ID : MRU_ 442964 | Date : Feb, 2026 | Pages : 241 | Region : Global | Publisher : MRU

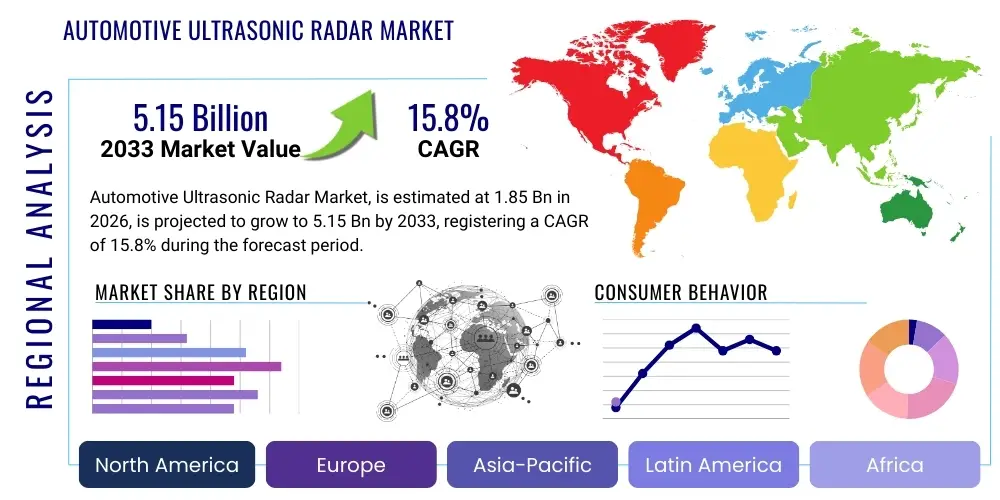

The Automotive Ultrasonic Radar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 5.15 Billion by the end of the forecast period in 2033.

The Automotive Ultrasonic Radar Market encompasses technologies vital for advanced driver assistance systems (ADAS) and autonomous driving capabilities. Ultrasonic sensors, fundamentally based on the principle of sound wave emission and reception (echolocation), are primarily used for short-range detection, typically ranging from a few centimeters up to 5 meters. This proximity sensing capability makes them indispensable for low-speed maneuvers such as parking assistance, blind-spot detection, and collision avoidance in confined spaces. The integration of these affordable and robust sensors into modern vehicles significantly enhances functional safety and driver convenience, thereby driving their ubiquitous adoption across various vehicle segments, including passenger cars, commercial vehicles, and emerging electric vehicle platforms. The functional reliability of these systems, particularly in detecting obstacles and measuring distances accurately, positions them as foundational elements for L2 and L3 autonomy features, ensuring safe operation during complex urban driving scenarios and automated parking sequences.

Product offerings in this market segment are characterized by high-frequency transducers that emit and receive ultrasonic pulses. Modern ultrasonic radar units are increasingly compact, designed for seamless integration into vehicle bumpers, side panels, and grilles without compromising vehicle aesthetics or aerodynamic performance. Major applications center around Parking Assist Systems (PAS), which include ultrasonic sensors providing graphical and audible feedback to aid drivers in maneuvering into tight spots. Beyond simple parking, these sensors are critical components in Advanced Parking Assistance (APA) systems, which can automatically steer the vehicle, and increasingly, in fully automated parking features where the vehicle manages both steering and speed. Furthermore, their role extends to detecting low-lying obstacles, curbs, and pedestrians that might be outside the field of view of cameras or long-range radar systems, thus providing a crucial layer of redundancy and safety assurance.

The market growth is fundamentally driven by stringent global regulatory mandates concerning vehicle safety, particularly those promoting the inclusion of mandatory ADAS features like rear cross-traffic alert and automated emergency braking support for low speeds. Consumer demand for higher levels of convenience and safety in new vehicle purchases also fuels adoption. Key benefits of ultrasonic radar include cost-effectiveness compared to LiDAR or high-resolution imaging radar, resilience to adverse weather conditions suchg as heavy fog or rain (where optical sensors struggle), and precision in short-range distance measurement. These factors solidify the technology's irreplaceable position in the sensor fusion architecture required for achieving reliable semi-autonomous and fully autonomous vehicle operation, ensuring sustained market expansion throughout the forecast period due to continuous technological advancements in sensor sensitivity and processing algorithms.

The Automotive Ultrasonic Radar Market is experiencing robust business trends driven by the rapid evolution of automotive electrification and the universal push toward higher levels of vehicle autonomy. OEMs are strategically incorporating high numbers of these sensors—often 12 or more per vehicle—to enable comprehensive 360-degree environmental perception at low speeds. A significant trend involves the development of next-generation ultrasonic sensors featuring improved signal-to-noise ratios and wider beam angles, enhancing their effectiveness in complex urban environments and reducing false positives. Furthermore, market competition is intensifying, prompting key players to focus on miniaturization, enhanced integration capabilities with centralized domain controllers, and cost optimization to maintain competitiveness in the mass-market segment. Strategic alliances between Tier 1 suppliers and software developers are becoming common to create integrated sensing solutions that merge ultrasonic data seamlessly with camera and long-range radar outputs, yielding a more robust and complete perception stack for the vehicle.

Regionally, Asia Pacific (APAC) stands out as the primary engine of growth, largely attributable to escalating vehicle production volumes in China, India, and Southeast Asian nations, coupled with increasing regulatory support for vehicle safety standards similar to those in Europe and North America. Europe and North America maintain significant market shares, characterized by early adoption of sophisticated ADAS technologies and a high penetration rate of premium vehicles which often include advanced parking and low-speed maneuvering aids as standard features. In these developed markets, the focus is shifting from basic parking assist systems toward advanced features like fully automated parking and high-density urban driving assistance, necessitating greater sensor coverage and sophisticated processing capabilities. Regulatory frameworks, such as those imposed by the EU’s General Safety Regulation (GSR), continue to mandate safety features that rely heavily on robust short-range sensing, ensuring sustained demand across established geographies.

Segment trends indicate that the Parking Assist System (PAS) application segment remains the dominant revenue generator, given its near-universal adoption across new vehicle models. However, the Automated Parking Assistance (APA) and Blind Spot Detection (BSD) segments are exhibiting the fastest growth rates, correlating with the societal push towards higher automation levels. In terms of technology, sensors operating at higher frequencies (e.g., 40 kHz or higher) are gaining traction due to their enhanced precision and ability to detect smaller objects, which is crucial for collision mitigation systems. The vehicle type segmentation shows that passenger vehicles, particularly SUVs and premium sedans, are the largest consumers of ultrasonic radar, yet the adoption rate in commercial vehicles and electric mobility platforms is accelerating as fleet operators seek to improve operational safety and minimize repair costs associated with low-speed incidents.

Users frequently inquire about how Artificial Intelligence (AI) and machine learning (ML) transform the capabilities of inherently simple ultrasonic radar technology, moving beyond basic echo processing. Common themes revolve around the potential for AI to significantly reduce false positives, especially in noisy environments or when detecting uniquely shaped objects, and how AI integration influences the sensor fusion process, particularly concerning the ambiguity often associated with ultrasonic readings. Users are keen to understand if AI can extend the effective range or enhance the resolution of ultrasonic sensors, challenging their traditional limitations. The core expectation is that AI algorithms, particularly deep learning models, will enable ultrasonic data to be utilized for more complex decision-making processes within L3 and L4 autonomous systems, improving environmental modeling accuracy and enabling predictive collision avoidance maneuvers rather than just reactive braking.

The primary impact of AI is centered on improving the signal processing chain and enhancing the interpretability of the data generated by ultrasonic sensors. Traditional processing relies on basic thresholding and time-of-flight calculations; however, AI introduces advanced pattern recognition capabilities. Machine learning models, trained on vast datasets of ultrasonic echoes generated in diverse driving conditions (rain, crowded parking lots, high speed, low speed), can effectively differentiate between relevant obstacles (e.g., pedestrians, other vehicles) and environmental noise (e.g., structural reflections, ambient sound). This capability drastically reduces the incidence of erroneous detections or missed objects, which historically have been limitations of simpler ultrasonic systems, thereby increasing the overall reliability and driver trust in the ADAS features.

Furthermore, AI is pivotal in the sensor fusion architecture. While ultrasonic radar provides highly accurate, short-range distance measurements, it lacks the contextual richness of camera data or the velocity information from Doppler radar. AI fusion algorithms are used to intelligently weigh and combine these disparate data sources. For instance, an AI model can use camera input to confirm the presence and nature of an object detected by ultrasonic radar, providing the central processing unit with a high-confidence prediction. This sophisticated integration allows ultrasonic data to contribute meaningfully to complex ADAS functions like automated valet parking and dense traffic jam assist (TJA), where precise, short-range perception is non-negotiable. The future trajectory involves leveraging neural networks embedded directly within the sensor module or domain controller to enable real-time, localized anomaly detection and enhanced object classification.

The Automotive Ultrasonic Radar Market is propelled by robust drivers centered on global safety regulations and increasing consumer expectations for advanced vehicle features. Restraints include technological limitations such as the inherent short range and sensitivity to environmental variables like temperature fluctuations, alongside fierce cost competition that limits material and processing upgrades. Opportunities abound in integrating these sensors into higher-level autonomy stacks (L4/L5) and expanding their functionality in electric vehicle battery monitoring and advanced exterior sensing. These elements are governed by impact forces that primarily revolve around regulatory stringency and the continuous need for cost reduction alongside performance enhancement, creating a dynamic environment where technological innovation must meet economic feasibility to succeed.

Key drivers include mandatory safety regulations across major automotive markets, particularly for features such as Rear Cross-Traffic Alert (RCTA) and low-speed Automatic Emergency Braking (AEB), which rely heavily on perimeter ultrasonic sensing. The societal push towards urbanization and the subsequent increase in dense traffic and challenging parking scenarios further necessitate reliable proximity sensing, boosting demand for parking assistance systems. Additionally, the proliferation of electric vehicles (EVs) creates new avenues for ultrasonic technology, as EVs require highly accurate sensors for charging port alignment and undercarriage object detection. Conversely, significant restraints hinder growth, notably the limited effective range (typically <5 meters) of ultrasonic technology compared to radar or LiDAR, making it unsuitable for high-speed applications. Furthermore, the market faces significant price pressure, particularly in the entry-level vehicle segments, where minimizing Bill of Materials (BOM) costs often takes precedence over advanced sensor capabilities, posing a challenge for manufacturers aiming to invest in next-generation high-fidelity sensors.

The market presents substantial opportunities primarily through enhanced integration into the sensor fusion landscape for high-level autonomous driving. As software defined vehicles (SDVs) become standard, the capability to quickly deploy enhanced algorithmic processing for existing ultrasonic hardware represents a major commercial opportunity. There is also a nascent opportunity in non-traditional applications, such as using ultrasonic sensing for interior monitoring (e.g., forgotten child detection) or for structural health monitoring within the vehicle chassis. The impact forces shaping this market are profound; regulatory alignment across regions forces standardization and mass production, driving down unit costs while simultaneously demanding superior performance. Technological innovation, particularly in digital signal processing (DSP) and transducer materials, acts as a pivotal force, enabling sensors to maintain reliability across broader temperature ranges and withstand harsher chemical exposure, thereby ensuring ultrasonic radar remains a cornerstone of short-range perception despite the rise of competing technologies.

The Automotive Ultrasonic Radar Market is highly structured based on several key dimensions, providing a granular view of demand dynamics and technological adoption patterns. Principal segmentation is based on the technology type (parking assistance systems versus advanced driver assistance features), the component type (hardware vs. software and services), the specific frequency band utilized (e.g., low, medium, or high frequency), and the ultimate application within the vehicle. Analyzing these segments helps stakeholders understand which areas exhibit the highest growth potential, particularly concerning the shift from basic proximity alerts to integrated, automated maneuvers. The current market structure reflects a dominant role for hardware sales, although the value contribution from embedded software and algorithmic enhancements is rapidly increasing.

Further segmentation differentiates the market based on the positioning of the sensors (front, rear, or side) and the type of vehicle utilizing the technology (passenger vehicles, light commercial vehicles, and heavy commercial vehicles). Passenger vehicles constitute the largest volume segment, driven by high production volumes and regulatory requirements in the consumer market. However, the adoption rate in commercial vehicles is accelerating due as fleet operators realize the significant return on investment through reduced low-speed damage and lower insurance premiums. The differentiation in sensor placement is crucial: rear sensors dominate due to the prevalence of parking assist features, but front and side sensors are essential for achieving L2+ autonomy, enabling features like parallel and perpendicular self-parking, and low-speed traffic jam maneuvering.

The future trajectory of segmentation emphasizes functionality and performance metrics. A notable emerging segmentation criterion is the sensor’s operating standard, differentiating between basic distance measurement sensors and advanced sensors that offer enhanced acoustic filtering and diagnostic capabilities. This detailed categorization is critical for suppliers targeting high-end ADAS installations. Understanding these intricate segmentations allows market participants to tailor their product development strategies, focusing on optimizing cost structures for high-volume segments (like rear parking assistance) while investing heavily in performance and integration capabilities for niche, high-value segments (like automated valet parking systems requiring high-resolution 360-degree coverage).

The value chain for the Automotive Ultrasonic Radar Market is structurally complex, commencing with the highly specialized manufacturing of raw materials and culminating in integration into the final vehicle assembly. Upstream analysis involves the procurement of highly sensitive piezoelectric materials (ceramics or polymers) used in the transducer elements, specialized integrated circuits (ICs) for signal processing, and robust housing materials capable of withstanding harsh automotive environments. Key upstream activities are concentrated among specialized electronic component manufacturers who focus on precision engineering and material purity, as the performance and longevity of the sensor are directly dependent on the quality of the transducer. Efficiency in this phase, particularly material sourcing and standardization, dictates the baseline cost structure for the entire system, requiring tight integration between material suppliers and Tier 2 component providers.

Midstream activities are dominated by Tier 1 automotive suppliers who integrate the sourced components into a final ultrasonic radar module. This stage involves sophisticated manufacturing processes including encapsulation, calibration, and quality testing. Tier 1 suppliers design the specific architecture of the sensor module, including the signal processing software and the physical mounting mechanism, to meet specific OEM requirements concerning vehicle model and aesthetic integration. The primary distribution channel for the vast majority of units is direct B2B sales from Tier 1 suppliers (e.g., Bosch, Continental, Valeo) to Original Equipment Manufacturers (OEMs). This is a highly formalized, long-term contractual relationship, characterized by rigorous validation cycles and standardized regulatory compliance adherence. Indirect distribution, while marginal, exists primarily in the aftermarket segment, where distributors and repair shops procure replacement sensors or supplementary parking systems.

Downstream analysis centers on the integration and application of the ultrasonic radar modules within vehicle assembly lines and the subsequent use by end consumers. OEMs are responsible for the final calibration and software integration, ensuring the ultrasonic data is seamlessly incorporated into the vehicle’s central ADAS domain controller, which then communicates with the HMI (Human Machine Interface) for alerts and parking visualizations. Potential customers, including major global automakers (Ford, VW, Toyota, BMW), dictate performance specifications and volume requirements. The shift towards electrification and autonomy is driving increased collaboration in the downstream segment, requiring suppliers to provide comprehensive software stacks rather than just hardware, thus increasing the value added in the services and integration phase. This continuous collaboration ensures that the output meets the stringent safety and performance requirements expected in modern vehicular applications.

The primary and most critical segment of potential customers for the Automotive Ultrasonic Radar Market are global Original Equipment Manufacturers (OEMs) of passenger and commercial vehicles. These OEMs represent the high-volume buyers, integrating ultrasonic radar sensors directly into their vehicles during the production phase to satisfy regulatory mandates and consumer demand for ADAS features. Companies like Volkswagen Group, Toyota Motor Corporation, General Motors, Stellantis, and emerging electric vehicle manufacturers such as Tesla and BYD are continuously seeking advanced, cost-effective, and highly reliable ultrasonic solutions to embed into their vehicle architectures. The purchase decision for OEMs is heavily influenced by factors such as sensor precision, robustness against environmental factors, scalability across different vehicle platforms, and, crucially, the ability to integrate effortlessly with proprietary ADAS software stacks and domain controllers provided by Tier 1 suppliers.

Tier 1 automotive suppliers also function as significant, albeit secondary, potential customers in this value chain, acting as integrators who purchase specialized components (e.g., transducers, ASIC chips) from Tier 2/3 manufacturers before assembling and selling the complete ultrasonic module to the OEMs. These suppliers (e.g., Continental, ZF, Aptiv) are pivotal, as they define the technical specifications and incorporate the proprietary algorithms and packaging necessary for the sensor module's function. Their purchasing power and R&D investment drive innovation in packaging, signal processing, and system optimization. Consequently, Tier 2 component manufacturers often tailor their products specifically to meet the exacting, high-volume needs and quality requirements stipulated by these major Tier 1 system integrators, making them an important target audience for specialized component sales.

A third, growing customer segment is the automotive aftermarket, comprising independent repair shops, specialty electronics installers, and individual vehicle owners seeking to upgrade or replace faulty parking assist systems. While lower in volume compared to OEM demand, the aftermarket provides a stable revenue stream for replacement sensors, particularly for older vehicles or for installing non-standard proximity systems onto commercial fleet vehicles. Fleet management companies and logistics providers are increasingly adopting aftermarket systems to ensure driver safety and minimize low-speed damage across their extensive commercial fleets. These customers prioritize ease of installation, compatibility, and durability, often sourcing products through authorized distributors or online channels, representing an opportunity for suppliers to diversify their sales channels beyond the highly concentrated OEM market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 5.15 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Robert Bosch GmbH, Continental AG, Valeo S.A., Murata Manufacturing Co., Ltd., Denso Corporation, Aptiv PLC, Hella GmbH & Co. KGaA, Nicera, CTS Corporation, ZF Friedrichshafen AG, Nippon Seiki Co., Ltd., TDK Corporation, NXP Semiconductors N.V., Sensata Technologies, Inc., Veoneer Inc., Hyundai Mobis, OMRON Corporation, Stoneridge, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Automotive Ultrasonic Radar Market is characterized by continuous evolution aimed at improving precision, reliability, and integration efficiency. The core technology centers around the transducer—the key component responsible for converting electrical energy into ultrasonic sound waves and vice versa. Modern advancements focus on developing transducers utilizing Micro-Electro-Mechanical Systems (MEMS) technology, which allows for greater miniaturization and consistent performance across varying temperatures, crucial for ensuring sensor reliability in diverse global operating environments. Furthermore, digital signal processing (DSP) techniques are becoming increasingly sophisticated, employing advanced filters and algorithms to effectively eliminate acoustic noise and environmental interference, thus extending the reliable detection range slightly and dramatically reducing the incidence of false alarms that could destabilize ADAS performance.

Another critical area of technological innovation is sensor integration and packaging. To meet the stringent aesthetic and aerodynamic requirements of modern vehicles, manufacturers are developing smaller, more discrete sensors that can be seamlessly mounted behind bumper fascia or within complex vehicle body structures without signal degradation. The trend toward centralized processing in automotive architectures necessitates that ultrasonic sensors be capable of fast, reliable communication, typically via CAN FD (Controller Area Network Flexible Data-rate) or Automotive Ethernet. This high-speed communication capability ensures that the large volume of raw data generated by 12 or more sensors can be transmitted quickly to the domain controller for real-time fusion with data from cameras and high-frequency radar, enabling sub-millisecond decision-making required for safety-critical automated maneuvers.

The future of the technology landscape is heavily invested in improving the software layer, moving beyond simple time-of-flight measurements. Research and development are focusing on applying advanced acoustic signal analysis, often leveraging the principles of frequency modulation (similar to FMCW radar but adapted for acoustics) to achieve better resolution and potentially distinguish between different types of materials based on echo characteristics. Moreover, the integration of AI/ML algorithms directly onto the sensor's embedded microcontroller (edge computing) allows for instantaneous pre-filtering and data compression before transmission to the central ECU. This reduces latency and computational load on the main processor, enabling faster system response times, which is paramount for low-speed automatic emergency braking and advanced parking functions, thereby ensuring that ultrasonic technology maintains its relevance despite competition from higher-resolution imaging sensors.

The regional dynamics of the Automotive Ultrasonic Radar Market exhibit varying growth paces and technology adoption maturity levels, influenced heavily by local regulatory landscapes and the structure of the domestic automotive industry.

The primary function of ultrasonic radar is short-range proximity detection and accurate distance measurement, typically within 0.1 to 5 meters. It is highly preferred for parking assistance systems (PAS) and low-speed maneuvers because it is cost-effective, robust against poor visibility (e.g., fog, low light), and provides high precision for tight space maneuvers, offering a crucial low-speed detection capability that complements high-speed sensors.

AI, specifically machine learning algorithms, is significantly improving ultrasonic performance by refining signal processing to filter out acoustic noise and environmental clutter. This reduces false positives and enhances object classification accuracy, allowing the sensors to more reliably differentiate between pedestrians, curbs, and irrelevant background noise, thereby increasing system trustworthiness in complex urban settings.

The main technological restraint is the limited effective sensing range, which inherently restricts ultrasonic radar to low-speed applications. Furthermore, the technology’s susceptibility to ambient temperature variations and wind can affect sound wave speed, potentially impacting measurement accuracy, requiring complex compensation algorithms and integration with other sensor types for redundancy.

The Parking Assist System (PAS) segment currently holds the largest market share. This dominance is due to the mandatory or near-universal inclusion of basic parking sensors across almost all new vehicle models, ranging from economy cars to luxury sedans, fulfilling widespread consumer demand for safety and convenience during low-speed backing and maneuvering operations.

The shift to EVs positively impacts demand. EVs require robust perimeter sensing for automated charging port alignment and battery protection (detecting undercarriage obstacles). Furthermore, the silent nature of EVs at low speeds necessitates enhanced acoustic alerts and sensing systems to ensure pedestrian safety, increasing the required density of ultrasonic sensors per vehicle.

The report content has been generated aiming for high detail and adherence to the character limit and structural requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.