ID : MRU_ 443841 | Date : Feb, 2026 | Pages : 257 | Region : Global | Publisher : MRU

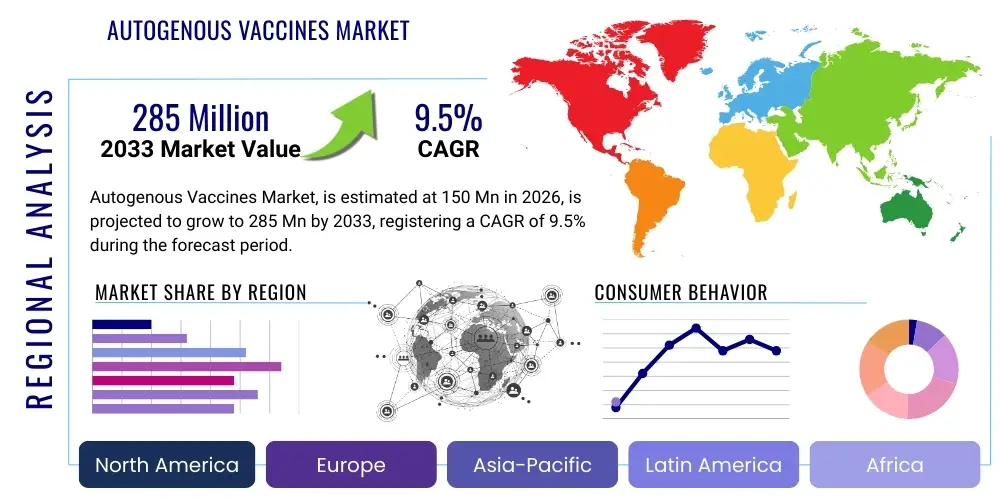

The Autogenous Vaccines Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 150 Million in 2026 and is projected to reach USD 285 Million by the end of the forecast period in 2033. This robust expansion is primarily driven by the increasing global prevalence of highly specific, localized bacterial and viral pathogens in livestock populations, demanding tailored immunological solutions that conventional commercial vaccines often fail to address effectively.

The Autogenous Vaccines Market encompasses the development, production, and distribution of vaccines derived from pathogens isolated directly from an infected animal or herd within a specific geographical location. These vaccines, also known as herd-specific or farm-specific vaccines, are crucial tools in veterinary medicine, particularly in intensive farming settings where rapid mutation and high disease pressure necessitate immediate, customized immunological intervention. The primary product offering involves inactivating the isolated pathogen and formulating a sterile vaccine designed to elicit a specific immune response solely within the source population, ensuring maximal relevance and efficacy against the circulating strain.

Major applications of autogenous vaccines span large-scale livestock operations, including poultry, swine, and cattle, where they are utilized for proactive disease control, outbreak management, and mitigation of antimicrobial resistance (AMR). They are particularly effective against difficult-to-treat chronic or recurring infections, such as those caused by variant strains of Pasteurella multocida, E. coli, or specialized viral agents that have evaded broad-spectrum commercial vaccine coverage. The inherent flexibility and rapid development timeline associated with autogenous solutions provide a distinct advantage over the lengthy regulatory and manufacturing processes required for traditional commercial vaccines, making them indispensable in managing emerging or localized animal health crises.

The market is primarily driven by escalating livestock populations globally, coupled with the imperative to enhance animal welfare and productivity while reducing reliance on antibiotics. Key benefits include superior antigenic matching, reduced risk of vaccine failure due to strain variability, and the ability to target multiple serotypes simultaneously in a single formulation. Furthermore, governmental and industry initiatives promoting responsible antimicrobial stewardship are bolstering the demand for preventive, highly effective, non-antibiotic solutions like autogenous vaccines, positioning them as critical components of modern biosecurity protocols and sustainable agriculture practices worldwide, thereby ensuring market resilience and growth.

The Autogenous Vaccines Market is characterized by sustained growth, fueled by the accelerating trend toward precision veterinary medicine and the rising complexity of infectious diseases in large animal populations. Business trends indicate a movement towards vertical integration among specialized vaccine manufacturers and diagnostic laboratories, aiming to shorten the turnaround time from pathogen isolation to vaccine delivery, a critical factor for farm profitability. Furthermore, strategic partnerships focusing on advanced sequencing technologies are emerging, enabling manufacturers to characterize pathogens rapidly and refine vaccine composition for optimal protection. The market structure remains competitive, with regional specialists holding significant influence due to localized regulatory requirements and the need for rapid service delivery, challenging the dominance of global animal health giants.

Regionally, North America and Europe maintain leading positions, primarily due to well-established regulatory frameworks, significant investments in advanced diagnostics, and high adoption rates of intensive animal farming practices where biosecurity is paramount. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth, driven by the massive expansion of its swine and poultry sectors, increasing consumer awareness regarding food safety, and governmental efforts in countries like China and India to modernize livestock production and control zoonotic diseases. Regulatory harmonization and easing of importation restrictions across various regions present both opportunities and challenges for cross-border vaccine provision, reshaping regional market dynamics.

Segment trends reveal that the Swine and Poultry segments currently dominate the market volume, largely due to the high density of animals and the rapid spread of viral and bacterial diseases like Porcine Reproductive and Respiratory Syndrome (PRRS) variants and avian influenza strains. The Bacterial Disease segment leads the market based on disease type, reflecting the chronic nature and high economic impact of bacterial infections in livestock. Application-wise, veterinary hospitals and large commercial farms remain the primary end-users, increasingly demanding multi-valent formulations that address complex co-infections efficiently. Future growth is expected to be catalyzed by the expansion into the aquaculture sector, where highly specific pathogens pose substantial economic threats and autogenous vaccines offer tailored solutions.

Common user questions regarding AI's influence on the Autogenous Vaccines Market often revolve around how artificial intelligence can accelerate pathogen identification, optimize antigen selection, and predict disease outbreaks, thereby enhancing the speed and efficacy of custom vaccine development. Users are keen to understand the shift from traditional laboratory processes to data-driven decision-making, asking if AI can significantly reduce the costs associated with strain isolation and safety testing. Key themes include the potential for AI algorithms to correlate epidemiological data with genomic sequencing results, allowing for proactive vaccine formulation adjustments and minimizing the lead time required for outbreak response. There is significant concern about data privacy, proprietary strain information, and the regulatory challenges associated with using AI-generated insights for pharmaceutical production, balanced against the expectation that AI integration will ultimately lead to higher quality, more rapidly deployable, and antigenically superior autogenous vaccines.

AI's role is transformative, primarily by streamlining the initial diagnostic and development phases. Machine learning algorithms are already being deployed to analyze vast datasets comprising pathogen genomic sequences, clinical efficacy data, and immunological profiles. This analysis enables the identification of conserved or highly immunogenic epitopes much faster than traditional methods, optimizing the selection of the most relevant antigen components for the final vaccine formulation. Furthermore, AI-powered predictive models are used in large commercial farms to forecast potential outbreaks based on environmental factors, feed patterns, and animal health metrics, allowing veterinarians and farmers to commission autogenous vaccines proactively before a severe outbreak takes hold, drastically improving biosecurity and reducing economic losses. The precision offered by AI minimizes the risk of antigenic drift mismatch, ensuring the resultant autogenous vaccine provides maximum protective immunity.

The application of deep learning in vaccine safety and stability testing also represents a major enhancement. AI can model complex interactions between the antigen, adjuvant, and delivery system, predicting potential adverse reactions or stability issues during manufacturing and storage, thereby improving overall product quality and regulatory compliance. While full regulatory integration of AI-driven design requires robust validation, the immediate impact is seen in operational efficiency, quality control, and the ability to handle the increasing volume and complexity of pathogen data generated through advanced molecular diagnostics. This enhanced speed and precision solidify AI as a critical technological pillar supporting the future expansion and efficacy of customized autogenous immunization strategies globally.

The Autogenous Vaccines Market is profoundly influenced by a complex set of drivers, restraints, opportunities, and their collective impact forces, shaping its trajectory toward specialized veterinary care. A key driver is the relentless evolution and emergence of highly virulent, localized strains of pathogens in concentrated animal feeding operations (CAFOs), which render standardized commercial vaccines ineffective, creating a necessity for customized, rapid-response solutions. This necessity is further amplified by global regulatory pressures and industry mandates to reduce the prophylactic use of antibiotics, positioning prophylactic autogenous vaccines as a primary tool in antimicrobial stewardship programs. However, market growth faces inherent restraints, most notably the complex and fragmented regulatory landscape, which varies significantly by country, making international distribution and standardization challenging. The high initial cost associated with customized development, stringent quality assurance requirements, and the need for highly specialized laboratory infrastructure also act as barriers to entry and adoption in resource-limited regions.

The primary opportunity lies in the untapped potential of autogenous vaccines in emerging livestock sectors, such as aquaculture (fish and shrimp farming), where specific localized pathogens pose severe economic threats and few commercial vaccines are available. Furthermore, the increasing acceptance of personalized medicine principles in companion animal health represents a niche but high-value opportunity. The convergence of advanced molecular diagnostics, genomics, and rapid manufacturing techniques (like next-generation sequencing coupled with bioinformatics) provides manufacturers with the technological capability to exploit these opportunities effectively, ensuring faster turnaround times and superior antigenic matching, which are critical competitive advantages in this sector. These technological advancements simultaneously address some of the cost and time restraints, creating a positive feedback loop for market innovation and penetration.

The impact forces generated by these DRO elements are substantial, pushing the market toward greater specialization and localized expertise. The dominant impact force is the necessity for rapid response and antigenic specificity. Unlike traditional pharmaceuticals, the timeliness of the autogenous vaccine delivery often dictates its success in controlling an outbreak; therefore, companies investing in decentralized production networks and rapid diagnostic capabilities will capture greater market share. The continuous pressure from antimicrobial resistance (AMR) acts as a powerful external force, compelling stakeholders—from farmers to regulators—to prioritize non-antibiotic preventative measures, thereby cementing autogenous vaccines as an essential component of modern sustainable livestock production protocols. Ultimately, the balancing act between stringent quality control (restraint) and the speed required for epidemic control (driver) will define the competitive environment and technological investment priorities within the market over the forecast period.

The Autogenous Vaccines Market is systematically segmented based on Animal Type, Disease Type, and Application, reflecting the highly specialized nature of the product and its targeted use in veterinary medicine. This segmentation is crucial for understanding the market's dynamics, as demand and growth rates vary significantly depending on the concentration of livestock, regulatory environment, and prevalent endemic diseases within each segment. The detailed segmentation analysis provides strategic insights for market participants regarding key investment areas, pipeline development focus, and geographical expansion strategies. The specificity of autogenous vaccines means that success is intrinsically linked to understanding the epidemiological needs of each animal type and region, necessitating tailored marketing and distribution approaches.

The segmentation by Animal Type—encompassing Poultry, Swine, Cattle, and Companion Animals—highlights the economic weight of commercial livestock, which dominates demand due to intense farming practices and the associated high risk of rapid disease transmission. Swine and Poultry collectively represent the largest share, driven by short production cycles and constant disease pressure. Disease Type segmentation distinguishes between Bacterial, Viral, and Parasitic infections; currently, bacterial diseases command the majority of the market due to the chronic nature of many livestock bacterial pathogens and the effectiveness of autogenous bacterins. Finally, the Application segmentation differentiates between demand originating from Veterinary Hospitals, large commercial Farms, and specialized Research Institutes, with commercial farms being the primary consumers due to their immediate need for herd-specific solutions.

Analyzing these segments reveals a trend toward higher growth in the Swine segment, correlating with global protein demand and the necessity to control high-impact diseases such as PRRS and swine influenza variants. Furthermore, the viral disease segment is expected to show accelerated growth as advanced diagnostic tools improve the identification of novel viral strains suitable for autogenous vaccine production. Strategic focus on developing multi-valent formulations that address common co-infections across these segments offers manufacturers a competitive edge, streamlining prophylactic programs for end-users and improving overall farm efficiency and animal health outcomes.

The value chain for the Autogenous Vaccines Market begins with crucial upstream activities, centered on pathogen isolation and characterization, primarily performed by specialized veterinary diagnostic laboratories or dedicated research facilities. This upstream segment is highly dependent on effective sample collection from infected animals in the field and the rapid, accurate identification of the causative agent, often requiring advanced molecular diagnostics like PCR and Next-Generation Sequencing (NGS). The efficiency of this initial phase—the speed and precision of isolation and identification—directly dictates the responsiveness and efficacy of the entire value chain. Key suppliers in this phase include providers of diagnostic kits, sequencing hardware, and specialized culture media, all of which must meet stringent quality and biosecurity standards to ensure the viability and purity of the isolated pathogen intended for vaccine development.

The midstream portion involves the highly regulated manufacturing process, where the isolated pathogen is cultured, inactivated (often using chemical or thermal methods), purified, and formulated with appropriate adjuvants to enhance the immune response. Unlike commercial vaccine manufacturing, which relies on large, standardized batches, autogenous manufacturing involves smaller, customized batch runs, demanding flexible, high-containment production facilities. Quality control and regulatory compliance are paramount in this stage, ensuring sterility, safety, and potency of the final product before release. Leading manufacturers often integrate diagnostic capabilities directly into their operational structure to maintain seamless control over the entire development lifecycle, optimizing the transition from isolated strain to finalized product.

Downstream activities involve the distribution and application of the finalized vaccine. Due to the requirement for specific cold chain management and prompt delivery, the distribution channel is typically direct or semi-direct, bypassing large-scale pharmaceutical wholesalers. Direct distribution involves the manufacturer shipping the vaccine directly to the prescribing veterinarian or the commercial farm. Indirect channels sometimes utilize specialized regional veterinary distributors who manage localized cold chain logistics and regulatory paperwork. The end-user uptake and successful application are highly dependent on the prescribing veterinarian’s expertise in farm biosecurity, disease epidemiology, and immunization schedules, making technical support and veterinary consultation essential components of the downstream service offering, which closes the feedback loop for future strain updates.

The primary customers for the Autogenous Vaccines Market are entities involved in large-scale animal production where infectious disease pressure poses significant economic risk and requires highly specific preventative measures. This includes large commercial livestock producers across the swine, poultry, and cattle industries, often operating concentrated animal feeding operations (CAFOs). These large farms are frequent buyers because they face recurring endemic diseases caused by localized strains that have developed resistance or variability against standard market-available vaccines, making the highly specific nature of autogenous vaccines essential for maintaining herd health and profitability. Their purchasing decision is driven by economic factors (reduced mortality and morbidity) and regulatory compliance regarding antimicrobial usage.

Another crucial customer segment is specialized veterinary practices and diagnostic centers that service these intensive livestock operations. These veterinarians act as gatekeepers, identifying the need for an autogenous solution, collecting the required samples, and prescribing the finalized product. They require manufacturers who offer fast turnaround times, robust diagnostic support, and reliable formulation quality. Furthermore, governmental or non-governmental organizations involved in public health and agricultural development, particularly those managing large-scale disease eradication or control programs, represent institutional buyers, utilizing autogenous vaccines to control widespread, localized outbreaks quickly before they become zoonotic threats or catastrophic economic events.

Emerging potential customer segments include high-value animal sectors such as aquaculture facilities (fish and shrimp farms), which are increasingly susceptible to highly specific bacterial and viral pathogens unique to their aquatic environment, and the companion animal market, though smaller in volume, demands autogenous solutions for complex, chronic infections that fail to respond to standard treatments. These diverse end-users require a manufacturer capable of meeting variable volume demands, maintaining rigorous quality standards, and providing specialized consultative services tailored to the specific immunological challenges faced by their animal population.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 150 Million |

| Market Forecast in 2033 | USD 285 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Ceva Santé Animale, Elanco, Merck Animal Health, Zoetis, Boehringer Ingelheim, Phibro Animal Health Corporation, Colorado Serum Company, Newport Laboratories, Epitopix LLC, Vaxxinova, IDT Biologika, Biogenesis Bago, Bio-Vet, Harris Vaccines, Customized Vaccines, Huvepharma, Hipra, Dechra Pharmaceuticals, Virbac, Hester Biosciences |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Autogenous Vaccines Market is characterized by the convergence of advanced molecular diagnostics and sophisticated microbial culturing techniques, crucial for reducing the development cycle and ensuring high antigenic specificity. Key enabling technologies include Next-Generation Sequencing (NGS) and whole-genome sequencing, which allow manufacturers to rapidly map the genetic makeup of an isolated pathogen, identifying key virulence factors and crucial antigenic variation points. This genomic information is essential for validating the need for an autogenous solution over a commercial one and optimizing the selection of antigen components, moving beyond traditional serotyping methods to achieve true precision targeting. The rapid utilization of sequencing data is a major competitive differentiator, directly impacting the speed of response during an animal disease outbreak.

Furthermore, advancements in high-throughput culturing and fermentation technologies are essential for the efficient and safe production of large, high-quality batches of the isolated pathogen biomass under strict containment protocols. Modern bioreactors and continuous culture systems ensure optimal yield and consistency, which, while challenging for small, unique batches, are critical for maintaining economic viability. The development and testing of novel adjuvants—substances added to the vaccine to boost the immune response—also represent a significant technological frontier. Companies are exploring personalized adjuvant selection tailored to the specific animal species and the nature of the infection (bacterial vs. viral) to maximize immunogenicity while minimizing local reactions at the injection site, thereby enhancing the vaccine's overall safety profile and user acceptance.

Finally, data management and bioinformatics play a vital role, acting as the bridge between raw genomic data and final formulation design. Sophisticated bioinformatics platforms are used to manage large databases of circulating strains, track epidemiological trends, and provide decision support for regulatory compliance and batch release. The integration of these digital tools facilitates better traceability and post-market surveillance, which are increasingly demanded by regulatory bodies. The technological focus remains centered on enhancing speed, improving the correlation between the field strain and the vaccine antigen, and ensuring the absolute sterility and stability of these highly customized biological products throughout their short shelf life.

North America currently holds a significant share of the Autogenous Vaccines Market, attributed to the presence of large-scale, highly industrialized animal farming sectors, particularly in the US and Canada. The region benefits from stringent biosecurity standards, high veterinarian adoption rates of advanced diagnostic tools, and supportive regulatory pathways (such as the USDA licensing process) that specifically cater to autogenous products. High capital investment in research and development, coupled with a dense network of specialized veterinary diagnostic laboratories, allows for rapid strain identification and quick vaccine turnaround times, which are critical for producers managing costly outbreaks of diseases like Porcine Epidemic Diarrhea virus (PEDV) variants and Bovine Respiratory Disease complex (BRDC).

Europe also represents a mature and vital market, driven by powerful regulatory initiatives focused on animal welfare and, critically, the stringent reduction of antibiotics under frameworks like the European Green Deal and related Farm-to-Fork strategies. European producers are heavily incentivized to adopt preventative measures like autogenous vaccines to comply with strict antimicrobial resistance (AMR) targets. Countries like Germany, the Netherlands, and France, with robust livestock sectors and a strong tradition of customized veterinary solutions, lead the adoption. The European market, however, is characterized by greater regulatory fragmentation compared to the US, requiring manufacturers to navigate differing national standards, although efforts are continuously underway to streamline processes across the EU.

The Asia Pacific (APAC) region is projected to be the fastest-growing market segment, fueled by rapid modernization and scale-up of swine and poultry production, particularly in China, India, and Southeast Asia. These regions face immense challenges from localized, rapidly mutating diseases and substantial pressure to improve food safety and reduce zoonotic risk. While initial adoption was slower, increasing awareness among local farmers, coupled with substantial government investments in animal health infrastructure and cold chain logistics, is driving exponential growth. Latin America, particularly Brazil and Argentina, also shows strong potential, driven by their massive cattle and poultry export industries, requiring high biosecurity to maintain international trade standards and control endemic diseases like Foot-and-Mouth Disease variants.

The primary difference is specificity and origin. Autogenous vaccines are custom-made from pathogens isolated directly from an infected animal or herd on a specific premise, targeting only the circulating localized strain. Commercial vaccines are mass-produced from standardized, generally accepted strains, offering broad, but sometimes less precise, protection across various regions and herds. Autogenous solutions are used for specific, localized outbreaks or strains resistant to commercial alternatives, offering superior antigenic matching and faster development time for emergent threats.

Yes, autogenous vaccines are rigorously regulated, although the specific regulatory path differs significantly from fully licensed commercial biologics. In most major markets, they are regulated under special veterinary provisions (e.g., USDA in the US or national competent authorities in Europe) ensuring stringent quality control, safety testing, and potency validation before release. They must be manufactured in licensed facilities adhering to Good Manufacturing Practices (GMP). Safety is generally considered high because they are highly specific and contain only inactivated pathogens, minimizing the risk of adverse systemic reactions when used correctly within the originating herd.

The turnaround time for autogenous vaccine production is significantly shorter than for commercial vaccines, typically ranging from 4 to 8 weeks from the time of pathogen submission to final product delivery. This timeframe is dependent on the speed of pathogen isolation, successful growth in culture, inactivation, and mandatory quality control testing. Advanced technologies like Next-Generation Sequencing (NGS) and efficient logistics are constantly being employed by manufacturers to push this time frame lower, especially during severe outbreaks where rapid intervention is critical for livestock survival and farm profitability.

The largest consumers of autogenous vaccines are the high-density livestock sectors, specifically Swine and Poultry, followed closely by Cattle operations. This dominance is due to the intense nature of these farming systems, which leads to high transmission rates and rapid mutation of endemic pathogens. Swine and Poultry farmers frequently require tailored solutions to combat strain variants of viral diseases (like PRRS in swine) and pervasive bacterial infections, making the economics of customized prevention highly favorable compared to the high cost of treatment or mortality.

The adoption of autogenous vaccines is strongly linked to global efforts to combat Antimicrobial Resistance (AMR). By providing a highly effective, preventative immunological solution targeted precisely at the circulating pathogen, autogenous vaccines reduce the necessity for therapeutic and prophylactic use of antibiotics in livestock. Governments and industry bodies increasingly view these customized vaccines as critical tools in antimicrobial stewardship programs, allowing producers to maintain animal health and productivity while adhering to strict guidelines aimed at reducing the overall usage and reliance on veterinary antimicrobial drugs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.