ID : MRU_ 443719 | Date : Feb, 2026 | Pages : 245 | Region : Global | Publisher : MRU

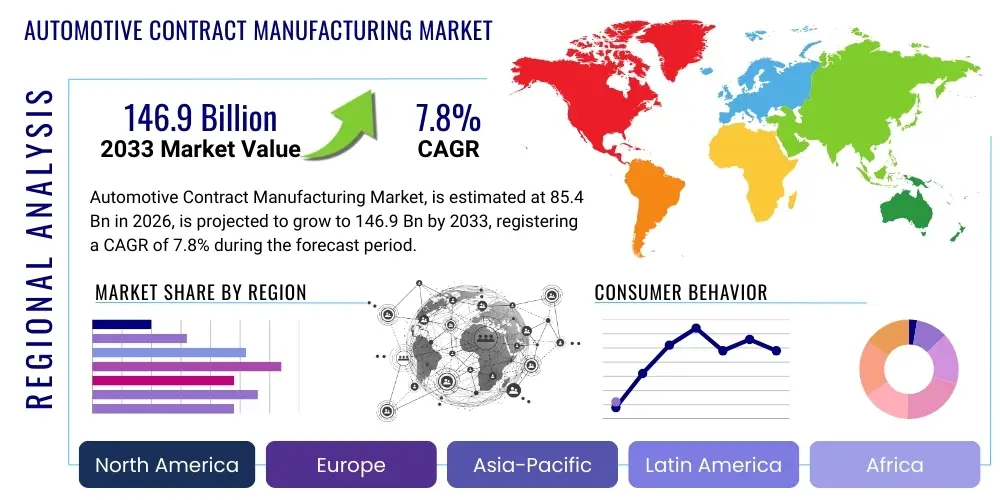

The Automotive Contract Manufacturing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $85.4 Billion in 2026 and is projected to reach $146.9 Billion by the end of the forecast period in 2033. This robust expansion is fueled by Original Equipment Manufacturers (OEMs) increasingly prioritizing core competencies such as branding and software development, leading to the strategic outsourcing of complex manufacturing processes, particularly in highly specialized component areas like advanced driver-assistance systems (ADAS) and electric vehicle (EV) battery packs. Economic pressures related to scaling production in diverse geographic locations, coupled with the necessity for highly flexible supply chains capable of navigating geopolitical instability, further solidify the reliance on specialized contract manufacturing partners who can provide agility and cost efficiency at scale. The transition towards electrification and connectivity demands significant capital investment in novel production techniques, making outsourcing an attractive proposition for mitigating risk.

The Automotive Contract Manufacturing (ACM) market encompasses the outsourcing of various stages of vehicle production, including design, engineering, component fabrication, sub-assembly, and sometimes full vehicle assembly, to third-party specialist manufacturers. This critical industry allows OEMs to leverage external expertise, optimize operational costs, and accelerate time-to-market for new models, particularly crucial in the fast-evolving landscape defined by electric vehicles (EVs) and autonomous driving technologies. The core product description involves providing high-precision manufacturing services for components ranging from basic body parts and interior systems to complex electronic control units (ECUs) and integrated power electronics. Major applications span across passenger vehicles, commercial vehicles, and specialty vehicles, where contract manufacturers manage large-volume production runs and specialized low-volume niche projects simultaneously. Key benefits derived from utilizing ACM include improved scalability, access to specialized technological capabilities without internal investment, robust quality assurance via stringent global standards compliance, and substantial capital expenditure avoidance. Driving factors for market growth include the global push for vehicle lightweighting using advanced materials, the complexity introduced by vehicle connectivity (V2X), and the need for scalable battery manufacturing solutions for the burgeoning EV sector, all of which necessitate specialized manufacturing partners.

The Automotive Contract Manufacturing Market is undergoing transformative growth characterized by profound shifts in business models and technological adoption. Current business trends indicate a significant consolidation among top-tier contract manufacturers, who are expanding their capabilities to offer end-to-end services, moving beyond simple fabrication to include advanced design engineering, software integration, and full lifecycle management, thereby creating deep strategic partnerships with OEMs. Financially, manufacturers are seeing improved profit margins due to high automation levels and efficient material sourcing capabilities, particularly those specializing in EV-related components like high-voltage wiring harnesses and thermal management systems, reflecting a premium placed on specialized technical expertise. Regionally, the market is highly dynamic; while Asia Pacific maintains its dominance as a high-volume production hub driven by favorable labor costs and established supply chain infrastructure, North America and Europe are experiencing rapid growth primarily in high-value, high-complexity sectors such as ADAS sensors and specialized EV platforms, fueled by stringent regulatory requirements and the aggressive pursuit of automotive innovation. Segment trends highlight an accelerating shift from traditional internal combustion engine (ICE) component manufacturing towards electronics, battery components, and complex modular assemblies, with the Electrical & Electronics segment projected to exhibit the fastest CAGR, underscoring the automotive industry’s ongoing transition from mechanical engineering focus to software and electrical systems dominance.

Common user questions regarding AI's impact on Automotive Contract Manufacturing center primarily on operational efficiency, quality control transformation, and supply chain resilience. Users frequently inquire about how AI can optimize complex production schedules involving numerous SKUs, minimize defects in high-tolerance manufacturing environments (especially critical for EV components), and predict equipment failures before they occur, thus avoiding costly downtime. There is also significant interest in AI's role in autonomous quality inspection systems, which ensure compliance with increasingly rigorous global standards, and how machine learning algorithms can stabilize volatile supply chains by forecasting material needs and geopolitical risks more accurately than traditional models. The consensus expectation is that AI integration will fundamentally shift the competitive landscape, creating a clear performance gap between manufacturers who successfully implement smart factory concepts and those who rely solely on conventional automation, ultimately driving down operational costs while simultaneously elevating production quality and flexibility, addressing the urgent market demand for personalized, customizable vehicle architectures manufactured efficiently.

The integration of Artificial intelligence (AI) and Machine Learning (ML) algorithms is rapidly transitioning the automotive contract manufacturing environment into a highly predictive and self-optimizing ecosystem. AI applications are revolutionizing shop floor management by enabling real-time process control, optimizing tool wear and tear, and facilitating dynamic adjustments to robotic path planning, which is essential for maintaining geometric accuracy in component production. Furthermore, the application of deep learning in vision systems allows for non-contact, high-speed inspection of complex assemblies, catching micron-level defects that human inspectors or traditional machine vision systems often miss, leading to unprecedented levels of zero-defect manufacturing capabilities. This technological leap is critical for safety-critical components such as braking systems and steering racks, enhancing overall product liability and reducing recall risks for OEMs. The ongoing necessity for manufacturers to produce highly customizable vehicle platforms necessitates agile production lines, a capability significantly augmented by AI-driven resource allocation and production scheduling optimization.

The Automotive Contract Manufacturing market is shaped by a confluence of powerful drivers (D), significant restraints (R), and compelling opportunities (O), whose interactive dynamics constitute the primary impact forces influencing strategic decision-making and market trajectory. Key drivers include the accelerated global shift towards Electric Vehicles (EVs) requiring massive capacity expansion for battery systems and power electronics, and the rising complexity of vehicle architecture due to Advanced Driver-Assistance Systems (ADAS) integration, compelling OEMs to outsource specialized manufacturing. Restraints, conversely, involve the high initial capital expenditure required for adopting specialized manufacturing technologies (e.g., Gigafactory setups for battery components), intellectual property (IP) protection concerns when sharing proprietary designs with third parties, and the persistent challenge of maintaining consistent quality across dispersed global manufacturing sites. Opportunities are vast, primarily centered on offering end-to-end integration services for modular EV platforms, specializing in sustainable manufacturing practices (green contracts), and expanding presence in emerging automotive markets like Southeast Asia and Eastern Europe. These elements interact forcefully; for instance, the opportunity presented by EV growth simultaneously acts as a driver for specialized outsourcing but imposes a restraint due to the immense investment required for new battery manufacturing capabilities, pushing smaller contractors into consolidation or niche specialization. The overall impact force is overwhelmingly positive, driven by technological evolution and OEMs' strategic necessity to remain capital-light and technologically agile in a period of rapid industry transformation.

The transition toward autonomous driving mandates contract manufacturers to acquire expertise in producing highly sensitive and accurate sensor components, LiDAR systems, and complex computing platforms, which elevates the competitive entry barrier but simultaneously drives market value. Furthermore, global regulatory pressures concerning emissions and safety standards push OEMs to adopt advanced lightweighting techniques using materials such as carbon fiber composites and high-strength aluminum alloys. Contract manufacturers specializing in processing these complex materials gain a distinct market advantage. However, this driver is restrained by the volatile pricing of raw materials, particularly lithium and nickel required for EV batteries, introducing an element of cost instability into long-term contracts. The requirement for zero-defect production in safety-critical systems, exacerbated by the integration of complex software and hardware, necessitates continuous investment in automated inspection and digital twin technologies, which is a major expense acting as a restraint for smaller market participants who cannot afford the continuous upgrade cycle required to stay competitive in this high-tech outsourcing environment.

A significant opportunity lies in the burgeoning aftermarket and service component sector, where contract manufacturers can provide optimized, small-batch production for legacy parts or specialized vehicle variants, leveraging advanced 3D printing and additive manufacturing technologies to meet customized demands efficiently. This contrasts with the primary manufacturing challenge of achieving economies of scale in high-volume production. Geopolitical tensions represent a critical, overarching impact force; as OEMs seek to regionalize supply chains to mitigate risks associated with cross-border dependence, contract manufacturers with strategically located facilities across North America, Europe, and Asia are uniquely positioned to capture these localized manufacturing contracts. The demand for sustainable manufacturing, including water conservation, waste reduction, and the use of renewable energy in production processes, is transforming from a regulatory burden into a crucial competitive opportunity, enabling contract manufacturers who invest in green technologies to secure contracts with environmentally conscious global OEMs who are increasingly focused on reducing Scope 3 emissions across their value chain.

The Automotive Contract Manufacturing Market is systematically segmented based on Component Type, Service Offered, Application (Vehicle Type), and Geographic Region, providing a granular view of specific market dynamics and growth pockets. The segmentation highlights the evolving nature of automotive outsourcing, moving from traditional mechanical parts to complex electronic modules and integrated software components, reflecting the ongoing digital revolution within the industry. Component Type segmentation, covering powertrain, chassis, interior, and electrical/electronics, is particularly relevant as it tracks the shift in manufacturing focus toward high-value EV components. Service Offered segmentation categorizes activities from design and prototyping to mass production and post-assembly logistics, allowing analysis of value-added services. The robust growth projections within the Electrical & Electronics segment underscore the criticality of specialized expertise in producing sensors, control units, and advanced display systems, which demand high precision and stringent testing protocols typically beyond the capacity of general manufacturers.

The increasing modularity of EV platforms, such as skateboard architectures, provides a substantial segmentation opportunity for contract manufacturers specializing in large, complex sub-assemblies. This strategic focus allows them to manage multi-tiered supplier integration and deliver complete modules ready for final vehicle assembly by the OEM, enhancing efficiency and reducing the OEM's logistical burden. Furthermore, the Service Offered category is seeing strong differentiation, with providers increasingly offering comprehensive product lifecycle management services, including design validation, testing for cyber security compliance in connected car features, and end-of-life recycling planning, establishing deeper, more long-term contractual relationships with automotive giants. Understanding these segmented demands is essential for market participants seeking to optimize their technological investments and operational footprint to align with the fastest-growing and highest-margin opportunities available in the highly competitive global automotive supply chain.

The value chain for Automotive Contract Manufacturing is characterized by a complex, multi-tiered structure beginning with raw material extraction and culminating in the delivery of finished components or modules to the OEM assembly line. Upstream activities involve securing foundational materials such as specialty steels, aluminum, polymers, and critical battery materials (lithium, cobalt, nickel). Efficiency at this stage is crucial, as volatile commodity prices directly influence contract profitability. Tier 2 and Tier 3 suppliers, often specialized in processes like deep drawing, specialized coatings, or electronic substrate production, transform these raw materials into basic inputs. Successful upstream management requires robust supplier relationship management (SRM), stringent quality control audits, and effective hedging strategies against material price fluctuations, ensuring a continuous flow of high-quality feedstock necessary for precision manufacturing operations.

The core midstream segment is occupied by the contract manufacturer (CM) itself, representing the highest value addition stage. Here, sophisticated processes such as robotic welding, advanced die casting, intricate PCB assembly, and complex systems integration take place. CMs invest heavily in industrial automation, specialized tooling, and smart factory technologies (IoT, AI) to maximize operational throughput and meet the exacting quality standards mandated by OEMs. This stage involves deep collaboration with the OEM on design verification and validation, utilizing advanced digital manufacturing techniques such as digital twins to simulate production runs and minimize physical prototypes. The contract manufacturer's ability to seamlessly integrate various component streams and manage complex sub-assembly logistics defines their competitive advantage in the market, often requiring globally synchronized production schedules to support multinational OEM operations.

Downstream analysis focuses on the distribution channel, which is highly efficient and optimized for Just-In-Time (JIT) delivery directly to OEM final assembly plants. Distribution channels are predominantly direct, involving CM-managed logistics, specialized shipping containers, and highly coordinated transport networks to minimize inventory holding costs for both the CM and the OEM. Indirect distribution, though less common for critical systems, may involve large logistics providers managing warehousing and specialized pre-assembly checks for non-time-critical components. The distribution infrastructure must be robust enough to handle the increasing volume and complexity of parts, especially large, sensitive components like EV battery packs that require specialized handling and temperature control during transit. Effective downstream execution ensures seamless integration into the OEM’s final production schedule, which is paramount for overall efficiency and maximizing vehicle build rates.

The primary potential customers and end-users of the Automotive Contract Manufacturing Market are the global Original Equipment Manufacturers (OEMs), encompassing established automotive giants, niche luxury and performance brands, and increasingly, new entrants focusing exclusively on Electric Vehicles (EVs) and autonomous technology. These major OEMs, such as General Motors, Volkswagen Group, Toyota, and Tesla, rely on contract manufacturers to scale production rapidly, especially when entering new technological domains like battery manufacturing or advanced sensor integration where internal expertise or immediate capacity may be insufficient. The necessity for strategic outsourcing is particularly acute among traditional OEMs undergoing the costly and risky transition from ICE platforms to electric and connected vehicle architectures. These established customers seek partners who offer not only high-quality manufacturing but also specialized engineering support and risk diversification across global supply chains, often engaging in multi-year, multi-billion dollar strategic contracts to ensure long-term stability and cost certainty for critical components.

In addition to traditional manufacturers, a rapidly growing customer segment comprises automotive technology companies and mobility providers. This includes specialized startups developing Level 4 or Level 5 autonomous driving systems, electric vehicle platforms utilizing highly customized components, and companies focused on implementing Mobility-as-a-Service (MaaS) solutions that require unique fleet vehicles. These customers often lack internal manufacturing infrastructure entirely, making contract manufacturing an essential prerequisite for their market entry and scalability. They prioritize CMs who offer flexible production volumes, expertise in software integration with hardware, and the capability to manage complex electronic systems assembly, moving beyond traditional automotive contract manufacturing into high-tech electronics integration services. This diverse customer base demands a highly adaptable and technologically advanced contract manufacturing ecosystem capable of handling both massive volume production and specialized, low-volume, high-complexity projects simultaneously.

Furthermore, Tier 1 suppliers, who historically acted as prime component providers, are also becoming significant customers for Tier 2 contract manufacturers. As Tier 1 suppliers focus on complex systems integration (e.g., integrating an entire cockpit module), they outsource the production of sub-components (e.g., plastic injection molded parts, specific electronic boards) to specialist CMs to maintain focus on their core competencies and manage internal capacity constraints. This inter-supplier outsourcing creates a multilayered customer relationship, requiring contract manufacturers to manage highly complex technical specifications and delivery timelines not only with OEMs but also with large Tier 1 integrators, underscoring the deep interwoven nature of the contemporary automotive supply chain and the pervasive reliance on outsourced expertise across all levels of component fabrication and assembly.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $85.4 Billion |

| Market Forecast in 2033 | $146.9 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Magna International, Continental AG, ZF Friedrichshafen, Aptiv PLC, Bosch, Flex Ltd., Gestamp, Lear Corporation, Faurecia, Linamar Corporation, Benteler International, Martinrea International, Valmet Automotive, Ricardo PLC, AVL, Wipro Infrastructure Engineering, Sanmina Corporation, Jabil Circuit, VDL Nedcar, Pininfarina. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape within the Automotive Contract Manufacturing market is rapidly evolving, driven by the imperative for precision, flexibility, and sustainability in component production, particularly for next-generation electric and autonomous vehicles. A cornerstone technology is the implementation of Industry 4.0 principles, integrating the Industrial Internet of Things (IIoT), cyber-physical systems, and cloud computing to create fully connected smart factories. This connectivity facilitates real-time data acquisition from machinery and production lines, enabling immediate process adjustments and superior operational transparency. Advanced automation, specifically utilizing highly flexible robotic cells equipped with sophisticated vision and haptic sensors, is critical for handling diverse materials and achieving micron-level tolerances required for ADAS components and sensitive battery cell assembly, significantly reducing human error and boosting throughput scalability across various product lines.

Furthermore, additive manufacturing (3D printing) is transitioning from a prototyping tool to a vital part of low-volume, high-complexity contract manufacturing. This technology is utilized for producing specialized tooling, jigs, and fixtures rapidly, drastically shortening lead times for new product introductions. More importantly, 3D printing, especially using advanced metal powders, is increasingly used to produce complex, lightweight vehicle components that cannot be easily manufactured using traditional methods like casting or stamping, offering mass customization capabilities. Simultaneously, the market is heavily reliant on sophisticated simulation and digital twin technology. These tools allow contract manufacturers to simulate the entire production environment digitally before cutting metal, optimizing production layouts, validating complex assembly sequences for EV battery packs, and predicting maintenance requirements, thereby guaranteeing first-time-right manufacturing execution and drastically cutting down on physical prototyping costs and time.

The increasing focus on cybersecurity represents another critical technological requirement, especially for manufacturers handling connected vehicle components (V2X systems, ECUs). Contract manufacturers must implement secure manufacturing environments, ensuring the integrity and authenticity of firmware and hardware produced, preventing unauthorized modifications or the injection of malicious code during the manufacturing process. Advanced inspection technologies, including computed tomography (CT) scanning and laser scanning, are now standard for non-destructive testing, ensuring the internal structural integrity of complex components like high-pressure aluminum castings used in vehicle frames. These combined technologies enable the contract manufacturer to meet the dual challenge of high-speed, high-volume production while adhering to the zero-defect tolerance necessary for modern, safety-critical automotive systems.

The primary driver is the complexity and cost of the transition to Electric Vehicles (EVs) and autonomous systems (ADAS). OEMs outsource manufacturing to specialized partners to mitigate the massive capital investment required for battery systems, power electronics, and high-precision sensor production, allowing them to focus resources on core competencies like software and branding. This strategy enhances scalability and accelerates time-to-market for new technological architectures.

IP protection is typically secured through rigorous contractual agreements, including Non-Disclosure Agreements (NDAs) and specific licensing terms defining usage rights. Leading contract manufacturers also employ advanced digital security measures, segregated manufacturing environments, and strict data governance protocols to prevent unauthorized access or replication of proprietary designs and firmware, ensuring client design integrity throughout the manufacturing lifecycle.

While Asia Pacific remains the largest volume market, North America and Europe show the highest growth potential for high-value, complex contract manufacturing, particularly concerning EV battery packs, advanced electronic control units, and ADAS components. This growth is driven by regulatory incentives promoting localized supply chains (e.g., IRA in the US) and the need for proximity between R&D centers and specialized production facilities for highly customized automotive systems.

Key risks include supply chain disruptions, potential quality control inconsistencies across geographically dispersed facilities, and dependence on a third party’s technological roadmap. OEMs mitigate these risks by implementing rigorous supplier qualification processes, maintaining diversified contract manufacturing partnerships, and utilizing real-time monitoring technologies to ensure operational alignment and product quality assurance.

Industry 4.0, characterized by AI, IIoT, and automation, is enabling contract manufacturers to establish smart factories capable of dynamic, flexible production schedules and predictive maintenance. This allows for rapid switchovers between different component models, ensures higher asset utilization, drastically reduces downtime, and enables real-time, autonomous quality inspection, delivering higher margins and superior service quality compared to traditional manufacturing models.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.