ID : MRU_ 434042 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

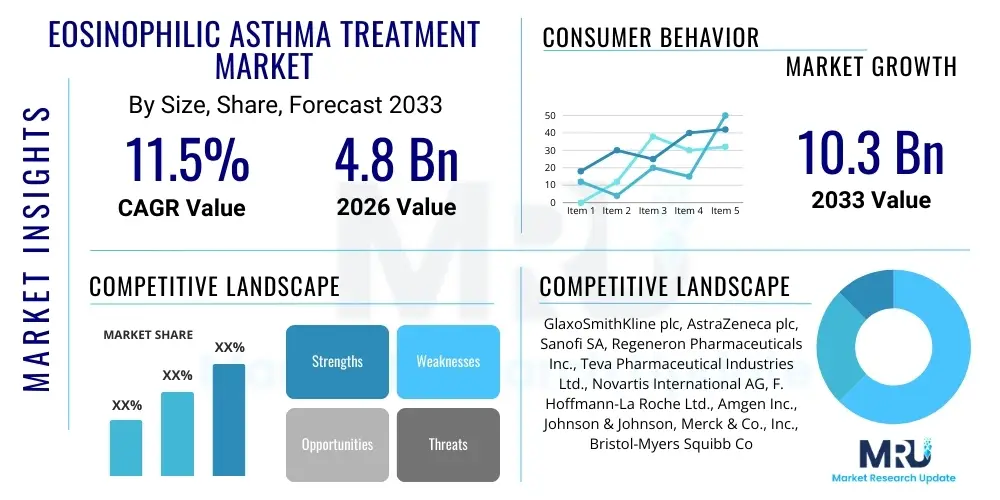

The Eosinophilic Asthma Treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 10.3 Billion by the end of the forecast period in 2033.

The Eosinophilic Asthma Treatment market primarily addresses a distinct and severe phenotype of asthma characterized by elevated blood and sputum eosinophil counts, which drive airway inflammation and hyperresponsiveness. Treatment strategies have significantly evolved beyond traditional inhaled corticosteroids (ICS) and long-acting beta-agonists (LABA), focusing increasingly on targeted biologic therapies designed to modulate the underlying inflammatory pathways. These therapies, particularly monoclonal antibodies targeting Interleukin-5 (IL-5), its receptor (IL-5R), or Interleukin-4/13 (IL-4/13), represent the core innovation driving market expansion, offering substantial clinical benefits for patients refractory to conventional high-dose treatments.

The introduction of novel biologics has fundamentally transformed the therapeutic landscape, shifting management towards a personalized medicine approach based on identified biomarkers. Key marketed products are designed to neutralize inflammatory cytokines, thereby reducing eosinophil levels, decreasing exacerbation rates, and improving overall lung function. Major applications of these treatments are centered on reducing the systemic burden of severe eosinophilic inflammation in adults and increasingly, in pediatric populations, where the disease presents significant quality of life and mortality risks.

Market growth is robustly supported by several key factors, including rising global prevalence of severe asthma, enhanced diagnostic capabilities (allowing for precise phenotyping), and growing awareness among healthcare providers regarding the efficacy and safety profile of targeted biologics. Furthermore, substantial investment in research and development aimed at discovering next-generation therapies and improving drug delivery methods ensures a dynamic and competitive environment, promising sustained innovation throughout the forecast period.

The Eosinophilic Asthma Treatment market is undergoing rapid transformation, dominated by the commercial success and expanding indications of monoclonal antibodies, which constitute the primary business trend. These biologics command premium pricing, yet their adoption is accelerating globally due to compelling efficacy data demonstrating reduced hospitalizations and improved patient outcomes. Key business strategies currently revolve around expanding geographic reach, particularly into emerging Asian markets, and securing favorable reimbursement policies across highly regulated healthcare systems like North America and Europe, alongside continuous investment in subcutaneous self-administration options to enhance patient adherence and convenience.

Regionally, North America maintains the largest market share, driven by high disease prevalence, advanced diagnostic infrastructure, and rapid uptake of innovative therapies supported by robust reimbursement frameworks. Europe follows, characterized by stringent regulatory pathways but high governmental focus on rare disease management and favorable pricing negotiations. The Asia Pacific region is poised for the highest growth rate, fueled by improving healthcare access, increasing disposable income, and rising awareness, though market penetration is currently challenging due to varied regulatory approval timelines and often fragmented healthcare delivery systems.

Segment trends emphasize the dominance of the Biologics class, specifically IL-5 inhibitors, which remain the foundation of targeted therapy. However, dual inhibitors (IL-4/13) are gaining significant traction, broadening the scope of treatable phenotypes. From an operational standpoint, the subcutaneous route of administration is increasingly preferred over intravenous infusion, promoting shifts in distribution channels from specialized infusion centers towards retail and specialty pharmacies, reflecting a trend towards decentralized patient care models and better management of chronic conditions.

User inquiries regarding the impact of Artificial Intelligence (AI) in the Eosinophilic Asthma Treatment market frequently center on three critical areas: enhanced precision diagnostics through biomarker identification, optimization of personalized treatment regimens, and acceleration of drug discovery pipelines. Users are keen to understand how machine learning models can sift through complex 'omics' data (genomics, proteomics, metabolomics) to identify novel, subtle biomarkers that accurately predict a patient's response to specific biologic agents, thereby minimizing the current trial-and-error approach inherent in severe asthma management. There is also significant anticipation concerning AI's role in optimizing clinical workflow, predicting exacerbation risk, and supporting dosage adjustments for existing treatments.

AI algorithms are fundamentally changing the early-stage drug development process by allowing pharmaceutical companies to rapidly screen vast molecular libraries and predict the efficacy and toxicity profiles of potential new drug targets for eosinophilic inflammation. This capacity for high-throughput computational modeling significantly reduces the time and cost associated with identifying novel therapeutic antibodies or small molecules, ultimately addressing currently underserved patient populations who may not respond optimally to available IL-5 or IL-4/13 inhibitors. Furthermore, AI is crucial in designing more efficient and inclusive clinical trials by selecting the most suitable patient cohort based on multi-dimensional patient data, thereby increasing the probability of trial success and speeding up market access for innovative treatments.

In the clinical setting, AI is enabling true personalized medicine by integrating Electronic Health Record (EHR) data, wearable device data, and specific biomarker results (like fractional exhaled nitric oxide (FeNO) levels or blood eosinophil counts) to build predictive models. These models provide clinicians with actionable insights into which biologic agent will offer the maximum benefit for an individual patient, moving beyond static threshold-based prescribing to dynamic, risk-stratified treatment plans. This refinement in patient selection not only improves clinical outcomes but also enhances cost-effectiveness for healthcare systems managing expensive biologic therapies, directly addressing user concerns about optimizing treatment selection and resource utilization.

The Eosinophilic Asthma Treatment market is primarily driven by the clinical success and expanding patient base eligible for targeted biologic therapies, offering a superior efficacy profile compared to standard care in severe, refractory cases. However, market expansion is significantly restrained by the extraordinarily high cost of these monoclonal antibodies and the resulting reimbursement challenges, particularly in developing economies or healthcare systems facing budget constraints. Opportunities for growth are heavily vested in the development of novel targets beyond the IL-5 pathway, the anticipated emergence of biosimilars offering cost-competitive alternatives, and geographical expansion into vast, underserved patient populations across Asia Pacific and Latin America, collectively shaping a high-impact, yet challenging, commercial landscape.

The Eosinophilic Asthma Treatment market is meticulously segmented based on Drug Class, Route of Administration, and Distribution Channel, reflecting the diverse approaches to managing this complex condition and the structural requirements for biologic delivery. Segmentation by Drug Class is the most critical, defining the competitive landscape where IL-5/IL-5R inhibitors currently hold the largest share, but face increasing competition from broader-spectrum agents like IL-4/IL-13 antagonists, which target multiple inflammatory pathways. Analyzing these segments is crucial for stakeholders to understand shifting prescribing patterns and invest strategically in either enhancing existing class dominance or developing innovative drugs that address treatment gaps not covered by current market leaders.

The segmentation by Route of Administration highlights the ongoing shift in patient care convenience and compliance. Historically, treatments required intravenous (IV) infusion, demanding administration in specialized clinical settings. However, the commercial success of biologics formulated for subcutaneous (SC) injection has significantly altered this dynamic, permitting self-administration or administration in less resource-intensive outpatient settings. This transition is not merely a logistical change but represents a profound opportunity to enhance patient quality of life and adherence, which is vital for long-term management of severe chronic diseases. The preference for SC administration is expected to grow rapidly, pushing the market towards decentralized care models.

Furthermore, segmentation across Distribution Channels reveals the specialized requirements inherent in handling expensive, temperature-sensitive biologic drugs. The channel structure includes hospital pharmacies, retail pharmacies, and specialized mail-order or specialty pharmacies, the latter being indispensable for managing the complex insurance verification and patient support programs associated with high-cost therapies. Trends show increasing reliance on specialty pharmacies due to their capability to manage intricate logistics, provide critical patient education, and ensure continuity of care, solidifying their role as essential gatekeepers in the effective delivery of eosinophilic asthma treatments.

The value chain for the Eosinophilic Asthma Treatment market is characterized by intense, capital-intensive research and development (R&D) activities focused on identifying specific inflammatory biomarkers and engineering highly targeted monoclonal antibodies. The upstream segment is dominated by large pharmaceutical and biotechnology firms investing heavily in genomics, proteomics, and advanced cell culture techniques required for large-scale biologic manufacturing. Unlike small-molecule drugs, the production phase requires complex, highly regulated bioprocessing facilities to ensure product purity, consistency, and stability, creating high barriers to entry and concentrating manufacturing capabilities among a few key players globally.

Moving downstream, the distribution channel is highly specialized, primarily relying on indirect methods through specialty pharmacies due to the high cost, specific storage requirements (cold chain logistics), and need for specialized patient services (insurance verification, adherence programs). Direct distribution is rare, typically limited to samples or specific hospital settings. The complexity of the logistics mandates a robust, highly compliant supply chain to maintain drug integrity from the manufacturing site to the patient. Effective distribution hinges on strong partnerships between manufacturers, third-party logistics (3PL) providers, and specialty pharmacy networks, ensuring the safe and timely delivery of these life-saving therapies.

The final stage involves healthcare providers (pulmonologists, allergists) prescribing the treatment and administering or training the patient for self-injection, supported by sophisticated patient support programs provided by the manufacturers. Regulatory compliance and pharmacovigilance are integrated throughout the chain, particularly crucial given the nature of biologic therapies. The high value added at the R&D and manufacturing stages underscores the premium pricing structure, while the specialized distribution channel ensures controlled access and proper patient management, forming a tightly controlled and highly profitable value chain.

The primary customers and end-users of Eosinophilic Asthma treatments are patients diagnosed with severe, uncontrolled eosinophilic asthma, typically defined by frequent exacerbations, persistent symptoms despite high-dose inhaled therapy, and elevated blood eosinophil counts. The purchasing decision, however, is significantly influenced by specialized healthcare providers, primarily board-certified pulmonologists and allergy/immunology specialists who possess the expertise to accurately phenotype severe asthma and determine eligibility for targeted biologic therapies. These specialists act as the gatekeepers for prescribing, requiring detailed education and clinical data to adopt new treatments into their practice algorithms, focusing on therapies that demonstrate strong efficacy in reducing oral corticosteroid dependency and improving lung function.

Institutional customers, including specialized hospital systems, infusion centers, and large accountable care organizations (ACOs), also represent a major segment of the potential customer base. These institutions manage large volumes of severe asthma patients and are responsible for procuring, storing, and sometimes administering the IV-formulated biologic treatments. Their purchasing decisions are heavily influenced by formulary inclusion, overall cost-effectiveness assessments (considering reduced hospitalizations), and integration into their managed care protocols. They prioritize treatments that align with clinical guidelines and offer robust data supporting long-term safety and efficacy.

A crucial secondary customer segment includes payers—government health insurance programs (like Medicare/Medicaid in the US), private insurance companies, and managed care organizations. While not the end-users of the product, their formulary coverage decisions dictate patient access and the ultimate commercial success of any eosinophilic asthma treatment. Manufacturers must demonstrate superior pharmacoeconomic value to these payers, proving that the high acquisition cost is offset by significant savings from avoiding emergency room visits, intensive care stays, and chronic use of oral corticosteroids, positioning the treatment as a cost-effective strategy for managing a complex, high-burden disease.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 10.3 Billion |

| Growth Rate | CAGR 11.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | GlaxoSmithKline plc, AstraZeneca plc, Sanofi SA, Regeneron Pharmaceuticals Inc., Teva Pharmaceutical Industries Ltd., Novartis International AG, F. Hoffmann-La Roche Ltd., Amgen Inc., Johnson & Johnson, Merck & Co., Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, Celltrion Healthcare, Takeda Pharmaceutical Company Limited, Boehringer Ingelheim International GmbH, Pfizer Inc., Biogen Inc., Dr. Reddy's Laboratories Ltd., Coherus BioSciences, Inc., Sandoz International GmbH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological backbone of the Eosinophilic Asthma Treatment market is overwhelmingly dominated by the sophisticated biotechnology required for the production of monoclonal antibodies (MABs). These biologic agents represent a paradigm shift from broad-spectrum anti-inflammatory drugs, relying on advanced genetic engineering and cell line development to create antibodies that precisely target specific inflammatory mediators like IL-5, IL-5R, or IL-4/13. The complexity of these technologies includes stable cell culture systems, large-scale bioreactors, and intricate purification processes, all necessary to ensure therapeutic efficacy and minimize immunogenicity, thereby establishing biologics manufacturing as a high-tech specialization that dictates the competitive structure of the market.

Beyond the core product technology, significant innovation is focused on enhancing drug delivery systems and improving diagnostics. The shift towards self-administration relies on advancements in formulation science and device technology, specifically the development of user-friendly autoinjectors and pre-filled syringes that maintain the stability of the biologic molecule while enabling reliable, accurate subcutaneous dosing outside of a clinical setting. This focus on decentralized administration is crucial for market penetration and patient quality of life, requiring robust material science and human factors engineering to perfect the administration process.

Furthermore, diagnostic technologies are evolving rapidly to support personalized treatment. The utilization of high-throughput molecular diagnostics and flow cytometry for precise eosinophil count quantification, alongside non-invasive biomarkers like fractional exhaled nitric oxide (FeNO), enables clinicians to accurately phenotype the disease severity and inflammatory driver. Future technological landscapes are anticipated to integrate multi-omics technologies and AI-driven platforms to identify complex biomarker panels, moving beyond simple blood counts to predict responders and non-responders with greater certainty, enhancing therapeutic precision and overall market efficiency.

The primary treatments are monoclonal antibodies (biologics) targeting key inflammatory cytokines. These include Interleukin-5 (IL-5) inhibitors (e.g., mepolizumab), IL-5 receptor alpha (IL-5R) inhibitors (e.g., benralizumab), and Interleukin-4/13 (IL-4/13) inhibitors (e.g., dupilumab), which are utilized for severe, refractory cases.

The Eosinophilic Asthma Treatment Market is projected to exhibit a robust growth trajectory, expected to register a CAGR of 11.5% during the forecast period from 2026 to 2033, driven largely by the expanding use of high-efficacy biologic therapies.

North America holds the largest share of the global market. This dominance is attributed to high patient prevalence of severe asthma, favorable and rapid market access for innovative biologics, and strong financial support from advanced reimbursement and insurance systems.

Technology is facilitating a significant shift towards patient-centric care through the development of self-administered subcutaneous injections, utilizing autoinjector pen technologies. This innovation improves patient adherence, reduces reliance on clinical infusion centers, and enhances overall convenience for chronic management.

The most significant restraint is the high acquisition cost of monoclonal antibody therapies. This expense creates substantial reimbursement challenges and affordability issues, particularly in emerging and price-sensitive healthcare markets, leading to restricted patient access.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.