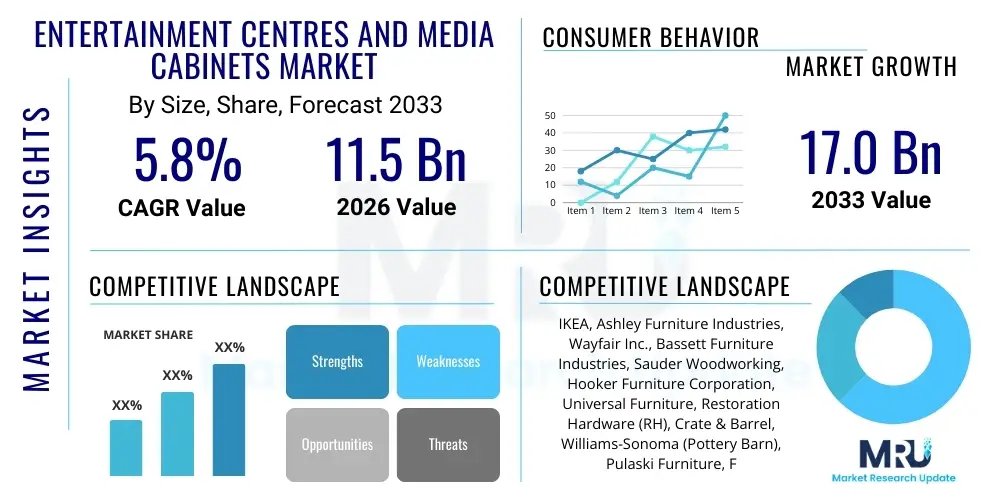

The Entertainment Centres and Media Cabinets Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 11.5 Billion in 2026 and is projected to reach USD 17.0 Billion by the end of the forecast period in 2033. This growth trajectory is fundamentally driven by the rising consumer demand for sophisticated, integrated home entertainment experiences and the continual miniaturization and integration of audiovisual technologies, necessitating specialized furniture solutions for optimized placement and aesthetic presentation.

The Entertainment Centres and Media Cabinets Market encompasses furniture solutions specifically designed to house, organize, and display audiovisual equipment, including televisions, soundbars, gaming consoles, digital media players, and associated storage media. These units, which range from small media consoles to expansive multi-component entertainment walls, serve dual purposes: functional equipment housing and aesthetic integration into modern living spaces. Major applications span residential homes, luxury apartments, and commercial settings such as hotel lounges and corporate breakout rooms, driven by the global proliferation of high-definition content consumption and streaming services. The primary benefits include enhanced cable management, protection of expensive electronics, and optimization of viewing angles. Driving factors propelling this market include increasing disposable incomes globally, the shift towards larger screen sizes (e.g., 65-inch and above), the adoption of smart home ecosystems, and a persistent focus on interior design trends that favor clean, minimalist aesthetics achieved through concealed storage.

The Entertainment Centres and Media Cabinets market is experiencing robust momentum, fundamentally supported by key business trends, including the rapid expansion of e-commerce channels, which allow manufacturers to reach niche consumer segments interested in highly customizable or bespoke furniture pieces. A significant segment trend is the sustained demand for modular and multifunctional units that can adapt to varying living space configurations and accommodate fluctuating technological requirements, such as built-in charging stations or integrated smart lighting. Geographically, North America and Europe remain mature, high-value markets, characterized by consumer preference for premium, durable materials like solid wood and integrated acoustic designs, while the Asia Pacific region is demonstrating the highest growth rates, fueled by burgeoning urbanization, increasing middle-class spending, and large-scale residential development projects requiring standardized yet stylish furniture solutions. Manufacturers are increasingly prioritizing sustainable sourcing and manufacturing processes, responding to growing consumer environmental consciousness, thereby establishing new competitive benchmarks centered around eco-friendly materials and design longevity.

User queries regarding AI’s influence on the Entertainment Centres and Media Cabinets Market predominantly revolve around the integration of voice command capabilities, the potential for furniture to dynamically adjust based on content being viewed (e.g., ambient lighting synchronization), and the role of AI in personalized furniture design. Users are concerned about future-proofing media cabinets against rapid technological obsolescence and expect AI to contribute to seamless user interaction and optimal environmental control within the entertainment space. The key thematic expectation is that AI will transform media cabinets from passive storage units into active, intelligent components of the smart home ecosystem, managing power, cable organization, and environmental conditions automatically to enhance the viewing experience while simplifying complex home theater setups for the average consumer, driving demand for technologically advanced, integrated furniture solutions.

The Entertainment Centres and Media Cabinets market dynamics are shaped by potent drivers, critical restraints, and substantial opportunities, which collectively define the impact forces acting upon industry growth. The market is primarily driven by the escalating demand for advanced home theater setups, the rapid global adoption of larger, flat-screen televisions (OLED, QLED technologies), and the continuous rise in discretionary consumer spending allocated toward home décor and modernization projects. Furthermore, urbanization trends, particularly in emerging economies, are increasing the demand for space-saving, aesthetically pleasing furniture solutions that integrate technology seamlessly into smaller living areas, emphasizing the need for vertical and modular designs. Restraints, conversely, include the high capital investment required for premium, solid-wood units, which deters price-sensitive consumers, and the increasing market saturation of low-cost, mass-produced cabinets, leading to intense pricing pressures across the entry-level segment. Additionally, the shift towards wall-mounting solutions for televisions and minimalist furniture designs, which sometimes bypass the need for traditional, bulky entertainment centers, poses a significant structural challenge to traditional cabinet manufacturers, requiring a pivot towards specialized media consoles.

Opportunities for expansion lie prominently in the development of 'smart furniture'—cabinets equipped with integrated wireless charging pads, hidden cable management systems, ambient LED lighting controlled via smartphone apps, and specialized acoustic materials designed to enhance speaker performance without visible modification. The increasing penetration of smart home technologies creates a fertile ground for manufacturers to offer high-margin, value-added products that act as centralized hubs for smart home networks. Geographically, untapped potential remains significant in developing regions where modernization of housing infrastructure is ongoing, offering substantial avenues for market entry through localized distribution partnerships and product customization tailored to regional aesthetic preferences and space constraints. Overcoming the restraint of perceived technological obsolescence requires manufacturers to adopt future-proof designs, such as adjustable shelving and standardized compartments capable of accommodating a wide array of existing and anticipated equipment form factors.

The principal impact forces shaping the market are the accelerating pace of technological innovation in audiovisual equipment, which necessitates continuous furniture redesign; the shifting landscape of distribution, heavily favoring direct-to-consumer (DTC) e-commerce models; and stringent environmental regulations concerning material sourcing, particularly forest certification standards (e.g., FSC), which influence manufacturing costs and consumer choice. Competitive pressure is intensifying as lifestyle brands and traditional furniture makers merge their product lines to offer holistic living room solutions, compelling specialized media cabinet manufacturers to differentiate through superior material quality, bespoke design services, and advanced functional integration. These forces collectively mandate agility in product development and supply chain management to maintain relevance in a rapidly evolving consumer electronics and interior design ecosystem.

The Entertainment Centres and Media Cabinets Market is meticulously segmented based on product type, material composition, distribution channel, and end-user application, allowing for a detailed examination of consumer preferences and market profitability across various subsets. Product segmentation is crucial, differentiating between large, multi-component entertainment walls that dominate high-end residential installations, and smaller, minimalist media consoles preferred in urban settings. Material segmentation highlights the perennial preference for durable, aesthetically pleasing woods (both solid and engineered) but also tracks the rising adoption of materials like tempered glass and lightweight metals for modern, industrial designs. Analyzing distribution channels reveals the profound impact of online retail, which has democratized access to customized furniture, contrasting with traditional brick-and-mortar stores that maintain significance for high-value, inspect-before-purchase items. This segmentation framework allows market players to tailor manufacturing capacities and marketing strategies to specific, high-potential consumer niches, maximizing return on investment across the varied market landscape.

The value chain for the Entertainment Centres and Media Cabinets market starts with upstream analysis, focusing heavily on raw material procurement, primarily wood, metal, and glass components. Critical upstream activities involve sustainable logging practices, sourcing certified engineered wood products (like MDF and particleboard), and the acquisition of specialized hardware such as hinges, drawer slides, and lighting components. Manufacturers must ensure reliable, cost-effective, and ethically sourced material supplies to maintain both competitive pricing and brand reputation, particularly regarding certifications like the Forest Stewardship Council (FSC). Efficiency in this phase directly impacts manufacturing costs and the final product's quality perception, requiring strong, long-term relationships with material suppliers and adherence to fluctuating commodity prices, which often dictate quarterly pricing adjustments in the retail segment.

The manufacturing phase involves design, cutting, assembly, finishing (e.g., veneers, painting, lamination), and quality control. Advances in automated woodworking machinery and computer numerical control (CNC) technology have streamlined production, enabling high volumes of precision-cut components necessary for modular designs and complex assemblies. Downstream analysis focuses on distribution and retail. The distribution channel is segmented into direct and indirect routes. Direct sales occur through branded showrooms or proprietary e-commerce platforms, offering higher margins and direct consumer feedback loops. Indirect sales, which dominate the mass market, utilize third-party distributors, large furniture retailers, and expansive e-commerce marketplaces like Wayfair and Amazon, providing wider geographical reach but necessitating higher marketing expenditure and commission payments. Logistics complexity is significant due to the size and weight of assembled or flat-packed furniture items.

Effective channel management is paramount, with the recent shift favoring online platforms demanding robust digital catalogs, optimized logistics for large-item delivery, and sophisticated returns management systems. Specialty furniture stores remain vital for consumers requiring professional consultation, custom designs, and high-touch customer service for premium, high-value purchases. For commodity segments, the focus remains on optimizing packaging for flat-pack assembly (Ready-to-Assemble or RTA), minimizing shipping damage, and reducing last-mile delivery costs. Successful market participants strategically balance investment across these channels, ensuring that high-margin bespoke offerings are supported by direct channels, while standardized products leverage the efficiency and scale of major online and physical retail partners, ultimately maximizing market exposure and operational efficiency.

Potential customers for Entertainment Centres and Media Cabinets are broadly segmented into residential consumers undergoing home renovation or moving into new properties, and commercial entities seeking integrated media solutions for public or employee-facing spaces. Within the residential sector, two primary buyer profiles exist: the value-conscious consumer focused on functional storage and competitive pricing, typically purchasing engineered wood RTA units through online marketplaces or big-box retailers, and the affluent consumer focused on design integration, premium materials (solid wood, custom finishes), and durability, often purchasing bespoke or designer units through specialty furniture stores. The increasing prevalence of home offices and dedicated media rooms (e.g., home theaters) has further widened the customer base, specifically driving demand for sound-optimized and aesthetically integrated solutions that match high-end AV equipment investments.

Commercial end-users, primarily luxury hotels, corporate offices, and institutional settings, represent a high-value, cyclical procurement segment. These buyers prioritize durability, commercial-grade finishes that withstand heavy use, and integrated technology infrastructure necessary for conferencing and digital signage. Hotel chains, for instance, often require standardized, high-quality media consoles that blend seamlessly with interior design themes across hundreds of rooms. Architects and interior designers frequently act as crucial intermediaries, specifying particular cabinet designs and material standards for large-scale commercial or high-end residential projects. Targeting these professional intermediaries through specialized product specifications and wholesale partnership programs is vital for sustained growth in the B2B segment, requiring manufacturers to maintain strict quality control and offer substantial warranties to meet commercial longevity requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 17.0 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | IKEA, Ashley Furniture Industries, Wayfair Inc., Bassett Furniture Industries, Sauder Woodworking, Hooker Furniture Corporation, Universal Furniture, Restoration Hardware (RH), Crate & Barrel, Williams-Sonoma (Pottery Barn), Pulaski Furniture, Flexsteel Industries, Natuzzi Italia, La-Z-Boy Incorporated, Stickley Furniture, Herman Miller, Steelcase, Bush Industries, Dorel Industries, Ethan Allen Interiors. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape within the Entertainment Centres and Media Cabinets Market is rapidly shifting from purely static, functional storage to dynamic, integrated furniture ecosystems. Key technological advancements revolve around miniaturization, material innovation, and electronic integration aimed at enhancing user convenience and aesthetic appeal. Wireless charging technology, particularly Qi standards, is increasingly being embedded into cabinet surfaces, allowing users to charge devices seamlessly without visible cables. Furthermore, sophisticated LED lighting systems (RGB and white spectrum) that can be controlled via smartphone apps or synchronized with ambient screen content are becoming standard features in mid-to-high-end units, transforming the atmosphere of the entertainment area. The adoption of advanced, integrated cable management systems, which include hidden power strips and ventilated compartments, is also critical for accommodating the growing number of consumer electronics while maintaining a clutter-free appearance, addressing a major pain point for consumers setting up complex home theaters.

Material science and manufacturing technology play a vital role in enabling complex, yet durable, designs. The use of highly durable, scratch-resistant laminates and eco-friendly engineered wood panels (low-VOC emission standards) is driving the mass market segment, meeting both longevity and sustainability expectations. On the production side, the pervasive use of Computer Numerical Control (CNC) cutting machines ensures extremely precise component production, crucial for RTA furniture where easy and accurate assembly by the consumer is paramount. Moreover, manufacturers are exploring the use of specialized acoustically transparent materials—such as perforated metal or fabric-covered panels—to conceal speakers and subwoofers within the cabinet structure without diminishing sound quality, a highly desirable feature for minimalist home design enthusiasts aiming for a clean visual presence.

The most transformative technologies pertain to smart integration and connectivity. Cabinets are evolving to become centralized hubs utilizing technologies such as Zigbee or Z-Wave protocols to communicate with other smart devices in the home. This includes sensors monitoring temperature and humidity within enclosed compartments to protect sensitive electronics, and motorized mechanisms for automated opening and closing of doors or lifting mechanisms for hidden TVs. The ability to integrate voice control capabilities through discreetly housed microphones and connectivity modules ensures that the media cabinet remains future-proofed against evolving smart home standards. Manufacturers leveraging these integrated technologies effectively gain a significant competitive edge by offering a complete, intelligent furniture solution rather than just a storage unit, aligning with the broader trend toward unified smart living environments.

The market is primarily driven by the increasing global demand for large-screen smart televisions (4K and 8K), the proliferation of streaming media content requiring enhanced viewing environments, and rising consumer spending on smart home integration and aesthetic home interior upgrades, favoring modular and technologically integrated furniture.

While wall-mounting reduces demand for traditional, bulky entertainment centers, it simultaneously fuels demand for specialized, low-profile media consoles and floating cabinets. These new designs provide necessary concealed storage for peripheral devices (soundbars, gaming consoles, receivers) and vital cable management while maintaining a minimalist aesthetic.

The Engineered Wood segment (including MDF and particleboard with laminates) holds the largest volume share due to its cost-effectiveness, versatility in design, and widespread use in Ready-to-Assemble (RTA) furniture, catering specifically to the mass market and younger, price-sensitive consumers.

E-commerce is a critical distribution channel, enabling manufacturers to offer extensive product customization and direct-to-consumer sales, bypassing traditional retail markups. Specialized online furniture retailers utilize advanced visualization tools and optimized logistics for large, flat-packed items, driving rapid growth in this distribution segment globally.

Smart media cabinets are defined by integrated features such as wireless charging pads, app-controlled ambient LED lighting systems, automated climate control (ventilation) for electronic protection, and seamless internal routing systems for comprehensive cable and power management that connects devices to a centralized hub.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.