ID : MRU_ 444826 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

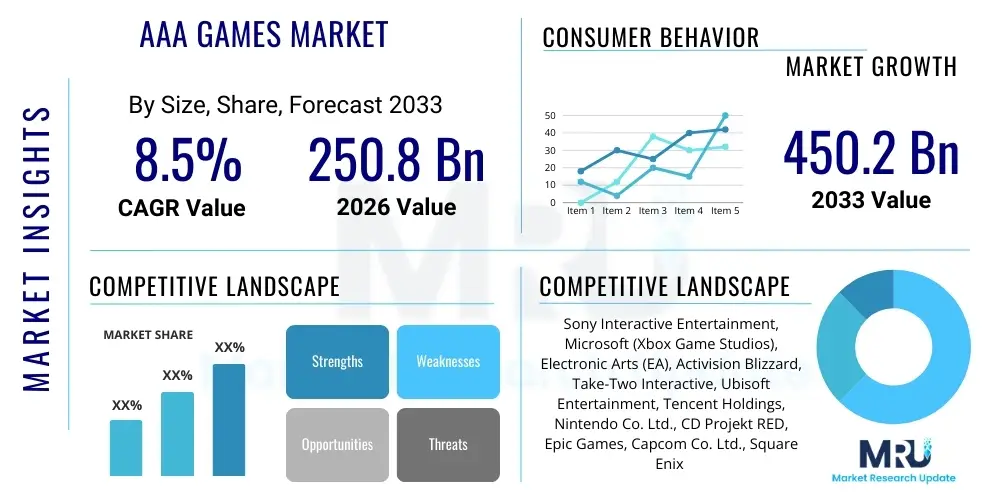

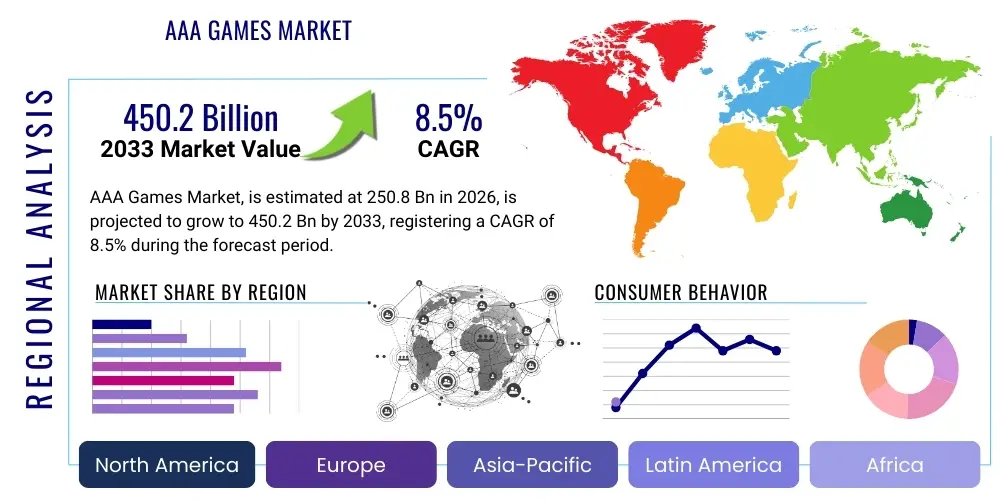

The AAA Games Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 250.8 Billion in 2026 and is projected to reach USD 450.2 Billion by the end of the forecast period in 2033.

The AAA Games Market encompasses high-budget, high-profile video game titles typically developed by large, established studios and backed by significant marketing campaigns. These games are characterized by exceptional production values, advanced graphical fidelity, complex narratives, and substantial development teams, often utilizing cutting-edge technology such as advanced ray tracing, sophisticated physics engines, and expansive open-world architectures. The product description centers on delivering premium interactive entertainment experiences across major platforms, including PC, consoles (PlayStation, Xbox, Nintendo), and increasingly, high-end mobile devices and cloud streaming services. The inherent complexity and scale of these projects necessitate massive capital investment, driving the market toward consolidation among leading publishers who can sustain multi-year development cycles.

Major applications of AAA games span consumer entertainment, competitive esports, and social interaction through persistent online multiplayer environments. They serve as technological showcases, often pioneering features that later trickle down to lower-budget titles, driving demand for high-performance consumer hardware. The primary benefits derived by consumers include high-quality, long-form entertainment, immersion in detailed virtual worlds, and engagement with rich, professionally written narratives. For publishers, AAA titles act as critical intellectual property (IP) anchors, generating substantial revenues through initial sales, recurrent consumer spending (RCS) via downloadable content (DLC), microtransactions, and season passes, thereby creating enduring franchises.

Driving factors for the sustained growth of the AAA Games Market include the increasing global availability of high-speed internet and reliable broadband infrastructure, particularly in emerging markets, which facilitates the distribution of large game files and supports low-latency online play. Furthermore, the continuous evolution of console hardware (e.g., generational upgrades like PS5 and Xbox Series X/S) and PC graphics technology (GPUs) mandates the development of more graphically intense and feature-rich titles, maintaining the demand for AAA content. The expansion of the global gaming audience, driven by increased leisure time and the normalization of gaming across diverse demographics, coupled with the success of monetization models focused on live service elements, further fuels the market’s expansion.

The AAA Games Market is exhibiting robust growth, driven primarily by favorable business trends centered around the expansion of "Games as a Service" (GaaS) models, which prioritize long-term player retention and maximized recurrent consumer spending. Major publishers are strategically shifting capital towards fewer, higher-quality, live-service-enabled titles, mitigating the risk associated with one-off launches and ensuring sustained revenue streams post-launch. Key business trends also involve significant merger and acquisition activity aimed at consolidating IP portfolios and securing essential development talent, alongside increasing utilization of proprietary game engines and cloud infrastructure to enhance scalability and cross-platform compatibility. Technological advancements in rendering capabilities and procedural content generation are improving development efficiency, though time-to-market remains substantial for flagship titles.

Regionally, North America and Europe continue to dominate the market share due to high disposable income, well-established console ecosystems, and robust PC gaming culture, characterized by early adoption of new hardware and subscription services. However, the Asia Pacific (APAC) region is demonstrating the highest growth velocity, fueled by explosive growth in mobile gaming transitioning to high-fidelity AAA experiences and the massive scale of the Chinese and Indian gaming populations. Regional trends emphasize localization excellence and adapting monetization strategies to local consumer preferences, particularly the strong preference for free-to-play models supported by cosmetic microtransactions in specific Asian markets. Infrastructure improvements, particularly 5G deployment, are accelerating market access across all territories.

Segmentation trends highlight the enduring dominance of the Console segment, particularly due to the current generation hardware cycle pushing graphical boundaries. Nevertheless, the PC segment maintains relevance through competitive esports titles and flexibility, while the Mobile segment, though previously distinct, is increasingly incorporating AAA production values (the 'AA/AAA' hybrid model) to capture the premium market space. Genre-wise, Role-Playing Games (RPGs) and Action-Adventure titles remain the most capital-intensive and highly anticipated segments, benefiting significantly from open-world design and extensive replayability. The distribution segment is overwhelmingly digital, with digital sales constituting over 90% of the revenue, significantly lowering logistical costs for publishers and enhancing direct consumer engagement.

Users and industry stakeholders frequently question how Artificial Intelligence will fundamentally alter the economics and creative output of AAA game development. Common concerns revolve around AI's potential role in displacing human development jobs, particularly in asset creation, animation, and quality assurance (QA). Expectations are high regarding AI's ability to create more dynamic, realistic, and personalized non-player characters (NPCs) and procedural content that enhances replayability without massive manual intervention. Users are also keen on understanding how AI will handle balancing in competitive multiplayer games and whether it can truly generate compelling, coherent narrative structures, moving beyond simple dialogue trees. The consensus theme is a cautious optimism: AI is viewed as a powerful tool for accelerating iterative development and increasing content volume, rather than a direct replacement for core creative direction, while simultaneously raising complex intellectual property (IP) and ethical concerns regarding the training data used by generative models.

The integration of advanced AI/Machine Learning (ML) techniques is transforming AAA production pipelines, shifting the focus from manual resource creation to system design and curation. AI models are becoming essential for generating vast quantities of high-fidelity environmental assets (textures, models, foliage), significantly reducing the time spent by artists on repetitive tasks. Furthermore, behavioral AI is enabling emergent gameplay through more sophisticated NPC interactions, pathfinding, and combat tactics, moving away from scripted sequences toward dynamic, player-driven experiences. This shift not only enhances the consumer experience by providing greater immersion and challenge but also allows creative teams to focus their resources on bespoke, high-impact narrative and design elements, fundamentally restructuring the allocation of development hours across multi-million dollar projects.

The AAA Games Market is fundamentally shaped by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO). Key drivers include relentless technological advancements, particularly in GPU capabilities and console generational shifts, which necessitate continuous investment in new AAA content to maximize hardware potential. The sustained success of the live service model, ensuring reliable, long-term revenue streams through microtransactions and recurring spending, incentivizes major publishers to commit immense budgets to these projects. Conversely, the primary restraints center on escalating development costs—often exceeding $200 million for a single title—which heighten financial risk and contribute to industry instability, frequently resulting in project cancellations or delays. Furthermore, intense market saturation and the limited release window for major titles create highly competitive conditions, where marketing expenses often rival development budgets.

Opportunities for expansion are primarily concentrated in emerging geographical markets, especially Asia Pacific and Latin America, where rapid growth in internet penetration and disposable income is unlocking millions of potential premium customers. Additionally, the nascent but rapidly maturing field of cloud gaming represents a significant opportunity, potentially lowering the barrier to entry for high-fidelity AAA experiences by eliminating the need for expensive local hardware. Strategic opportunities also lie in further developing cross-platform play capabilities and leveraging major cinematic or television IP integrations, capitalizing on existing brand recognition to guarantee large initial audience uptake. The impact forces affecting the market are heavily weighted toward technological disruption, consumer expectations for flawless launches, and the competitive landscape for securing and retaining elite development talent, which is highly specialized and scarce.

The structural impact forces governing the AAA Games market include the power of buyers, which is high due to the abundance of competitive entertainment options, making consumers highly selective regarding title quality and value proposition. The threat of substitutes, comprising other forms of digital entertainment (e.g., streaming video, social media, independent games), is substantial. However, the high barrier to entry—mandating massive capital, sophisticated proprietary technology, and established IP—keeps the threat of new entrants relatively low for true AAA titles. Supplier power (talent, engine providers like Unity/Epic, and hardware manufacturers) exerts moderate influence but is typically managed through long-term contracts and strategic partnerships, focusing on optimizing the multi-year production cycle necessary for success.

The AAA Games Market is strategically segmented across several key dimensions, providing a refined view of revenue generation and consumer behavior. Primary segmentation occurs by Platform Type, distinguishing between Console, PC, and Mobile (high-end). A critical distinction is also made by Revenue Model, separating traditional upfront purchases from the highly lucrative Recurrent Consumer Spending (RCS) derived from microtransactions, subscriptions, and DLC. Further segmentation is analyzed by Genre, reflecting the varying investment requirements and audience sizes for different game types, such as Action-Adventure, RPG, Shooter, and Sports/Racing simulations. Understanding these segments is crucial for publishers to allocate resources efficiently, target marketing campaigns accurately, and forecast long-term franchise viability, especially as cross-platform play blurs the traditional boundaries between these categories.

The AAA Games market value chain is extensive and highly integrated, beginning with upstream activities focused on content creation and foundational technology. Upstream analysis involves the core intellectual property (IP) creation, typically managed by internal studio teams or acquired through licensing deals. This phase heavily relies on technology suppliers, including providers of powerful proprietary game engines (such as Unreal Engine or internal solutions like the Frostbite engine), sophisticated development tools, and high-end hardware for asset rendering and testing. The crucial upstream bottleneck often lies in securing specialized talent—programmers, animators, and writers—who command high salaries and determine the quality benchmark of the final product. Financial investment and early-stage publishing decisions define the scope and budget at this initial stage, setting the trajectory for the entire development lifecycle.

The midstream process is dominated by the development and publishing activities. Development involves multi-year sprints focused on asset production, coding, level design, and quality assurance (QA). Publishing houses manage financing, external marketing, and securing deals with platform holders (Sony, Microsoft). This stage is characterized by high operational complexity and coordination across multiple global teams. Downstream activities focus entirely on market delivery, customer acquisition, and post-launch revenue generation. The distribution channel is predominantly digital, relying on platform marketplaces (direct distribution) like Steam or PlayStation Network. The shift to digital distribution has fundamentally altered the physical retail component, greatly improving margins and allowing publishers direct control over pricing and post-launch patching/updates.

Direct distribution through proprietary launchers or console marketplaces allows publishers to bypass intermediaries, maximizing revenue per unit sold and providing direct access to crucial consumer data for optimizing live service games. Indirect distribution still exists through third-party digital storefronts and, minimally, physical retail partners, which primarily serve niche markets or collector editions. The profitability of the downstream segment is increasingly tied not just to initial sales but to the effectiveness of marketing campaigns, which often leverage massive influencer networks and digital advertising budgets, and the long-term success of recurrent consumer spending strategies (DLC, microtransactions), ensuring that the post-launch service phase is now a core component of the value chain, extending the lifecycle of the product and generating revenue years after the initial release.

The primary target demographic and potential customers for the AAA Games Market are broadly categorized as dedicated and core gamers, typically aged 18 to 45, who possess high disposable income and significant leisure time allocated to gaming. These consumers are platform-agnostic but show strong loyalty to their preferred ecosystems (PC master race, specific console loyalty). They prioritize graphical fidelity, sophisticated narrative depth, extensive replayability, and competitive multiplayer engagement. Key buyers are often early adopters of new hardware, willing to invest heavily in premium consoles, high-end PCs, and supporting peripherals (high-refresh-rate monitors, specialized controllers), ensuring they experience the content exactly as intended by the developers. This segment drives initial unit sales and provides critical feedback during pre-release testing phases.

A rapidly expanding secondary customer base includes the casual enthusiast and the live-service participant, drawn in by successful monetization loops rather than initial hype alone. These customers may not purchase every new AAA release but commit heavily to established titles with ongoing content updates, particularly those focused on social interaction or competitive ranking (e.g., massive multiplayer titles or games utilizing battle passes). For this group, the value proposition is defined by sustained engagement, community features, and the perceived fairness and cosmetic appeal of in-game purchases. Geographical expansion means that potential customers in emerging economies are becoming increasingly important, requiring flexible pricing strategies and localized content to meet regional market dynamics.

Finally, the growing accessibility provided by cloud gaming platforms (like Xbox Cloud Gaming and PlayStation Plus Premium) is expanding the potential customer pool to individuals who previously lacked the requisite capital for high-end hardware. These consumers, though potentially spending less per title initially, represent a massive volume opportunity for subscription-based access to back catalogs and new releases. The ultimate end-user is anyone seeking the pinnacle of interactive digital entertainment, whether through solo narrative immersion, global competitive esports, or shared social experiences within persistent virtual worlds, making high production value and technical polish the non-negotiable expectation for market success.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 250.8 Billion |

| Market Forecast in 2033 | USD 450.2 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sony Interactive Entertainment, Microsoft (Xbox Game Studios), Electronic Arts (EA), Activision Blizzard, Take-Two Interactive, Ubisoft Entertainment, Tencent Holdings, Nintendo Co. Ltd., CD Projekt RED, Epic Games, Capcom Co. Ltd., Square Enix Holdings, Bandai Namco Holdings, Sega Sammy Holdings, Embracer Group, Warner Bros. Games, Konami Group, Bethesda Softworks (ZeniMax Media), Roblox Corporation, Krafton Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological foundation of the AAA Games Market is characterized by continuous innovation aimed at increasing visual realism, complexity, and performance efficiency. Core to this landscape are advanced proprietary and commercial game engines, such as Epic’s Unreal Engine 5 and Unity’s high-definition render pipeline (HDRP), which support cinematic rendering capabilities like path tracing and virtualized geometry (e.g., Nanite). These technologies enable developers to utilize film-quality assets and massive, detailed environments without crippling performance requirements on consumer hardware. Crucially, the implementation of Ray Tracing (RT) and hardware-accelerated rendering on current-generation consoles and high-end PC GPUs dictates the visual benchmark for all new AAA titles, pushing the boundaries of lighting, reflections, and shadowing to unprecedented levels of photorealism.

Beyond visual rendering, a significant technological shift involves the integration of sophisticated network infrastructure and cloud technologies. Cloud computing is vital not only for supporting massive, persistent multiplayer environments and managing the enormous data traffic associated with live-service games but also for facilitating remote development workflows and collaborative content creation across globally dispersed teams. Server-side computational power is increasingly utilized for complex physics simulations and AI processing that cannot be handled efficiently by the client device. Furthermore, the adoption of proprietary compression techniques and streaming technologies (like DirectStorage) minimizes loading times and optimizes asset delivery, which is critical for maintaining immersion in expansive open-world games and meeting high user expectations for instantaneous responsiveness.

Future growth in the AAA technology landscape will be dominated by generative AI and Machine Learning (ML) techniques applied to content production, quality assurance, and player experience personalization. ML models are now essential for optimizing frame rates, performing intelligent upscaling (e.g., DLSS, FSR), and predicting player churn in live-service titles. As development costs escalate, tools that leverage procedural generation combined with AI supervision will become mandatory for studios to remain competitive. Furthermore, the burgeoning requirement for cross-platform compatibility necessitates robust technology solutions that allow for seamless scaling and unified performance across diverse hardware architectures, from high-end PCs to mobile devices capable of running AAA-quality streamed content.

Growth is primarily driven by continuous technological advancements in console and PC hardware, the sustained profitability of the "Games as a Service" (GaaS) revenue model utilizing microtransactions and subscriptions, and the expansion of the global gaming audience through improved internet infrastructure and cloud gaming accessibility. Generational console upgrades mandate new AAA content.

The average development budget for a major AAA title often ranges between USD 100 million and USD 300 million, not including marketing and distribution costs, which can add another 50% to 100% to the total investment. This high cost is due to lengthy development cycles, high labor requirements for specialized talent, and complex asset creation.

While initial full game purchases remain significant, Recurrent Consumer Spending (RCS)—derived from downloadable content (DLC), expansions, and, critically, microtransactions (cosmetic items, season passes)—is increasingly the primary driver of long-term profitability and revenue stability for successful AAA franchises operating as live service models.

The most significant challenge is managing the escalating complexity and scale of content required for open-world games while maintaining performance and avoiding development bottlenecks. This complexity necessitates reliance on advanced real-time rendering technologies (like Ray Tracing) and the implementation of AI/procedural tools to accelerate asset creation and quality assurance processes efficiently.

The Asia Pacific (APAC) region, driven by markets such as China, South Korea, and India, exhibits the fastest growth rate due to increased internet penetration, rising disposable incomes, and the normalization of high-fidelity gaming across mobile and PC platforms, rapidly increasing the addressable market size for AAA titles.

Cloud gaming services are acting as a major market opportunity by lowering the hardware entry barrier for consumers, allowing them to access high-fidelity AAA titles without owning an expensive local console or PC. This model supports subscription-based access and expands the potential audience demographic significantly, particularly in regions with established broadband access.

Proprietary engines (e.g., those developed internally by studios like Rockstar or EA) provide a competitive advantage by offering highly customized toolsets optimized for specific artistic visions and performance targets unique to major franchises. They are central to intellectual property management and technological differentiation, though commercial engines like Unreal Engine are also extensively used for their robust feature sets.

Primary risks include commercial failure due to intense competition and market saturation, high user expectations leading to severe backlash if quality or performance issues are present at launch (often termed 'launch day failures'), and the financial instability caused by multi-year development cycles which commit immense capital upfront before any return is realized.

Physical sales have significantly diminished in relevance, now representing a small, though stable, fraction of total revenue, primarily catering to collector editions, second-hand markets, and regions with less reliable internet infrastructure. Digital distribution accounts for over 90% of revenue for most major publishers due to better margins and direct consumer relationship management.

AI is increasingly utilized to create complex, emergent narrative systems rather than static, pre-scripted stories. This includes generating procedural dialogue options, adapting NPC behavior based on player choices, and contributing to the dynamic placement of side quests, ultimately enhancing the player’s sense of agency and replay value within the game world.

Large-scale acquisitions (e.g., Microsoft acquiring Activision Blizzard) reduce the overall number of major independent publishers, leading to increased market consolidation. This trend concentrates intellectual property and development talent under fewer entities, potentially increasing competition among the remaining giants while raising concerns over platform exclusivity and market choice for consumers.

AAA titles are distinguished by their exceptional budgetary scale (often exceeding $100M), massive development team sizes, use of proprietary or cutting-edge commercial engines, aggressive global marketing campaigns, and high expectations for technical polish, graphical fidelity, and lengthy playtime. AA titles typically operate with significantly smaller budgets and focused scope.

Labor trends, particularly focusing on reducing 'crunch culture' and improving working conditions, are challenging traditional AAA development timelines. While beneficial for employee welfare, this often leads to longer, more deliberate development cycles and increased utilization of external support studios or AI tools to manage workload and meet release demands.

Action-Adventure and large-scale Role-Playing Games (RPGs), especially those incorporating persistent open-world elements and high narrative complexity, currently attract the highest level of investment. These genres maximize consumer retention and recurrent spending opportunities over multi-year lifecycles.

AEO (Answer Engine Optimization) and GEO (Generative Engine Optimization) are strategies ensuring that complex market analysis content is structured for direct retrieval by AI-powered search and generative models. In this context, it ensures the report's structure (using precise HTML tags, detailed lists, and direct answers in FAQs) maximizes visibility and utility when processed by large language models seeking definitive market insights on AAA games.

5G technology is crucial because it provides the necessary low latency and high bandwidth to deliver high-quality cloud gaming experiences to mobile devices and remote locations. This infrastructure enhancement expands the potential market by making platform-agnostic AAA access reliable and seamless, particularly in congested urban areas and developing regions.

Risk mitigation strategies include transitioning franchises to GaaS models to ensure predictable revenue streams, utilizing established, proven intellectual property (IP), extensive pre-release testing and beta phases to gauge market reception, and securing platform exclusivity deals or major financing from platform holders to guarantee initial funding.

Cross-platform play, or 'cross-play,' is rapidly becoming a standard, expected feature for multiplayer AAA titles. It is vital for maximizing the total active player base, extending the social reach of the title, and ensuring healthy long-term matchmaking queues necessary for live service profitability across all major ecosystems (PC, Xbox, PlayStation).

While VR still represents a niche segment, the future outlook is positive as hardware fidelity increases (e.g., advanced headsets with higher resolution and integrated tracking) and development standards mature. Major publishers are cautiously investing in high-budget VR experiences or AAA titles with dedicated VR modes, anticipating significant long-term growth as adoption rates rise.

Social and community features are fundamentally important, acting as the primary mechanism for retaining players in the GaaS ecosystem. Features such as integrated chat, shared progression systems, cosmetic customization, and persistent team structures encourage continuous player interaction, directly supporting engagement and increasing the likelihood of recurrent consumer spending.

The most crucial metric is Lifetime Value (LTV) of the customer, often correlated with retention rates (daily/monthly active users). High LTV demonstrates that the title effectively monetizes through recurrent consumer spending over an extended period, confirming the franchise's sustainability and viability over initial sales figures alone.

Publishers manage IPs strategically by maintaining a balanced release slate, ensuring sequels or reboots are spaced appropriately, and expanding IPs into complementary media (film, television, merchandise). This minimizes market fatigue while maximizing the total revenue potential across different consumer segments and maximizing the brand recognition of core AAA properties.

'Crunch culture' refers to periods of mandatory, extreme overtime, often involving 60-100 hour work weeks, utilized primarily in the months leading up to a major AAA game release. While historically common, it is increasingly viewed as unsustainable and detrimental to talent retention, leading companies to seek more disciplined production scheduling and leverage AI tools to alleviate pressure.

Platform holders wield substantial influence by setting technical certification standards, driving the adoption of specific hardware features (like ray tracing or specialized SSD requirements), and often providing significant financial support or marketing partnerships that effectively shape the design and exclusivity decisions of major AAA titles.

AAA RPGs prioritize extensive character customization, complex progression systems (skill trees, level grinding), moral choice systems impacting narrative, and a high degree of player control over stats and gear. Action-Adventure games, while often featuring narrative elements, focus more intensely on mechanical precision, environmental traversal, and cinematic presentation rather than deep statistical character management.

Western AAA markets tend to rely heavily on initial full-price purchases combined with paid DLC/Season Passes, while key Asian markets (particularly China and South Korea) favor robust Free-to-Play models supported almost entirely by microtransactions, typically focusing on cosmetic items rather than content gating, due to high sensitivity toward upfront investment.

Increasing regulatory scrutiny, particularly in Europe and parts of Asia, focuses on loot box mechanics, which are being classified in some jurisdictions as forms of gambling due to their random nature. These regulations force publishers to redesign monetization systems to ensure transparency, probability disclosure, or, in some cases, remove these mechanics entirely to comply with local laws and consumer protection acts.

The PC platform is vital because it often serves as the testing ground for the highest graphical fidelity and technological innovation (e.g., advanced GPU features). It also hosts the most intense competitive esports titles and provides the most favorable digital distribution margins for publishers using proprietary launchers, making it a critical segment despite the dominance of console hardware unit sales.

Publishers combat piracy primarily through advanced digital rights management (DRM) software, transitioning critical game elements to server-side processing (essential for GaaS titles), and rapidly issuing legal takedowns. The shift to live-service games, which require persistent online authentication and updates, is naturally the most effective long-term deterrent against unauthorized distribution.

The expectation for cinematic quality—including high-end voice acting, professional motion capture, and Hollywood-level narrative direction—drives up the cost and complexity of development significantly. This emphasis demands cross-industry expertise and tools traditionally reserved for film, further distinguishing AAA titles from standard game releases.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.