ID : MRU_ 442760 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

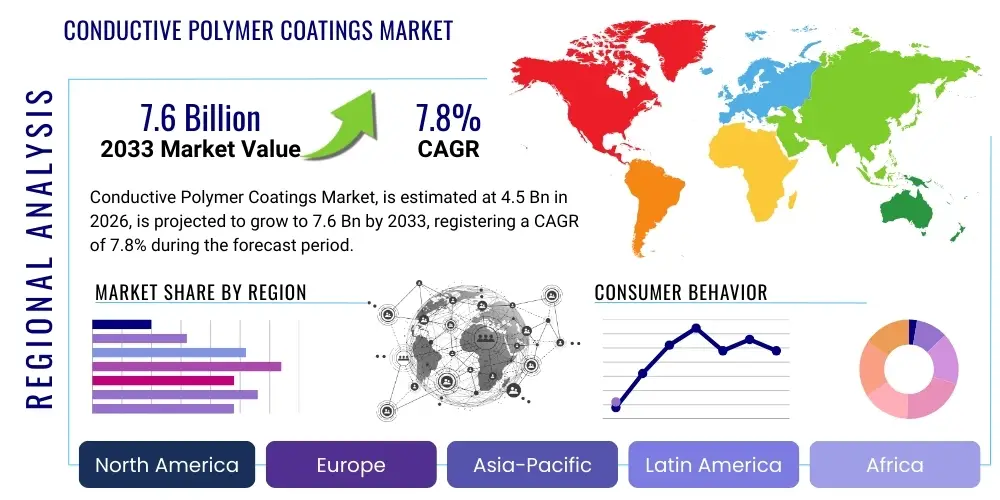

The Conductive Polymer Coatings Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 4.5 billion in 2026 and is projected to reach USD 7.6 billion by the end of the forecast period in 2033. This growth trajectory is fundamentally supported by the escalating demand for advanced materials offering superior electromagnetic interference (EMI) shielding capabilities, particularly within the burgeoning consumer electronics and automotive electrification sectors. The versatility of these coatings, encompassing applications from anti-static protection in sensitive manufacturing environments to highly efficient electrodes in energy storage devices, solidifies their critical role in future technological infrastructure. Furthermore, ongoing research and development aimed at improving the processability, stability, and cost-effectiveness of these materials, such as intrinsically conductive polymers (ICPs) like PEDOT:PSS, are expected to significantly broaden their industrial adoption over the coming years, positioning the market for sustained expansion.

The Conductive Polymer Coatings Market encompasses specialized surface modification solutions that leverage intrinsically conductive polymers (ICPs) or polymer matrices laden with conductive fillers (such as carbon nanotubes, graphene, or metallic particles) to impart electrical conductivity or electrostatic dissipation (ESD) properties to substrates. These coatings are utilized across diverse industries to achieve functionalities unattainable with conventional insulating materials, ranging from electromagnetic compatibility (EMC) in electronic assemblies to enhanced performance in flexible printed circuit boards (FPCBs) and solar panels. Conductive polymer coatings offer distinct advantages over traditional metal coatings, including lighter weight, inherent corrosion resistance, and greater flexibility, making them essential materials for miniaturization and performance enhancement in modern technological devices. Their ability to be processed through conventional coating techniques, such as spray coating, dipping, or printing, further drives their widespread industrial application.

Product descriptions typically center on the type of conductive polymer employed, with Polyaniline (PANI), Polypyrrole (PPy), and Poly(3,4-ethylenedioxythiophene) (PEDOT) being the dominant classes due to their high intrinsic conductivity and relatively good environmental stability. Major applications span critical infrastructure areas including advanced semiconductor manufacturing, where anti-static properties are mandatory; telecommunications, requiring robust EMI shielding against signal degradation; and the aerospace sector, demanding lightweight materials with high electrical integrity. The inherent flexibility of these polymer systems also positions them as pivotal components in the rapidly expanding fields of flexible electronics and wearable technology, facilitating the creation of truly conformable electronic devices without compromising performance or durability. These advanced applications underscore the high-value proposition of conductive polymer coatings in future-proof material science.

The primary benefits derived from the deployment of conductive polymer coatings include enhanced device reliability through effective static charge dissipation, improved regulatory compliance concerning EMI/RFI emissions, and optimized operational efficiency in energy-related applications like batteries and supercapacitors. Key driving factors propelling market expansion include the exponential growth in consumer electronics production, particularly smart devices and IoT components, which necessitates superior EMI shielding in compact form factors. Furthermore, the global shift toward electric vehicles (EVs) significantly boosts demand for corrosion-resistant, lightweight conductive materials for battery pack components and sensor housing. Technological advancements leading to the synthesis of highly stable and processable ICPs are continuously lowering application barriers, making these coatings accessible to broader industrial segments and maintaining robust market growth momentum.

The Conductive Polymer Coatings Market is exhibiting robust growth, propelled primarily by macro-level business trends centered on digitalization, electrification, and miniaturization across global manufacturing sectors. The transition from bulk electronics to integrated, high-frequency devices has created an indispensable requirement for advanced shielding and ESD solutions, directly benefiting the conductive polymer segment. Business trends indicate a strong move towards environmentally sustainable and solvent-free coating systems, aligning with stringent global environmental regulations, which favors water-borne conductive polymers, such as certain PEDOT:PSS formulations. Furthermore, strategic alliances between chemical manufacturers and electronics OEMs are accelerating innovation, leading to specialized coatings optimized for specific substrate requirements, particularly for flexible substrates utilized in wearable technology and bendable displays. This collaborative approach is proving essential for achieving the stringent performance characteristics required in cutting-edge applications.

Regionally, the Asia Pacific (APAC) continues to dominate the market, driven by its unparalleled manufacturing capacity for consumer electronics, automotive components, and solar energy infrastructure, particularly in China, South Korea, and Taiwan. Significant investments in 5G network deployment and the concomitant surge in data center construction within APAC further amplify the need for advanced conductive materials for heat dissipation and signal integrity. North America and Europe, while mature, demonstrate strong growth in high-value segments like aerospace, defense, and specialized medical devices, where performance specifications justify higher material costs. These regions are also at the forefront of regulatory changes demanding enhanced electromagnetic compatibility (EMC), thereby securing sustained demand for high-performance conductive coatings. The geographical market dynamic reflects a balance between volume-driven expansion in the East and high-specification, performance-driven growth in the West.

Segmentation trends highlight the increasing dominance of the Electronics end-user segment, primarily for EMI shielding and anti-static applications in high-density integrated circuits and sensitive components. By product type, Poly(3,4-ethylenedioxythiophene) or PEDOT-based coatings are witnessing the fastest adoption rate due to their excellent conductivity, optical transparency, and ease of processing, positioning them favorably against traditional materials. Moreover, the Application segment is seeing a significant uplift in demand for coatings optimized for energy storage, serving as electrode materials or current collectors in next-generation lithium-ion and solid-state batteries. This trend is accelerating the development of highly durable and chemically stable conductive polymer systems capable of sustaining thousands of charge/discharge cycles, proving that the market is rapidly diversifying beyond its traditional static protection role into functional energy components.

User inquiries regarding AI's influence on the Conductive Polymer Coatings Market frequently revolve around optimizing material synthesis, predicting long-term coating performance under stress, and automating quality control processes during large-scale manufacturing. Key concerns include how AI algorithms can accelerate the discovery of novel conductive polymer compositions with enhanced stability and lower synthesis costs, and the potential for AI-driven simulation to replace lengthy, expensive physical testing cycles for application-specific coatings (e.g., aerospace requirements). Users are eager to understand if AI can effectively model the complex interaction between polymer structure, filler concentration, and conductive pathway formation, thereby streamlining R&D pipelines. Expectations are high that AI will significantly reduce the time-to-market for next-generation coatings, especially those targeted at highly specialized fields like flexible OLED fabrication and advanced sensor technology, fundamentally changing the material design paradigm from empirical experimentation to data-driven prediction and optimization.

The incorporation of Artificial Intelligence and Machine Learning (ML) techniques is poised to revolutionize several critical facets of the conductive polymer coatings value chain. In research and development, ML models are being trained on vast datasets of molecular structures and resulting conductive properties to predict the optimal formulation required to achieve specific performance targets, such as conductivity thresholds or environmental durability. This predictive capability drastically reduces the number of experimental iterations, enhancing the efficiency of material innovation. Furthermore, AI is crucial in quality control, employing computer vision and sensor fusion to monitor coating uniformity, thickness, and defect detection in real-time during high-speed production runs. This automated inspection ensures consistent product quality and minimizes material wastage, which is critical given the specialized nature and cost of highly conductive materials.

Beyond material science, AI-driven process optimization is impacting manufacturing logistics and supply chain management within the conductive polymer sector. Machine learning algorithms analyze production parameters—such as curing temperature, dispersion rates, and solvent concentration—to dynamically adjust processes for maximum yield and energy efficiency. This is particularly relevant for maintaining the highly sensitive dispersion stability required when incorporating nanomaterials like graphene or carbon nanotubes into polymer matrices. Moreover, AI aids in demand forecasting by analyzing market trends across diverse end-use sectors (electronics, automotive, healthcare), allowing manufacturers to optimize inventory levels and production schedules for specific conductive polymer types, thus securing operational resilience and responsiveness to fluctuating global market demands.

The dynamics of the Conductive Polymer Coatings Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming the market’s impact forces. A dominant driver is the pervasive trend of miniaturization and increased functional density in consumer electronics, which necessitates highly efficient and thin EMI shielding materials that conductive polymers readily provide. Simultaneously, the global push toward sustainable and lightweight material solutions, especially within the aerospace and electric vehicle industries, bolsters demand. However, the market faces significant restraints, primarily revolving around the relatively high cost of advanced intrinsically conductive polymers compared to traditional metallic fillers, alongside inherent stability challenges, such particularly the sensitivity of certain ICPs to heat, moisture, and chemical degradation, which limits their suitability in harsh industrial environments. Managing these material vulnerabilities remains a crucial technological hurdle requiring persistent research and development investment to overcome the barriers to broader industrial integration.

Opportunities for exponential market growth are abundant, notably within emerging technological domains such as flexible electronics, where conductive polymer coatings are indispensable for creating bendable displays, smart textiles, and wearable biometric sensors. The rapidly expanding field of renewable energy also presents a substantial growth avenue, with conductive polymers serving as transparent conductive electrodes (TCEs) in advanced solar cells and as key components in high-performance supercapacitors and batteries, improving charge transfer efficiency and cycle life. The development of hybrid materials, combining the chemical stability of conventional polymers with the high conductivity of nanomaterials (like graphene or carbon nanotubes), represents a significant impact force, offering a pathway to mitigate existing material instability restraints and unlock high-temperature or highly corrosive application settings that were previously inaccessible to pure ICPs. These opportunities are driving strategic investments in advanced synthesis techniques and coating application methodologies.

The impact forces exerted on the market emphasize the shift towards performance-based differentiation. The need for precise and repeatable conductivity levels across large-area applications, coupled with regulatory pressure concerning hazardous substances (e.g., REACH, RoHS compliance), forces manufacturers to continually innovate and certify their formulations. Successfully navigating these forces requires sustained investment in stability testing, quality assurance protocols, and the scalability of specialized polymer synthesis. Ultimately, the future growth trajectory will be determined by the industry’s ability to address the cost-to-performance ratio and enhance the environmental robustness of conductive polymer coatings, thereby enabling their ubiquitous adoption across both high-end specialized applications and high-volume commercial products, solidifying their competitive advantage over conventional metallic alternatives.

The Conductive Polymer Coatings Market is comprehensively segmented based on Type, Application, and End-User Industry, allowing for a detailed analysis of market dynamics and identifying high-growth niches. This segmentation reflects the chemical diversity of conductive polymers and their functional deployment across various industrial ecosystems. The market is highly specialized, with performance characteristics such as electrical conductivity, optical transparency, and flexibility being key differentiators across segments. The fastest-growing segments typically align with rapid technological innovation, such as the adoption of advanced materials in energy storage and high-frequency communication devices, demanding highly customized coating solutions that cater to stringent regulatory and performance standards. Understanding these segment interactions is crucial for strategic market positioning and product development targeting.

Segmentation by Type reveals distinct market preferences based on required performance and cost constraints. For instance, PEDOT:PSS dominates applications requiring transparency and low sheet resistance, such as touchscreens and flexible displays, while Polyaniline (PANI) and Polypyrrole (PPy) find primary utility in corrosion protection and traditional anti-static coatings due to their robust chemical structures and cost-effectiveness. The application landscape is shifting, moving beyond standard EMI shielding to include specialized functions like conductive inks for printed electronics and bio-compatible coatings for medical devices. End-user segmentation underscores the market's dependence on the electronics industry, yet significant expansion is noted in the automotive sector, driven by the electrification trend requiring lightweight battery components and sophisticated sensor integration, demanding coatings with specific thermal and electrical management capabilities.

The value chain for the Conductive Polymer Coatings Market commences with the Upstream Analysis, which involves the sourcing and refinement of key chemical precursors and raw materials necessary for synthesizing the basic conductive monomers and polymers. This stage requires rigorous quality control, as the purity of these precursors directly impacts the ultimate conductivity and stability of the final coating product. Key activities include the synthesis of monomers (e.g., EDOT for PEDOT:PSS), the production of high-purity conductive fillers (e.g., specialized carbon black, metallic microparticles, or high-aspect-ratio nanomaterials like graphene), and the manufacturing of proprietary dispersing agents and solvents essential for creating stable, coatable formulations. Major chemical companies and specialized material science firms dominate this upstream segment, investing heavily in polymerization research and process scaling to achieve industrial volumes and cost efficiencies necessary to support downstream demand.

The midstream of the value chain is characterized by the formulation and manufacturing of the conductive coatings themselves, where polymerization, compounding, and dispersion technologies are paramount. Coating manufacturers take the raw conductive polymers and fillers and integrate them into solvent or water-borne systems, adjusting viscosity, adhesion properties, and cure profiles to meet specific application requirements. Distribution channels are highly specialized; Direct distribution is common for high-volume, customized industrial applications, particularly those involving major automotive or aerospace clients who require strict supply chain controls and technical support. Indirect distribution, leveraging specialized chemical distributors, agents, and regional coating service providers, caters to smaller volume users and geographically dispersed markets, offering logistical efficiency and localized technical service capabilities crucial for ensuring correct application in diverse manufacturing settings.

Downstream analysis focuses on the application and end-use of the coatings across critical industrial sectors. This stage involves specialized coating equipment and expertise, ensuring precise thickness control and uniform deposition, which are crucial for achieving reliable conductivity and shielding performance. Potential customers, including electronics manufacturers (for PCBs and device housing), automotive Tier 1 suppliers (for sensor casings and battery components), and medical device integrators (for ESD protection in sterile environments), rely heavily on the technical support and certification provided by the coating manufacturers. The feedback loop from the downstream users regarding performance, durability, and compliance requirements drives iterative product improvement upstream, emphasizing the integrated nature of this high-performance materials value chain. Successful market penetration relies on providing not just the material, but comprehensive application knowledge.

The primary potential customers and end-users of conductive polymer coatings span across several high-technology and high-value manufacturing sectors, where electrical function, reliability, and lightweight characteristics are non-negotiable requirements. The largest segment of buyers resides within the Electronics and Semiconductor manufacturing industries. These customers require conductive polymer coatings primarily for electromagnetic interference (EMI) shielding of integrated circuits and device enclosures to ensure signal integrity and compliance with regulatory electromagnetic compatibility (EMC) standards. Furthermore, these coatings are indispensable in cleanroom environments for anti-static (ESD) protection, preventing damage to sensitive components during assembly and handling processes, thus encompassing both original equipment manufacturers (OEMs) and contract electronics manufacturers (CEMs).

Another significant customer base is found within the Automotive and Transportation sector, driven by the global transition to electric vehicles (EVs) and advanced driver-assistance systems (ADAS). Automotive buyers utilize these coatings for lightweight corrosion protection on battery pack components, internal shielding for complex infotainment systems, and as current collectors for next-generation energy storage solutions. Similarly, the Aerospace and Defense industries represent a high-value customer segment, demanding highly durable, lightweight, and radar-absorbent conductive coatings for sensitive electronic systems, satellite components, and aircraft structures, where adherence to rigorous material specifications and long service life under extreme environmental conditions is mandatory for procurement.

Emerging key buyers are strongly represented in the Healthcare and Energy sectors. Healthcare end-users, including medical device manufacturers and diagnostic equipment providers, require bio-compatible and anti-static conductive coatings for monitoring equipment, surgical tools, and wearable diagnostic patches. In the Energy sector, solar panel manufacturers and battery producers are increasingly adopting specialized conductive polymer coatings to enhance the efficiency and lifespan of photovoltaic cells and internal battery components (anodes and cathodes), seeking materials that improve charge transfer dynamics and reduce internal resistance. These diverse end-user applications highlight the critical role of conductive polymers as functional materials enabling next-generation technology development across multiple vertical markets.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 billion |

| Market Forecast in 2033 | USD 7.6 billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Dow Inc., Covestro AG, PPG Industries, Akzo Nobel N.V., Henkel AG & Co. KGaA, 3M Company, Sika AG, The Lubrizol Corporation, Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd., BASF SE, KCC Corporation, Mitsubishi Chemical Corporation, Sumitomo Chemical Co., Ltd., Heraeus Group, Parker-Hannifin Corp., Trelleborg AB, Merck KGaA, Exatec LLC, RTP Company. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Conductive Polymer Coatings Market is defined by continuous advancements focused on increasing conductivity while enhancing stability, processability, and environmental compatibility. A core technological area involves the refinement of intrinsically conductive polymers (ICPs), specifically improving the doping process for PEDOT:PSS to boost conductivity to levels comparable with metallic materials, which is crucial for applications like transparent conductive electrodes (TCEs). Furthermore, significant innovation is centered on developing water-borne and solvent-free coating formulations to meet stringent environmental regulations, requiring sophisticated dispersion techniques to ensure the uniform distribution of conductive species without sacrificing performance or increasing the required cure time. These advancements are necessary for the seamless integration of conductive polymers into large-scale, high-throughput manufacturing processes such as roll-to-roll printing.

Another pivotal technological trend is the development of hybrid conductive coating systems, which incorporate high-performance nanomaterials—such as carbon nanotubes (CNTs), graphene, silver nanowires, or metallic nanoparticles—within the polymer matrix. The aim of these hybrid systems is to leverage the synergistic benefits of polymers (flexibility, adhesion, corrosion resistance) and nanomaterials (ultra-high conductivity), thereby overcoming the inherent limitations of pure ICPs, particularly their susceptibility to thermal degradation and relatively lower intrinsic conductivity compared to metals. Advanced surface modification techniques, including plasma polymerization and vapor deposition, are also being employed to create ultra-thin, highly conformal conductive layers on complex or heat-sensitive substrates, opening new opportunities in advanced microelectronics and implantable medical devices where precision and minimal material usage are paramount.

The application technology aspect is equally dynamic, focusing on sophisticated deposition methods to achieve precise patternability and low-cost manufacturing. Technologies such as inkjet printing, gravure printing, and screen printing are being optimized to use conductive polymer inks for mass production of flexible electronics, sensors, and OLED components. These additive manufacturing techniques offer significant material efficiency and design flexibility compared to traditional subtractive methods. The ongoing development of self-healing conductive polymers represents an advanced frontier, aiming to create coatings capable of autonomously repairing damage to conductive pathways, thus dramatically extending the lifespan and reliability of devices in demanding mechanical or operational environments, thereby providing a clear technological edge in reliability-critical applications like aerospace and defense electronics.

The global market for Conductive Polymer Coatings exhibits distinct regional growth patterns driven by varying industrial landscapes, regulatory environments, and technological adoption rates. Asia Pacific (APAC) dominates the market share due to its established position as the global hub for electronics manufacturing, including semiconductors, displays, and consumer devices. Countries such as China, South Korea, Japan, and Taiwan possess massive production capacities, generating immense demand for EMI shielding and anti-static coatings. Furthermore, aggressive governmental investments in solar energy projects and the burgeoning electric vehicle sector in China and India fuel the adoption of conductive polymers for energy storage and lightweight structural components, cementing APAC's leadership in volume and sustained growth.

North America and Europe represent mature yet highly lucrative markets characterized by stringent regulatory frameworks (e.g., EMC directives) and a focus on high-specification, niche applications. North America's growth is driven primarily by the robust aerospace, defense, and specialized medical device sectors, which require ultra-high-performance and certified conductive materials. The region is also a key innovation center for flexible electronics and advanced sensor technology, pushing the demand for next-generation polymer coatings with superior flexibility and durability. Europe, similarly, emphasizes high-quality automotive manufacturing (particularly EVs) and advanced industrial automation, requiring reliable, durable conductive coatings for complex machinery and electronic control units.

The Latin America (LATAM) and Middle East & Africa (MEA) regions, while currently holding smaller market shares, are forecast to exhibit promising growth, largely driven by expanding infrastructure development, increasing mobile technology penetration, and diversifying manufacturing bases. In MEA, the emphasis is often on oil & gas infrastructure, where corrosion protection and anti-static measures are critical safety requirements, creating demand for robust polymer coatings. LATAM, particularly Brazil and Mexico, benefits from growing automotive assembly operations and an expanding consumer electronics market, necessitating localized supply chains for standard EMI and ESD protective coatings, signaling future potential for significant market penetration as local manufacturing capabilities advance.

The primary function is providing electromagnetic interference (EMI) shielding, ensuring signal integrity by blocking external electromagnetic noise, and providing electrostatic discharge (ESD) protection to prevent component damage in sensitive electronic devices.

Conductive polymer coatings offer significant advantages in flexibility, lighter weight, ease of processing (e.g., printing methods), and enhanced corrosion resistance compared to bulk metal or metal-filled paint systems, making them ideal for modern compact and flexible devices.

Poly(3,4-ethylenedioxythiophene) or PEDOT:PSS is the most commonly used conductive polymer for applications requiring high optical transparency combined with good electrical conductivity, such as in touchscreens, OLEDs, and flexible solar cells.

The primary challenge is the inherent thermal and environmental instability of some intrinsically conductive polymers (ICPs), which can degrade in the presence of high heat, moisture, or harsh chemicals, leading to a loss of conductivity over time.

The EV market significantly boosts demand by requiring lightweight, corrosion-resistant conductive coatings for internal battery components, current collectors, and sensor enclosures to manage electrical flow and ensure the longevity and safety of battery packs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.