ID : MRU_ 432474 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

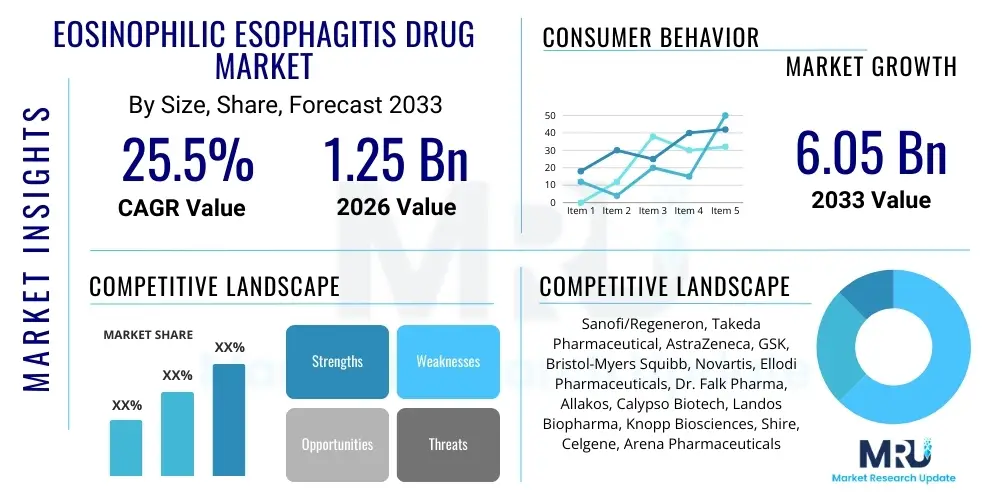

The Eosinophilic Esophagitis Drug Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2026 and 2033. The market is estimated at 1.25 Billion USD in 2026 and is projected to reach 6.05 Billion USD by the end of the forecast period in 2033.

The Eosinophilic Esophagitis (EoE) Drug Market is currently experiencing a profound transformation, moving rapidly from reliance on off-label therapies, such as proton pump inhibitors (PPIs) and swallowed topical corticosteroids, toward highly specific targeted treatments. Eosinophilic Esophagitis is a chronic, immune-mediated disorder characterized by eosinophil-predominant inflammation of the esophageal mucosa, leading to symptoms like dysphagia and food impaction. The recent commercialization of the first FDA-approved biologic therapy specifically for EoE, Dupixent (dupilumab), marks a critical inflection point, validating EoE as a distinct therapeutic category and encouraging substantial investment in pipeline development.

The primary applications of EoE drugs involve the reduction of esophageal inflammation and the mitigation of symptoms, thereby improving patient quality of life and preventing long-term complications such as esophageal strictures and fibrosis. Traditional treatment paradigms focused on symptom relief and dietary elimination, but the introduction of novel formulations of corticosteroids designed for esophageal adherence (e.g., budesonide oral suspension or effervescent tablets) and, crucially, biologics targeting Type 2 inflammation pathways (IL-4, IL-13, TSLP) are revolutionizing clinical practice. These products offer superior efficacy in achieving histologic remission, a key metric for disease control, which is driving substantial market expansion.

Driving factors for this robust market growth include the rising prevalence and improved diagnosis of EoE globally, increasing awareness among gastroenterologists and allergists, and a significant unmet need for effective, long-term maintenance therapies. Furthermore, the expiration of patents for some existing non-specific treatments and the strong pricing power associated with first-in-class biologic drugs contribute significantly to the escalating market valuation. Regulatory approvals incentivizing precision medicine approaches tailored to the underlying inflammatory etiology are accelerating the adoption rate of these advanced drug classes.

The Eosinophilic Esophagitis Drug Market is characterized by intense innovation and rapid commercialization, fundamentally shifting from a niche indication to a high-growth therapeutic area. Business trends underscore a substantial pivot toward specialty pharmacy distribution channels, driven by the complexity and high cost of newly approved biologic treatments. Pharmaceutical companies are heavily investing in long-term safety and efficacy studies to support label expansion and demonstrate disease-modifying capabilities, establishing strong competitive moats around their biologic portfolios. Mergers and acquisitions, particularly involving smaller biotech firms with promising Phase 2 and Phase 3 assets targeting specific inflammatory pathways, are common as major pharmaceutical players seek to dominate this lucrative segment. Furthermore, strategic collaborations are focused on developing user-friendly drug delivery systems, such as auto-injectors, to enhance patient compliance for chronic administration.

Regional trends indicate that North America, particularly the United States, holds the dominant market share due to high disease prevalence, advanced diagnostic capabilities, favorable reimbursement policies for specialty drugs, and the presence of leading research institutions and pharmaceutical headquarters. Europe is also a high-growth region, driven by increasing clinical guidelines advocating for targeted therapy and the subsequent market entry of approved formulations and biologics. The Asia Pacific region, while currently lagging in market size, is anticipated to register the fastest growth rate, fueled by improving healthcare infrastructure, rising disposable incomes, and increasing epidemiological data confirming EoE prevalence, particularly in industrialized nations.

Segment trends highlight the burgeoning importance of the Biologics segment, which is projected to surpass conventional corticosteroid and PPI therapies in revenue generation by the mid-forecast period. This segment’s growth is directly attributable to the high efficacy rates and premium pricing structure associated with targeted antibodies that interfere with Type 2 inflammation (e.g., IL-4/IL-13 antagonists). Within routes of administration, injectables are gaining traction for systemic therapies, while novel oral formulations (such as dissolvable tablets or viscous suspensions) designed to coat the esophagus remain critical for locally acting corticosteroid segments. The shift in treatment guidelines prioritizing histologic remission over symptomatic relief ensures that high-impact, targeted therapies will lead segment revenue growth throughout the forecast period.

Common user questions regarding AI's influence on the Eosinophilic Esophagitis drug market frequently center on three critical areas: Can AI accelerate the diagnostic process, particularly pathology review? How can AI enhance the efficiency and precision of new drug discovery for novel targets? And finally, what role will AI play in personalizing EoE treatment plans, predicting patient response, and optimizing dosing strategies? These inquiries reflect the medical community's expectation that AI and Machine Learning (ML) can overcome current challenges, such as the subjectivity inherent in manual eosinophil counting and the significant heterogeneity in patient response to existing therapies. Users anticipate that AI platforms will reduce the time from symptom onset to definitive diagnosis and enable pharmaceutical companies to identify and validate promising therapeutic molecules faster than traditional methods, thereby streamlining clinical trials and reducing the substantial R&D expenditure currently associated with drug development.

The application of Artificial Intelligence is poised to significantly impact the EoE drug market, primarily by revolutionizing diagnostic pathology. AI algorithms are being developed to analyze digital images of esophageal biopsies, offering automated and highly accurate eosinophil counting, reducing inter-observer variability, and expediting the histopathological confirmation required for diagnosis and monitoring. This efficiency gain directly supports the market by facilitating quicker patient identification for clinical trials and commercial treatment initiation. Furthermore, AI platforms can analyze vast genomic, proteomic, and transcriptomic datasets derived from EoE patients to uncover subtle disease endotypes that may respond differently to various drug classes, moving the field towards highly stratified clinical trials and targeted therapeutic selection.

In drug development, AI is instrumental in identifying novel inflammatory pathways beyond the established Type 2 immunity targets. Machine learning models are capable of predicting the safety and efficacy profiles of potential drug candidates before synthesis, optimizing molecular structure, and accelerating lead identification. For the marketed drugs segment, AI models analyzing real-world evidence (RWE) from electronic health records (EHRs) can monitor long-term treatment outcomes, detect rare adverse events, and establish predictive biomarkers for treatment non-response, informing clinicians on optimal therapy rotation or combination strategies, ultimately maximizing the utilization and clinical relevance of currently approved EoE drugs.

The Eosinophilic Esophagitis Drug Market is driven primarily by the paradigm shift from generalized symptom management to targeted, anti-inflammatory biologic therapies, fueled by increasing physician and patient awareness and robust clinical data validating the long-term benefits of achieving histologic remission. However, market growth faces significant restraints, chiefly related to the extremely high cost of specialty biologic treatments and persistent challenges in early, accurate diagnosis, as symptoms often overlap with other gastrointestinal disorders like GERD. Opportunities for explosive market expansion lie in the successful development and launch of next-generation oral small molecules and specific biologics targeting alternative inflammatory cytokines (e.g., IL-15, IL-5), offering improved convenience and expanding the pool of patients who may not respond adequately to current therapies. These dynamics create a powerful impact force matrix where the necessity of disease modification clashes with accessibility barriers, compelling manufacturers to focus on demonstrating superior value and securing favorable reimbursement policies.

Key drivers include the substantial investment in R&D by major pharmaceutical companies focusing on the EoE indication, spurred by the success of the first approved biologic. The growing clinical consensus that prolonged, uncontrolled EoE leads to irreversible fibrosis and stricture formation necessitates effective maintenance therapy, expanding the target population receiving chronic treatment. Furthermore, improvements in upper endoscopy techniques and the increasing implementation of standardized diagnostic protocols contribute to a more accurately estimated patient population. These factors create a high demand environment, allowing premium pricing for truly innovative treatments that offer superior disease control and potentially reduce the need for repeat endoscopies and dilations.

Restraints impeding faster growth include market access hurdles due to the high cost of biologic drugs, often leading to restricted coverage or complex prior authorization requirements, especially in managed care systems. Another significant restraint is the continued use of compounded or extemporaneously prepared topical corticosteroids due to lower cost, despite the availability of FDA-approved alternatives. The market also faces the fundamental restraint of patient heterogeneity; not all patients respond optimally to anti-IL-4/IL-13 therapies, necessitating ongoing research into non-responders and contributing to clinical development complexity and cost. Opportunities are concentrated in developing orally available therapies that target novel mechanisms and offer a lower administrative burden compared to injectables, broadening patient acceptance and compliance. The expansion of clinical trials into pediatric populations, where EoE prevalence is substantial and the need for safe long-term therapies is paramount, also represents a major untapped opportunity.

The Eosinophilic Esophagitis Drug Market is comprehensively segmented based on Drug Class, Route of Administration, and Distribution Channel. This segmentation is essential for understanding the underlying competitive dynamics and technological shifts within the therapeutic landscape. The market structure is heavily influenced by the recent transition from generic, off-label treatments to highly specialized branded pharmaceuticals. The Drug Class segmentation highlights the shift in clinical preference towards targeted biologics, which offer superior efficacy and specificity compared to traditional anti-inflammatory agents. Understanding these segments allows market stakeholders to tailor their commercial strategies, focusing on educational initiatives for specific patient administration routes (e.g., self-injection versus hospital-administered) and optimizing supply chain logistics through targeted distribution channels.

The segmentation by Route of Administration (Oral vs. Injectable) reflects the ongoing trade-offs between systemic efficacy and localized action. Oral routes dominate the corticosteroid segment, prioritizing localized delivery to the esophageal tissue (e.g., viscous suspensions designed to minimize systemic absorption), which is vital for reducing potential side effects associated with chronic steroid use. Conversely, biologics primarily utilize the injectable route (subcutaneous), offering systemic control of Type 2 inflammation, thereby addressing the root cause of the disease. Future market growth will depend significantly on the development of orally bioavailable small molecules that can replicate the systemic efficacy of biologics while offering the patient convenience associated with oral ingestion, potentially disrupting the current dominance of injectable biologics in the high-value segment.

Analysis of the Distribution Channel segmentation reveals the strong influence of specialty pharmacy networks. Given the high cost, specific storage requirements (cold chain management), and complex patient support needs (e.g., patient adherence programs, prior authorization assistance) associated with biologic therapies, the distribution is tightly controlled. While hospital pharmacies remain crucial for initial dosing and patient training, the vast majority of ongoing biologic prescriptions are fulfilled by specialty pharmacies that manage end-to-end patient care services. Retail and online pharmacies primarily cater to the distribution of standard oral therapies (PPIs and older corticosteroids), but their role in the overall market value is diminishing as the treatment paradigm shifts toward high-value specialty drugs.

The value chain for the Eosinophilic Esophagitis drug market starts with intense upstream activities focused on drug discovery and preclinical research, where substantial investments are made in identifying and validating novel inflammatory targets, such as specific interleukins and thymic stromal lymphopoietin (TSLP). This stage involves high technical risk and requires expertise in immunology, personalized medicine, and large-scale genetic screening. The subsequent manufacturing phase, particularly for complex biologic drugs, requires highly specialized facilities compliant with stringent global regulatory standards (cGMP) for cell culture, purification, and sterile filling. The high barriers to entry and intellectual property protection at this stage secure substantial profits for originators. The complexity of formulation for esophageal delivery, such as creating muco-adherent corticosteroid suspensions or dissolvable oral tablets, adds a unique step to the manufacturing process, ensuring the active pharmaceutical ingredient remains localized.

The midstream elements focus on clinical development, regulatory approval, and marketing, which are critical for market success. Due to the chronic nature of EoE and the need to demonstrate long-term safety and histological efficacy, clinical trials are often long, resource-intensive, and involve multiple centers globally. Distribution channels for EoE drugs are bifurcated: generic PPIs and standard corticosteroids follow traditional large-scale pharmaceutical distribution models, while the high-value biologics utilize controlled, cold-chain logistics managed primarily by specialized third-party logistics providers (3PLs) and specialty pharmacies. Direct channels are becoming increasingly important as manufacturers offer patient assistance programs (PAPs) and directly manage patient enrollment and compliance monitoring.

Downstream activities center on patient prescription, reimbursement management, and administration. The end-users—patients, gastroenterologists, and allergists—rely heavily on detailed educational materials provided by the manufacturers and specialty pharmacies regarding proper administration techniques (especially for self-injectable biologics or swallowed suspensions). The reimbursement landscape involves complex negotiations between manufacturers, payers, and pharmacy benefit managers (PBMs) to ensure patient access, often influencing drug choice. Success in the downstream segment is highly dependent on effective market access strategies and patient adherence programs that mitigate the financial burden and complexity of chronic specialty therapy, solidifying product uptake and long-term revenue streams.

The primary customers in the Eosinophilic Esophagitis Drug Market are patients diagnosed with active EoE who require therapeutic intervention to manage their symptoms, reduce esophageal inflammation, and prevent long-term complications. These patients span all age groups, including a significant pediatric population, necessitating drugs tailored for safe, long-term use in children. Secondary customers include healthcare providers, specifically gastroenterologists and allergists, who act as gatekeepers for prescriptions, basing their decisions on clinical guidelines, efficacy data, safety profiles, and patient insurance coverage. Furthermore, institutional purchasers such as hospitals, specialized clinics, and Ambulatory Surgical Centers (ASCs) purchase drugs for in-house administration, particularly for initial loading doses of infused or supervised injectable therapies. The purchasing power of government agencies and private payers (insurance companies and PBMs) is paramount, as their formulary decisions dictate which drugs are accessible and affordable to the vast majority of patients.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.25 Billion USD |

| Market Forecast in 2033 | $6.05 Billion USD |

| Growth Rate | CAGR 25.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sanofi/Regeneron, Takeda Pharmaceutical, AstraZeneca, GSK, Bristol-Myers Squibb, Novartis, Ellodi Pharmaceuticals, Dr. Falk Pharma, Allakos, Calypso Biotech, Landos Biopharma, Knopp Biosciences, Shire, Celgene, Arena Pharmaceuticals |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Eosinophilic Esophagitis Drug market is primarily defined by advanced pharmaceutical development focusing on precision therapeutics and optimized drug delivery systems. The most critical technological advancements reside in the Biologics segment, specifically the development and scaling of monoclonal antibodies engineered to neutralize key inflammatory mediators (cytokines) such as Interleukin-4, Interleukin-13, and TSLP, which drive the Type 2 inflammatory response characteristic of EoE. Manufacturing technologies supporting these biologics require highly complex cell line development, fermentation, purification chromatography, and stringent quality control systems to ensure product consistency and efficacy. Furthermore, formulation technology is crucial for maintaining the stability and long shelf life of these protein-based drugs, particularly within cold chain logistics.

In parallel, significant technological innovation is directed towards improving localized drug delivery for topically acting agents. This involves formulation science aimed at maximizing drug residence time within the esophagus while minimizing systemic absorption. Key technologies include the development of muco-adhesive suspensions, effervescent tablet technologies that dissolve slowly to create a viscous coat, and microparticle encapsulation techniques. These delivery systems ensure the corticosteroid or small molecule drug reaches and remains on the inflamed mucosal surface, enhancing therapeutic index and minimizing undesirable systemic side effects, thereby offering a crucial technological advantage over legacy swallowed steroid inhaler formulations.

Future technology advancements are concentrating on pharmacogenomics and biomarker identification to guide personalized treatment. High-throughput sequencing and advanced bioinformatics tools are being utilized to correlate patient genetic profiles and peripheral blood eosinophil counts with treatment response, aiming to develop companion diagnostics. Furthermore, the integration of digital health platforms and connected devices (such as smart injection pens or adherence monitoring apps) represents a growing technological focus, intending to support patient compliance with chronic therapy and facilitate real-time monitoring of symptoms and side effects, ultimately improving patient outcomes and generating valuable real-world data for post-marketing studies.

The primary growth drivers are the recent regulatory approval of targeted biologic therapies, such as dupilumab, the increasing global prevalence and improved diagnosis of EoE, and a recognized need for effective, long-term treatments that achieve histologic remission and prevent esophageal remodeling (fibrosis and strictures).

The Biologics drug class, specifically monoclonal antibodies targeting Type 2 inflammation pathways (IL-4/IL-13), currently generates the highest revenue due to their premium pricing structure, strong clinical efficacy in achieving histological remission, and addressing the significant unmet need for specialty treatments.

The treatment paradigm is shifting from generalized, often off-label use of high-dose PPIs and extemporaneous swallowed topical corticosteroids toward disease-specific, targeted therapies, including specially formulated oral corticosteroids and high-value injectable biologics, focusing on sustained reduction of eosinophil counts in the esophagus.

High drug costs and complex reimbursement hurdles are the primary regional challenges, particularly in Europe and Latin America, where price negotiations and fragmented healthcare systems often delay patient access to expensive, yet effective, biologic and specialty corticosteroid formulations, leading to continued reliance on cheaper, less specific treatments.

AI is essential for accelerating diagnosis by automating the quantitative analysis of eosinophils in esophageal biopsies, improving standardization. In treatment, AI analyzes large datasets to predict patient responsiveness to specific therapies and assists in discovering novel therapeutic targets beyond established Type 2 inflammation pathways.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.