ID : MRU_ 442825 | Date : Feb, 2026 | Pages : 241 | Region : Global | Publisher : MRU

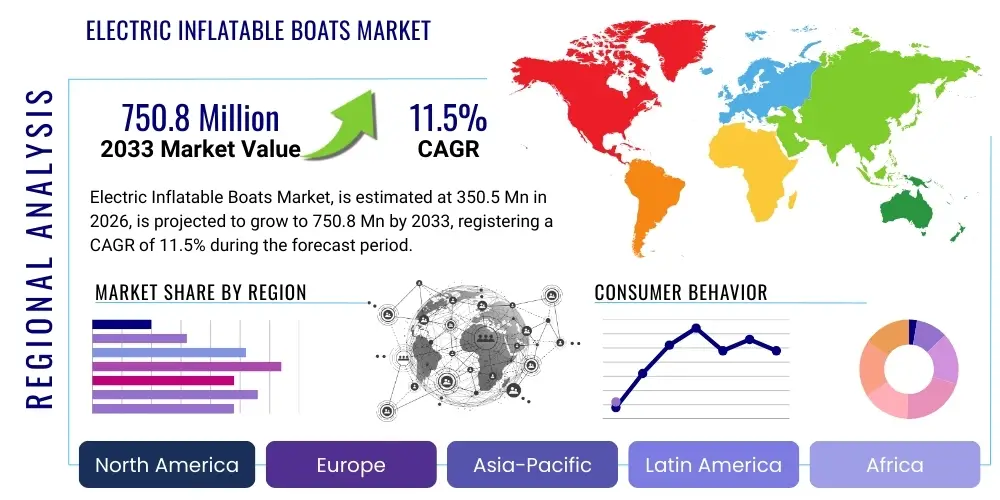

The Electric Inflatable Boats Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 350.5 Million in 2026 and is projected to reach USD 750.8 Million by the end of the forecast period in 2033.

The Electric Inflatable Boats Market encompasses the design, manufacture, and distribution of inflatable watercraft powered primarily by electric propulsion systems, utilizing advanced battery technologies instead of traditional internal combustion engines (ICE). These boats offer significant advantages in terms of reduced noise pollution, zero direct emissions, and lower maintenance requirements, making them increasingly popular across recreational, commercial, and governmental sectors. The market is defined by continuous innovation in battery energy density and motor efficiency, addressing historical limitations related to range and power output. Key product offerings span from small, portable dinghies suitable for tenders to larger, high-performance Rigid Inflatable Boats (RIBs) used for tactical operations or luxury tenders.

Major applications for electric inflatable boats are broad and diversified. In the recreational segment, they are favored for quiet lake cruising, fishing, and as auxiliary vessels for larger yachts, driven by increasing regulatory restrictions on ICEs in specific waterways and a growing consumer preference for sustainable leisure activities. Commercially, they are utilized in eco-tourism, rental fleets operating in environmentally sensitive areas, and harbor management. The robustness, low draft, and maneuverability characteristic of inflatable hulls, combined with the instantaneous torque and reliability of electric motors, position them as highly effective tools across various operational environments.

The market is primarily driven by global governmental mandates promoting decarbonization within the marine sector, coupled with substantial improvements in lithium-ion battery technology. Benefits include enhanced operational stealth, reduced fuel dependency, and compliance with stringent environmental regulations such as those imposed in European protected marine zones and certain North American lakes. Furthermore, the simplicity of electric systems appeals to end-users by minimizing complex mechanical breakdowns and simplifying winterization processes, ultimately contributing to a superior ownership experience and fostering robust market growth throughout the forecast period.

The Electric Inflatable Boats Market is poised for significant expansion, fueled by regulatory push toward sustainable boating practices and rapid technological convergence in battery and motor efficiency. Current business trends indicate a strategic shift among traditional boat manufacturers toward hybrid and full-electric models, often achieved through key acquisitions of specialized electric propulsion startups. Regional dynamics show North America and Europe leading in adoption, primarily due to well-established recreational boating cultures, high disposable incomes, and early imposition of environmental regulations impacting marine activities. Furthermore, the emphasis on lightweight materials, such as advanced polymers and composites for hull construction, is optimizing boat performance and extending range capabilities, thereby overcoming crucial barriers to widespread consumer acceptance.

Segment trends highlight the strong performance of the Lithium-ion battery segment, dominating the market due to its superior energy-to-weight ratio and cycle life compared to traditional lead-acid alternatives. Within the application segment, Recreational use remains the largest revenue contributor, but the Commercial and Military/Rescue segments are exhibiting the fastest growth rates as organizations recognize the operational advantages of quiet, emission-free vessels for surveillance, search and rescue, and sensitive area patrol. This commercial acceleration is vital, driving economies of scale that subsequently lower overall component costs for the recreational sector, thus creating a positive feedback loop for market accessibility.

Overall, the market landscape is characterized by moderate fragmentation, with strong competition between established marine brands and agile electric powertrain specialists. Strategic imperatives for market participants include securing reliable supply chains for critical battery components, investing heavily in charging infrastructure compatibility, and developing proprietary battery management systems (BMS) to maximize safety and longevity. Successful market penetration relies on effective branding that emphasizes sustainability, performance parity with ICE counterparts, and superior reliability, positioning electric inflatable boats not merely as eco-friendly alternatives but as technologically advanced superior solutions for modern marine requirements.

User queries regarding the impact of Artificial Intelligence (AI) on the Electric Inflatable Boats Market often revolve around enhanced navigation, predictive maintenance, and optimized battery performance. Key themes include concerns about autonomy integration in smaller vessels, the reliability of AI-driven safety systems in dynamic marine environments, and expectations for prolonged battery life through smart monitoring. Users are primarily interested in how AI can move these boats beyond basic electric operation into highly functional, connected marine platforms, focusing particularly on maximizing range and mitigating risks associated with remote operation or prolonged storage. The analysis indicates a high user expectation for AI to fundamentally improve operational efficiency and safety, rather than merely enhancing existing features.

AI’s influence is manifesting significantly in sophisticated Battery Management Systems (BMS). Machine learning algorithms are being employed to analyze real-time usage data—including speed profiles, wave resistance, temperature fluctuations, and charging habits—to dynamically adjust power output and optimize energy consumption. This predictive optimization not only extends the boat’s operational range far beyond static estimates but also enhances the overall lifespan and safety of the expensive battery packs by anticipating potential failures or stress points. Furthermore, AI contributes to smart charging protocols, determining the optimal charging rate based on grid load, battery state of health, and anticipated next use, thereby minimizing degradation.

Beyond powertrain management, AI is crucial for developing advanced navigation and safety features. Integration of AI-powered sensor fusion allows electric inflatable boats to utilize autonomous collision avoidance systems (ACAS), especially critical in crowded harbors or low-visibility scenarios. Additionally, AI facilitates predictive maintenance schedules by continuously monitoring motor vibration, electrical resistance, and component wear, alerting operators before mechanical failures occur. This shift from reactive to proactive maintenance minimizes downtime, a crucial factor for commercial operators, while significantly enhancing the safety profile for recreational users.

The market trajectory is shaped by a powerful interplay of Drivers, Restraints, and Opportunities, collectively forming the Impact Forces that dictate investment and consumer behavior. The primary driver is the accelerating global movement toward marine decarbonization, supported by stringent regulations banning or limiting internal combustion engines in environmentally sensitive freshwater bodies and coastal areas, particularly across Europe and North America. This regulatory pressure effectively creates a captive market for electric alternatives. Counterbalancing this growth are significant restraints, notably the relatively high initial capital expenditure required for purchasing electric boats, primarily driven by the cost of advanced lithium-ion batteries. Range anxiety also remains a psychological barrier for prospective buyers accustomed to the easy refuel capacity of gasoline engines, although rapid technological advancements are steadily mitigating this concern.

Key opportunities for market players lie in exploiting technological niches such as fast-charging infrastructure development suitable for marine environments and implementing sophisticated lightweight material engineering to maximize boat performance without compromising durability. The development of standardized, swappable battery systems, akin to those used in smaller electric vehicles, represents a transformative opportunity, potentially solving range anxiety and simplifying operational logistics, especially for rental fleets and tenders. Furthermore, penetrating emerging markets in Asia Pacific and Latin America, where boating culture is expanding but regulatory frameworks are still nascent, provides significant long-term growth avenues, allowing companies to establish dominance early in the adoption curve.

The cumulative impact forces strongly favor market expansion over the long term. While high battery costs and the need for dedicated marine charging infrastructure currently act as frictional restraints, the overwhelming external pressures from environmental mandates and persistent consumer demand for sustainable leisure options provide persistent momentum. The market exhibits high susceptibility to technological breakthroughs; a significant increase in battery energy density or a substantial drop in manufacturing costs could act as a catalytic force, rapidly accelerating mass adoption. Therefore, strategic focus must be placed on vertical integration and collaborative partnerships aimed at reducing overall system costs and enhancing the user experience through superior range and rapid power replenishment capabilities.

The Electric Inflatable Boats Market is segmented based on critical technical and application parameters, providing a detailed view of current market demands and future growth areas. Primary segmentation is observed across Boat Type (Rigid Inflatable Boats vs. Soft Inflatable Boats), Motor Type (Outboard vs. Inboard), Battery Technology (Lithium-ion vs. Lead-acid), and End-Use Application (Recreational, Commercial, Military/Rescue). Understanding these segments is crucial for manufacturers to tailor their product development strategies and marketing efforts effectively, ensuring offerings align precisely with the operational requirements and budget constraints of specific customer groups.

The segmentation by Boat Type is particularly important as it dictates performance, durability, and cost. Rigid Inflatable Boats (RIBs), which feature a solid hull and inflatable tubes, dominate higher-performance and commercial applications due to superior handling and stability in rough waters. Conversely, Soft Inflatable Boats (SIBs) are favored for portability, storage convenience, and lower cost, making them ideal for the tender market and casual recreational use. The technological segmentation by Battery Type highlights the transition from heavier, lower-density lead-acid batteries—still found in entry-level models—to the higher-performing, lightweight, and longer-cycle-life lithium-ion systems, which command premium pricing but deliver superior operational utility.

Application-based segmentation reveals underlying market drivers. While the Recreational segment is volume-intensive, the Commercial segment, including eco-tourism and charter operations, demands robustness and sustained operational uptime, driving innovation in reliability and charging solutions. The Military and Rescue segment, though smaller in volume, demands the highest specifications regarding stealth, reliability, and rapid deployment capabilities, often acting as an incubator for advanced battery and motor technologies before they cascade down to the mass market. This hierarchical requirement structure across segments ensures a constant push for technological improvement across the entire product ecosystem.

The Value Chain of the Electric Inflatable Boats Market is complex, beginning with upstream raw material suppliers and culminating in downstream distribution channels and end-user services. Upstream analysis focuses heavily on the procurement of critical components: battery cells (primarily lithium-ion), advanced electric motors (often high-torque permanent magnet motors), and high-durability fabrics (PVC or Hypalon) for the inflatable tubes. The bargaining power of battery cell suppliers is notably high due to global supply chain constraints and the strategic importance of energy density, making secure long-term contracts for battery procurement a primary concern for boat manufacturers. Collaboration between component manufacturers and boat builders is crucial early in the design phase to optimize weight distribution and motor integration.

Midstream activities involve the specialized manufacturing and assembly process. This phase requires expertise in integrating sensitive electrical systems with marine-grade materials, focusing intensely on waterproofing, corrosion resistance, and safety protocols for high-voltage systems. Unlike traditional boat manufacturing, the electric segment demands specialized capabilities in thermal management systems for batteries and proprietary software development for motor control units and battery management systems. Efficiency in production largely depends on standardized module integration and minimizing manual assembly steps, which contributes directly to competitive pricing and rapid scaling.

Downstream analysis covers distribution channels and post-sale services. Distribution is bifurcated into direct sales to large commercial and governmental entities, and indirect sales through a specialized network of authorized marine dealers and distributors, particularly for recreational units. Dealers require specific training to handle electric propulsion diagnostics, maintenance, and complex warranty issues, necessitating manufacturers to invest heavily in dealer education programs. The quality of post-sale servicing, including the availability of specialized electric boat mechanics and accessible charging points, directly influences customer satisfaction and brand loyalty, serving as a significant differentiator in a rapidly maturing market.

The potential customer base for electric inflatable boats is segmented primarily into three distinct categories: recreational users, commercial operators, and governmental/military entities, each with unique purchasing criteria and usage patterns. Recreational buyers, including yacht owners seeking environmentally compliant tenders and casual boaters looking for quiet, low-maintenance leisure craft for use on restricted inland waters, represent the largest volume market. These customers prioritize ease of use, portability, aesthetic design, and zero-emission operation, often viewing the purchase as an investment in sustainable lifestyle choices and seeking boats that require minimal technical upkeep.

Commercial operators form a crucial segment, encompassing eco-tourism companies, marina management services, rental fleets, and coastal research institutions. For this segment, the Total Cost of Ownership (TCO) is paramount. Electric inflatable boats offer substantial savings on fuel and drastically reduced maintenance complexity compared to ICE counterparts, translating directly into higher operational margins. Reliability, durability, and swift maintenance turnaround are critical requirements, leading commercial buyers to favor robust, high-specification RIBs with institutionalized warranty support and fleet management capabilities, typically powered by high-capacity lithium-ion systems.

Governmental and military agencies constitute the third segment, focusing on specialized applications such as harbor security, border patrol, search and rescue (SAR), and rapid deployment scenarios. These customers prioritize operational stealth, superior performance under adverse conditions, and extremely high reliability. The inherent quietness of electric propulsion is a significant tactical advantage for surveillance and reconnaissance. While cost remains a factor, performance specifications, compliance with strict operational standards, and the ability to integrate sophisticated electronics and communication systems are the determining factors in procurement decisions for defense and civil protection buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350.5 Million |

| Market Forecast in 2033 | USD 750.8 Million |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Zodiac Nautic, Highfield Boats, Walker Bay, AB Inflatables, Bombard, ePropulsion, Torqeedo (now part of Mercury Marine), BRIG, Mercury Marine, Sirocco Marine, Newport Vessels, Seamax, Saturn Boats, Ocean Craft Marine, Vita Yachts, Whisper Power |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Electric Inflatable Boats Market is defined by convergence between advanced marine engineering and electric mobility innovations originally developed for the automotive sector. Central to this evolution is the ongoing refinement of lithium-ion battery technology, focusing on increasing volumetric and gravimetric energy density while simultaneously improving safety protocols through enhanced thermal management systems (TMS). Manufacturers are actively adopting robust, IP-rated battery enclosures and designing sophisticated passive and active cooling solutions to ensure optimal performance and longevity in corrosive, high-vibration marine environments, a crucial differentiator from land-based electric vehicles.

Propulsion technology is rapidly evolving, moving toward highly efficient permanent magnet synchronous motors (PMSM) or specialized electric outboards that maximize torque delivery at low RPMs, essential for maneuvering heavy loads or operating in strong currents. The development of hydrofoils, particularly in performance RIB segments, is a notable trend. While not exclusive to electric systems, hydrofoils significantly reduce drag, making the most efficient use of battery capacity by lifting the hull out of the water at speed, thereby directly mitigating range limitations and dramatically improving energy efficiency—a core value proposition for electric vessels.

Furthermore, connectivity and digital integration play a vital role. Modern electric inflatable boats are increasingly equipped with integrated GPS, detailed digital charting systems, and telemetry capabilities. These systems allow for remote diagnostics, over-the-air (OTA) software updates, and sophisticated performance monitoring accessible via mobile applications. The integration of advanced power electronics, including bidirectional charging capabilities and efficient DC-DC converters, ensures seamless power management between solar charging sources, shore power, and the main propulsion battery, establishing these vessels as truly smart, networked components of the broader marine ecosystem.

Regional dynamics heavily influence the adoption rates and product preferences within the Electric Inflatable Boats Market, reflecting local regulatory environments, consumer wealth, and the prevalence of specific waterways. Europe currently holds a leading position in market share and technological innovation, primarily driven by stringent environmental policies, particularly in countries like Norway, Germany, and the Netherlands, which have restrictions on noise and emissions in inland lakes and protected coastal zones. The mature recreational boating culture in the Mediterranean and Northern Europe, coupled with robust infrastructure investment, makes this region a primary growth engine, focusing heavily on premium RIBs and high-capacity tenders.

North America, encompassing the United States and Canada, represents the second largest market, characterized by extensive freshwater recreational areas and a growing focus on sustainability, particularly among younger boating demographics. The US market exhibits strong demand for electric inflatables used in bass fishing, lake cruising, and as tenders for large coastal yachts. While regulatory drivers are strong, particularly at the state level (e.g., California), the pace of charging infrastructure rollout remains a critical factor impacting mass adoption, leading to strong emphasis on products with exceptional range capabilities designed to overcome "range anxiety" inherent in vast distances.

The Asia Pacific (APAC) region is forecasted to exhibit the highest Compound Annual Growth Rate (CAGR) due to rapidly expanding coastal tourism, increasing disposable incomes in key economies such as China, Australia, and South Korea, and emerging environmental awareness. While the market base is smaller than Europe or North America, rapid urbanization and investment in marine infrastructure are catalyzing growth. Opportunities are particularly high in Southeast Asian eco-tourism sectors and in countries like Australia, where the large coastline and diverse aquatic environments favor robust, low-maintenance electric vessels for surveillance and leisure activities. The Middle East and Africa (MEA) and Latin America currently represent nascent markets, driven primarily by luxury tourism projects and niche commercial applications, often relying on imported technology.

The Electric Inflatable Boats Market is projected to experience robust expansion, forecasting a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. This growth is primarily fueled by environmental regulation compliance and continuous advancements in lithium-ion battery technology.

Electric inflatable boats are considered significantly more environmentally friendly because they produce zero direct emissions (NOx, SOx, CO2) during operation. They also minimize noise pollution, which is crucial for preserving wildlife habitats and enhancing the experience of users in quiet, protected waterways.

The main challenges are the high initial purchase price, largely due to the cost of high-density lithium-ion batteries, and limited public marine charging infrastructure. Consumer anxiety regarding operational range (range anxiety) compared to conventional fuel sources is also a persistent psychological barrier, though technological gains are mitigating this.

Europe currently holds the largest market share, driven by stringent national and EU-level regulations limiting emissions and noise in marine environments, coupled with a highly developed infrastructure and high consumer demand for sustainable recreational and commercial vessels.

AI primarily enhances performance and safety through sophisticated Battery Management Systems (BMS) that optimize power draw, extend battery life, and predict maintenance needs. Furthermore, AI is increasingly integrated into navigation systems for autonomous functions and improved collision avoidance, making operations safer and more efficient.

The report structure ensures comprehensive coverage of the market, focusing on technological advancements, regulatory pressures, and key strategic imperatives for success within the rapidly evolving marine electric mobility sector. The detailed analysis across segments and regions provides a robust foundation for market entry or expansion strategies.

Further detailed analysis of the competitive environment reveals a dual strategy among market leaders: first, focused investment in miniaturization and integration of higher capacity battery cells to improve overall boat range without increasing bulk; and second, the establishment of certified service networks capable of handling complex electric drivetrains. Companies like Zodiac Nautic and BRIG, traditional leaders in the RIB sector, are leveraging their established hull design expertise while forging strategic alliances with electric motor specialists such as ePropulsion and Torqeedo to accelerate their electric product lineups. This hybridization of core competencies is vital for maintaining market relevance against pure-play electric disruptors. The recreational segment remains highly sensitive to charging convenience; thus, manufacturers prioritizing fast-charging compatibility and swappable battery designs gain significant competitive edge, especially in rental or shared-use environments where minimizing downtime is mission-critical. The necessity of standardized charging ports and protocols across the marine industry is a collaborative opportunity that could unlock substantial market liquidity.

In terms of component sourcing, volatility in the global supply chain for raw materials like lithium, cobalt, and nickel continues to pressure manufacturing costs. Electric inflatable boat manufacturers are strategically diversifying their procurement strategies, seeking long-term contracts and exploring alternative battery chemistries, such as Lithium Iron Phosphate (LFP), which offers greater safety and cycle stability despite slightly lower energy density, making it suitable for lower-speed, stability-critical commercial applications. Vertical integration, where major marine players acquire or develop their own battery pack assembly capabilities, is becoming an increasingly common strategy to mitigate risk and control intellectual property related to battery thermal management and software controls. This trend underscores the seriousness with which the marine industry is committing to electric transition, moving beyond simple component substitution to deep-seated technological redesigns tailored specifically for harsh marine conditions.

The role of regulatory bodies extends beyond emission control into product safety and performance standards for electric marine vessels. As the technology is relatively nascent, international standards organizations are developing specific safety criteria for high-voltage DC systems on boats, impacting design requirements for wiring harnesses, battery enclosures, and emergency shutdown mechanisms. Compliance with these evolving standards is non-negotiable for market access, particularly in heavily regulated markets like the European Union and the United States. Furthermore, government subsidies and tax incentives for the purchase of zero-emission vessels in certain regions are significantly lowering the effective purchase price for consumers, directly counteracting the restraint of high initial cost and serving as a crucial short-to-medium-term market accelerator. These fiscal incentives, coupled with expanding environmental consciousness among the global populace, cement the foundational drivers for sustained market growth well into the next decade.

The application of advanced materials continues to revolutionize the design of electric inflatable boats. Lightweight, high-strength composite materials, particularly carbon fiber reinforcements, are being integrated into the rigid hulls of RIBs to offset the weight of the battery packs, ensuring that the vessel maintains optimal planing characteristics and minimizes energy consumption. Simultaneously, the materials used for the inflatable tubes—high-grade PVC and Hypalon—are being enhanced for UV resistance, abrasion resistance, and temperature tolerance, extending the lifespan of the vessel and reducing maintenance requirements. This focus on material science ensures that electric models not only meet but often exceed the durability and performance standards of their conventional counterparts, addressing consumer skepticism about the ruggedness and sustained reliability required in marine environments. Innovative manufacturing techniques, such as rotational molding for complex hull shapes, further contribute to reducing manufacturing complexity and improving material consistency.

A burgeoning area of opportunity lies in the intersection of electric boating and renewable energy sources. The integration of high-efficiency flexible solar panels onto the decks or biminis of inflatable boats, combined with smart charging algorithms, allows for trickle charging or maintenance charging, especially crucial during long periods of mooring or storage. While solar charging may not provide propulsion for extended periods, it significantly reduces parasitic power loss and helps maintain optimal battery State of Charge (SOC), thus enhancing operational readiness. This complementary technology is especially appealing to recreational users and remote operators who may not have access to consistent shore power. The synergistic deployment of battery technology, lightweight hull design, and renewable energy integration defines the cutting edge of innovation, differentiating high-performance electric inflatable boats in a crowded market landscape and addressing the fundamental need for self-sustaining marine mobility.

The competitive landscape is increasingly characterized by strategic acquisitions designed to consolidate technological expertise. For instance, large traditional marine engine manufacturers have been acquiring specialized electric outboard producers to rapidly integrate proven, reliable electric powertrains into their extensive dealer networks and existing boat lines. This M&A activity signals a mature stage of market development where scaling up production and securing robust distribution channels are prioritized over isolated technological breakthroughs. Smaller, innovative startups continue to play a crucial role, often focusing on niche technological enhancements like advanced propeller design optimized for electric torque delivery or specialized modular battery systems. Their role as innovation incubators often makes them attractive acquisition targets for larger entities seeking to quickly expand their intellectual property portfolio and reduce time-to-market for next-generation products. This dynamic environment of competition and consolidation ensures continuous technological refinement and market accessibility.

Focusing on the segmentation by Motor Type, the Outboard Motor segment overwhelmingly dominates the market for electric inflatable boats. Electric outboards are favored for their ease of installation, high maneuverability, and simplicity of maintenance, making them suitable for retrofitting existing hulls and for modular design strategies. The instantaneous torque delivered by electric outboards provides excellent acceleration, a key safety feature in rough waters or emergency situations. Conversely, Inboard Motors, while representing a smaller share, are critical for larger, custom-built RIBs or commercial vessels where complex hull integration is required for optimal hydrodynamics and superior performance. Inboard electric systems often allow for larger battery banks and more sophisticated thermal management, catering to long-range commercial or governmental missions where sustained high speed is essential. The differentiation in motor choice directly reflects the intended application and required performance envelope of the inflatable craft.

Customer education and transparency are becoming increasingly critical marketing functions, especially concerning battery performance metrics. Unlike fuel consumption, electric range is highly dependent on environmental factors (wind, wave height, payload) and operator behavior (speed profile). Successful market players are developing sophisticated digital tools and mobile applications that provide accurate, dynamic range estimates based on real-time data input, helping users plan trips safely and manage expectations effectively. This focus on digital transparency builds trust and mitigates range anxiety, transforming a perceived restraint into a manageable operational variable. Effective communication of the Total Cost of Ownership (TCO) advantage—highlighting savings in fuel and reduced annual maintenance compared to high-cost servicing of complex ICE outboards—is paramount in converting potential customers facing the high initial investment hurdle.

In conclusion, the Electric Inflatable Boats Market stands at the cusp of mainstream adoption, driven by unavoidable global shifts toward sustainable marine transport and underpinned by substantial technological progress in energy storage and propulsion systems. While infrastructural constraints and initial costs pose challenges, the robust regulatory environment in developed markets and compelling TCO proposition for commercial users provide powerful tailwinds. Strategic imperatives must center on minimizing battery costs, expanding charging access, and leveraging AI/digital technologies to enhance range predictability and user experience. The market’s future is intrinsically linked to the speed of innovation in battery chemistry and the industry’s capacity to standardize components and infrastructure, ensuring long-term viability and dominance over fossil fuel alternatives in the light marine segment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.