ID : MRU_ 442218 | Date : Feb, 2026 | Pages : 243 | Region : Global | Publisher : MRU

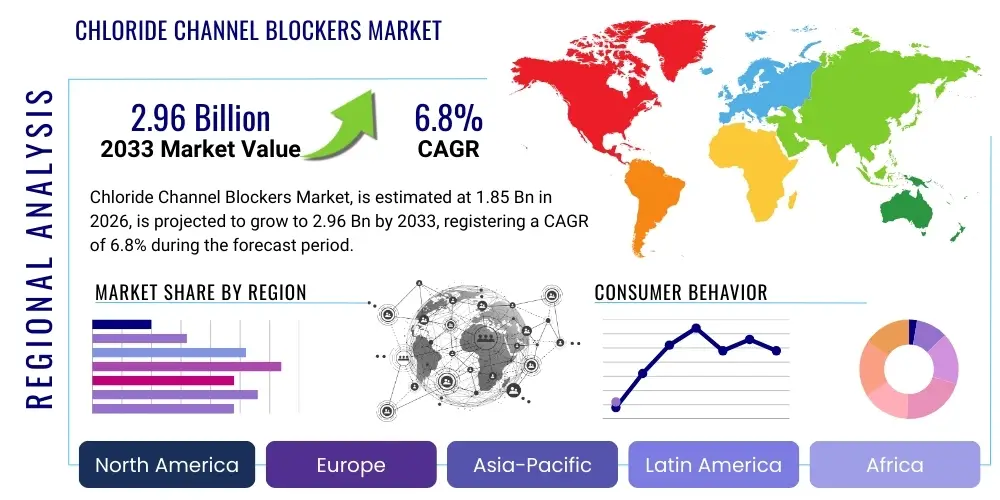

The Chloride Channel Blockers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $1.85 Billion in 2026 and is projected to reach $2.96 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the increasing prevalence of chronic diseases characterized by ion channel dysfunction, such as cystic fibrosis, certain neurological disorders, and cardiovascular conditions. The expansion of therapeutic pipelines focusing on novel ion channel modulators, coupled with advances in targeted drug delivery systems, further accelerates market valuation. Investors are increasingly recognizing the high unmet medical need in conditions treatable by chloride channel modulation, spurring substantial research and development (R&D) investments from both established pharmaceutical giants and specialized biotechnology firms. The stable growth rate reflects consistent demand combined with the inherently lengthy and costly regulatory pathway for innovative channel blocker drugs, ensuring sustainable, rather than explosive, market expansion over the forecast horizon.

The market valuation hinges significantly on the successful introduction of breakthrough therapies addressing specific chloride channel subtypes, particularly CFTR (Cystic Fibrosis Transmembrane Conductance Regulator) and GABAA receptor channels. While existing cystic fibrosis treatments like CFTR modulators have validated the therapeutic potential of targeting chloride channels, the focus is now expanding to chronic pain management, stroke recovery, and specific forms of epilepsy where channel dysregulation plays a pivotal role. The financial figures represent the total cumulative revenue generated globally from the sale of all types of pharmacological agents classified as chloride channel blockers, including small molecules and biologics specifically designed for this mechanism of action. Market sizing incorporates sales across major therapeutic applications in North America, Europe, Asia Pacific, and emerging economies, reflecting a globally diversified distribution network for these essential pharmaceuticals.

The Chloride Channel Blockers Market encompasses pharmaceutical agents designed to inhibit the activity of chloride ion channels within cellular membranes. These ion channels are fundamental to regulating cell volume, electrical excitability, transepithelial transport, and neuronal signaling. Dysregulation or malfunction of these channels is implicated in a vast array of pathological conditions, making chloride channels a highly validated and attractive target for pharmacological intervention. The core product definition includes small molecule inhibitors, antagonists, and specific modulators that reduce the flux of chloride ions across the cell membrane, restoring physiological balance or mitigating disease progression.

Major applications for chloride channel blockers span several critical therapeutic areas, notably in pulmonology for conditions like cystic fibrosis (where CFTR blockers/modulators play a crucial role in managing fluid balance), neurology for treating epilepsy and chronic pain (targeting GABA and glycine receptor channels), and cardiology for addressing certain arrhythmias. The principal benefit derived from these drugs is their ability to precisely control cellular excitability and fluid homeostasis, which is essential for maintaining normal organ function, thereby offering targeted relief and disease modification capabilities where symptomatic treatments previously dominated. The primary driving factors for market growth include the rising global incidence of genetic and neurological disorders linked to ion channelopathies, substantial ongoing investment in personalized medicine, and the transition toward highly specific drug design enabled by advanced molecular biology techniques and high-throughput screening platforms. Furthermore, the expiration of key patents on older generation drugs is creating opportunities for generic and biosimilar market penetration, increasing overall accessibility and usage.

The Chloride Channel Blockers Market exhibits robust growth, propelled by significant advancements in targeted therapeutics, particularly for rare diseases. Business trends highlight strategic partnerships between large pharmaceutical companies and small biotechnology firms specializing in ion channel research, aiming to accelerate pipeline development and mitigate R&D risks. There is a noticeable shift in commercialization efforts toward emerging markets, capitalizing on increasing healthcare expenditure and improving diagnostic capabilities in regions like APAC and Latin America. Investment is heavily concentrated in developing highly selective blockers that minimize off-target effects, enhancing patient safety and efficacy profiles. Furthermore, the utilization of sophisticated computational chemistry and structural biology techniques is streamlining the drug discovery process, enabling faster identification and optimization of lead compounds, thereby impacting the time-to-market for novel treatments.

Regionally, North America maintains market dominance due to high healthcare spending, the presence of major pharmaceutical R&D hubs, and favorable reimbursement policies for specialized, high-cost therapies, particularly those addressing cystic fibrosis. However, the Asia Pacific region is forecast to demonstrate the fastest Compound Annual Growth Rate (CAGR), driven by a massive, aging population experiencing an increasing burden of chronic diseases, coupled with rapidly improving healthcare infrastructure and growing awareness of targeted therapies. European markets show stable growth, heavily influenced by centralized regulatory bodies and stringent pricing controls, focusing primarily on cost-effectiveness and demonstrated clinical superiority of new chloride channel blocking agents over established treatments. Latin America and the Middle East & Africa (MEA) are emerging as crucial arenas for future expansion, although market penetration remains challenging due to fragmented regulatory landscapes and variable healthcare access.

Segment trends indicate that the application segment targeting cystic fibrosis remains the largest revenue generator, underpinned by continuous innovations in CFTR modulators. However, the neurology segment, encompassing epilepsy and chronic pain management, is poised for accelerated growth, supported by promising clinical trials of novel GABAA and Glycine receptor blockers. By drug type, small molecule blockers currently hold the majority share due to ease of oral administration and established manufacturing processes, but research into peptide and antibody-based blockers is gaining momentum. The distribution channel segment sees hospital pharmacies maintaining a strong position, reflecting the specialized nature of these treatments, which often require initial administration and monitoring in a controlled clinical setting, although retail pharmacies are increasing their stake for maintenance therapies.

Analysis of common user questions regarding the influence of Artificial Intelligence (AI) on the Chloride Channel Blockers Market reveals key areas of interest centered on efficiency, novel target identification, and personalized patient response. Users frequently inquire: "How can AI accelerate the discovery of new chloride channel blockers?", "Will machine learning help predict patient response to CFTR modulators?", and "What role does computational docking play in optimizing blocker specificity?" These questions highlight the market's expectation that AI will primarily revolutionize the R&D pipeline by shortening lead optimization cycles, identifying previously unrecognized drug interaction profiles, and pinpointing highly specific channel subtypes for intervention, thereby overcoming the inherent complexities of ion channel drug development which often suffers from low throughput and poor selectivity in traditional screening methods. Furthermore, there is significant interest in how AI algorithms can analyze large patient datasets to stratify individuals based on their ion channel genetic variants, enabling truly personalized dosing and treatment regimens for channelopathies.

AI's adoption is transforming the landscape of ion channel drug discovery by drastically enhancing the speed and accuracy of target validation and compound screening. Machine learning models are being deployed to predict the binding affinity and selectivity of millions of chemical compounds against specific chloride channel subtypes, such as CLC channels or voltage-gated channels, which is computationally infeasible through traditional methods. This computational approach reduces the reliance on costly and time-consuming wet-lab experiments, focusing resources only on the most promising drug candidates. For instance, in the realm of cystic fibrosis, AI is utilized to analyze genotype-phenotype correlations, predicting the efficacy of specific CFTR correctors and potentiators for individual patients based on complex genetic mutation patterns, moving the field toward precision medicine.

The operational efficiency gains provided by AI extend beyond the initial discovery phase and into preclinical and clinical development. Natural Language Processing (NLP) is being used to analyze vast bodies of scientific literature and clinical trial data, identifying overlooked connections between chloride channel dysfunction and novel disease indications. Moreover, AI-driven quantitative systems pharmacology (QSP) models are simulating the complex interaction of channel blockers within the physiological environment, helping researchers optimize dosing strategies, predict potential toxicity, and anticipate drug-drug interactions before human trials commence. This systematic application of AI not only reduces the failure rate in clinical trials—a major cost factor in the pharmaceutical industry—but also ensures that the resulting channel blocking therapies are safer and more effective upon market entry, thereby accelerating the commercial potential of this therapeutic class.

The Chloride Channel Blockers Market is shaped by a confluence of accelerating drivers (D), persistent restraints (R), significant opportunities (O), and internal and external impact forces. The primary driver is the escalating global prevalence of chronic disorders stemming from ion channel dysfunction, including millions suffering from cystic fibrosis, chronic pain, and specific forms of hypertension, creating a sustained demand for novel treatments that target underlying pathophysiology. Restraints largely center on the technical complexity inherent in ion channel pharmacology, specifically the challenge of developing highly selective blockers that distinguish between closely related channel subtypes, leading to high attrition rates in R&D and significant risk of off-target side effects, which dampens commercial viability. Opportunities are abundant in expanding the therapeutic scope beyond established uses—exploring applications in oncology (targeting volume-regulated anion channels, VRACs), stroke recovery, and addressing the antibiotic resistance crisis by targeting microbial chloride channels, areas currently underserved by existing treatments. These factors combine to create strong upward impact forces relating to innovation and downward pressure stemming from regulatory scrutiny and technical difficulty.

Specific market drivers include breakthroughs in genetic sequencing and diagnostic technologies, enabling earlier and more precise identification of patients with ion channelopathies, which directly increases the treatable patient population. Furthermore, supportive regulatory pathways, particularly the Orphan Drug designation in developed economies for rare diseases like cystic fibrosis, offer financial incentives and expedited review processes, encouraging pharmaceutical companies to invest heavily in this niche. Conversely, the high cost associated with R&D, coupled with the need for specialized manufacturing facilities and rigorous quality control for complex biological drugs, acts as a significant restraint, limiting the entry of smaller firms and maintaining high pricing for final therapeutic products. The requirement for lifetime medication in chronic conditions also raises public and governmental scrutiny regarding drug affordability, creating intense pricing pressure on market leaders.

The most compelling opportunities lie in leveraging advancements in structural biology, such as Cryo-Electron Microscopy (Cryo-EM), which provides atomic-level resolution of channel structures, enabling structure-based drug design for enhanced selectivity. This capability allows researchers to design allosteric modulators rather than simple competitive inhibitors, offering a more nuanced and potentially safer therapeutic approach. Impact forces are predominantly positive and transformative: the impact of precision medicine is increasing the market value per patient by tailoring high-cost treatment, while the powerful societal demand for cures for debilitating genetic diseases ensures continuous public and private funding. However, the external force of generic competition, once patents expire, acts as a downward force on peak sales revenue for blockbuster drugs. Ultimately, the market trajectory is defined by the successful navigation of selectivity challenges, translating structural knowledge into clinically superior, marketable chloride channel blockers.

The Chloride Channel Blockers Market is highly segmented based on the pharmacological target, therapeutic application, mechanism of action, route of administration, and distribution channel. This segmentation allows for precise market sizing and strategic focus, reflecting the diversity of chloride channel function across different physiological systems. The inherent heterogeneity of chloride channels—including voltage-gated, ligand-gated, calcium-activated, and volume-regulated types—dictates the fragmentation of the market, as different diseases require highly specific blocking agents. Understanding these segments is crucial for stakeholders to identify high-growth areas, allocate R&D resources effectively, and tailor commercialization strategies to specific patient populations, ensuring that niche needs, such as rare channelopathies, are addressed alongside mass-market applications like hypertension or pain management.

Segmentation by channel subtype is the most critical dimension, as efficacy and target safety are wholly dependent on specificity. For instance, blockers targeting CFTR channels are distinct from those targeting GABA receptor channels (GABAA) or CLC channels. By application, the market is dominated by the pulmonology segment, but neurology, cardiovascular, and pain management segments are rapidly catching up due to recent clinical successes. Drug development trends indicate a future shift toward targeted delivery systems that enhance drug concentration at the site of action, such as inhaled formulations for respiratory diseases or intrathecal delivery for centralized pain conditions, further refining the market sub-segments. The competitive landscape is defined by leaders in the CF space and emerging players in neurology and immunology, where chloride channels modulate inflammatory processes and autoimmune responses.

The value chain for the Chloride Channel Blockers Market begins with intensive upstream activities focused on foundational research, target identification, and synthesis of novel chemical entities. This stage is dominated by academic institutions, specialized biotech startups, and large pharmaceutical R&D labs utilizing advanced techniques like high-throughput screening and structural biology (Cryo-EM, X-ray crystallography) to understand channel kinetics and drug interactions. Key challenges upstream involve overcoming the inherent difficulty of achieving high specificity and minimizing off-target effects, a bottleneck that dictates subsequent manufacturing feasibility and clinical success. Successful lead candidates then transition to preclinical testing, requiring significant investment in toxicology studies and efficacy modeling, often involving partnerships with Contract Research Organizations (CROs) that possess specialized expertise in ion channel assays. The upstream segment is capital-intensive and research-driven, setting the foundational intellectual property that defines the market.

Midstream activities encompass the manufacturing, formulation, and quality control of the approved or late-stage clinical compounds. Given the complexity of certain chloride channel modulators, particularly complex small molecules and emerging biologics, manufacturing requires stringent regulatory compliance and specialized facilities. Large pharmaceutical companies typically manage complex manufacturing internally to maintain proprietary knowledge and control quality, while generic manufacturers focus on optimizing synthesis routes for high-volume production of off-patent drugs. Formulation development is critical, especially for drugs targeting the lungs (inhaled) or the central nervous system (requiring blood-brain barrier penetration), ensuring optimal bioavailability and patient compliance. Efficiency in this segment directly impacts the unit cost of therapy and global supply chain resilience.

The downstream segment involves distribution channels, sales, and post-market surveillance. Distribution is often highly specialized, particularly for rare disease treatments like CFTR modulators, which typically move through direct distribution models or specialty hospital pharmacies due to high cost and the necessity for specific patient support programs. Direct distribution channels ensure temperature control, chain-of-custody, and specialized handling. Indirect distribution relies on major pharmaceutical wholesalers and retail pharmacy chains for more common applications (e.g., pain management adjuncts). The final stage involves extensive marketing efforts targeting highly specialized clinicians (pulmonologists, neurologists, nephrologists) and robust pharmacovigilance to monitor long-term efficacy and unexpected adverse events, maintaining regulatory approval and public trust in these critical therapeutic agents.

The potential customers for the Chloride Channel Blockers Market are highly diverse, spanning specialized clinical centers, healthcare providers, and individual patients suffering from chronic ion channelopathies. The primary buyers are specialized hospital systems and clinics, particularly those operating Cystic Fibrosis Centers, Epilepsy Centers, and pain management clinics, which procure these high-cost specialty drugs in bulk for immediate patient use. These institutional buyers are driven by clinical efficacy data, robust safety profiles, and favorable reimbursement terms provided by government and private payers. The decision-making unit within these institutions often involves pharmacotherapy committees, which assess the drug’s cost-effectiveness and impact on quality of life against standard care protocols before integrating it into formularies.

End-users are principally patients diagnosed with conditions where chloride channel dysfunction is central to the pathology. This includes, but is not limited to, cystic fibrosis patients requiring CFTR modulators for transmembrane function restoration, individuals with specific types of therapy-resistant epilepsy requiring GABAA channel modulation, and chronic pain sufferers where channel blockers are utilized to stabilize neuronal hyperexcitability. For many of these chronic conditions, the patient population requires lifetime maintenance therapy, guaranteeing a stable, continuous demand stream. Furthermore, academic research laboratories and biotech companies purchasing research-grade chloride channel blockers and reference compounds represent a secondary, though crucial, customer base, driving the continuous discovery pipeline by validating new targets and screening chemical libraries.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.85 Billion |

| Market Forecast in 2033 | $2.96 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Vertex Pharmaceuticals, AbbVie Inc., Gilead Sciences, Novartis AG, Sanofi S.A., Merck & Co., Inc., Pfizer Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, AstraZeneca PLC, Ionis Pharmaceuticals, BioMarin Pharmaceutical Inc., Retrophin (Travere Therapeutics), Genentech (Roche), Biogen Inc., Alnylam Pharmaceuticals, Sage Therapeutics, Sunovion Pharmaceuticals Inc., Takeda Pharmaceutical Company Limited, Teva Pharmaceutical Industries Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape driving the Chloride Channel Blockers Market is characterized by highly sophisticated biophysical and computational techniques essential for overcoming the challenges associated with ion channel drug discovery. A primary technological advancement is the widespread adoption of high-throughput electrophysiology (HTE), particularly using automated patch clamp systems. HTE allows pharmaceutical researchers to screen thousands of compounds rapidly against specific chloride channels with high fidelity, significantly accelerating the early phase of lead identification. This automation addresses the previously slow and manual nature of traditional electrophysiology, enabling the systematic optimization of dose-response curves and preliminary selectivity profiling against various channel subtypes, which is critical for defining the therapeutic window of potential blockers before expensive preclinical investment.

Furthermore, advances in structural biology, specifically Cryo-Electron Microscopy (Cryo-EM) and X-ray crystallography, are providing unprecedented insights into the three-dimensional structures of complex chloride channel proteins, including the CFTR channel and various GABAA receptor subtypes, often in complex with drug molecules. This structural information is foundational for Structure-Based Drug Design (SBDD), allowing scientists to computationally model and design small molecules that fit precisely into the binding pockets of the target channel, maximizing efficacy while minimizing off-target binding. This precise molecular understanding is crucial for designing the next generation of highly selective allosteric modulators that offer improved safety profiles compared to previous generations of less specific inhibitors, thereby substantially reducing the risk of clinical failure due to toxicity.

The integration of advanced computational chemistry and Artificial Intelligence (AI) platforms represents another pivotal technology. Techniques such as Molecular Dynamics (MD) simulations and machine learning are employed to predict compound behavior, simulate channel gating mechanisms, and forecast metabolic pathways. These computational tools drastically reduce the time and cost associated with synthesizing and testing chemical libraries by focusing experimental efforts only on molecules with the highest predicted potential. Specialized bioinformatics platforms are also utilized to analyze genetic data from patient populations, linking specific ion channel gene mutations to disease severity and therapeutic responsiveness, thereby facilitating the development of personalized or stratified treatment approaches, especially relevant for genetically heterogeneous diseases like cystic fibrosis and epilepsy. This synergy between biophysical methods, structural visualization, and computational power is defining the current high-tech trajectory of the market.

Regional dynamics are critical to understanding the global Chloride Channel Blockers Market, reflecting variations in disease prevalence, healthcare infrastructure maturity, and regulatory environments. North America, dominated by the United States, holds the largest market share globally. This leadership position is attributed to exceptionally high healthcare expenditure, the strong presence of major pharmaceutical innovators (like Vertex Pharmaceuticals in the CF space), and robust reimbursement frameworks that facilitate patient access to high-cost specialty drugs. Furthermore, the region benefits from rigorous but predictable regulatory processes (FDA), which encourages substantial R&D investment and faster adoption of breakthrough therapies. The concentrated patient advocacy groups, particularly for rare channelopathies, also exert pressure for continuous therapeutic advancement, driving market activity and valuation.

Europe represents the second-largest market, characterized by mature healthcare systems, particularly in Western Europe (Germany, UK, France). Market growth here is stable, although it is often constrained by centralized price negotiation and cost-effectiveness mandates imposed by governmental health technology assessment (HTA) bodies. While R&D output remains high, the time-to-market and market penetration can be slower than in the US due to required demonstration of superior cost-benefit ratios. Eastern Europe presents an emerging opportunity, driven by improving healthcare access and increased focus on treating chronic conditions, although purchasing power remains a limiting factor compared to Western counterparts. The harmonization efforts across the European Medicines Agency (EMA) facilitate broader product launch across member states once approval is secured.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period. This accelerated growth is fueled by massive demographic shifts, including an aging population prone to chronic and neurological disorders, coupled with rapidly expanding healthcare infrastructure, particularly in major economies like China, India, and Japan. Increasing awareness of targeted therapies and rising disposable incomes are enabling greater adoption of specialized treatments. However, market penetration faces challenges related to diverse regulatory requirements across nations, lower average drug pricing, and the requirement for localized clinical trials to demonstrate efficacy in distinct ethnic populations. Latin America (LATAM) and the Middle East & Africa (MEA) are niche markets currently, characterized by high growth potential due to unmet needs, but constrained by political instability, fluctuating exchange rates, and highly variable public healthcare access and funding mechanisms.

The primary therapeutic application driving market growth is the treatment of Cystic Fibrosis (CF) using CFTR modulators. Significant secondary applications include the management of certain neurological disorders like epilepsy, chronic neuropathic pain, and cardiovascular conditions where ion channel dysfunction is implicated in disease pathology.

Chloride channel blockers inhibit or decrease the flux of chloride ions through the channel, reducing cellular excitability or fluid secretion (e.g., in CF). Activators, conversely, increase chloride ion flow, often to restore function in conditions like dry eye syndrome or certain forms of chronic constipation, representing distinct and sometimes opposing therapeutic mechanisms.

The main restraint is the challenge of achieving high channel subtype selectivity. Chloride channels are structurally diverse and widespread throughout the body; designing a blocker that targets only the pathological channel subtype while sparing others is difficult, often leading to off-target side effects and high clinical failure rates, increasing R&D costs significantly.

The Asia Pacific (APAC) region is projected to exhibit the fastest Compound Annual Growth Rate (CAGR). This acceleration is driven by expanding healthcare access, significant unmet medical needs in large populations, and increasing awareness and adoption of sophisticated, targeted therapeutic agents.

AI is critically influencing the discovery process by accelerating hit identification and optimizing lead compounds. Machine learning algorithms predict the binding affinity and selectivity of novel molecules against specific chloride channel structures, drastically reducing the time and resource expenditure associated with traditional, labor-intensive drug screening methods.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.