ID : MRU_ 443796 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

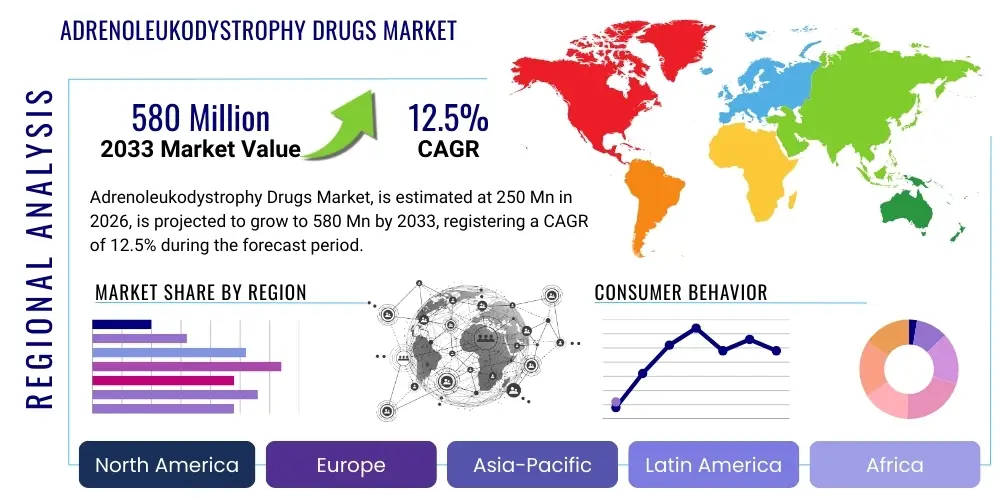

The Adrenoleukodystrophy Drugs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 250 Million in 2026 and is projected to reach USD 580 Million by the end of the forecast period in 2033.

The Adrenoleukodystrophy (ALD) Drugs Market encompasses pharmaceuticals, therapeutic compounds, and gene therapies specifically designed to manage or cure this debilitating, rare, X-linked inherited disorder. ALD is characterized by progressive demyelination in the central nervous system, leading to severe neurological dysfunction, and often involves primary adrenal insufficiency. The disease stems from a pivotal mutation in the ABCD1 gene, which encodes the peroxisomal transporter protein responsible for metabolizing very long-chain fatty acids (VLCFAs). The resultant pathological accumulation of VLCFAs, particularly in the brain and adrenal cortex, triggers chronic neuroinflammation and subsequent irreversible demyelination. The core market drivers include the increasing efficacy and subsequent regulatory approval of advanced genetic therapies, coupled with the global momentum toward implementing comprehensive newborn screening programs that enable crucial early detection before irreversible neurological damage occurs. This proactive approach is fundamental to maximizing the therapeutic benefit of existing and pipeline treatments.

The current landscape features a critical divide between curative intent therapies, primarily hematopoietic stem cell transplantation (HSCT) and ex vivo gene therapy, and supportive care measures, such as corticosteroid replacement for adrenal failure and the nutritional supplement Lorenzo’s Oil. Gene therapy, specifically utilizing lentiviral vectors to introduce a functional copy of the ABCD1 gene into autologous CD34+ hematopoietic stem cells, represents the pinnacle of innovation and a major catalyst for market valuation. The high pricing associated with these specialized, potentially one-time curative treatments significantly impacts the overall market size and growth trajectory. Furthermore, pharmaceutical companies are actively exploring anti-inflammatory agents and small molecules designed to mitigate the underlying immunological response and reduce VLCFA load in patients ineligible for or unresponsive to genetic intervention. The specialization required for diagnosis and treatment positions this market firmly within the ultra-orphan drug category, benefiting significantly from favorable regulatory fast-track pathways and incentives aimed at fostering innovation for rare diseases.

Major applications of ALD drugs are primarily focused on preventing the onset or halting the progression of Cerebral ALD (cALD), the rapidly advancing and often fatal form of the disease typically affecting young boys. Treatments also target the slower, adult-onset form, Adrenomyeloneuropathy (AMN), although therapeutic breakthroughs for AMN are still considered a substantial unmet medical need and a key area for future development. The market benefits substantially from the Orphan Drug Designation status granted by regulatory bodies in major economies, providing crucial incentives such as extended market exclusivity, tax credits, and financial grants, which mitigate the considerable financial risk associated with developing drugs for small patient populations. The collective efforts in clinical research, aiming for less invasive delivery methods and safer conditioning regimens for stem cell delivery, are expected to further broaden the market’s reach and patient eligibility criteria throughout the forecast period of 2026 to 2033, underpinning the high projected Compound Annual Growth Rate.

The Adrenoleukodystrophy Drugs Market exhibits highly dynamic business trends characterized by intense competition and rapid technological advancement within the genetic therapy sector. Key strategic movements include substantial capital investments in manufacturing scalability for highly complex viral vectors and personalized autologous cell processing, as firms transition successfully from clinical development to commercial supply. Financial trends reflect the high-premium pricing model typical of ultra-orphan drugs, necessitating complex payer negotiations and the establishment of sophisticated value-based pricing agreements and outcomes-based reimbursement models to ensure broad market access. Strategic alliances between pioneering academic research centers—the sources of early intellectual property—and commercial pharmaceutical entities are critical for securing pipeline assets and leveraging specialized expertise in rare disease clinical execution. The drive for operational efficiency is particularly focused on optimizing the logistical "vein-to-vein" time for autologous cell therapies to ensure maximum cell viability and patient safety, a crucial operational differentiator in the intensely competitive landscape.

Regionally, North America maintains indisputable market leadership due to its robust healthcare funding, established infrastructure for advanced cellular therapies, and a generally favorable regulatory and reimbursement environment that accommodates the exceptionally high cost of gene therapies. European markets are experiencing moderate but stable growth, balancing high clinical standards with rigorous national health technology assessments (HTA) that often exert downward pressure on pricing points. The greatest potential for rapid expansion resides in the Asia Pacific region, specifically driven by increasing governmental focus on improving rare disease access in countries like Japan, which have well-developed regulatory pathways for regenerative medicine, and expanding diagnostic capabilities in emerging economies such as China and India. These existing regional disparities necessitate tailored market entry strategies, emphasizing infrastructure development and specialized physician education in emerging economies to ensure successful product uptake and safe administration of complex treatments.

Analysis of segment trends shows the Gene Therapy segment dominating revenue generation, directly correlating with the high clinical value and subsequent high cost of these life-changing treatments. The Cerebral ALD (cALD) disease type segment remains the immediate commercial focus because of the profound urgency and clear, demonstrated clinical benefit achieved by genetic interventions when applied early. However, future market growth opportunities are increasingly shifting towards the Adrenomyeloneuropathy (AMN) phenotype, as it represents a larger, though currently underserved, adult patient population seeking sustained symptom management and disease modification. End-users are consolidating into specialized pediatric hospitals and neuroscience centers recognized for expertise in rare genetic disorders and possessing the requisite transplant and cell-processing facilities, making market penetration highly selective and focused on institutional capability rather than broad geographical coverage, thereby concentrating demand.

User inquiries regarding AI's influence on the Adrenoleukodystrophy Drugs Market frequently explore how Artificial Intelligence (AI) and Machine Learning (ML) can effectively overcome the inherent limitations of rare disease research, specifically concerning sparse, heterogeneous patient data and the critical need to shorten diagnostic delays. A major focus is on the capability of AI models to analyze complex phenotypic variations arising from the single ABCD1 gene mutation, linking specific genetic variations to varied clinical outcomes, thereby significantly aiding prognostic assessment—for instance, predicting the critical switch from an asymptomatic state to rapidly progressive cALD. There is also substantial user interest in AI's role in optimizing the design of inherently small-cohort clinical trials, which often struggle with statistical power, efficient patient recruitment, and complex logistical management across multiple global sites, essential for generating robust efficacy data.

Furthermore, AI is viewed as an absolutely essential tool for enhancing diagnostic throughput and ensuring accuracy. By applying sophisticated convolutional neural networks (CNNs) to analyze subtle, early-stage changes in brain MRI scans characteristic of incipient cALD lesions, AI can potentially detect disease progression much earlier than conventional human radiographic assessment. This capability is paramount for determining the narrow, time-sensitive therapeutic window for successful gene therapy administration. The computational analysis of newborn screening data, integrating both biochemical markers and genetic sequencing results, allows for highly efficient and accurate risk stratification of neonates. This capability directly supports commercial strategies by allowing manufacturers to identify high-priority patients requiring immediate specialized intervention, thus significantly driving the market demand for curative drugs and improving overall patient outcomes. Simultaneously, the ethical and regulatory challenges concerning data privacy and potential algorithmic bias when diagnosing vulnerable, rare disease patient populations are emerging concerns that require careful governance as AI deployment becomes routine in rare disease management.

The practical application of AI extends robustly into therapeutic manufacturing and stringent quality control. Machine learning algorithms are being trained to continuously monitor and optimize the intricate cell modification process in gene therapy production, ensuring product consistency, high yield, and high purity of the cellular product—elements absolutely critical to the safety and long-term efficacy of autologous treatments. Moreover, predictive maintenance for specialized cGMP equipment and the optimization of specialized cold chain logistics required for transporting highly sensitive, cryopreserved biological products are additional areas where AI offers tangible operational efficiencies. These technological integrations indirectly reduce overall manufacturing costs and drastically improve the reliability of drug delivery across the specialized, geographically dispersed supply chain inherent to the ALD market, supporting broader global access and sustainability.

The Adrenoleukodystrophy Drugs Market is critically governed by a distinctive set of powerful internal and external forces summarized by key Drivers, Restraints, and Opportunities (DRO) that firmly reflect its status as an ultra-orphan market currently undergoing a rapid technological revolution. Key drivers include the demonstrated high efficacy and expected long-term durability of recently approved gene therapies, offering a functional, potentially one-time cure for early-stage cALD, which dramatically escalates the perceived value and commercial attractiveness of these treatments. Supportive regulatory frameworks globally, such as the U.S. FDA's Regenerative Medicine Advanced Therapy (RMAT) designation and similar programs in Europe, accelerate clinical development and time to market entry. Most significantly, the continuous expansion of mandated newborn screening for ALD in industrialized nations is a monumental driver, ensuring that a greater proportion of patients are identified and treated within the critical window of therapeutic opportunity, thereby maximizing the clinical and commercial success of early intervention strategies. This synergy between advanced science and crucial public health initiatives underpins the high projected market CAGR.

However, the market faces several significant, entrenched restraints that temper overall growth and global accessibility. Paramount among these is the extremely high cost of advanced therapies, which places severe strain on national healthcare budgets and necessitates complex and often protracted negotiations with governmental and private payors regarding highly specific reimbursement terms and risk-sharing payment models. Furthermore, the limited overall prevalence of the disease results in small, geographically dispersed patient populations, making large-scale, international clinical trials exceptionally difficult, time-consuming, and resource-intensive. The non-negotiable requirement for highly specialized infrastructure—including sterile, state-of-the-art cleanrooms, specialized cryogenic storage, and expert multidisciplinary medical teams trained in complex cell transplantation procedures—limits treatment delivery to only a select few specialized medical centers, thereby creating significant logistical and geographical access restraints for many potential patients globally. Manufacturing complexity, particularly ensuring the consistency, high yield, and uncompromising quality control of viral vectors, also presents a substantial and ongoing operational hurdle that impacts supply stability.

The primary opportunities for substantial market expansion involve strategically broadening the therapeutic scope beyond the highly focused pediatric cALD population to effectively address the larger, chronically affected adult population suffering from the debilitating Adrenomyeloneuropathy (AMN) phenotype, for which no definitive disease-modifying therapies currently exist. Developing orally administered small molecules or pursuing less invasive, in vivo gene editing techniques (e.g., direct liver or CNS delivery of gene payloads) represents a substantial commercial opportunity by significantly lowering logistical barriers, potentially simplifying administration, and reducing the total cost of therapy. Moreover, strategic global expansion into promising emerging markets, achieved through technology transfer and localized manufacturing partnerships, can unlock significant untapped patient populations, improving equity of access. The collective impact forces highlight a dynamic market where groundbreaking technological success is now assured, but widespread global adoption relies critically on innovative pricing, sustainable and scalable manufacturing, and coordinated international policy support to ensure equitable access to these specialized, life-saving treatments.

The comprehensive segmentation of the Adrenoleukodystrophy Drugs Market is an essential requirement for detailed strategic planning and market analysis, accurately reflecting the clinical heterogeneity of the disease and the resulting diversity in specialized therapeutic needs. Segmentation by Treatment Type clearly delineates the market into ultra-high-cost curative options (Gene Therapy, AHSCT) and maintenance/supportive modalities (Pharmacological, Dietary Management), providing clear and detailed insights into revenue distribution, technological maturity, and current R&D focus. The most valuable revenue segment remains Gene Therapy due to its transformative clinical potential and high price point, commanding a substantial share of the overall market value. Segmentation by Disease Type, which contrasts the aggressive Cerebral ALD (cALD) with the slower-progressing Adrenomyeloneuropathy (AMN), is pivotal, as cALD intervention drives the immediate high-value market, while AMN represents a chronic, growing unmet medical need for symptomatic and potentially disease-slowing treatments in the future. Accurate market forecasting and resource allocation rely heavily on precise quantification within these distinct therapeutic avenues.

Further delineation by Route of Administration—primarily Intravenous for cell and gene therapies requiring systemic delivery, and Oral for supportive drugs and potentially future small molecule candidates—informs specialized supply chain design and institutional logistics planning. End-User segmentation explicitly emphasizes the market’s reliance on highly Specialized Hospitals and academic centers equipped to handle complex autologous cell manipulation and advanced transplantation protocols. These institutions serve as concentrated points of consumption, requiring highly targeted marketing efforts and bespoke support services from manufacturers, including specialized training and logistical coordination. The regional segmentation is essential for understanding global market maturity, regulatory hurdles, and access barriers, clearly showing the advanced adoption rates in North America versus the promising but challenging emerging potential in the Asia Pacific region. Each segment requires a tailored commercial approach, acknowledging the distinct clinical guidelines, reimbursement complexities, and technological requirements associated with ultra-rare genetic disorders.

The continuous refinement of diagnostic tools, including non-invasive biomarker assays and sophisticated neuroimaging techniques, further influences segmentation accuracy by allowing for earlier and more definitive classification of patients into specific disease categories, thereby streamlining clinical decision-making and optimal treatment selection. The potential future introduction of specific small molecules targeting VLCFA synthesis or transport mechanisms would create an entirely new, potentially broader, and more scalable market segment, especially relevant for the vast, untreated AMN population who often do not meet the strict criteria for or benefit from current cALD-focused gene therapies. Strategic focus across all segments remains rooted in delivering highly personalized medicine, which necessitates detailed patient stratification based on comprehensive genetic and clinical profiles, driving the urgent need for continued investment in integrated diagnostic support alongside therapeutic development and commercialization efforts.

The value chain of the Adrenoleukodystrophy Drugs Market is structurally complex and specifically optimized for the bespoke production and highly controlled delivery of ultra-specialized biological products, differentiating it significantly from conventional pharmaceutical models. Upstream activities commence with intensive and long-term Research and Development, often originating in university labs or small, highly specialized biotechnology firms focusing on genetic engineering, hematology, and virology. This stage is dedicated to designing highly efficient and safe viral vectors (e.g., third-generation lentiviral vectors) capable of stable transduction of the functional ABCD1 gene. Key upstream requirements include the stringent procurement of specialized, high-purity reagents, proprietary cell culture media, and the development of robust, validated assays for consistently measuring product quality and functional potency. This phase demands rigorous intellectual property management and is characterized by high capital expenditure due to the highly customized nature of vector engineering and extensive early-stage toxicology testing, establishing the crucial foundation for the therapy’s effectiveness and long-term safety profile.

Midstream processes center exclusively on sophisticated, highly regulated manufacturing conducted in specialized Current Good Manufacturing Practice (cGMP) facilities. For autologous gene therapy, this intricate process involves apheresis (harvesting the patient's own cells), subsequent cell processing and genetic modification (transduction with the viral vector), cell expansion, and final cryopreservation. This manufacturing stage is intensely complex, demanding strict adherence to personalized, patient-specific protocols, impeccable sterile conditions, and extremely rapid turnaround times to maximize cell viability and integrity. Quality control (QC) is absolutely paramount, encompassing extensive and rapid testing for sterility, residual vector copy number, and functional potency before the product can be cleared for final clinical release. Successfully scaling up this personalized production remains a critical technological and operational challenge, requiring continuous innovation in closed-system automation to efficiently transition from personalized small batches to a commercially viable supply chain while maintaining uncompromising quality standards essential for patient safety.

Downstream activities involve specialized logistics, distribution, and clinical administration, which are tightly interwoven. Due to the inherent fragility and limited shelf stability of the therapeutic cell product, the distribution channel is overwhelmingly Direct (Manufacturer-to-Specialized Treatment Center), relying on highly specialized cold chain management (typically utilizing controlled-rate freezers and liquid nitrogen shippers) to safely transport the cryopreserved, often patient-specific, cells. Clinical administration necessitates highly trained transplant teams, specific clinical site certification, and meticulous post-treatment monitoring to manage conditioning regimens and vigilantly track for potential long-term adverse effects. Market access is heavily influenced by payer negotiation and the creation of comprehensive patient access programs designed to efficiently overcome the significant financial barriers associated with these one-time curative treatments. Indirect channels primarily manage adjunctive supportive drugs, ancillary medical supplies, and preparatory medications, playing a necessary but subsidiary role in the overall patient care pathway. The integration and rigorous oversight across all stages are fundamental to ensuring maximum patient safety and therapeutic success, particularly for fragile biological products targeting a vulnerable, ultra-rare disease population.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 250 Million |

| Market Forecast in 2033 | USD 580 Million |

| Growth Rate | CAGR 12.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | bluebird bio, Shire (now Takeda), Sanofi Genzyme, Novartis, Pfizer, Amicus Therapeutics, Orpheris, Viking Therapeutics, Nutricia Advanced Medical Nutrition, Regeneron Pharmaceuticals, PTC Therapeutics, Orchard Therapeutics, Homology Medicines, Allogene Therapeutics, Voyager Therapeutics, Sangamo Therapeutics, Passage Bio, Genentech (Roche), Biogen, Alexion Pharmaceuticals. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological core of the Adrenoleukodystrophy Drugs Market is situated firmly within advanced genetic manipulation and cellular engineering disciplines. The foundational technology driving current market revenues is the ex vivo gene therapy platform, which relies on high-titer, replication-incompetent lentiviral vectors to efficiently carry the functional ABCD1 gene into a patient’s own hematopoietic stem cells (HSCs). This technology requires highly specialized infrastructure, including stringent biosafety level 2 (BSL-2) containment and precision cell processing to ensure the long-term safety and high efficacy of the transduced cells. Ongoing technological refinement is currently focused on developing more efficient and significantly safer conditioning regimens (the required chemotherapy administered before cell infusion), moving towards less toxic, potentially antibody-based, or targeted conditioning methods to minimize severe long-term side effects and consequently broaden the eligibility of vulnerable pediatric patients. Optimizing the genomic stability and long-term functional expression profile of the integrated gene payload within the HSCs remains a critical technological pursuit to ensure sustained therapeutic benefit.

Emerging technologies promise to reshape the landscape further, particularly through the aggressive introduction of next-generation gene editing systems such as CRISPR/Cas9 and advanced base editing tools. These novel approaches aim to accurately correct the native ABCD1 gene mutation directly within the patient’s cells (both in controlled ex vivo settings and potentially through future in vivo delivery), offering a highly precise alternative to traditional gene addition approaches that rely on semi-random viral integration. This potential shift targets superior efficacy and a significantly reduced risk profile associated with insertion mutagenesis. Additionally, the development of sophisticated diagnostic technologies, including quantitative mass spectrometry-based assays for accurately measuring VLCFAs and their pathological ratios (e.g., C26:0/C22:0), along with advanced molecular imaging techniques (like high-resolution Diffusion Tensor Imaging), allows for highly sensitive, early monitoring of disease progression and precise assessment of therapeutic response, serving as indispensable technological adjuncts to the specialized drug products themselves.

Manufacturing technology represents a significant, non-negotiable area of high investment. The widespread adoption of closed-system automation for cell processing (e.g., integrated systems like CliniMACS Prodigy and specialized bioreactor technologies) is crucial for standardizing production protocols, minimizing human error, and achieving the required scalability and consistency essential for reliable commercial supply. Furthermore, continuous advancements in specialized cryopreservation techniques ensure the long-term stability and optimal viability of the cellular product during intricate transport and prolonged storage, effectively addressing the inherent logistical fragility of the specialized supply chain. Overall, the technological evolution is decisively moving towards increased therapeutic personalization, reduced patient invasiveness, and enhanced manufacturing predictability, firmly positioning the ALD market at the innovative forefront of personalized medicine and ultra-rare genetic disease therapeutics research and development.

North America maintains its dominant share and leadership position in the Adrenoleukodystrophy Drugs Market, primarily fueled by the substantial resources and favorable environment in the United States. This regional supremacy is strongly attributed to several crucial factors: the presence of major biopharmaceutical innovators actively engaged in ALD research, a high concentration of specialized academic medical centers certified to administer complex cell and gene therapies, and an aggressive, state-mandated push for newborn screening for ALD across numerous jurisdictions, ensuring a high rate of essential early diagnosis. The U.S. regulatory environment, particularly the incentives provided by the FDA’s Orphan Drug and RMAT designations, offers significant financial incentives, accelerating clinical trials and subsequent market entry. Furthermore, the robust public and private insurance systems facilitate access to extremely high-cost treatments, despite continuous scrutiny over pricing and reimbursement models, resulting in the highest per-patient expenditure globally for ALD treatments.

Europe constitutes the second most influential market, characterized by comprehensive universal healthcare coverage and a strong, sustained commitment to rare disease research fostered through continent-wide initiatives such as the European Reference Networks (ERNs). Key established markets such as Germany, the UK, and France possess well-developed, specialized medical infrastructure. However, market access is often critically determined by stringent Health Technology Assessment (HTA) evaluations conducted by powerful national bodies (e.g., NICE in the UK, IQWiG in Germany). These assessments focus intensely on long-term clinical data and demonstrable cost-effectiveness, leading to variable and sometimes protracted pricing and reimbursement timelines across the continent. While the adoption rate of gene therapies is generally high once approval is secured, the commercial environment mandates a nuanced, country-specific strategy addressing multiple national payer systems, unlike the relatively unified North American commercial landscape.

The Asia Pacific (APAC) region is convincingly forecasted to exhibit the highest rate of market growth, driven by fundamental improvements in diagnostic accuracy, rapidly rising healthcare expenditure, and increasing governmental willingness to actively address unmet medical needs in rare diseases. Japan is a significant, early market leader within APAC, benefiting from supportive regulatory schemes for regenerative medicine, which successfully attracts early clinical trials and commercialization efforts. While initial adoption rates of advanced therapies remain lower in vast countries like China and India due to underlying infrastructure limitations and fragmented healthcare access, awareness campaigns and strategic partnerships aimed at localizing manufacturing and delivery expertise are beginning to unlock this region’s vast, potential patient base. Latin America and the Middle East & Africa (MEA) represent challenging but strategically crucial future markets, where accessibility is currently heavily reliant on philanthropy, international humanitarian aid, and highly specific government tenders to secure access to these life-altering but resource-intensive therapies.

The primary driver is the successful commercialization and regulatory approval of curative gene therapies, such as lentiviral vector-based treatments, which offer definitive genetic correction for early-stage Cerebral ALD (cALD), coupled with the expansion of mandatory newborn screening programs facilitating essential timely intervention.

Newborn screening programs are critical because they ensure the early, pre-symptomatic identification of ALD patients. This early detection is essential, as the therapeutic window for high-efficacy treatments (like gene therapy or AHSCT) is narrow, thereby significantly expanding the eligible patient pool and maximizing clinical benefit for manufacturers.

Current main therapeutic options include advanced ex vivo gene therapy (for eligible cALD patients), allogeneic Hematopoietic Stem Cell Transplantation (AHSCT), and necessary supportive pharmacological management, including corticosteroid replacement for adrenal insufficiency and essential dietary interventions like Lorenzo's Oil.

North America dominates the ALD drugs market due to its advanced, specialized healthcare infrastructure, high research investment capacity, strong favorable regulatory support (Orphan Drug Designation), and established reimbursement mechanisms that facilitate patient access to expensive, specialized genetic treatments.

The extremely high list price of sophisticated gene therapies, often coupled with complex reimbursement processes and the need for highly specialized institutional infrastructure for administration, poses the most significant restraint, severely limiting global accessibility and widespread adoption across diverse healthcare systems.

The treatment strategy for cALD (Cerebral ALD) focuses urgently on curative intervention via gene therapy or AHSCT to halt rapid, fatal neurodegeneration. In contrast, AMN (Adrenomyeloneuropathy) management currently relies primarily on symptomatic and supportive care, as effective disease-modifying therapies for the larger adult-onset phenotype remain a major, persistent unmet medical need.

The ALD drug value chain is characterized by highly specialized, personalized upstream manufacturing (viral vector production and autologous cell manipulation), necessitating stringent cold-chain logistics and a predominantly direct distribution model to expert treatment centers, unlike the mass production and broad distribution networks of conventional small-molecule drugs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.