ID : MRU_ 444160 | Date : Feb, 2026 | Pages : 245 | Region : Global | Publisher : MRU

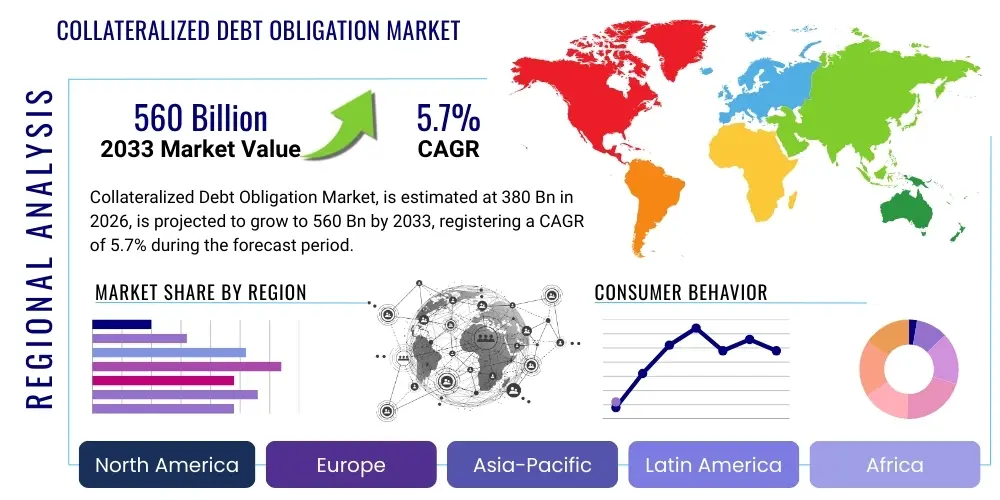

The Collateralized Debt Obligation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2026 and 2033. The market is estimated at USD 380 billion in 2026 and is projected to reach USD 560 billion by the end of the forecast period in 2033.

The Collateralized Debt Obligation (CDO) market encompasses a complex financial instrument that repackages and securitizes various types of debt, such as corporate bonds, mortgage-backed securities (MBS), and other asset-backed securities (ABS), into different tranches with varying risk and return profiles. This structuring allows investors to tailor their credit risk exposure, from senior tranches offering lower risk and yield to equity tranches promising higher returns but bearing the first losses. CDOs were originally conceived to provide institutional investors with diversified exposure to a broad pool of assets, enhancing liquidity in credit markets and offering potentially attractive risk-adjusted returns, especially in periods of low interest rates where traditional fixed-income investments yield less attractive yields.

Major applications of CDOs are predominantly found among institutional investors, including large banks, asset managers, hedge funds, pension funds, and insurance companies seeking to optimize their portfolios. These entities utilize CDOs for various strategic reasons, such as achieving diversification across different asset classes and geographies, enhancing yield in a low-yield environment, and customizing risk exposure to align with their specific investment mandates and regulatory capital requirements. The product’s intricate structure, which often involves a special purpose vehicle (SPV) to hold the collateral and issue the notes, appeals to sophisticated investors capable of understanding and modeling the inherent credit risks and correlations within the underlying portfolio. This complexity necessitates robust due diligence and analytical capabilities from market participants.

The primary benefits driving the CDO market include the ability to transform illiquid assets into tradable securities, thereby increasing market liquidity, and the potential for investors to achieve higher yields compared to similarly rated traditional bonds through structured finance techniques. Furthermore, CDOs facilitate risk transfer and distribution across the financial system, allowing originators to free up capital and manage their balance sheets more effectively. The market is also driven by financial innovation, where new structures and underlying asset classes are continuously explored to meet evolving investor demands and market conditions. Sustained demand from institutional investors for diversified income streams and customized risk exposures continues to act as a significant driving factor for the growth and evolution of the Collateralized Debt Obligation market, despite the historical challenges and increased regulatory scrutiny following past financial crises.

The Collateralized Debt Obligation market is experiencing a period of cautious but steady recovery and evolution, marked by significant shifts in business trends driven by post-crisis regulatory reforms and changing investor risk appetites. Financial institutions are now focusing on more transparent and standardized CDO structures, prioritizing collateral quality and comprehensive risk management frameworks. There is an observable trend towards customized, smaller deal sizes, often tailored to specific investor needs rather than the broad, complex structures prevalent before the 2008 financial crisis. Furthermore, the integration of advanced analytics and technology, including artificial intelligence and machine learning, is becoming increasingly critical for collateral selection, risk assessment, and performance monitoring, enhancing the efficiency and robustness of CDO management throughout its lifecycle.

Regional trends indicate a varied landscape in the CDO market. North America, particularly the United States, remains a dominant force, characterized by a sophisticated investor base and a well-developed legal and regulatory framework that supports structured finance. Europe is also a significant market, albeit with greater fragmentation due to differing national regulations and slower recovery in certain jurisdictions. The Asia Pacific (APAC) region is demonstrating considerable growth potential, driven by increasing institutional wealth, developing capital markets, and a rising demand for structured products as investors seek higher yields and diversification opportunities. Emerging markets in Latin America and the Middle East & Africa (MEA) are still nascent but show promise, with gradual improvements in financial infrastructure and increased interest from global investors looking for new avenues of growth and yield.

Segmentation trends within the CDO market highlight a shift towards certain asset classes and structures. While corporate debt and broadly syndicated loans continue to form a significant portion of collateral, there is growing interest in specialized CDOs backed by niche assets such as middle-market loans, esoteric asset-backed securities, and increasingly, those aligned with environmental, social, and governance (ESG) criteria. Synthetic CDOs, which derive their value from credit default swaps rather than actual assets, have seen reduced activity due to heightened regulatory scrutiny, though they still exist in more regulated forms. The market also observes an emphasis on senior and super-senior tranches, reflecting a preference for lower-risk investment profiles among institutional buyers, indicating a more conservative approach compared to pre-crisis periods and a focus on capital preservation and predictable income streams.

User inquiries concerning AI's influence on the Collateralized Debt Obligation market frequently revolve around its potential to revolutionize risk assessment, enhance pricing models, and streamline the complex operational aspects of CDO management. Common questions highlight curiosity about how AI can provide more granular insights into collateral performance, identify hidden correlations, and predict default probabilities with greater accuracy than traditional statistical methods. Concerns often arise regarding data quality, the interpretability of AI models ("black box" problem), potential biases embedded in algorithms, and the ethical implications of automating critical financial decisions. Users are also keen to understand if AI will lead to more efficient capital allocation, reduce human error, and foster greater transparency, while simultaneously questioning its resilience during periods of market stress and its ability to adapt to unforeseen economic shocks.

The Collateralized Debt Obligation market is shaped by a dynamic interplay of drivers, restraints, and opportunities, alongside significant impact forces. Key drivers include the persistent demand for yield enhancement in a low-interest-rate environment, pushing institutional investors towards structured products that offer higher risk-adjusted returns. The continuous financial innovation capabilities of investment banks to create bespoke financial instruments catering to specific investor risk appetites and regulatory frameworks also propels the market forward. Furthermore, the benefits of securitization, such as improved liquidity for illiquid assets and efficient risk transfer from originators to a broader investor base, remain compelling factors for market growth. These drivers collectively foster complex financial engineering meeting sophisticated market needs, enabling efficient capital allocation and portfolio diversification.

Conversely, the market faces several significant restraints, primarily stemming from heightened regulatory scrutiny and the lingering reputational damage incurred during the 2008 global financial crisis. Regulations like Dodd-Frank in the U.S. and CRD IV/CRR in Europe have imposed stricter capital requirements, risk retention rules, and transparency mandates, increasing the cost and complexity of issuing and managing CDOs. The inherent complexity of CDO structures, which can be challenging for even sophisticated investors to fully comprehend, also acts as a restraint, limiting the pool of potential buyers and increasing due diligence requirements. Moreover, the lack of liquidity in certain CDO tranches, particularly during periods of market stress, and the difficulty in accurately valuing illiquid collateral can deter investors and increase perceived risks, thus tempering market expansion and demanding more robust investor protection mechanisms.

Opportunities for growth in the CDO market lie in several promising areas. The rise of ESG (Environmental, Social, and Governance) investing presents an opportunity for the creation of "green" or "social" CDOs, backed by assets that align with sustainable development goals, attracting a new segment of socially conscious investors. The ongoing development of capital markets in emerging economies also provides a fertile ground for new securitization products, including CDOs, as these regions seek to diversify funding sources and enhance liquidity for their growing debt markets. Technological advancements, particularly in AI and blockchain, offer avenues to improve transparency, efficiency, and risk management within CDO structures, potentially alleviating some of the complexity and trust issues that have historically restrained the market. These innovations could lead to more robust, transparent, and resilient CDO products, expanding their appeal to a wider range of institutional investors globally.

The Collateralized Debt Obligation market is segmented to provide a granular view of its diverse landscape, enabling investors and market participants to understand the various types of structures, underlying assets, risk profiles, and investor preferences that define this complex financial instrument. This segmentation helps in identifying specific niches, assessing market trends within different categories, and tailoring investment strategies to particular risk-return objectives. The primary segmentation criteria typically include the type of CDO, the nature of the underlying collateral, the different tranches offered, and the categories of investors participating in the market, each presenting unique characteristics influencing market behavior and growth across economic cycles and regulatory environments.

The value chain of the Collateralized Debt Obligation market is a multi-faceted process involving several key stages, each with distinct participants and functions. It begins with the upstream activities centered around the origination and aggregation of underlying assets. Commercial banks, investment banks, and other financial institutions serve as originators, creating a pool of diverse debt instruments such as corporate loans, mortgages, or other receivables. These entities are responsible for underwriting and servicing the initial loans, forming the raw material for CDOs. Quality and diversity of upstream assets are paramount, directly influencing CDO risk profile and returns. Rigorous credit assessment and due diligence are performed at this stage to ensure the soundness of the collateral pool, forming the foundational layer of the entire structured finance mechanism.

Following origination, the structuring and issuance phase represents the core transformation process. Investment banks play a critical role here, acting as structurers who design the CDO product, define its tranches, and determine the cash flow waterfalls. This involves creating a Special Purpose Vehicle (SPV) that legally owns the collateral pool and issues the CDO notes to investors. Legal firms provide essential support in drafting offering documents and ensuring compliance with complex securities laws. Rating agencies (e.g., S&P, Moody's, Fitch) are integral to this stage, providing independent credit ratings for each tranche, which are crucial for investor confidence and regulatory capital treatment. The structuring process aims to optimize the risk-return profile across different tranches, appealing to a wide spectrum of institutional investors seeking specific levels of credit exposure and yield enhancement.

The downstream activities involve the distribution, trading, and ongoing management of the CDO securities. Investment banks’ sales desks and broker-dealers distribute the CDO tranches to institutional investors, including asset managers, hedge funds, pension funds, and insurance companies. Post-issuance, a secondary market for CDOs facilitates trading among these investors, providing liquidity and price discovery, though liquidity can vary significantly depending on the tranche and market conditions. Collateral managers are responsible for actively managing the underlying asset pool in managed CDOs, making investment decisions within specified guidelines to optimize performance and mitigate risk. Trustees, typically financial institutions, oversee the SPV, ensure adherence to the CDO indenture, and manage cash flows to investors. Direct and indirect distribution channels both play a role; direct placements often occur for highly customized CDOs to specific institutional buyers, while broader distribution leverages broker networks and electronic trading platforms to reach a wider investor base, thereby completing the extensive value chain.

The potential customers for Collateralized Debt Obligation products are primarily sophisticated institutional investors with a robust understanding of complex financial instruments and a capacity for detailed risk analysis. These entities typically possess large asset bases and specific investment mandates that often require exposure to diversified credit risk and enhanced yield opportunities that traditional fixed-income markets may not consistently provide. Their investment decisions are driven by regulatory capital, liability matching, and strategic portfolio diversification. Furthermore, their analytical capabilities allow them to perform the extensive due diligence necessary to evaluate the intricate structures and underlying collateral pools of CDOs, making them well-suited for these specialized investment vehicles.

Key categories of end-users and buyers include a broad spectrum of financial institutions. Commercial banks and investment banks often invest in CDOs to manage their balance sheets, diversify credit risk exposures, and generate incremental returns, particularly in highly-rated senior tranches that carry favorable capital treatment. Asset managers, including mutual funds and exchange-traded funds with structured credit mandates, seek CDOs to enhance portfolio yields and provide exposure to a granular set of credit risks not easily accessible through direct investments. Their analytical teams focus on fundamental credit analysis of the underlying assets and the structural integrity of the CDO to ensure alignment with their investment objectives and client expectations.

Other significant buyers include insurance companies and pension funds, which, due to their long-term liability profiles, are often attracted to the stable, predictable cash flows and enhanced yields offered by investment-grade CDO tranches. They typically prioritize capital preservation and consistent income, making them ideal candidates for senior and super-senior CDO segments. Hedge funds, on the other hand, frequently target more junior, higher-risk, and higher-return tranches, often employing complex arbitrage, relative value, or distressed debt strategies to extract alpha. Sovereign wealth funds, with their typically long investment horizons and diverse mandates, may also allocate portions of their portfolios to CDOs as part of a broader strategy to diversify across asset classes and generate stable long-term returns from global credit markets.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 380 Billion |

| Market Forecast in 2033 | USD 560 Billion |

| Growth Rate | 5.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | JPMorgan Chase & Co., Citigroup Inc., Bank of America Merrill Lynch, Goldman Sachs Group Inc., Morgan Stanley, Wells Fargo & Company, Credit Suisse Group AG, Deutsche Bank AG, Barclays PLC, UBS Group AG, BNP Paribas SA, Natixis SA, Société Générale SA, BlackRock Inc., PIMCO, Apollo Global Management Inc., KKR & Co. Inc., Blackstone Inc., Ares Management Corporation, Prudential Financial Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Collateralized Debt Obligation market's technological landscape is rapidly evolving, driven by the need for enhanced risk management, greater transparency, and operational efficiency, especially in the wake of past financial crises and increasing regulatory demands. A cornerstone of this landscape is the extensive use of sophisticated financial modeling software. These platforms utilize advanced statistical methods and quantitative models to price CDO tranches, simulate cash flow waterfalls, and conduct complex scenario analyses under various economic conditions. Tools for Monte Carlo simulations, Gaussian copula models, and other correlation-based models are crucial for assessing the interdependencies and default probabilities of the underlying collateral, allowing for a more nuanced understanding of risk and return profiles across the CDO structure. These technologies empower structurers and investors to navigate securitized product complexities with greater precision.

The advent and growing maturity of Artificial Intelligence (AI) and Machine Learning (ML) are significantly transforming how CDOs are managed and analyzed. AI/ML algorithms are being deployed for predictive analytics, offering superior capabilities in forecasting collateral performance, identifying early signs of credit deterioration, and optimizing asset selection within CDO pools. These technologies can process vast amounts of unstructured and structured data, including market news, economic indicators, and issuer financials, to uncover subtle patterns and correlations that human analysts might miss. Furthermore, AI-driven automation is increasingly applied to operational processes, such as data reconciliation, compliance checks, and report generation, thereby reducing manual errors, improving efficiency, and freeing up human capital for more strategic tasks. The integration of big data analytics complements AI/ML by providing the necessary infrastructure to handle and interpret the enormous datasets characteristic of the credit markets.

Beyond traditional and AI-driven tools, emerging technologies like blockchain are poised to introduce a new paradigm of transparency and efficiency to the CDO market. Blockchain's distributed ledger technology could revolutionize the lifecycle of CDOs by providing an immutable, tamper-proof record of all underlying assets, ownership transfers, and payment flows. This would significantly reduce the need for intermediaries, enhance trust among participants, and potentially lower operational costs associated with auditing and reconciliation. Smart contracts, built on blockchain platforms, could automate the execution of complex CDO tranche payments and default triggers, improving speed and accuracy. While still in its nascent stages of adoption within structured finance, the potential for blockchain to create a more transparent, efficient, and resilient CDO market is substantial, paving the way for enhanced investor confidence and reduced systemic risk. Automated trading platforms are also integral, allowing for efficient execution of CDO trades in the secondary market.

The Collateralized Debt Obligation market demonstrates distinct characteristics and varying levels of activity across major global regions, reflecting diverse economic conditions, regulatory environments, and investor preferences. Understanding regional nuances is crucial for identifying growth opportunities, assessing localized risks, and tailoring strategies effectively. Each region contributes uniquely to the global CDO landscape, shaped by historical developments, domestic financial infrastructure maturity, and the specific needs of local institutional investor bases. The fragmented nature of global financial regulations also plays a significant role in dictating the types of CDOs that can be structured and the extent of their issuance and adoption within different jurisdictions, leading to a patchwork of market activity and product innovation.

A Collateralized Debt Obligation (CDO) is a complex structured finance product pooling various types of debt, like corporate bonds or mortgages, then slicing this into tranches with varying risk and return. Investors purchase these tranches, receiving payments from the underlying collateral. Tranches are prioritized in payment, with senior tranches having lower risk and returns, while junior tranches bear higher risk for potentially higher returns. This structuring allows for diversified credit risk exposure and provides investors with tailored access to credit markets based on their risk appetite, transforming illiquid assets into tradable securities by securitizing cash flows.

Main CDO types include Cash CDOs, backed by cash-generating assets like corporate loans (CLOs), mortgage-backed securities (MBS), or other asset-backed securities (ABS). Synthetic CDOs use credit default swaps (CDS) to transfer credit risk without physical asset transfer. Hybrid CDOs combine both. Underlying assets vary widely, from broadly syndicated leveraged loans, residential and commercial mortgages, auto loans, and credit card receivables, to esoteric assets like intellectual property royalties. The asset type largely determines the CDO's risk profile and sensitivity to market factors, making asset quality and diversity critical for all participants.

The 2008 financial crisis profoundly impacted the CDO market, especially those backed by subprime mortgages, causing massive losses and investor confidence erosion. The crisis exposed excessive complexity, opacity, and interconnectedness in some CDO structures, hindering risk assessment. Since then, stringent regulatory reforms like Dodd-Frank and CRD IV/CRR introduced stricter capital requirements, risk retention rules, and transparency mandates. Issuance volumes decreased, and there is a renewed focus on simpler, more transparent structures, higher collateral quality, and active management, particularly within the CLO segment, which has shown greater resilience and recovery due to its corporate loan collateral.

Technology, particularly Artificial Intelligence (AI) and Machine Learning (ML), significantly enhances efficiency, transparency, and risk management in the modern CDO market. AI algorithms are deployed for advanced predictive analytics, improving credit risk assessments for collateral, forecasting default probabilities, and identifying complex correlations. This leads to more precise pricing and valuation of CDO tranches. AI also automates critical operational processes like collateral monitoring, compliance reporting, and fraud detection, reducing errors and increasing efficiency. Emerging technologies like blockchain hold promise for future enhancements in transparency and auditability through immutable records and smart contracts, strengthening investor confidence and streamlining transaction lifecycles.

Primary investors in Collateralized Debt Obligations are sophisticated institutional entities capable of managing complex instruments and risks. This diverse group includes commercial banks and investment banks, often investing in senior, lower-risk tranches for balance sheet management and regulatory capital. Asset managers, including large mutual funds and specialized structured credit funds, participate for yield enhancement and portfolio diversification. Hedge funds are prominent, frequently targeting higher-risk, higher-return mezzanine and equity tranches through complex strategies. Additionally, long-term investors like pension funds and insurance companies invest in highly-rated CDO tranches seeking stable, predictable income streams to match their liabilities and optimize risk-adjusted returns.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.