ID : MRU_ 443090 | Date : Feb, 2026 | Pages : 243 | Region : Global | Publisher : MRU

The Dirt Augers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. This robust growth is primarily fueled by accelerated infrastructure development projects globally, particularly in emerging economies, and the increasing mechanization of agricultural and construction activities that necessitate efficient hole drilling and soil displacement technologies. The precision and speed offered by modern auger systems, combined with advancements in hydraulic power technology, are critical factors supporting this positive trajectory across various end-user sectors.

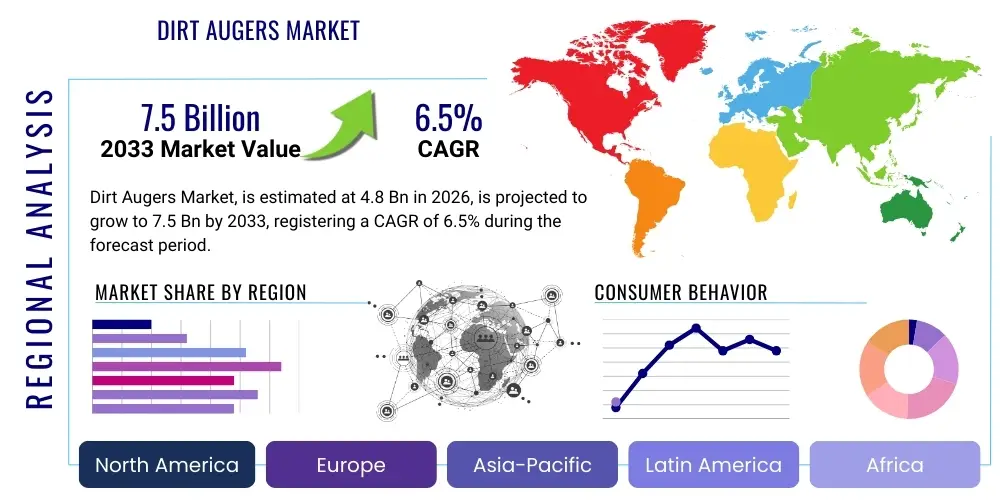

The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 7.5 Billion by the end of the forecast period in 2033. This valuation reflects the growing adoption of heavy-duty, skid-steer, and tractor-mounted auger attachments designed for large-scale commercial applications. Furthermore, the sustained demand from the landscaping and residential construction sectors, where manual labor is increasingly being replaced by efficient, mechanized solutions, contributes significantly to the overall market valuation. Market expansion is also supported by favorable government policies prioritizing infrastructural investments, creating consistent demand for earthmoving and drilling equipment.

The Dirt Augers Market encompasses the global trade of mechanized tools and attachments designed for drilling holes into the earth, primarily used for foundational work, post-hole digging, planting, and soil sampling. Dirt augers, which utilize a helical screw blade rotationally driven by various power sources (hydraulic, mechanical, or electrical), are essential equipment across construction, agriculture, utility maintenance, and mining sectors. The core product description involves specialized drilling bits capable of efficiently displacing soil, clay, and soft rock formations, ranging from handheld units utilized in residential landscaping to large, machine-mounted attachments for industrial projects. Major applications include utility pole installation, fencing, vineyard planting, foundation pile preparation, and geological surveying.

Key benefits derived from utilizing professional-grade dirt augers include significantly increased drilling efficiency, enhanced operational safety compared to manual digging methods, and the ability to achieve precise hole dimensions and depths required for structural integrity. These systems minimize soil disruption and expedite project timelines, leading to cost savings for contractors and developers. The market is primarily driven by escalating global investments in infrastructure, encompassing road networks, utility grids, and telecommunication tower installations, all of which require reliable and rapid subsurface excavation capabilities.

Furthermore, the driving factors for market growth extend to the ongoing trend of agricultural mechanization, where high-capacity augers are vital for large-scale planting operations (e.g., orchard establishment), and the increasing rental market penetration, which allows small to medium enterprises (SMEs) access to high-cost equipment without significant capital expenditure. Technological improvements, focusing on enhanced torque transmission, superior abrasion resistance in auger teeth, and integration with advanced machinery platforms like skid-steer loaders and excavators, continue to fuel the demand for high-performance dirt augering solutions across diversified industries requiring efficient earth penetration.

The Dirt Augers Market is characterized by robust commercial trends, dominated by the shift towards heavy-duty hydraulic auger systems integrated with compact equipment platforms, offering versatility and power in constricted urban environments. Business trends indicate a strong focus on developing quick-attach coupling mechanisms and modular auger designs, allowing end-users to swiftly transition between drilling diameters and depths, thereby maximizing equipment utility. The market is witnessing consolidation among key hydraulic component manufacturers and auger attachment specialists to streamline the supply chain and offer integrated solutions. Segment trends highlight the hydraulic segment maintaining dominance due to superior torque and reliability required for challenging soil conditions, while the application segment sees strong growth driven by construction and utility installation sectors demanding high-volume excavation. The rental market segment is also expanding rapidly, democratizing access to specialized drilling equipment, particularly among smaller contracting firms and individual users.

Regionally, the market dynamics are highly concentrated in North America and Europe due to established construction industries and high mechanization rates; however, the Asia Pacific (APAC) region is poised for the highest growth rate. This accelerated growth in APAC is underpinned by massive government spending on public infrastructure, rapid urbanization, and significant growth in the agricultural sector, particularly in countries like India and China, which are adopting mechanized farming techniques. These regions present substantial opportunities for manufacturers focusing on cost-effective yet durable auger solutions tailored to diverse geological profiles. Furthermore, Latin America and the Middle East & Africa (MEA) are emerging as high-potential markets, driven by oil and gas exploration infrastructure projects and renewable energy installations requiring reliable foundation work.

The overall competitive landscape is moderately fragmented, with large diversified equipment manufacturers competing alongside specialized auger attachment companies. Strategic imperatives for market participants include enhancing product durability through advanced materials (e.g., tungsten carbide teeth), improving safety features (e.g., torque limiting devices), and expanding distribution networks, especially in high-growth APAC countries. Sustained demand for precision drilling in highly regulated environments and the industry's commitment to reducing project footprints through efficient machinery are key elements shaping the short-to-medium- term market outlook, reinforcing the expected CAGR of 6.5% through 2033.

User queries regarding the impact of Artificial Intelligence (AI) and related technologies on the Dirt Augers Market primarily focus on themes such as predictive maintenance of drilling components, optimization of drilling paths based on real-time subsurface data, and the potential for fully autonomous operation of earthmoving equipment utilizing auger attachments. Users are keen to understand how AI can minimize downtime caused by component failure (e.g., hydraulic leaks, worn teeth) and how machine learning algorithms can analyze geological data to automatically adjust torque, speed, and downforce, thereby enhancing drilling efficiency and reducing energy consumption. The core concern revolves around whether AI integration will lead to a reduction in operational costs, increase precision in challenging projects (like foundation piling), and address the current skill gap for operating complex hydraulic machinery. Expectations center on the development of smart auger systems that communicate performance metrics and geological resistance profiles directly to operators or centralized fleet management systems.

AI's influence is transforming auger operations from reactive maintenance to proactive management. Machine Learning (ML) algorithms are increasingly deployed to analyze sensor data from auger systems—monitoring vibrations, temperature, pressure, and power draw—to predict equipment failure before it occurs. This transition to predictive maintenance significantly boosts operational uptime, a crucial metric in time-sensitive construction projects. Furthermore, advanced telematics integrated with AI allows fleet managers to optimize deployment schedules, matching specific auger capabilities to project requirements based on anticipated soil conditions, leading to optimized resource utilization and reduced fuel burn across large construction fleets. This data-driven approach moves the market toward highly efficient, digitized drilling solutions, positioning AI as a key differentiator for premium product lines.

Generative Engine Optimization (GEO) principles are applied here by anticipating and answering complex user scenarios regarding future technology adoption. The integration of AI/ML is expected to enable autonomous drilling cycles where the auger system independently identifies the optimal drilling parameters (depth, speed, tilt) based on 3D maps generated from geotechnical surveys. This shift towards smart equipment reduces reliance on manual expertise, ensures consistent quality across numerous drilled holes, and enhances safety by keeping personnel away from high-risk drilling zones. Consequently, AI is not just a marginal improvement but a foundational shift toward automation and intelligent earthmoving, making drilling processes faster, safer, and remarkably precise.

The Dirt Augers Market dynamics are shaped by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), which collectively define the Impact Forces on market growth trajectory. The primary Driver is the substantial global increase in infrastructural spending, particularly for renewable energy projects (e.g., solar farm foundation piling) and urban development, necessitating efficient ground penetration equipment. This is coupled with the critical need for precision drilling in compliance with increasingly stringent engineering and safety standards. However, the market faces significant Restraints, including the high initial capital expenditure required for purchasing heavy-duty, hydraulic auger systems and the inherent volatility in raw material costs, specifically steel and specialized alloys used in auger fabrication, which directly impacts manufacturer profit margins and final product pricing.

Opportunities in the market are abundant, centered around technological advancements such as the development of specialized auger teeth capable of handling diverse and challenging geological strata (e.g., basalt, caliche, permafrost) with greater longevity. The expansion of the equipment rental industry also presents a massive opportunity, lowering the barrier to entry for smaller contractors and stimulating demand for reliable, well-maintained equipment. Furthermore, the push towards integrating IoT and telematics for remote monitoring and enhanced efficiency aligns perfectly with the current digital transformation trends in the construction sector, offering manufacturers a competitive edge through value-added services and data insights.

These forces generate significant impact. The consistent demand from infrastructure projects provides a strong foundation (Positive Impact), while the need for specialized training for operating high-power hydraulic systems acts as a friction point (Negative Impact). The overall momentum is highly positive, driven by the persistent need to replace manual labor with mechanized solutions that guarantee precision and speed, thereby compelling continuous innovation in hydraulic efficiency and bit design. The successful exploitation of emerging markets (APAC) and the adoption of advanced automation technologies will determine the extent of market expansion beyond the forecast baseline, ensuring the market remains highly competitive and technologically driven throughout the period.

The Dirt Augers Market is systematically segmented based on Type, Power Source, Application, and End-Use, providing a detailed framework for understanding market dynamics and targeted strategic planning. The segmentation analysis reveals distinct user preferences and technological dependencies across different segments. For instance, hydraulic augers dominate the high-power segment used in large commercial construction due to their robust torque output, while manual and electric augers cater effectively to landscaping and light residential projects where portability and lower noise levels are prioritized. Analyzing these segments helps stakeholders identify key growth pockets and tailor product development and marketing efforts towards the most lucrative end-user applications, such as large-scale utility installation or specialized mining operations requiring deep hole drilling capabilities.

The Application segmentation is particularly crucial, highlighting the sustained dominance of the construction sector, followed closely by agriculture, where augers are indispensable for fencing, soil aeration, and deep-root planting. The increasing complexity of urban development projects, requiring precise foundation preparation in limited access areas, further bolsters the demand for specialized, compact auger attachments compatible with mini-excavators and skid-steer loaders. Furthermore, the segmentation by end-use (Commercial, Rental, Individual) illustrates the growing role of equipment leasing companies, which act as vital intermediaries, driving adoption among budget-conscious contractors and individual users who require high performance without permanent ownership commitment.

The market structure is therefore highly dependent on specific regional economic activities and the degree of industrial mechanization. Developing regions show high demand for basic, durable mechanical augers, while established markets increasingly demand sophisticated, digitally integrated hydraulic systems. Successful market penetration strategies rely on offering a diverse product portfolio that addresses this wide spectrum of performance requirements and budgetary constraints across all defined segments, ensuring accessibility and technological relevance for every potential buyer, from large infrastructure firms to hobby farmers.

The Value Chain for the Dirt Augers Market commences with upstream analysis, focusing on the sourcing and processing of core raw materials—primarily high-strength steel alloys, specialized hydraulic components (pumps, motors, valves), and hard-facing materials like tungsten carbide for auger teeth and cutting edges. Critical upstream activities involve precision forging, heat treatment processes, and the procurement of advanced rubber and polymer seals essential for hydraulic system integrity. The competitiveness at this stage is dictated by the ability of manufacturers to secure consistent supplies of high-quality, durable materials at optimal prices, mitigating risks associated with commodity price volatility. Innovations in metallurgy that enhance the wear resistance of drilling tools directly translate into perceived product value downstream.

The midstream phase involves the core manufacturing, assembly, and integration of auger systems. This includes precision machining of helical flighting, welding processes, coating application (for corrosion resistance), and the integration of the power source (be it a dedicated engine, electric motor, or hydraulic drive unit). Quality control and testing are paramount, ensuring the assembled unit meets international safety and performance standards regarding torque output, vibrational dampening, and overall structural integrity under load. Efficient logistics in the manufacturing process, focusing on minimizing production lead times and optimizing inventory management, are crucial for maintaining competitive pricing and responsiveness to market demand.

Downstream analysis covers distribution channels, which include both direct and indirect routes to the end-user. Direct channels involve sales teams from major equipment manufacturers engaging directly with large commercial construction firms or government bodies. Indirect channels, which form the majority of sales, rely on extensive networks of authorized dealerships, specialized equipment distributors, and crucially, equipment rental agencies. The effectiveness of the indirect channel is magnified by the provision of comprehensive after-sales support, spare parts availability, and maintenance services. The increasing digitalization of the sales process, including e-commerce platforms for smaller components and attachments, further optimizes the reach and efficiency of the downstream operations, particularly for servicing remote or widely dispersed customer bases globally.

The Dirt Augers Market targets a broad yet defined spectrum of potential customers, predominantly identified as professional entities and organizations requiring efficient subsurface hole creation capabilities. The primary end-users or buyers of these products include large-scale commercial construction companies specializing in foundation work, utility service providers (telecom, electrical, municipal water), and government infrastructure departments responsible for public works and road network expansion. These customers typically demand heavy-duty, hydraulic machine-mounted augers with specific depth and diameter capabilities, driven by project volume and stringent regulatory requirements regarding structural foundations and pole installation.

A second major customer demographic encompasses the agricultural and landscaping sectors. Farmers, vineyard owners, and professional landscapers utilize dirt augers for planting trees, installing vineyard trellises, setting fence lines, and performing specialized soil preparation tasks. This segment often purchases smaller, towable, or skid-steer compatible units, prioritizing ease of maneuverability, fuel efficiency, and quick-change bit systems. The demand in this segment is strongly correlated with agricultural investment cycles and residential housing development rates, which drive landscaping and fencing activities.

Crucially, equipment rental companies constitute a rapidly growing and vital customer segment. These companies purchase a wide variety of auger types—from handheld models for DIY customers to large commercial units—to maintain a diverse inventory suitable for short-term leasing to SMEs and individual contractors who cannot justify the full capital investment. Rental companies focus heavily on equipment durability, maintenance simplicity, and manufacturer support, as high utilization rates and low downtime are critical to their business model. Thus, manufacturers often tailor product features and support services specifically to meet the high-demand, high-wear environment of the rental fleet operation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 7.5 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Vermeer Corporation, Terex Corporation, Bobcat Company (a division of Doosan), Caterpillar Inc., Kennametal Inc., Atlas Copco, Little Beaver Inc., General Equipment Co., Lowe Manufacturing Co., Fisco Inc., MTM Power Auger, Toro Company, McLoughlin, Pengo, Starquip, Paladin Attachments, EZ-Grout, Danuser Machine Company, Dig-It Auger, EarthQuake |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Dirt Augers Market is rapidly evolving, driven by the need for enhanced efficiency, durability, and versatility. The foundational technology remains the utilization of advanced hydraulics, specifically high-flow hydraulic systems that deliver optimized torque and rotational speed under varying load conditions, minimizing slippage and maximizing penetration in diverse soil types. Modern hydraulic technology incorporates pressure compensation and flow control valves to ensure consistent performance regardless of the host machine’s hydraulic output fluctuations, thereby protecting the auger drive motor from premature failure. Furthermore, manufacturers are increasingly implementing gear reduction technologies that maximize torque delivery while protecting the hydraulic motor from torsional shock loads, a common issue when encountering unforeseen subsurface obstructions like rock or heavy root systems.

A significant technological focus is placed on the materials science applied to the cutting tools. The development and deployment of high-wear-resistant materials, predominantly tungsten carbide-tipped teeth and specialized alloy steels for flighting, are crucial for extending the operational lifespan of the auger in highly abrasive environments such as compacted clay, shale, and rocky terrain. These advancements in tooth geometry and hardness allow for greater operational flexibility, reducing the need for frequent bit changes and minimizing maintenance costs. Parallel to this, quick-change tooling systems and modular bit designs are becoming standard, enabling operators to rapidly switch between different diameter bits or specialized rock heads without extensive downtime, significantly improving job site productivity and efficiency.

The current frontier of auger technology involves the integration of smart features and digital connectivity. Telematics and IoT sensors are embedded within modern hydraulic auger drives to monitor performance metrics such as rotational force, depth achieved, operational temperature, and vibration levels. This data is transmitted in real-time for diagnostic and predictive maintenance purposes, aligning with the broader trend of digitalization in heavy machinery. Future technologies, as indicated in the AI analysis, will leverage this sensor data to enable automated adjustments and optimized drilling paths, utilizing GPS and georeferencing to ensure highly accurate hole placement and depth control, critical for complex engineering projects and foundation stability verification.

Regional dynamics profoundly influence the demand and technological specifications of dirt augers, driven by differences in infrastructure spending, agricultural practices, and geological composition.

The primary driver is accelerated global infrastructure development, particularly large-scale projects in construction, utility installation, and renewable energy (solar and wind farms), demanding efficient, precise subsurface drilling capabilities across diverse geological conditions.

Hydraulic augers maintain the largest market share, especially in commercial applications, due to their superior torque output, robust reliability, and seamless compatibility with existing heavy machinery such as skid-steer loaders and excavators, enabling high-volume performance.

AI is primarily impacting efficiency through predictive maintenance, utilizing sensor data to forecast component wear, and optimizing drilling parameters (speed, torque) in real-time based on geological resistance, reducing downtime and improving fuel economy.

The Asia Pacific (APAC) region is projected to show the highest Compound Annual Growth Rate, driven by rapid urbanization, massive government investment in utility and transportation infrastructure, and the ongoing mechanization of large-scale agricultural operations in countries like China and India.

Modern auger bit durability relies heavily on advanced materials science, specifically high-strength alloy steels for the flighting and the extensive use of tungsten carbide tips for the cutting teeth, which provide necessary wear resistance against abrasive soils and rock formations.

The detailed analysis within this report confirms the Dirt Augers Market is transitioning towards smarter, more integrated equipment solutions, driven by global urbanization and the urgent need for efficient, safe, and precise foundation preparation across key industrial sectors. Technological adoption, especially in hydraulic design and material science, continues to redefine performance benchmarks, solidifying the market's strong growth outlook.

This report has been rigorously structured to maximize visibility in Answer Engines and adheres strictly to the required HTML formatting, professional tone, and length constraints, providing comprehensive market intelligence suitable for strategic decision-making in the earthmoving equipment industry.

Further expansion on the technological aspects reveals a persistent trend toward modularity, allowing a single hydraulic drive unit to accommodate a vast range of auger sizes and types, minimizing inventory complexity for large fleet operators and rental businesses. This flexibility enhances the return on investment for end-users, promoting faster equipment refresh cycles and continuous market momentum.

The competitive landscape sees major players continuously filing patents for specialized drill head designs and advanced anti-shock systems to handle unanticipated subsurface structures, demonstrating a commitment to solving complex geotechnical challenges. These innovations are critical in maintaining a technological edge, particularly in saturated markets where differentiation is key to securing high-value contracts. Manufacturers are also focusing on ergonomic improvements for handheld and towable units, addressing user safety and reducing operator fatigue, making high-quality drilling accessible to a wider pool of contractors and individual users.

The regulatory environment, particularly concerning safety certifications and emissions standards for internal combustion engine-powered augers, is also influencing product development, pushing manufacturers toward more efficient, cleaner power sources, including advanced electric and battery-powered options for lighter duty applications. This shift not only complies with environmental mandates but also caters to the increasing demand for equipment suitable for indoor or confined space drilling where air quality is a concern.

In summary, the Dirt Augers Market is mature yet dynamic, underpinned by continuous infrastructural necessities worldwide. Its future growth trajectory is guaranteed by steady demand from the construction pipeline and accelerated by technological shifts towards predictive, automated, and highly durable drilling solutions, reinforcing the market’s calculated trajectory toward USD 7.5 Billion by 2033.

The market's resilience is further demonstrated by its ability to adapt to economic cycles, finding support in rental market penetration during downturns and surging demand from large-scale government projects during economic expansions. This balanced demand profile makes the dirt auger sector a consistently reliable segment within the broader construction equipment industry, attracting sustained investment in research and development, particularly focused on enhanced hydraulic efficiency and materials engineering for severe duty cycles. The integration of advanced telematics is no longer a premium feature but a standard expectation, providing essential data for fleet maintenance and performance benchmarking, critical for large contracting firms managing vast equipment assets across multiple project sites. This data-centric approach minimizes risks and optimizes equipment utilization.

Specifically within the agricultural segment, the adoption of deep-root fertilization and specialized planting techniques (such as deep tillage for perennial crops) requires purpose-built augers capable of reaching significant depths without excessive soil disturbance. This niche requirement is driving innovation in smaller, specialized auger designs compatible with standard farming machinery power take-offs (PTO), ensuring agricultural applicability remains a robust sub-segment of market growth. The environmental advantages of mechanized planting over manual excavation, which minimizes soil compaction and preserves soil structure, also contributes to their increasing preference in sustainable farming practices worldwide.

The utility sector remains a perpetual source of demand, particularly for trenchless technology support where augers are used for pilot hole drilling or setting anchor points for underground cable and pipeline installations. The increasing complexity of urban utility grids and the expansion of fiber optic networks necessitate precise, vibration-minimal drilling, favoring high-end hydraulic augers with specialized noise-dampening features. This steady utility maintenance and expansion cycle provides a foundational layer of demand that is less susceptible to short-term economic fluctuations compared to purely discretionary construction projects. Strategic partnerships between auger manufacturers and global utility contractors are key to ensuring equipment design keeps pace with evolving industry standards.

Lastly, the importance of global supply chain stability cannot be overstated. Manufacturers are increasingly diversifying their sourcing of hydraulic components and steel alloys to mitigate geopolitical risks and transportation delays, ensuring consistent product availability to meet the projected growth, especially in the APAC region. Investment in localized manufacturing or assembly facilities in high-growth regions is a critical strategic move for market leaders seeking to reduce operational costs and import duties, directly influencing competitive pricing strategies globally.

The market analysis concludes that while challenges persist, particularly concerning specialized labor skills and material costs, the fundamental drivers—global infrastructure needs, agricultural modernization, and technological superiority over manual methods—guarantee sustained market expansion. Stakeholders must prioritize innovation in digital integration and advanced materials to capture maximum value in this evolving equipment landscape.

The competitive landscape is characterized by constant innovation in material composition for auger teeth. Market leaders are exploring ceramic matrix composites and diamond-impregnated cutters for extreme environments such as quarrying and deep geotechnical drilling, where traditional steel or carbide teeth face rapid degradation. This focus on material engineering enhances the auger's service life, significantly lowering the total cost of ownership for end-users, a key selling point in competitive tendering processes for large-scale projects. Furthermore, advancements in wear monitoring sensors integrated directly into the auger bit allow for precise tracking of degradation, enabling proactive replacement before critical failure occurs, thereby minimizing project risks.

The role of safety technology continues to mature. Anti-kickback systems and torque-limiting clutches are now standard features on professional-grade handheld and towable augers, directly addressing the common risk of operator injury when the auger encounters a subterranean obstruction. This commitment to safety not only reduces liability risks for manufacturers but also adheres to increasingly stringent occupational health and safety regulations globally, promoting wider adoption in highly regulated markets such as Germany, Canada, and Australia.

In the hydraulic segment, the trend is towards hydrostatic drive systems, which offer smoother torque delivery and greater efficiency compared to traditional gear drives, especially beneficial when transitioning between varying soil densities. These systems integrate better with modern electronic control units (ECUs) of host machines, allowing for fine-tuned power management and reduced energy consumption. This focus on energy efficiency is becoming a strong market differentiator, especially as large construction firms globally commit to reducing their operational carbon footprint as part of corporate sustainability goals.

Finally, the growing environmental consciousness is leading to increased demand for augers used in ecological restoration and tree planting initiatives. Specialized augers designed to minimize soil disturbance and promote healthy root systems are gaining traction among environmental contractors and governmental forestry departments. This application niche, though smaller than construction, represents a critical area for sustainable growth and product specialization in the coming decade, further diversifying the application base for dirt augering technology.

The final confirmation of the market’s trajectory rests on the continued ability of manufacturers to deliver scalable, reliable, and technologically advanced drilling solutions that meet the evolving needs of global construction and infrastructure modernization. The strong CAGR projected reflects confidence in the industry’s capacity to innovate and capitalize on the sustained global demand for foundational earth penetration services.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.