ID : MRU_ 444809 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

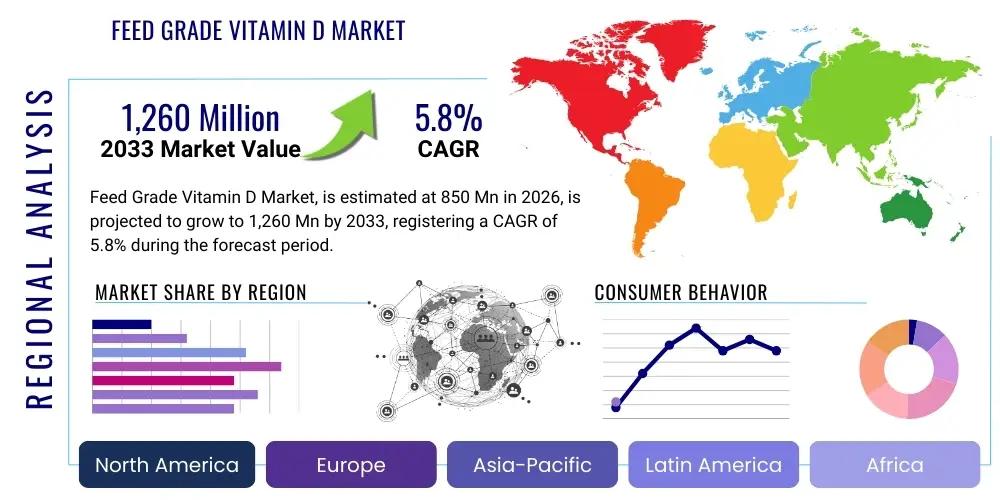

The Feed Grade Vitamin D Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 850 Million in 2026 and is projected to reach USD 1,260 Million by the end of the forecast period in 2033.

Feed Grade Vitamin D, primarily comprising Vitamin D3 (cholecalciferol) and Vitamin D2 (ergocalciferol), is an essential nutritional additive used globally in livestock and poultry diets to regulate calcium and phosphorus metabolism. This critical micronutrient ensures optimal bone development, improves immune response, and enhances reproductive performance across various animal species, including poultry, swine, cattle, aquaculture, and companion animals. The market is driven by increasing global demand for high-quality animal protein and the stringent regulatory requirements mandating nutritional completeness in commercial feed formulations. Technological advancements in synthesis and stabilization processes, particularly in developing highly bioavailable and stable forms of Vitamin D, further contribute to market expansion.

The primary applications of Feed Grade Vitamin D span the entire spectrum of commercial animal husbandry. In poultry, it is vital for eggshell quality and preventing leg weakness, while in swine, it supports growth rate and reduces skeletal disorders. For dairy and beef cattle, adequate Vitamin D status is crucial for preventing milk fever and enhancing overall herd health and productivity. The product description emphasizes its role not just as a supplement, but as a critical performance enhancer, directly impacting feed conversion ratios and overall production efficiency, making it indispensable for modern, intensive farming systems.

Key driving factors accelerating the adoption of Feed Grade Vitamin D include the rapid industrialization of the meat and dairy industries, rising consumer awareness regarding animal welfare standards (which often tie into nutritional requirements), and the necessity for livestock producers to mitigate nutritional deficiencies associated with indoor farming or specialized diets. The inherent benefits, such as reduced mortality rates, improved hatchability in poultry, and enhanced calcification, ensure its continued market prominence. Moreover, continuous research demonstrating the links between optimal Vitamin D levels and reduced incidence of disease supports sustained demand.

The Feed Grade Vitamin D market demonstrates robust growth, underpinned by fundamental demographic shifts, specifically the rising global population and the corresponding increase in animal protein consumption, particularly in emerging economies in Asia Pacific and Latin America. Business trends indicate a strong focus on backward integration among key feed manufacturers, securing raw material supply chains for precursor substances like cholesterol (for D3) or ergosterol (for D2). Strategic mergers, acquisitions, and collaborations between vitamin manufacturers and large animal nutrition companies are defining the competitive landscape, aiming to broaden geographical reach and specialized product portfolios, such as highly concentrated or microencapsulated vitamin forms designed for better stability and palatability.

Regional trends highlight Asia Pacific as the fastest-growing market, largely due to explosive growth in the livestock sector in countries like China, India, and Southeast Asian nations. These regions are transitioning from traditional farming practices to large-scale industrial operations, thereby increasing the reliance on scientifically formulated and vitamin-enriched commercial feed. North America and Europe maintain substantial market share, characterized by high regulatory oversight regarding feed quality and sophisticated consumer demand for traceability and animal health certifications, driving continuous innovation in delivery systems and quality control for Feed Grade Vitamin D products.

Segment trends underscore the dominance of Vitamin D3 over Vitamin D2, primarily due to D3’s superior bioavailability and efficacy in most monogastric animals (poultry and swine), which constitute the largest segments of commercial livestock production. However, the organic feed segment and specialized ruminant feed markets are showing increasing interest in naturally derived Vitamin D sources. Furthermore, the segmentation by form reveals a preference for powder and granular formulations due to ease of handling, mixing, and storage stability, although liquid forms are gaining traction in certain niche applications requiring precise dosing via drinking water.

Common user questions regarding AI's influence in the Feed Grade Vitamin D market center on optimizing formulation precision, predicting supply chain bottlenecks, and enhancing livestock health monitoring to prevent deficiencies. Users are keenly interested in how machine learning algorithms can analyze vast datasets—including weather patterns, feed ingredient variability, genetic profiles of animals, and disease outbreaks—to recommend dynamic, individualized Vitamin D supplementation levels rather than static averages. Key expectations include reduced over-supplementation (cost savings), minimized nutrient waste, and quicker detection of sub-clinical deficiencies, leading to better resource management and improved profitability for integrators and farmers. The application of AI is primarily viewed as a tool for elevating efficacy and sustainability within the complex realm of micro-nutrient management.

The Feed Grade Vitamin D market is significantly influenced by a confluence of driving factors, regulatory constraints, and emerging opportunities, all of which shape the competitive dynamics and long-term trajectory. Key drivers include the mandatory inclusion of Vitamin D in commercial animal diets, driven by the shift towards large-scale, indoor confinement farming where animals lack natural sun exposure. This structural change ensures a baseline demand that is highly inelastic. Furthermore, the increasing scientific evidence linking optimal Vitamin D levels to enhanced animal immunity and reduced reliance on antibiotics acts as a powerful catalyst, aligning with global efforts to combat antimicrobial resistance (AMR).

Restraints primarily revolve around the inherent instability of Vitamin D when exposed to heat, moisture, or certain minerals (like trace elements) during feed processing and storage. This instability necessitates costly stabilization techniques and potentially results in nutrient losses, impacting efficacy and cost-effectiveness. Additionally, stringent regulatory limitations on maximum inclusion levels in some developed regions, imposed to prevent toxicity, create a constraint on usage flexibility. Economic volatility in the pricing of key precursor chemicals and complex synthesis processes also poses a continuous challenge to maintaining stable profit margins for manufacturers.

Opportunities for market growth lie predominantly in the aquaculture and companion animal segments, which currently represent smaller but rapidly expanding areas of Vitamin D application. The development of next-generation, highly stabilized, and bioavailable forms (such as encapsulated or coated products) that withstand harsh pelleting conditions offers a significant technological opportunity for product differentiation. Furthermore, expansion into organic and non-GMO certified feed production, requiring specialized sources of Vitamin D2, presents a niche yet lucrative growth avenue. The market impact forces indicate that legislative requirements regarding animal health and food safety standards globally exert the strongest influence, dictating mandatory inclusion rates and quality benchmarks, thus guaranteeing consistent market performance.

The Feed Grade Vitamin D market is comprehensively segmented based on Type, Application, Form, and Region, allowing for a detailed understanding of consumer preferences and operational requirements across the diverse animal nutrition industry. Segmentation by Type distinguishes between Vitamin D3 (cholecalciferol), which dominates due to its superior efficacy in poultry and swine, and Vitamin D2 (ergocalciferol), which is gaining traction in organic and specialized ruminant diets. The application segment reflects the largest end-user markets, with poultry maintaining the foremost position globally, followed by swine, cattle, and the high-growth aquaculture sector. Understanding these segments is crucial for manufacturers in tailoring product specifications, such as concentration levels and particle size, to specific animal nutritional needs.

Segmentation by Form is critical for assessing processing requirements and storage logistics within feed mills. Powder and granular forms currently hold the majority share, appreciated for their ease of uniform dispersion within dry feed mixes and their relatively stable shelf life. The granular form is often preferred in large-scale operations due to reduced dust exposure and improved flowability. Conversely, liquid forms, although sensitive to degradation, are increasingly utilized in veterinary medicine and precision liquid feed supplementation systems, offering rapid absorption and targeted dosing capabilities, particularly for sick or recovering animals.

The market structure is highly fragmented yet exhibits consolidation potential in the core manufacturing sector. Market participants strategically invest in quality assurance and traceability systems to comply with international standards, ensuring that the Feed Grade Vitamin D meets strict purity criteria required for certified feed production. The continuous introduction of enhanced formulations, such as those co-processed with antioxidants or encapsulated with protective matrices, reflects the market's response to the persistent technical challenge of nutrient degradation during feed production processes.

The value chain for Feed Grade Vitamin D is intricate, starting with the synthesis of key precursor molecules in the upstream stage. For Vitamin D3, this involves the synthesis or extraction of cholesterol, which is then chemically or photosynthetically converted to 7-dehydrocholesterol, followed by irradiation and purification to yield the final vitamin concentrate. For Vitamin D2, the process begins with the fermentation or extraction of ergosterol, primarily derived from yeast. The upstream segment is capital-intensive and concentrated among a limited number of specialized chemical and pharmaceutical manufacturers, exerting significant control over raw material pricing and global supply stability. Quality control at this initial stage is paramount, as purity directly impacts the effectiveness and safety of the final feed additive product.

The midstream phase involves the stabilization, formulation, and blending of the raw vitamin concentrate into a commercially viable feed grade product. This crucial stage addresses the vitamin’s inherent sensitivity to oxidation and degradation. Manufacturers develop various protective matrix technologies—such as spray drying, microencapsulation, and lipid coating—to ensure the vitamin remains active and homogenous when mixed into complex feed premixes. Distribution channels are highly specialized, relying on both direct sales to large integrators and indirect sales through a network of specialized feed additive distributors and nutrition consultants who provide technical support to end-users on appropriate inclusion rates and handling protocols.

The downstream segment culminates in the integration of the vitamin product into final animal feed. This process is carried out by commercial feed manufacturers (integrators) and livestock producers (on-farm mixers). The direct channel involves high-volume sales to major global feed companies that often incorporate the vitamin directly into their own premixes. The indirect channel relies on regional distributors serving smaller, localized farms and specialized producers. End-user feedback, especially concerning palatability, shelf stability, and animal performance metrics, drives product modification and innovation within the upstream formulation segment, completing the circular flow of the value chain.

The primary potential customers and end-users of Feed Grade Vitamin D products are globally integrated animal protein producers and specialized commercial feed manufacturers. Large-scale poultry integrators, covering both broiler and layer operations, represent the largest and most consistently growing customer base due to the non-negotiable requirement for Vitamin D in achieving optimal bone integrity and eggshell quality. These customers demand high-purity, standardized products, often purchased in bulk directly from major global vitamin suppliers to ensure supply chain efficiency and competitive pricing.

Another significant customer group includes swine producers and cattle operations (both dairy and beef). Swine farms utilize Vitamin D to support rapid skeletal growth and prevent lameness, while dairy farms focus on minimizing the incidence of post-parturient diseases like milk fever, which is directly linked to calcium metabolism regulated by Vitamin D. These segments often rely on local or regional feed mills to supply specialized supplements, making distribution networks that cater to regional livestock practices highly critical for market penetration.

The rapidly expanding niche customer segments, such as aquaculture and companion animal feed manufacturers, offer substantial growth potential. Aquaculture feed producers for salmon, tilapia, and shrimp require tailored Vitamin D formulations that remain stable in aquatic environments and support efficient mineralization. Similarly, premium pet food brands emphasize nutritional completeness and often utilize advanced, high-stability forms of Vitamin D to meet the rising consumer expectations regarding pet health and longevity. These customers prioritize product quality, traceability, and robust technical support over cost, representing a lucrative opportunity for innovative suppliers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1,260 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DSM Nutritional Products, BASF SE, ADM Animal Nutrition, Lonza Group, Zhenjiang Holley Chemical Co., Ltd., Dishman Group, Zhejiang Garden Bio-chemical High-tech Co., Ltd., Zhejiang Xinhecheng Co., Ltd., Zhejiang NHU Co., Ltd., Novozymes A/S, Kemin Industries, Nutreco N.V., Cargill Incorporated, Bluestar Adisseo Co., Ltd., Global Bio-Chem Technology Group Company Limited, Givaudan SA, Balchem Corporation, Phibro Animal Health Corporation, Vaxxinova, Impextraco NV |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Feed Grade Vitamin D market is dominated by synthesis and stabilization innovations designed to overcome the inherent fragility of the vitamin molecule. The production of both Vitamin D2 and D3 relies on highly specialized photochemical conversion processes, primarily involving UV irradiation of precursor sterols (7-dehydrocholesterol or ergosterol). Advanced manufacturing utilizes highly controlled reactor environments and chromatographic purification techniques to maximize yield and ensure high purity levels, minimizing the presence of inactive isomers or byproducts which could affect animal health or product stability. Manufacturers are heavily investing in process optimization, often incorporating continuous flow chemistry to enhance efficiency and scalability of the synthesis phase.

The most crucial technological advancements are observed in formulation and stabilization, aimed at protecting the vitamin during the harsh pelleting and storage conditions typical of commercial feed production. Key technologies include microencapsulation, where active Vitamin D particles are sealed within a protective matrix of starch, gelatin, or lipid layers. This technology significantly improves thermal stability, reduces degradation upon contact with trace minerals (which act as catalysts for oxidation), and extends the shelf life of the premix. Furthermore, the development of stabilized dry Vitamin D powders with high concentrations minimizes freight costs and enhances ease of handling for feed mill operators.

Emerging technologies focus on enhancing bioavailability and moving towards sustainable sourcing. Research is progressing on enzymatic methods for producing precursor sterols, potentially offering a more sustainable alternative to chemical synthesis. Furthermore, novel delivery systems, such as nano-emulsions or liposomal delivery, are being explored, particularly for liquid supplements used in high-value livestock or companion animals, promising faster and more efficient absorption. The integration of digital monitoring tools throughout the value chain, utilizing sensors to track temperature and humidity in storage, also represents a critical technological layer for maintaining product integrity until consumption.

Regional dynamics play a significant role in shaping the Feed Grade Vitamin D market, driven by varying livestock demographics, consumption patterns, and regulatory frameworks. Asia Pacific (APAC) stands out as the primary growth engine, fueled by the massive scale of poultry and swine production in countries like China, Indonesia, and Vietnam. The rapid adoption of modern, intensive farming techniques across APAC necessitates the consistent use of commercial feed supplements, directly correlating with high demand for Vitamin D. Regulatory initiatives in this region, increasingly focusing on feed safety and disease prevention, further solidify market penetration.

North America and Europe represent mature markets characterized by stringent quality standards and a high degree of technological integration. In these regions, demand is stable, driven by constant optimization in feed formulation and a strong emphasis on animal welfare, which mandates optimal nutrition to ensure robust skeletal and immune health. European manufacturers often favor Vitamin D products that adhere to complex EU Novel Food regulations, pushing innovation towards specific stabilized and traceable formulations. The focus here is less on volume growth and more on value-added, highly technical products.

Latin America (LATAM), particularly Brazil and Argentina, demonstrates strong growth potential, primarily driven by expanding beef and poultry export markets. The scale of livestock operations in these countries requires large volumes of feed additives, positioning LATAM as a key manufacturing and consumption hub. Conversely, the Middle East and Africa (MEA) market is smaller but expanding, primarily driven by localized growth in poultry production to meet rising domestic meat consumption, though market growth can be constrained by local sourcing challenges and logistical complexities.

Vitamin D3 (cholecalciferol) is generally preferred in monogastric animals (poultry, swine) due to its higher biological activity and efficacy. Vitamin D2 (ergocalciferol), derived from plant sterols (ergosterol), is often utilized in organic feed formulations and is considered effective for ruminants and certain specialized feeds.

The heat, pressure, and moisture generated during feed pelleting processes can significantly degrade unprotected Vitamin D, leading to a loss of nutritional value. Manufacturers utilize advanced stabilization technologies, such as microencapsulation and coating, to create products that withstand high temperatures and harsh mixing conditions, ensuring retained efficacy upon consumption.

The poultry feed segment, encompassing both broiler and layer operations, holds the largest market share globally. This dominance is due to the critical role of Vitamin D in ensuring robust bone development, preventing leg disorders in broilers, and maximizing eggshell strength and hatchability in laying hens.

Regulatory bodies, particularly in North America and the European Union, impose strict maximum inclusion limits for Feed Grade Vitamin D to prevent toxicity and ensure food safety. These regulations necessitate precise formulation and rigorous quality control, directly impacting manufacturing costs and pricing strategies for compliant products.

Key opportunities lie in the rapidly expanding aquaculture sector and the premium companion animal segment, both demanding specialized, highly stable vitamin formulations. Furthermore, product innovation focusing on enhanced bioavailability and solutions for organic/sustainable feed production offers significant revenue potential.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.