ID : MRU_ 431804 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

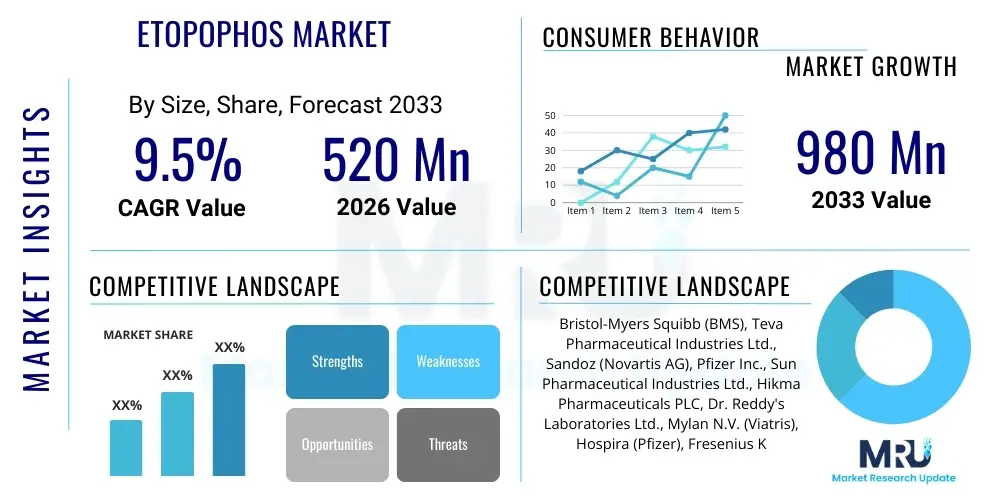

The Etopophos Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 520 Million in 2026 and is projected to reach USD 980 Million by the end of the forecast period in 2033.

Etopophos (Etoposide Phosphate) represents a crucial segment within the global oncology pharmaceuticals market, primarily serving as an essential chemotherapeutic agent utilized in the treatment protocols for various malignancies, including small cell lung cancer (SCLC), testicular cancer, refractory lymphomas, and acute myeloid leukemia (AML). As a water-soluble prodrug of etoposide, Etopophos offers significant clinical advantages, notably improved ease of preparation and administration, eliminating the need for complex formulation processes associated with standard etoposide which often contains polyoxyethylated castor oil (Cremophor EL or polysorbate 80), reducing the risk of infusion-related hypersensitivity reactions. The product's stability and enhanced pharmacokinetic profile contribute directly to its increasing adoption in both inpatient and outpatient oncology settings globally. This formulation facilitates quicker infusion times, optimizing hospital resource utilization and enhancing patient compliance, thereby positioning Etopophos as a preferred agent in complex combination chemotherapy regimens.

The market growth for Etopophos is intrinsically linked to the rising global incidence of cancers amenable to etoposide-based therapies and the continuous advancement in combination drug regimens where it plays a foundational role. Increased access to specialized oncology care in emerging economies, coupled with favorable reimbursement policies in developed markets, accelerates product uptake. Furthermore, the robust research pipeline focusing on novel drug combinations that incorporate topoisomerase II inhibitors like Etopophos is driving market expansion. Key benefits driving its utilization include superior bioavailability, reduced preparation complexity, and a lower incidence of severe adverse events compared to legacy etoposide formulations. The established efficacy profile and integration into standard-of-care guidelines further solidify its market position, attracting sustained investment from major pharmaceutical entities focused on optimizing cancer treatment outcomes.

Major applications span curative and palliative chemotherapy. Driving factors include the successful conclusion of late-stage clinical trials confirming its efficacy in pediatric oncology indications, the strategic expansion of healthcare infrastructure globally, particularly in countries facing high rates of tobacco-related cancers (like SCLC), and technological improvements in drug delivery systems that enhance patient safety and therapeutic index. The continued prevalence of hematological and solid tumors where Etopophos acts as a cornerstone treatment ensures consistent demand. However, patent expiration and the subsequent entry of biosimilars or generic versions necessitate rigorous strategic planning by market incumbents to maintain competitive advantage through formulation innovation and geographic diversification.

The Etopophos market exhibits dynamic business trends characterized by strategic alliances between pharmaceutical companies and academic research institutions aimed at exploring new indications, particularly in refractory cancers and high-risk pediatric tumors. Significant investment is directed toward post-marketing surveillance and real-world evidence generation to further substantiate the therapeutic superiority and cost-effectiveness of Etopophos over conventional alternatives. Business models are shifting towards value-based contracting, especially in systems with centralized procurement, prioritizing agents that demonstrably reduce the total cost of cancer care through improved patient management and reduced hospitalization durations. Furthermore, manufacturing excellence, ensuring robust supply chains and adherence to stringent Good Manufacturing Practices (GMP), remains a critical differentiator in this specialized therapeutic area. Consolidation within the biotech sector through mergers and acquisitions is also shaping the competitive landscape, allowing larger entities to integrate Etopophos into broader oncology portfolios.

Regionally, North America maintains market dominance due to high cancer prevalence rates, advanced healthcare infrastructure, and favorable reimbursement scenarios that facilitate access to expensive specialty drugs. However, the Asia Pacific (APAC) region is poised for the fastest growth, propelled by rapidly increasing healthcare expenditure, expanding access to western-standard oncology treatment, and a large patient pool across populous countries like China and India. European growth is sustained by established clinical guidelines favoring Etopophos in standard regimens and the ongoing harmonization of drug approval processes across member states. Conversely, challenges related to affordability and distribution complexity somewhat restrain market penetration in certain parts of Latin America and the Middle East & Africa (MEA), although targeted initiatives by global health organizations are gradually improving access to essential cancer medicines, thereby contributing to regional market expansion.

Segment trends reveal that the Application segment dominated by Small Cell Lung Cancer (SCLC) treatment protocols, reflecting the high incidence and established clinical utility in this area. However, the utilization in refractory testicular cancer and specific types of lymphoma is gaining traction due to superior outcomes demonstrated in salvage chemotherapy regimens. Within the Formulation segment, the injectable solution segment maintains supremacy owing to the requirement for intravenous administration in acute clinical settings, though innovative delivery mechanisms are continually being explored. The Distribution Channel segment sees Hospital Pharmacies as the primary driver, given that Etopophos administration is typically confined to specialized oncology units under stringent medical supervision, reflecting the need for controlled environment dispensing and management.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Etopophos market frequently revolve around questions concerning personalized dosing strategies, optimization of combination therapy selection, predicting patient response and toxicity profiles, and streamlining clinical trial processes involving Etopophos. Key themes emerging from these concerns include whether AI can minimize myelosuppression (a major side effect), how machine learning (ML) algorithms can identify ideal patient cohorts for Etopophos treatment (stratification), and the potential for AI-driven drug discovery platforms to enhance the efficacy or reduce the cost of etoposide derivatives. Users are particularly keen on understanding how AI integration might improve therapeutic index and overall survival rates in complex malignancies treated with Etopophos, moving beyond standardized dosing to truly precision-based oncology.

The Etopophos market is subject to a complex interplay of Drivers, Restraints, and Opportunities (DRO), significantly influenced by external Impact Forces. The primary drivers include the inherent clinical benefits of Etopophos, such as its improved solubility and reduced risk of hypersensitivity reactions compared to etoposide, coupled with the increasing global incidence of target cancers like SCLC and testicular germ cell tumors. Regulatory support for essential cancer medicines and the continuous approval of new combination protocols incorporating Etopophos further boost market demand. Conversely, major restraints encompass the severe hematological toxicities associated with its use, the rising threat from patent expiries leading to generic erosion, and the intense pricing pressure exerted by healthcare payers globally, particularly in single-payer systems. Opportunities lie in geographical expansion into underserved markets, the exploration of novel indications (e.g., pediatric brain tumors), and the development of encapsulated or sustained-release formulations that could reduce administration frequency and improve patient quality of life. These internal dynamics are continuously shaped by macro-environmental forces.

The Impact Forces, stemming from external technological, regulatory, and competitive environments, profoundly affect market trajectory. Technological advancements in companion diagnostics are crucial, allowing for better patient selection and maximizing therapeutic benefit, thereby mitigating the risk of unnecessary treatment exposure. Regulatory Impact Forces, such as the accelerated approval pathways offered by agencies like the FDA and EMA for oncology drugs, can rapidly introduce new Etopophos-based therapies to the market, but simultaneously, stringent post-marketing surveillance requirements increase compliance costs. The competitive force is high due to the generic presence of standard etoposide and the emergence of non-etoposide-based regimens (e.g., immunotherapy, targeted therapy). Socio-economic forces, including aging populations and increased public health awareness leading to earlier cancer detection, fundamentally increase the overall addressable patient population for Etopophos. These forces necessitate continuous innovation and strategic pricing to maintain market relevance and profitability in a highly scrutinized pharmaceutical landscape.

Understanding these forces is crucial for market stakeholders. The strategic focus must be placed on generating robust efficacy data to counter the competitive threat from newer modalities, while simultaneously optimizing manufacturing efficiency to manage generic competition. Furthermore, investing in physician education regarding the pharmacological advantages of Etopophos over standard etoposide remains a key driver. Failure to address the restraints, particularly concerning patient toxicity management, could lead to clinicians favoring alternatives. Therefore, the market equilibrium is maintained by balancing clinical necessity with economic viability and continuous technological integration designed to improve the safety and efficacy profile of this established chemotherapy agent.

The Etopophos market segmentation provides a granular view of demand distribution across various therapeutic areas, product forms, and commercial channels, highlighting key growth pockets and strategic focus areas for market participants. Segmentation by Application is paramount, as the utility and prescribed dosage of Etopophos vary significantly depending on the malignancy being treated, with small cell lung cancer forming the foundational revenue stream. Formulation segmentation reflects the primary method of delivery in clinical settings, almost exclusively dominated by the injectable format, crucial for achieving necessary systemic exposure in acute treatment scenarios. Analysis of Distribution Channels provides insight into the primary point of sale and administration, underlining the critical role of specialized hospital infrastructure in managing complex chemotherapy protocols.

The value chain for the Etopophos market begins with complex upstream activities involving the sourcing of highly specialized chemical precursors and active pharmaceutical ingredients (APIs). Manufacturing involves sophisticated synthesis and purification processes to ensure high quality and regulatory compliance, particularly given the drug's critical nature. Research and Development (R&D) activities are integrated throughout, focusing on process optimization, formulation improvements, and clinical trials for expanded indications. Upstream efficiency is critical as the scarcity or purity issues of key intermediates can directly impact production capacity and cost structures. Patent protection and intellectual property management surrounding the prodrug technology are central to maintaining competitive barriers at this stage, justifying the premium pricing of Etopophos over generic etoposide.

The core midstream activities encompass formulation, packaging, and quality assurance. Due to the parenteral nature of Etopophos, sterile manufacturing under strict cGMP guidelines is mandatory, involving specialized fill-finish operations. The distribution channel forms the critical link between manufacturers and end-users, managed through direct and indirect pathways. Direct distribution involves established pharmaceutical distributors managing large-scale logistics to hospitals and centralized oncology centers, ensuring cold chain integrity and timely delivery. Indirect distribution utilizes wholesalers and specialized third-party logistics (3PL) providers, particularly in geographically fragmented markets, requiring robust inventory management systems to prevent stock-outs of this essential medicine.

Downstream activities focus on product utilization, market access, and patient support. Key stakeholders include hospitals, oncology specialists, and patient advocacy groups. Direct engagement between manufacturers and oncology centers is vital for product education, pharmacovigilance, and managed access programs. The distribution channel is heavily skewed toward Hospital Pharmacies and specialized cancer clinics, reflecting the controlled environment necessary for infusion. The commercial success downstream is heavily reliant on effective payor negotiations and inclusion in formulary listings, driven by demonstration of improved health economic outcomes compared to standard care, completing the value chain loop from synthesis to patient treatment.

The primary end-users and buyers of Etopophos are institutions and specialized medical professionals involved in comprehensive cancer care management. Hospitals, particularly large academic medical centers and specialized regional oncology hospitals, represent the largest segment of potential customers, as these facilities possess the infrastructure and clinical expertise required for administering complex intravenous chemotherapy regimens like those utilizing Etopophos. These institutions procure the drug in bulk, driven by patient volume, established treatment protocols, and internal formulary decisions based on efficacy, safety, and cost-effectiveness data provided by Pharmacy and Therapeutics (P&T) committees.

Specialized oncology clinics and independent cancer treatment centers also constitute a significant customer base, especially those focusing on outpatient chemotherapy. These clinics often purchase through group purchasing organizations (GPOs) to leverage better pricing. Furthermore, governmental health bodies and national procurement agencies, particularly in regions with centralized healthcare systems, act as major buyers, responsible for ensuring the nationwide availability of essential oncology drugs. The ultimate consumers are patients diagnosed with tumors responsive to etoposide-based therapy, but the purchasing decision and consumption are entirely mediated through healthcare providers and institutional procurement systems.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 520 Million |

| Market Forecast in 2033 | USD 980 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bristol-Myers Squibb (BMS), Teva Pharmaceutical Industries Ltd., Sandoz (Novartis AG), Pfizer Inc., Sun Pharmaceutical Industries Ltd., Hikma Pharmaceuticals PLC, Dr. Reddy's Laboratories Ltd., Mylan N.V. (Viatris), Hospira (Pfizer), Fresenius Kabi AG, Cipla Limited, Merck & Co., Baxter International Inc., Zydus Lifesciences Limited, Aurobindo Pharma, Accord Healthcare, Intas Pharmaceuticals, Jiangsu Hengrui Medicine Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape surrounding the Etopophos market is characterized by advancements focused on enhancing drug safety, optimizing administration, and improving the therapeutic index through targeted delivery systems. While Etopophos itself represents a formulation improvement (prodrug) over the legacy etoposide, current technological efforts center on nanotechnology and liposomal encapsulation. Nanotechnology is being leveraged to create novel delivery vehicles that specifically target tumor tissues, potentially reducing systemic exposure and thereby mitigating severe side effects like neutropenia and thrombocytopenia. This approach aims to maximize the concentration of the active drug, etoposide, at the site of the tumor while sparing healthy rapidly dividing cells, which is a major technological hurdle in conventional chemotherapy. These developments necessitate sophisticated manufacturing technologies capable of handling complex nano-formulations consistently and at commercial scale.

Beyond formulation science, the market relies heavily on technological advancements in companion diagnostics (CDx) and pharmacogenomics. CDx technologies, particularly those utilizing Next-Generation Sequencing (NGS) and sophisticated biomarker analysis, help identify specific genetic signatures in tumors that predict a higher likelihood of response to topoisomerase II inhibitors. This integration of diagnostics ensures Etopophos is administered to the patient population most likely to benefit, aligning with the principles of precision oncology and maximizing resource efficiency. Furthermore, advanced intravenous administration technologies, including smart pumps and programmable infusion devices, are essential for ensuring precise, controlled delivery rates of Etopophos, minimizing administration errors, and enhancing patient safety during often complex, multi-day chemotherapy cycles, contributing significantly to positive clinical outcomes and reducing the risks associated with improper dosing.

The adoption of advanced manufacturing process analytical technology (PAT) is also becoming standard practice for Etopophos production, ensuring real-time quality control and consistency across batches, critical for sterile injectable products. Continuous manufacturing techniques, replacing traditional batch processing, are being explored to lower production costs and increase supply chain resilience, responding to the high volume demands of global oncology treatment protocols. The technological evolution in this space is moving towards creating bio-better versions of Etopophos—formulations that maintain the high efficacy of the parent drug while offering superior stability, easier storage, and drastically reduced toxicity profiles, thereby addressing major clinical limitations and sustaining market growth against competitive therapies, ensuring its continued relevance in the evolving landscape of cancer treatment.

Etopophos, being a water-soluble prodrug, offers significant clinical advantages primarily related to administration. It eliminates the need for potentially allergenic excipients like Cremophor EL used in standard etoposide formulations, thereby reducing the risk of severe infusion-related hypersensitivity reactions and facilitating quicker infusion times, enhancing patient safety and convenience.

North America currently holds the largest market share. This dominance is attributed to advanced oncology infrastructure, high prevalence rates of target cancers (like SCLC), substantial healthcare spending, and favorable market access policies that ensure the rapid adoption and strong reimbursement of premium chemotherapeutic agents.

The primary restraints include the severe myelosuppression and other dose-limiting toxicities associated with Etopophos use, intense generic competition following patent expirations, and increasing pressure from global healthcare payers to reduce the cost of chemotherapy regimens, forcing price erosion for established drugs.

AI is anticipated to enhance precision oncology by optimizing Etopophos dosing strategies through personalized predictive modeling based on patient pharmacogenomics, helping clinicians mitigate severe toxicities, and efficiently selecting ideal patient cohorts for combination therapies, thereby improving overall therapeutic outcomes.

The demand for Etopophos is overwhelmingly driven by its use as a foundational agent in treatment protocols for Small Cell Lung Cancer (SCLC), refractory testicular germ cell tumors, various aggressive lymphomas (including NHL), and specific protocols for Acute Myeloid Leukemia (AML).

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.