ID : MRU_ 443875 | Date : Feb, 2026 | Pages : 255 | Region : Global | Publisher : MRU

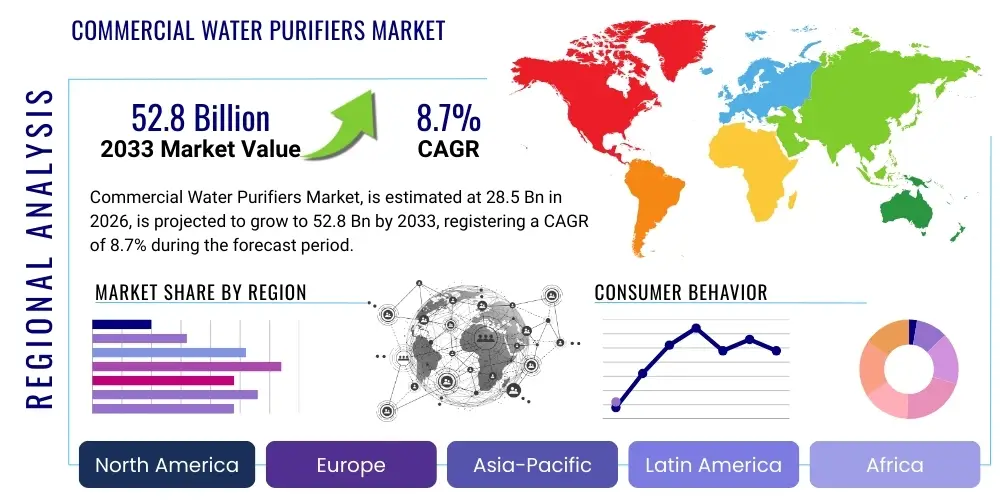

The Commercial Water Purifiers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2026 and 2033. The market is estimated at USD 28.5 Billion in 2026 and is projected to reach USD 52.8 Billion by the end of the forecast period in 2033.

The Commercial Water Purifiers Market encompasses advanced filtration and treatment systems designed for non-residential applications, including hospitality, healthcare, manufacturing, education, and corporate sectors. These sophisticated systems are engineered to address specific water quality challenges prevalent in commercial environments, ranging from sediment removal and chemical purification to microbiological pathogen inactivation. Unlike residential units, commercial purifiers are characterized by their high capacity, robust construction, and ability to meet stringent regulatory standards for water quality. They employ a diverse array of technologies, such as reverse osmosis (RO), ultraviolet (UV) sterilization, ultrafiltration (UF), activated carbon filtration, and advanced oxidation processes, often integrated into multi-stage systems to deliver purified water suitable for various operational needs, including drinking, cooking, process water, and laboratory applications.

The primary benefit of deploying commercial water purifiers extends beyond merely providing safe drinking water; it significantly contributes to operational efficiency, cost savings, and enhanced brand reputation for businesses. For instance, in the food and beverage industry, purified water directly impacts the quality and consistency of products, while in healthcare, it is crucial for patient safety and equipment sterilization. Major applications span from ensuring potable water for employees and customers in offices and restaurants to critical process water in pharmaceutical manufacturing and semiconductor fabrication. The driving factors propelling this market's growth are manifold, including the escalating concerns over municipal water quality, the stringent regulatory landscape mandating safe water use in various industries, the growing awareness among businesses about the health benefits for their workforce and customers, and the continuous technological advancements making purification systems more efficient, reliable, and sustainable.

Furthermore, the increasing global industrialization and urbanization contribute to higher demand for reliable and high-quality water sources across diverse commercial establishments. Businesses are recognizing the long-term economic advantages of investing in robust water purification infrastructure, such as reduced maintenance costs for machinery, improved product quality, and compliance with environmental and health standards. The integration of smart technologies, offering real-time monitoring and predictive maintenance, further enhances the appeal of these systems, positioning commercial water purifiers as an indispensable asset for modern enterprises aiming for operational excellence and sustainability.

The Commercial Water Purifiers Market is experiencing robust expansion, driven by critical business trends such as the increasing demand for high-quality water across industries, a heightened focus on health and hygiene, and the pervasive integration of smart technologies. Businesses are prioritizing sustainable water management, leading to a surge in the adoption of advanced filtration solutions that offer not only superior purification but also optimized resource utilization. Customization and modularity in system design are emerging as key trends, enabling businesses to tailor purification solutions to their specific operational requirements and water quality challenges. Furthermore, the shift towards service-based models, where providers offer installation, maintenance, and monitoring as part of a comprehensive package, is gaining traction, alleviating the burden of ownership for end-users.

Regionally, the market exhibits diverse growth dynamics. Asia-Pacific stands out as a dominant and rapidly expanding region, fueled by rapid industrialization, urbanization, increasing disposable incomes, and growing awareness regarding waterborne diseases, particularly in countries like China and India. North America and Europe, characterized by stringent regulatory frameworks and a strong emphasis on technological innovation and environmental compliance, continue to witness steady growth, with a focus on advanced and energy-efficient systems. Emerging economies in Latin America, the Middle East, and Africa are showing significant potential, driven by improving infrastructure, increasing commercial investments, and addressing acute water scarcity issues. Each region's unique socio-economic landscape and regulatory environment profoundly influence the types of purifiers demanded and the pace of market development, with a global trend towards decentralized water treatment solutions.

In terms of segment trends, the Reverse Osmosis (RO) technology segment maintains a significant market share due to its effectiveness in removing a broad spectrum of contaminants, including dissolved solids and heavy metals, making it ideal for diverse commercial applications. However, other technologies like Ultraviolet (UV) sterilization and Ultrafiltration (UF) are also experiencing substantial growth, often integrated into multi-stage systems for enhanced purification against specific microbial and particulate threats. The end-user segment of Hospitality (Hotels, Restaurants, Cafes - HORECA) and Healthcare is projected to demonstrate remarkable growth due to their immediate need for high-quality, safe water for consumption and operational processes. The industrial sector, including food and beverage, pharmaceuticals, and manufacturing, continues to be a cornerstone of demand, driven by stringent product quality standards and process efficiency requirements. The market is also witnessing a trend towards larger capacity systems to meet the increasing water demands of growing commercial establishments.

The integration of Artificial Intelligence (AI) into the commercial water purifiers market represents a transformative shift, addressing critical user questions around efficiency, reliability, and proactive management. Users are particularly keen on understanding how AI can enhance the performance of purification systems, optimize operational costs, and minimize downtime through predictive capabilities. Common inquiries revolve around the ability of AI to monitor water quality in real-time, predict maintenance needs before failures occur, and automatically adjust purification processes for optimal output and energy consumption. Furthermore, there is significant interest in how AI can contribute to data-driven decision-making, providing actionable insights into water usage patterns, contaminant levels, and system health. The overarching themes reflect a desire for smarter, more autonomous, and highly efficient water purification solutions that can adapt to changing conditions and reduce the human intervention required for complex operations.

AI's influence is particularly evident in the development of smart water purifiers that can leverage machine learning algorithms to analyze vast datasets collected from sensors regarding water quality, flow rates, and component wear. This analytical prowess enables systems to self-diagnose potential issues, schedule proactive maintenance, and even communicate directly with service providers, significantly reducing unexpected breakdowns and extending the lifespan of equipment. Users are looking for solutions that not only purify water but also provide a comprehensive ecosystem for water management, offering unparalleled transparency and control over their water infrastructure. The capacity for AI to learn from historical data and optimize parameters such as filter backwashing cycles, membrane flushing, and chemical dosing leads to substantial savings in water, energy, and consumable costs, directly addressing businesses' financial and environmental sustainability goals. The ability to automatically adapt to variations in raw water quality ensures consistent output purity without constant manual adjustments, a major concern for commercial operators.

Moreover, AI is pivotal in enhancing the security and resilience of commercial water supply systems. By continuously analyzing operational data and identifying anomalies, AI can detect potential contamination events or system breaches faster than traditional monitoring methods, enabling swift responses to mitigate risks. This level of intelligent oversight provides an added layer of assurance for businesses, especially those in sensitive sectors like healthcare and pharmaceuticals, where water quality is paramount for regulatory compliance and public health. The future trajectory of AI in this market points towards increasingly autonomous systems that can not only purify but also intelligently manage the entire water cycle within a commercial facility, from source water intake to wastewater discharge, optimizing every stage for efficiency, safety, and environmental responsibility, thereby setting new benchmarks for operational excellence.

The Commercial Water Purifiers Market is significantly influenced by a dynamic interplay of drivers, restraints, and opportunities, alongside broader impact forces that shape its growth trajectory and competitive landscape. A primary driver is the accelerating deterioration of municipal water quality globally, stemming from industrial pollution, agricultural runoff, and aging infrastructure, which compels businesses to seek independent and reliable purification solutions. Coupled with this, the increasing awareness regarding the health implications of contaminated water among consumers and employees, alongside stringent regulatory mandates imposed by health authorities for various commercial sectors, further boosts demand. Rapid industrialization and urbanization in emerging economies also contribute, as more commercial establishments require purified water for operational processes and daily consumption. Furthermore, continuous technological advancements, particularly in membrane technology, smart monitoring, and energy efficiency, make commercial purifiers more effective, sustainable, and appealing to a wider range of businesses.

However, the market faces several significant restraints that could impede its growth. The high initial capital investment required for installing advanced commercial water purification systems can be a deterrent for small and medium-sized enterprises (SMEs) with limited budgets. Operational complexities, including the need for regular maintenance, filter replacements, and technical expertise for troubleshooting, also present challenges. In some developing regions, a lack of widespread awareness regarding the long-term benefits of commercial purification and the availability of affordable, high-quality systems can limit adoption. Additionally, the energy consumption associated with certain purification technologies, such as Reverse Osmosis, raises concerns regarding operational costs and environmental impact, pushing for the development of more energy-efficient alternatives.

Despite these challenges, numerous opportunities are emerging within the market. The vast untapped potential in developing and underdeveloped regions, where water quality issues are acute and commercial infrastructure is rapidly expanding, presents significant growth avenues. The increasing trend towards decentralized water treatment solutions, driven by their efficiency and resilience, offers new market penetration strategies. Furthermore, the growing focus on sustainability and eco-friendly practices across industries is creating demand for purifiers that minimize waste and energy footprint, including advanced membrane technologies and water recycling systems. The integration of IoT, AI, and cloud-based analytics for smart water management systems represents a considerable opportunity for value addition, enabling predictive maintenance, real-time monitoring, and enhanced operational efficiency. The impact forces, such as the moderate bargaining power of buyers due to diverse product offerings and intense competition, and the bargaining power of suppliers being influenced by the proprietary nature of certain purification technologies, continuously shape market dynamics. The threat of new entrants is moderate, given the capital intensity and regulatory hurdles, while the threat of substitutes, though present from bottled water or alternative supply sources, is mitigated by the scale and economic benefits of on-site purification for commercial entities. Intense competitive rivalry among established players and innovative startups drives continuous innovation and market expansion.

The Commercial Water Purifiers Market is comprehensively segmented based on various critical attributes, including technology, capacity, end-user industry, and distribution channel, providing a granular understanding of market dynamics and growth potential across different verticals. This detailed segmentation allows stakeholders to identify specific market niches, tailor product offerings, and devise effective market entry and expansion strategies. Each segment exhibits unique demand drivers, technological preferences, and growth trajectories, reflecting the diverse requirements of commercial establishments for purified water. The technological segmentation, for instance, highlights the prevalence and evolution of various purification methods, while end-user segmentation reveals the industries with the highest adoption rates and specific water quality needs. This structured approach to market analysis ensures that all facets of the commercial water purification landscape are thoroughly examined, from the fundamental purification mechanisms to the final consumption points, illustrating the intricate web of supply and demand.

The market's segmentation by technology is crucial as it dictates the efficacy against specific contaminants, operational costs, and suitability for different applications. Reverse Osmosis (RO) remains a dominant segment due to its unparalleled ability to remove dissolved solids, heavy metals, and microorganisms, making it indispensable for critical applications in healthcare and manufacturing. However, Ultraviolet (UV) sterilization systems are rapidly gaining traction, particularly where microbial contamination is the primary concern, offering a chemical-free and energy-efficient solution. Ultrafiltration (UF) and microfiltration (MF) are valued for their effectiveness in removing suspended solids, bacteria, and viruses without removing essential minerals, suitable for general commercial use. Activated Carbon and sediment filters are often employed as pre-treatment stages or standalone units for improving taste, odor, and chlorine removal. The emergence of multi-stage hybrid systems, combining various technologies, addresses complex water quality challenges and offers a holistic approach to purification, catering to the demand for comprehensive solutions.

Further segmentation by end-user industry illustrates the diverse needs across different commercial sectors. The Hospitality (HORECA) sector, encompassing hotels, restaurants, and cafes, represents a significant segment due to the high demand for safe drinking water, ice production, and culinary applications. The Healthcare sector, including hospitals, clinics, and laboratories, requires ultra-pure water for sterilization, medical processes, and diagnostics, making it a critical segment with stringent quality requirements. Industrial applications, such as food and beverage processing, pharmaceuticals, electronics manufacturing, and chemical industries, necessitate specific water purities for their respective production processes, driving demand for specialized and high-capacity systems. Educational institutions, corporate offices, and retail establishments also constitute substantial end-user segments, prioritizing health and wellness for their occupants. Understanding these distinct requirements is vital for manufacturers and service providers to develop targeted solutions and marketing strategies that resonate with each specific commercial client base.

A comprehensive value chain analysis for the Commercial Water Purifiers Market reveals the intricate network of activities and stakeholders involved in bringing purification solutions from raw materials to end-users, ultimately creating value at each stage. This analysis begins with the upstream segment, which involves the sourcing and processing of critical raw materials and components. This foundational stage includes manufacturers of membranes (RO, UF, MF), filter media (activated carbon, sediment), pumps, pressure vessels, electronic controls, and specialized plastics and metals. Key players in this segment focus on material science innovation, cost efficiency, and ensuring the consistent quality of components, as these directly impact the performance and longevity of the final purification systems. The bargaining power of these suppliers can be significant, especially for proprietary technologies or high-quality, specialized components, influencing the overall cost structure of commercial purifiers.

Moving downstream, the value chain progresses through the manufacturing and assembly of the purification systems themselves. This stage is dominated by commercial water purifier manufacturers who integrate various components, develop proprietary designs, and often specialize in specific technologies or end-user applications. Value addition here comes from research and development (R&D) in system design, efficiency enhancements, smart technology integration (IoT, AI), and quality control. Following manufacturing, the products enter the distribution channels, which are crucial for market reach and customer accessibility. These channels can be direct, where manufacturers sell and install systems directly to large commercial clients, or indirect, involving a network of distributors, resellers, and specialized water treatment service providers. Indirect channels often provide localized support, installation services, and post-sales maintenance, which are critical for commercial clients who require reliable and continuous operation.

The final stages of the value chain involve installation, operation, and extensive after-sales support, including maintenance, spare parts supply, and performance monitoring. Service providers and authorized dealers play a vital role in ensuring that commercial purifiers operate optimally throughout their lifecycle, providing technical assistance, scheduled maintenance, and emergency repairs. This downstream segment is characterized by strong customer relationships and recurring revenue streams through service contracts. The efficiency and reliability of this support significantly influence customer satisfaction and loyalty. The entire value chain is underpinned by logistics and supply chain management, ensuring timely delivery of components and finished products. Understanding these dynamics helps identify areas for cost optimization, quality improvement, and strategic partnerships, enhancing the overall competitive advantage within the Commercial Water Purifiers Market.

The Commercial Water Purifiers Market caters to a diverse and extensive base of potential customers, spanning across virtually every sector that requires high-quality, reliable, and voluminous sources of purified water for their operations, employees, or patrons. These end-users are not merely seeking basic filtration; they demand tailored solutions that address specific water quality challenges, meet stringent regulatory standards, and contribute to their overall operational efficiency and brand reputation. Key segments of potential customers include the vast Hospitality sector, comprising hotels, resorts, restaurants, cafes, and catering businesses. In these environments, purified water is essential for drinking, cooking, ice production, dishwashing, and even specialized applications like coffee and tea brewing, directly impacting customer experience and food safety. Ensuring a consistent supply of safe and great-tasting water is a critical differentiator for businesses in this highly competitive industry, driving a continuous need for robust purification systems.

Another significant group of potential customers resides within the Healthcare and Pharmaceutical industries. Hospitals, clinics, dental offices, laboratories, and pharmaceutical manufacturing plants have some of the most rigorous water quality requirements. Purified water is indispensable for surgical procedures, dialysis, sterilization of medical equipment, laboratory testing, and as a critical ingredient in drug formulation. Any compromise in water purity can have severe consequences for patient safety and product integrity, making commercial water purifiers an absolute necessity rather than a luxury. These customers often require systems capable of producing ultra-pure water, free from bacteria, viruses, pyrogens, and dissolved solids, often necessitating multi-stage purification processes involving technologies like RO, UV, and deionization.

Furthermore, the industrial sector represents a broad and varied customer base for commercial water purifiers. This includes manufacturing facilities across diverse verticals such as food and beverage processing, electronics manufacturing (e.g., semiconductor production), chemical industries, and textiles. In the food and beverage sector, purified water is a primary ingredient and is used extensively for cleaning, blending, and bottling, directly impacting product quality and shelf life. Electronics manufacturing requires ultra-pure water to prevent contamination of sensitive components. Beyond these specific industries, general commercial establishments like corporate offices, educational institutions (schools, colleges, universities), fitness centers, and government buildings also constitute significant potential customers. They prioritize providing safe drinking water for their employees, students, and visitors, ensuring a healthy and productive environment. This wide spectrum of needs underscores the versatility and indispensable nature of commercial water purification solutions across the modern economic landscape.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 52.8 Billion |

| Growth Rate | 8.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Evoqua Water Technologies, Veolia Water Technologies, Suez SA, Xylem Inc., Pentair plc, Culligan International, 3M Company, Dow Water & Process Solutions, A. O. Smith Corporation, LG Electronics, Panasonic Corporation, Honeywell International Inc., Parker Hannifin Corporation, Watts Water Technologies, Ecowater Systems LLC, Kinetico Incorporated, Waterlogic plc, Best Water Technology AG (BWT), Lenntech B.V., Pureflow, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Commercial Water Purifiers Market is dynamic and continuously evolving, driven by the escalating demand for higher purification standards, enhanced efficiency, and sustainable solutions. At its core, the market is characterized by a blend of established and emerging technologies, often integrated into sophisticated multi-stage systems to address a wide spectrum of contaminants. Reverse Osmosis (RO) remains a cornerstone technology, renowned for its ability to effectively remove dissolved salts, heavy metals, bacteria, and viruses through a semi-permeable membrane. Advancements in RO membrane materials and configurations are leading to improved flux rates, reduced fouling, and lower energy consumption, making RO systems more efficient and economical for commercial applications requiring ultra-pure water, such as in the pharmaceutical and electronics industries.

Alongside RO, Ultraviolet (UV) sterilization plays a critical role, offering a chemical-free method to inactivate bacteria, viruses, and other microorganisms by disrupting their DNA. Innovations in UV technology include advanced UV-C lamps with longer lifespans and higher germicidal efficacy, often integrated into point-of-entry or point-of-use systems to provide an immediate barrier against microbial contaminants. Ultrafiltration (UF) and Microfiltration (MF) technologies are also widely employed, utilizing physical barriers to remove suspended solids, particulates, and larger microorganisms, serving as effective pre-treatment stages or standalone solutions for applications where mineral retention is desired. Furthermore, activated carbon filters are indispensable for removing chlorine, organic compounds, and improving water's taste and odor, frequently used in conjunction with other technologies to enhance overall water quality. Sediment filters, typically the first line of defense, efficiently remove larger particles like sand, rust, and silt, protecting downstream components and extending their lifespan.

A significant trend in the modern technology landscape is the integration of digital technologies, most notably the Internet of Things (IoT), Artificial Intelligence (AI), and cloud computing. These smart technologies enable real-time monitoring of water quality parameters, system performance, and predictive maintenance scheduling. IoT sensors gather data on flow rates, pressure, temperature, and contaminant levels, which AI algorithms then analyze to optimize purification processes, detect anomalies, and even automate adjustments for peak efficiency. This leads to more reliable operations, reduced operational costs, and proactive problem-solving, moving beyond traditional manual oversight. Additionally, advancements in sustainable technologies, such as improved wastewater recycling techniques, energy recovery devices in RO systems, and greener membrane cleaning agents, are gaining traction, reflecting the industry's commitment to environmental responsibility. The convergence of these diverse technologies allows for highly customizable, resilient, and intelligent commercial water purification solutions tailored to the precise demands of various industrial and commercial sectors, ensuring both high-quality water output and operational excellence.

The global Commercial Water Purifiers Market demonstrates distinct regional dynamics, influenced by varying levels of industrialization, regulatory frameworks, water scarcity challenges, and consumer awareness regarding water quality. Each major geographical region contributes uniquely to the market's growth and technological adoption. North America, encompassing the United States and Canada, represents a mature market characterized by stringent water quality regulations and a high adoption rate of advanced purification technologies. The region benefits from significant investments in research and development, leading to innovations in smart water purifiers and sustainable treatment solutions. Industries such as healthcare, food and beverage, and pharmaceuticals drive substantial demand, coupled with a strong emphasis on operational efficiency and compliance. The market here is competitive, with a focus on comprehensive service contracts and customized solutions to meet diverse commercial needs.

Europe, including key economies like Germany, the UK, France, and Italy, is another prominent market, distinguished by its robust environmental protection policies and strong emphasis on sustainability. European businesses are increasingly investing in energy-efficient and eco-friendly water purification systems to comply with strict EU directives and corporate social responsibility initiatives. The region sees strong demand from the HORECA sector, manufacturing, and municipal buildings, driven by concerns over public health and water resource management. Technological innovation, particularly in membrane filtration and water recycling, is a key characteristic, with a growing trend towards decentralized and modular purification systems. The Middle East and Africa (MEA) region is experiencing rapid growth, primarily driven by increasing water scarcity, fast-paced urbanization, and significant government investments in infrastructure development, particularly in GCC countries. Large-scale commercial projects, coupled with the need for reliable water sources in arid environments, fuel the demand for high-capacity and robust purification systems. Investment in desalination and advanced filtration technologies is particularly strong, aiming to secure sustainable water supplies for commercial and industrial expansion.

Asia Pacific (APAC), comprising economic powerhouses like China, India, Japan, South Korea, and Australia, is poised to be the fastest-growing and largest market for commercial water purifiers. This growth is propelled by rapid industrialization, burgeoning population growth, increasing urbanization, and a rise in health consciousness among businesses and consumers. Countries like China and India face significant challenges with water pollution, leading to a massive demand for effective purification solutions across manufacturing, food and beverage, and healthcare sectors. Government initiatives to improve water infrastructure and regulate industrial discharges further stimulate market growth. Latin America, including Brazil, Mexico, and Argentina, represents an emerging market with considerable potential. Improving economic conditions, coupled with expanding commercial and industrial sectors, are driving the adoption of water purification systems. While still developing, the region is witnessing increasing awareness about water quality and a gradual shift towards investing in reliable purification technologies to support economic development and public health initiatives. Each region's unique blend of challenges and opportunities necessitates tailored market approaches and product offerings from industry players.

Commercial water purifiers are designed for high-volume, continuous operation and greater capacity, typically serving businesses with specific and often stringent water quality requirements for drinking, process water, or specialized applications like healthcare. They are more robust, offer advanced filtration stages, and often include monitoring and management systems suitable for industrial-scale use, unlike residential units built for smaller-scale household consumption.

The main technologies include Reverse Osmosis (RO) for removing dissolved solids and heavy metals, Ultraviolet (UV) sterilization for microbial inactivation, Ultrafiltration (UF) and Microfiltration (MF) for particulate and larger microorganism removal, and Activated Carbon filters for enhancing taste, odor, and chlorine reduction. Many commercial systems integrate these technologies into multi-stage processes for comprehensive purification.

Key benefits include ensuring the health and safety of employees and customers, complying with industry-specific water quality regulations, improving product quality and consistency (especially in food and beverage or pharmaceuticals), reducing operational costs associated with bottled water or equipment maintenance from poor water, and enhancing brand reputation through a commitment to quality and sustainability.

AI is transforming commercial purifiers by enabling real-time water quality monitoring, predictive maintenance to prevent failures, automated optimization of purification processes for energy and water efficiency, and smart fault detection. This leads to reduced downtime, lower operational costs, consistent water quality, and a more sustainable overall water management system for businesses.

The market is driven by deteriorating municipal water quality, stringent regulatory standards for commercial water use, increasing health and hygiene awareness among businesses, rapid industrialization and urbanization in emerging economies, and continuous technological advancements making purifiers more efficient and intelligent. These factors collectively push commercial entities to invest in reliable purification solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.