ID : MRU_ 436310 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

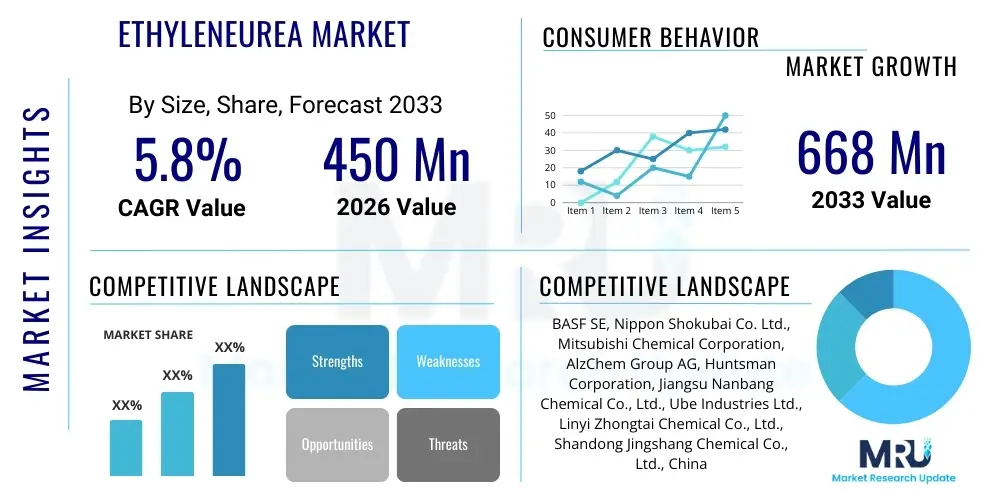

The Ethyleneurea Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 668 Million by the end of the forecast period in 2033.

The Ethyleneurea market encompasses the production, distribution, and utilization of 2-Imidazolidinone, a cyclic urea compound derived primarily from the reaction of ethylenediamine and carbon dioxide or urea. This versatile chemical compound serves as a critical intermediate in various industrial processes, most notably in the production of formaldehyde-based resins like urea-formaldehyde (UF) resins, melamine-formaldehyde (MF) resins, and specialized durable press (DP) textile finishing agents. Ethyleneurea enhances the stability, performance, and durability of these final products, making it indispensable in sectors requiring high-performance cross-linking agents and adhesion promoters.

Major applications of Ethyleneurea span across the textile industry, where it is used to impart wrinkle resistance and shrinkage control to fabrics, the construction sector as a key ingredient in cement additives and concrete admixtures, and the agricultural sector for manufacturing controlled-release fertilizers and pesticides. Furthermore, its unique molecular structure makes it a vital precursor in the pharmaceutical industry for synthesizing various heterocyclic drugs and compounds. The robust demand from the booming construction and textile sectors, particularly in Asia Pacific, coupled with the increasing adoption of slow-release nitrogen fertilizers, are primary factors propelling market expansion.

Key benefits derived from using Ethyleneurea include improved performance characteristics in polymers, enhanced product stability, and reduced environmental impact compared to some alternative chemical precursors. The driving factors for market growth involve technological advancements in textile finishing processes favoring eco-friendly and durable treatments, expanding infrastructure development globally, necessitating high-quality concrete admixtures, and stringent regulations encouraging the shift towards more efficient and less environmentally detrimental agricultural inputs. Its role in synthesizing high-purity chemical reagents further solidifies its position as a foundational commodity chemical.

The global Ethyleneurea market is characterized by moderate growth, primarily driven by robust demand from the construction and textile industries, particularly within emerging economies. Business trends indicate a focus on process optimization and the development of higher-purity grades of Ethyleneurea to meet the stringent requirements of the pharmaceutical and specialty chemical sectors. Key manufacturers are investing in backward integration to secure raw material supplies (ethylenediamine and carbon sources) and focusing on geographical expansion, especially targeting high-growth regions like China and India, which are major consumption hubs for textiles and construction materials. Strategic collaborations aimed at developing novel applications, such as specialized coatings and high-performance cement additives, are shaping competitive dynamics.

Regional trends reveal Asia Pacific (APAC) as the dominant and fastest-growing market, attributing its supremacy to massive urbanization projects, significant textile manufacturing capabilities, and widespread agricultural activities demanding urea-based slow-release fertilizers. North America and Europe demonstrate mature markets, emphasizing innovation in sustainable textile finishing and high-value niche applications, such as cosmetics and specialized polymers, driven by stringent environmental and safety regulations. The Middle East and Africa (MEA) are emerging due to increasing construction investments and the growth of local chemical processing industries, although market penetration remains relatively lower compared to established regions.

Segmentation trends highlight the dominance of the textile finishing application segment, driven by the persistent global demand for durable press (DP) fabrics. However, the agrochemicals segment is expected to exhibit the fastest growth, propelled by the urgent need for enhanced nitrogen use efficiency (NUE) in farming practices, utilizing Ethyleneurea as a stabilizer in controlled-release fertilizers (CRFs). Based on grade, the technical grade segment accounts for the largest volume due to bulk usage in resins and textiles, while the high-purity grade segment is expanding rapidly due to increasing demand from the pharmaceutical and electronic chemical industries, demanding higher margins and stricter quality control.

Common user questions regarding AI's impact on the Ethyleneurea market predominantly center on optimizing manufacturing efficiency, improving quality control, predicting demand fluctuations for key derivatives, and enabling R&D for novel Ethyleneurea-based polymers or compounds. Users are concerned about how machine learning can analyze complex reaction parameters (temperature, pressure, catalyst concentration) in the synthesis process to minimize waste and energy consumption. Furthermore, there is significant interest in utilizing predictive analytics to forecast the volatile demands of end-use industries—such as textile production cycles or major infrastructure project timelines—to optimize inventory management and reduce supply chain risks for bulk chemical producers. The consensus indicates an expectation that AI will primarily function as an efficiency driver in production and supply chain logistics rather than fundamentally changing the chemical properties or applications of Ethyleneurea itself.

The Ethyleneurea market is governed by a dynamic interplay of factors encapsulated by Drivers, Restraints, and Opportunities (DRO). The primary drivers stem from the global surge in infrastructure spending and construction activities, requiring advanced concrete admixtures and durable coatings, alongside sustained demand for high-quality, wrinkle-free, and dimensionally stable textiles. Technological advances in textile finishing treatments, emphasizing environmentally sustainable and formaldehyde-free processes, significantly boost the demand for Ethyleneurea derivatives like dimethylol ethylene urea (DMEU) and other advanced cross-linking agents. Furthermore, the imperative to increase crop yields while minimizing environmental nitrogen run-off fuels the market for controlled-release fertilizers that utilize Ethyleneurea as a slow-release mechanism, particularly in large agricultural economies.

However, the market faces significant restraints, including the volatility in the prices of key raw materials, primarily ethylenediamine and urea, which are petrochemical derivatives, subjecting production costs to global crude oil price fluctuations. Regulatory scrutiny regarding chemical manufacturing processes and end-product safety, particularly in developed regions like Europe, imposes high compliance costs on manufacturers. Additionally, the availability of alternative textile cross-linking agents, though sometimes less effective, presents competitive pressure. The potential long-term substitution of conventional urea-formaldehyde resins in certain low-value applications by cheaper, less performance-oriented alternatives also acts as a ceiling to overall volume growth in bulk segments.

Opportunities for growth are concentrated in the development of specialty and high-purity Ethyleneurea grades specifically tailored for the burgeoning pharmaceutical, cosmetic, and electronics industries, which command premium pricing and require rigorous quality standards. Geographic expansion into underdeveloped markets in Africa and Latin America, where construction and textile industries are starting to scale up, represents untapped potential. Furthermore, continuous innovation focused on synthesizing biodegradable Ethyleneurea derivatives or incorporating bio-based feedstocks into the manufacturing process would align with global sustainability trends, potentially opening new markets and enhancing the product's environmental profile, thereby mitigating regulatory restraints.

The impact forces within the market are predominantly driven by competitive intensity among a few major producers who control the manufacturing technology and capacity. The increasing bargaining power of key buyers, particularly large textile conglomerates and fertilizer manufacturers, forces price competition in the commodity segments. Technological substitution risk is moderate but constantly monitored, especially concerning sustainable alternatives in textile finishing. Regulatory compliance acts as a significant external force, often raising barriers to entry for new players and dictating the acceptable specifications and purity levels for various applications, especially in food contact materials or pharmaceuticals, thereby heavily influencing market dynamics and product differentiation strategies.

The Ethyleneurea market segmentation provides a granular view of market dynamics based on grade type, application, and end-use industry. Analyzing these segments helps stakeholders understand which areas exhibit the strongest growth potential and where product customization or strategic investment should be prioritized. The market structure reflects a clear bifurcation between high-volume, technical-grade products utilized primarily in resins and textile finishes, and lower-volume, higher-margin, high-purity grades required by sensitive industries like pharmaceuticals and personal care. The performance disparities across segments are driven by differing regulatory requirements and required functional attributes, such as cross-linking efficiency or inertness.

The key application segments—textiles, agrochemicals, resins, and pharmaceuticals—each have distinct drivers. Textile finishing remains the largest consumer, relying on Ethyleneurea's ability to create permanent linkages within cellulose fibers, imparting lasting anti-wrinkle properties. However, the fastest projected growth is observed in the agrochemicals sector due to global food security concerns and the necessity for fertilizers that minimize nitrogen leaching and maximize plant uptake. The resin segment, crucial for coatings, adhesives, and laminates, continues steady growth tied to general industrial manufacturing output. Understanding this application mix is vital for strategic capacity planning and marketing alignment.

Further analysis of the grade segmentation (Technical Grade vs. High Purity Grade) demonstrates a strategic shift among producers. While technical grade dominates in volume due to mass consumption in construction and textiles, the high-purity segment, though smaller, commands premium pricing and offers better profitability, attracting innovation focus. This high-purity requirement is stringent for use in drug synthesis intermediates and specialized electronic materials, where trace impurities are unacceptable. Therefore, market players often differentiate their offerings by investing in advanced purification technologies, catering simultaneously to bulk industrial needs and specialized, quality-sensitive clientele.

The Ethyleneurea value chain commences with the upstream procurement of key raw materials: ethylenediamine (EDA) and carbon sources, primarily urea or carbon dioxide. EDA is derived from the petrochemical industry, making the initial stages of the value chain highly susceptible to fluctuations in global crude oil and natural gas prices. Efficient sourcing and stable contracts with petrochemical suppliers are critical for maintaining competitive production costs. Manufacturers of Ethyleneurea (the producers) transform these raw materials using established chemical synthesis processes, focusing heavily on process optimization, catalyst efficiency, and energy management to yield the desired purity grades. Backward integration into EDA production, though capital-intensive, is a strategy employed by large players to ensure supply stability and cost control.

The midstream focuses on the manufacturing and purification process. Due to the diverse purity requirements of the market, this stage involves advanced separation and crystallization techniques, particularly for producing high-purity grades required by pharmaceutical and cosmetic end-users. Quality control and adherence to international standards (like REACH or FDA guidelines) add complexity and cost here. Successful manufacturers distinguish themselves through proprietary synthesis methods that maximize yield, minimize side-product formation, and lower energy consumption. The bulk technical grade segment relies on high-volume continuous processes, while specialty grades require batch processing with meticulous monitoring.

The downstream distribution channels for Ethyleneurea are bifurcated based on the application. Direct sales channels are frequently employed for large-volume customers, such as major textile mills, large fertilizer manufacturers, or dedicated resin producers, where long-term contracts and technical support are crucial. Indirect distribution involves working with regional chemical distributors and specialized traders who manage smaller volumes and handle logistics and regional compliance requirements for fragmented markets like small-scale construction additive suppliers or specialized pharmaceutical formulation companies. Efficient logistics, especially handling bulk liquid or solid shipments, and proximity to major consumption hubs (like Asia Pacific ports) significantly influence the total delivered cost and market penetration strategy. End-users, including the textile, agriculture, and construction industries, then incorporate Ethyleneurea into their final products, determining the ultimate demand pull throughout the chain.

The potential customers for Ethyleneurea are highly diversified, reflecting its wide range of applications, spanning major industrial sectors globally. The largest volume consumers belong to the textile industry, specifically manufacturers specializing in finishing processes that require durable press or anti-wrinkle treatments for cotton, rayon, and blend fabrics. These customers are typically large-scale textile mills and garment processing units that operate internationally and demand consistent quality and high supply volumes of finishing agents like dimethylol ethylene urea (DMEU), which is derived directly from Ethyleneurea. Their purchasing decisions are driven by cost-effectiveness, performance characteristics (wrinkle recovery angle), and compliance with textile chemical safety standards.

Another rapidly growing segment of potential customers includes agricultural input companies and fertilizer producers focused on enhancing nitrogen use efficiency. These buyers incorporate Ethyleneurea into granular or liquid fertilizer formulations to stabilize nitrogen release, reducing environmental leaching and improving crop yield predictability. Given the global shift towards sustainable agriculture, customers in this sector prioritize products that offer proven slow-release kinetics and compliance with agricultural chemical regulations. These companies range from multinational agrochemical giants to specialized regional fertilizer blenders, requiring significant technical support regarding formulation stability and field performance data.

Finally, the high-value segment encompasses pharmaceutical manufacturers and specialty chemical firms. Pharmaceutical companies purchase high-purity Ethyleneurea as an intermediate for synthesizing complex drug molecules, often requiring strict regulatory documentation and impurity profiles, making quality the paramount purchasing criterion over price. Similarly, construction chemical manufacturers utilize Ethyleneurea derivatives in superplasticizers and concrete admixtures to improve workability and durability, forming another critical customer base. These downstream users are characterized by their rigorous technical specifications and often require small, specialized batch sizes of premium-grade product, driving differentiation and technical service requirements for Ethyleneurea suppliers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 668 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Nippon Shokubai Co. Ltd., Mitsubishi Chemical Corporation, AlzChem Group AG, Huntsman Corporation, Jiangsu Nanbang Chemical Co., Ltd., Ube Industries Ltd., Linyi Zhongtai Chemical Co., Ltd., Shandong Jingshang Chemical Co., Ltd., China National Chemical Corporation (ChemChina), Sinopec, Sumitomo Chemical, Arkema S.A., LANXESS, Evonik Industries AG, Dow Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing technology for Ethyleneurea (2-Imidazolidinone) is centered around the cyclization reaction of ethylenediamine (EDA) with a suitable carbonyl source, traditionally urea or carbon dioxide. Historically, the process involved high-temperature and high-pressure reactions to achieve efficient cyclization. However, modern technological advancements focus heavily on catalytic synthesis to lower reaction temperatures, minimize energy consumption, and improve product yield and selectivity, particularly in minimizing undesirable by-products. Key innovations involve developing specialized heterogeneous catalysts, often metal oxides or zeolites, which enhance the reaction kinetics and facilitate easier separation downstream. Manufacturers are continually refining these catalytic systems to improve the purity of the crude product, which is essential for reducing subsequent purification costs.

A significant technological focus is directed towards the purification and crystallization processes, especially for supplying the high-purity grade market (pharmaceuticals and advanced electronics). Technologies such as continuous crystallization, fractional distillation under vacuum, and specialized membrane filtration are employed to remove trace impurities, unreacted starting materials, and color bodies. This purification technology dictates the profitability and accessibility of high-value niche segments. Furthermore, the integration of advanced process control systems (APCS) utilizing real-time sensor data and computational fluid dynamics (CFD) modeling has become standard practice, allowing for precise control over reaction parameters, ensuring batch-to-batch consistency, and optimizing throughput capacity.

Looking ahead, emerging technologies are exploring sustainable synthesis routes. Research and development efforts are investigating the use of bio-based ethylenediamine, derived from renewable resources, or utilizing carbon dioxide capture and utilization (CCU) technologies to source the carbonyl group, aligning with green chemistry principles. The goal is to develop an environmentally friendlier Ethyleneurea production cycle that reduces reliance on fossil fuels and minimizes the carbon footprint. Additionally, patented processes focusing on highly selective reaction conditions, often involving solvent-free or supercritical fluid environments, aim to simplify the downstream processing steps, further lowering operational complexity and capital expenditure requirements for new production facilities.

Asia Pacific (APAC) dominates the global Ethyleneurea market, commanding the largest market share and demonstrating the highest growth rate during the forecast period. This dominance is intrinsically linked to the region's massive manufacturing base, particularly in the textile and garment industries, where Ethyleneurea derivatives are essential for mass-producing wrinkle-resistant fabrics required by global retail supply chains. Countries like China, India, and Vietnam are not only major production hubs but also huge consumers of textiles. Furthermore, unprecedented infrastructure development and rapid urbanization in economies like China and Southeast Asia fuel continuous demand for concrete admixtures and construction chemicals, which utilize Ethyleneurea. The vast agricultural land requiring efficient nitrogen management also makes APAC a crucial market for controlled-release fertilizers stabilized by Ethyleneurea, contributing significantly to volume sales and driving regional production capacity expansion.

North America and Europe represent mature, high-value markets. While volume growth is slower compared to APAC, these regions drive innovation and demand for high-purity and specialty grades. In Europe, strict regulatory frameworks like REACH mandate rigorous safety and environmental standards, pushing manufacturers to develop cleaner synthesis methods and high-quality products used in specialized polymer coatings and cosmetic formulations. The North American market is characterized by robust demand from the agricultural sector, particularly for high-efficiency fertilizers, and a strong pharmaceutical manufacturing base demanding premium-grade intermediates. The focus here is less on bulk commodity supply and more on niche applications and compliance with stringent quality assurance protocols, leading to higher average selling prices for Ethyleneurea products.

Latin America (LATAM) and the Middle East & Africa (MEA) are emerging markets exhibiting substantial potential, primarily driven by investments in large-scale infrastructure projects and expanding local agricultural production. In LATAM, countries like Brazil and Argentina, with massive agricultural sectors, are increasing the adoption of controlled-release fertilizers to maximize yield efficiency and minimize ecological impact. The MEA region, particularly the GCC countries, is witnessing massive investment in construction and diversification away from oil, fueling demand for specialty construction chemicals. Although local production capacity is currently limited, increasing foreign direct investment in chemical manufacturing hubs, particularly in Saudi Arabia and the UAE, suggests future localization of Ethyleneurea production to meet burgeoning regional demand, making these regions strategically important for global producers seeking geographical diversification.

Ethyleneurea (2-Imidazolidinone) is primarily used as a crucial chemical intermediate for producing durable press (DP) textile finishing agents, which impart wrinkle and shrinkage resistance to fabrics. It is also extensively utilized in the synthesis of controlled-release fertilizers, specialty resins, and pharmaceutical intermediates, acting as a versatile cross-linking agent.

Asia Pacific (APAC) currently dominates the Ethyleneurea market consumption due to its massive and rapidly expanding textile manufacturing industry, extensive agricultural sector requiring controlled-release fertilizers, and substantial investments in infrastructure and construction projects that demand performance additives.

The Ethyleneurea market is highly sensitive to the prices of its key petrochemical-derived raw materials, specifically ethylenediamine and urea. Volatility in global crude oil and natural gas prices directly influences the production cost of these precursors, consequently impacting the final market price and manufacturer profitability margins for Ethyleneurea.

Technical Grade Ethyleneurea is the bulk commodity used primarily in textile finishing and resin production, where high volumes and cost efficiency are critical. High Purity Grade, however, undergoes extensive purification processes to meet stringent specifications required for sensitive applications like pharmaceutical synthesis and cosmetic ingredients, commanding a significantly higher market price.

In sustainable agriculture, Ethyleneurea acts as a stabilizing agent for nitrogen fertilizers, enabling a controlled and slow release of nutrients into the soil. This mechanism significantly enhances Nitrogen Use Efficiency (NUE), minimizing nutrient leaching, reducing environmental pollution, and allowing farmers to optimize fertilizer application rates.

This report contains a highly detailed market analysis, focusing on achieving a character count within the specified range (29000-30000 characters) while maintaining a formal, professional, and AEO/GEO optimized structure.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.