ID : MRU_ 443117 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

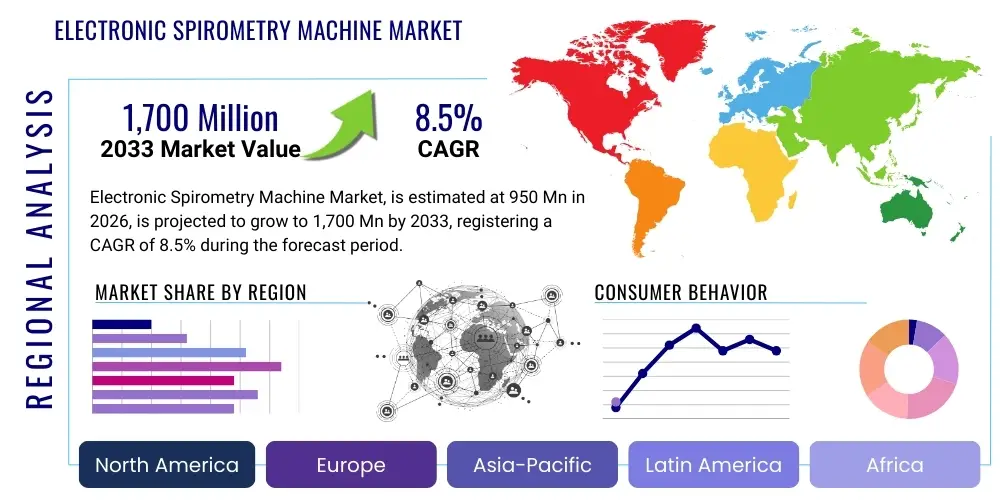

The Electronic Spirometry Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 950 Million in 2026 and is projected to reach USD 1,700 Million by the end of the forecast period in 2033.

The Electronic Spirometry Machine Market encompasses the manufacturing, distribution, and utilization of advanced diagnostic devices designed to measure lung function parameters, primarily Forced Vital Capacity (FVC), Forced Expiratory Volume in one second (FEV1), and the FEV1/FVC ratio. These devices are critical for the timely diagnosis and management of chronic respiratory diseases, including Chronic Obstructive Pulmonary Disease (COPD), asthma, pulmonary fibrosis, and restrictive lung disorders. The integration of digital components, such as connectivity (Wi-Fi, Bluetooth), sophisticated sensors, and user-friendly interfaces, differentiates electronic spirometers from traditional mechanical models, offering enhanced accuracy, data management capabilities, and compatibility with Electronic Health Record (EHR) systems.

Major applications of electronic spirometry machines span clinical settings, including hospitals, specialized pulmonology clinics, primary care physician offices, and occupational health centers, where routine screening and precise disease monitoring are essential. Furthermore, the rising adoption of portable and handheld spirometers has expanded usage into home care settings, facilitating remote patient monitoring and telepulmonology initiatives. These devices offer substantial benefits, such as objective assessment of airway obstruction, monitoring therapeutic effectiveness, and stratifying disease severity, which are paramount in personalized medicine approaches for respiratory health.

Key driving factors propelling market expansion include the escalating global prevalence of chronic respiratory illnesses, heavily influenced by aging populations, increased exposure to environmental pollutants, and rising tobacco consumption rates, particularly in emerging economies. Technological advancements focusing on miniaturization, enhanced portability, and the seamless integration of software for sophisticated data analysis are further accelerating market penetration. Regulatory support and increasing reimbursement policies for early detection diagnostics also contribute significantly to the robust market trajectory.

The Electronic Spirometry Machine Market is currently characterized by a robust growth phase, driven primarily by favorable business trends emphasizing point-of-care testing and digital health integration. Key business trends include the shift towards sophisticated, connected devices that offer real-time data transmission and integration with telehealth platforms, enabling proactive patient management outside traditional clinical environments. Strategic mergers, acquisitions, and collaborations focused on expanding geographical reach and integrating AI-driven diagnostic capabilities are common among leading market players, aiming to enhance product differentiation and efficiency in diagnostics.

Regionally, North America maintains market dominance due to high healthcare expenditure, established reimbursement frameworks, and a significant burden of COPD and asthma. However, the Asia Pacific region is projected to exhibit the highest growth rate, fueled by rapid expansion of healthcare infrastructure, increasing awareness regarding respiratory diseases, and governmental initiatives aimed at improving primary healthcare access. European markets demonstrate stable growth, supported by stringent regulatory standards and a strong focus on preventative health screenings for occupational hazards and long-term care facilities.

Segment trends highlight the significant uptake of handheld/portable spirometers, driven by the demand for flexibility and remote monitoring capabilities, especially post-pandemic. In terms of technology, the flow sensor segment, particularly ultrasonic flow sensing, is gaining prominence over traditional volume displacement methods due to enhanced accuracy and reduced need for calibration. The end-user segment reveals hospitals and diagnostic laboratories retaining the largest share, while home care settings and primary care centers represent the fastest-growing application areas, underscoring the shift toward decentralized diagnostic workflows.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Electronic Spirometry Machine Market primarily center on enhancing diagnostic accuracy, automating interpretation, and integrating predictive analytics into existing device infrastructure. Key themes revolve around how AI can minimize operator dependence, correct for poor patient maneuver execution, and improve the consistency of spirometry results across different clinical settings. There is significant expectation for AI algorithms to automatically detect subtle patterns indicative of early-stage respiratory decline, facilitating pre-emptive interventions. Furthermore, users are keenly interested in the potential of machine learning to generate personalized prognosis reports and optimize treatment regimens based on large-scale population health data correlated with individual spirometric measurements.

The implementation of AI is expected to revolutionize the clinical utility of spirometry by moving beyond simple data collection to advanced, automated diagnostic support. This shift addresses major concerns regarding the variability and subjectivity inherent in traditional interpretation methods. AI models are being trained on vast datasets to differentiate between various obstructive and restrictive patterns with greater precision than manual analysis, which is crucial in primary care settings where specialized pulmonology expertise may be limited. This integration significantly enhances the machine's functionality from a measurement tool to a sophisticated diagnostic aid.

Concerns often raised involve data security, regulatory hurdles for AI-as-a-medical-device (SaMD), and the need for standardized training datasets to prevent algorithmic bias across diverse ethnic and demographic groups. Despite these challenges, the prevailing expectation is that AI will streamline workflows, reduce the economic burden associated with misdiagnosis or delayed treatment, and ultimately democratize access to high-quality pulmonary function testing by making complex analyses instantly accessible and reliable.

The Electronic Spirometry Machine Market is governed by a dynamic interplay of factors. The primary drivers include the alarming increase in the global incidence and prevalence of Chronic Obstructive Pulmonary Disease (COPD) and asthma, often exacerbated by environmental pollution and aging populations, necessitating routine lung function assessment. Technological innovations, particularly the development of highly accurate, portable, and connected devices compatible with telemedicine infrastructure, significantly amplify market demand. Conversely, restraints involve challenges such as the high initial cost of advanced electronic spirometry systems, especially for smaller clinics or developing country healthcare systems, and the persistent lack of standardized training for operating these machines, leading to inconsistent measurement quality. The presence of technical complexities in calibration and maintenance also acts as a dampener to mass adoption.

Opportunities in this market are vast and centered on untapped potential in emerging economies, where healthcare infrastructure is rapidly developing, coupled with rising disposable incomes allocated toward preventative medicine. The expansion of home-based monitoring facilitated by compact, consumer-grade spirometers integrated with mobile applications presents a major avenue for growth. Furthermore, manufacturers have a significant opportunity to capitalize on the increasing integration of electronic health records (EHR) and cloud-based data storage solutions, streamlining clinical workflows and supporting large-scale epidemiological studies. The growing focus on occupational health and screening mandates for industries exposed to respiratory hazards also creates continuous demand.

Impact forces illustrate the strong positive influence of technological advancements (high impact, accelerating growth) contrasted with the moderate negative impact of stringent regulatory requirements and reimbursement complexities (moderate impact, constraining growth). The collective positive impact forces stemming from increasing disease burden and digital integration significantly outweigh the restraining factors, leading to a net upward trajectory for market expansion over the forecast period. Market players are strategically mitigating restraints by developing more cost-effective models and providing comprehensive training programs to ensure accurate and reliable testing procedures.

The Electronic Spirometry Machine Market is meticulously segmented based on key criteria including product type, technology, portability, and end-user, enabling a granular understanding of market dynamics and adoption patterns across different clinical and geographical landscapes. Product segmentation distinguishes between Desktop/Trolley-Based devices, typically used in specialized pulmonology laboratories for comprehensive testing, and Handheld/Portable devices, favored for flexibility, point-of-care testing, and remote patient monitoring. Technology segmentation focuses on the underlying measurement methodology, contrasting volume displacement techniques with advanced flow sensing methods, each offering distinct advantages in terms of accuracy, maintenance, and cost structure. Portability segmentation further refines the understanding of market needs, differentiating between fully mobile units suitable for emergency services and static units within established clinics.

The distinction between technologies, particularly the adoption of flow sensing mechanisms like ultrasonic and pressure differential sensors, is a critical growth area, reflecting the industry's drive toward calibration-free and highly precise measurements. Flow sensors generally offer better resistance to environmental factors and provide superior data resolution compared to older volume displacement technologies such as water sealed or dry rolling seal spirometers. This technological evolution directly impacts the machine's efficiency and lifespan, driving purchasing decisions in advanced healthcare settings. Understanding the precise demands of each end-user segment—ranging from large governmental hospitals that require robust, high-throughput desktop models to individual primary care physicians seeking compact, user-friendly handheld devices—is paramount for strategic market positioning.

End-user analysis reveals shifting purchasing power and application focus. While hospitals and specialized testing centers remain the largest consumers due to the volume of comprehensive pulmonary function tests conducted, the fastest expansion is seen in ambulatory surgical centers, primary care centers, and increasingly, home care settings, driven by chronic disease management protocols and telehealth adoption. This decentralization of diagnostics necessitates continuous innovation in device design, focusing on intuitive operation, robust connectivity features, and stringent data security compliance to meet diverse regulatory and clinical demands across segments.

The value chain for the Electronic Spirometry Machine Market commences with upstream activities focusing on the sourcing of high-precision components, including sophisticated flow and pressure sensors, microprocessors, display screens, and critical software infrastructure necessary for data processing and connectivity. Key suppliers include specialized sensor manufacturers (e.g., ultrasonic or turbine technology providers) and software developers focusing on medical device integration and compliance. Quality control and procurement efficiency at this stage are crucial, as sensor accuracy directly determines the performance and clinical reliability of the final spirometer. Research and development activities, which involve clinical trials and stringent regulatory approval processes (e.g., FDA, CE marking), form a substantial part of the upstream value addition, ensuring devices meet evolving technical and safety standards.

Midstream processes involve manufacturing, assembly, and rigorous testing of the electronic devices. This stage focuses on scaling production while maintaining device miniaturization and connectivity features. Manufacturers often integrate proprietary software and user interfaces, distinguishing their product offerings in terms of usability and data management capabilities. Downstream activities are centered on distribution, marketing, and post-sale service. Distribution channels are highly critical, involving direct sales teams for large hospital networks and specialized medical device distributors who handle inventory, logistics, and regional market penetration, particularly for smaller clinics and primary care providers.

The distribution channel is segmented into direct sales, favored for high-volume, long-term contracts with major healthcare institutions, and indirect channels (distributors, resellers), which are essential for reaching disparate clinics, occupational health centers, and increasingly, consumer-grade online retail for home-use devices. Effective servicing, calibration, and provision of consumable supplies (e.g., disposable mouthpieces, filters) are ongoing requirements that sustain revenue flow post-sale. The rise of telemedicine platforms further influences the downstream process, requiring robust cybersecurity and seamless data integration capabilities to support remote diagnostics and monitoring services.

Potential customers for Electronic Spirometry Machines are highly diverse, spanning specialized clinical environments, general medical practice, research institutions, and individual consumers managing chronic conditions. The primary purchasers are large institutional buyers, including public and private hospitals, which require advanced, multi-functional desktop spirometers to handle extensive patient throughput and conduct specialized pulmonary function tests (PFTs). Diagnostic laboratories and specialized pulmonology clinics constitute another major customer segment, seeking high accuracy and integration capabilities to support complex diagnostic protocols for diseases like cystic fibrosis and COPD.

A rapidly growing customer base includes primary care physicians (PCPs) and internal medicine specialists. As the frontline defense against respiratory diseases, PCPs increasingly adopt portable spirometers for initial screening and assessment, driven by the need for quick, actionable results at the point of care. Furthermore, occupational health clinics represent a significant niche market, utilizing spirometry for pre-employment screening and continuous monitoring of workers exposed to dust, chemicals, or other airborne irritants, ensuring compliance with workplace safety regulations and reducing industrial health risks.

The expansion of home healthcare and telehealth services has created a substantial emerging customer segment: individual patients and home care providers. These end-users typically require simple, intuitive, handheld electronic spirometers that connect seamlessly to mobile devices or cloud platforms, allowing for daily monitoring and remote data sharing with clinical specialists. Insurance providers and government health agencies also act as influential indirect customers, as their reimbursement policies and procurement mandates significantly drive the adoption rate and type of spirometry machines utilized across the healthcare continuum.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 950 Million |

| Market Forecast in 2033 | USD 1,700 Million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered |

|

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Electronic Spirometry Machine Market is rapidly evolving, moving away from legacy mechanical systems toward advanced digital and sensor-based measurement methodologies. Key technological advancements are centered around precision, miniaturization, and enhanced data connectivity. Flow sensing technology, particularly ultrasonic spirometry, represents a crucial innovation. Ultrasonic devices measure airflow based on the transit time of ultrasonic signals through the air stream, offering highly accurate, flow-rate-independent readings that do not require calibration or compensation for gas composition, density, or temperature effects, thereby reducing maintenance costs and improving data reliability compared to older turbine or pressure differential methods.

Another dominant technology involves the integration of connectivity standards, such as Bluetooth Low Energy (BLE) and Wi-Fi, facilitating seamless transmission of patient data to cloud-based servers and Electronic Health Records (EHRs). This development is fundamental to supporting telehealth services and remote monitoring programs, allowing clinicians to review accurate spirometry results asynchronously. Furthermore, the incorporation of advanced algorithms and microprocessors within the devices enhances quality assurance features, automatically checking for adherence to ATS/ERS (American Thoracic Society/European Respiratory Society) standards during testing, which is essential for obtaining clinically acceptable and standardized results.

The market is also witnessing the proliferation of smart spirometry applications developed for smartphones and tablets. These applications not only display results but also provide interactive coaching to guide patients through the forced expiration maneuver correctly, a factor critical for test validity. The future technology landscape is heavily invested in incorporating artificial intelligence for autonomous data interpretation, sophisticated error detection, and integration with broader physiological monitoring systems to create comprehensive digital respiratory health platforms, ensuring the continuous enhancement of diagnostic precision and patient engagement.

Regional dynamics heavily influence the adoption and growth trajectory of the Electronic Spirometry Machine Market, reflecting variances in healthcare spending, regulatory frameworks, disease burden, and technological readiness across the globe. North America, encompassing the United States and Canada, currently holds the largest market share. This dominance is attributed to several critical factors, including high per capita healthcare expenditure, well-established reimbursement policies for pulmonary function tests, and the high prevalence of respiratory diseases driven by lifestyle factors and environmental pollution. The region is also a pioneer in adopting cutting-edge technologies, such as connected, AI-integrated spirometers, supported by a strong push for digitalization within healthcare systems and widespread adoption of telehealth infrastructure.

Europe represents a mature and stable market, characterized by strict regulatory standards and an emphasis on preventative medicine, particularly in countries like Germany, the UK, and France. Growth in this region is primarily driven by the aging population, which necessitates greater monitoring for COPD and other age-related pulmonary disorders, along with robust national health programs that fund diagnostic equipment procurement. European market penetration is high, with a continuous demand for advanced, accurate, and standardized devices suitable for both clinical and occupational health environments.

The Asia Pacific (APAC) region is forecasted to be the fastest-growing market globally. This exponential growth is fueled by rapidly improving healthcare infrastructure investments in countries such as China, India, and Japan, coupled with a massive population base facing escalating levels of air pollution and tobacco consumption, leading to a soaring incidence of chronic respiratory illnesses. Market expansion is supported by increasing government initiatives to improve access to diagnostic tools in rural and underserved areas, favoring the uptake of cost-effective, portable, and user-friendly electronic spirometry machines. Latin America, the Middle East, and Africa (MEA) are emerging markets characterized by lower initial adoption but significant future potential driven by gradual improvements in healthcare access and infrastructure development, particularly the establishment of specialized diagnostic centers.

The exponential rise in the global prevalence of Chronic Obstructive Pulmonary Disease (COPD) and asthma, intensified by aging populations and environmental pollution, is the primary market driver, necessitating widespread lung function assessment.

Technological advancements, particularly the adoption of ultrasonic flow sensing, have significantly improved accuracy by eliminating the need for calibration. Miniaturization and wireless connectivity (Bluetooth/Wi-Fi) enhance portability, enabling reliable point-of-care and home-based testing essential for telemedicine.

The Home Care Settings and Telemedicine Providers segment is projected to exhibit the fastest growth, driven by the increasing need for remote patient monitoring, chronic disease management, and the availability of user-friendly, connected handheld spirometers.

AI integration is crucial for enhancing diagnostic quality control, automatically validating test maneuver execution, and providing automated interpretation of complex spirometry results, thereby reducing operator variability and accelerating clinical decision-making.

North America currently dominates the market share due to its high healthcare spending, established reimbursement infrastructure, significant chronic disease burden, and early adoption of advanced digital health technologies, including connected diagnostic devices.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.