ID : MRU_ 443721 | Date : Feb, 2026 | Pages : 255 | Region : Global | Publisher : MRU

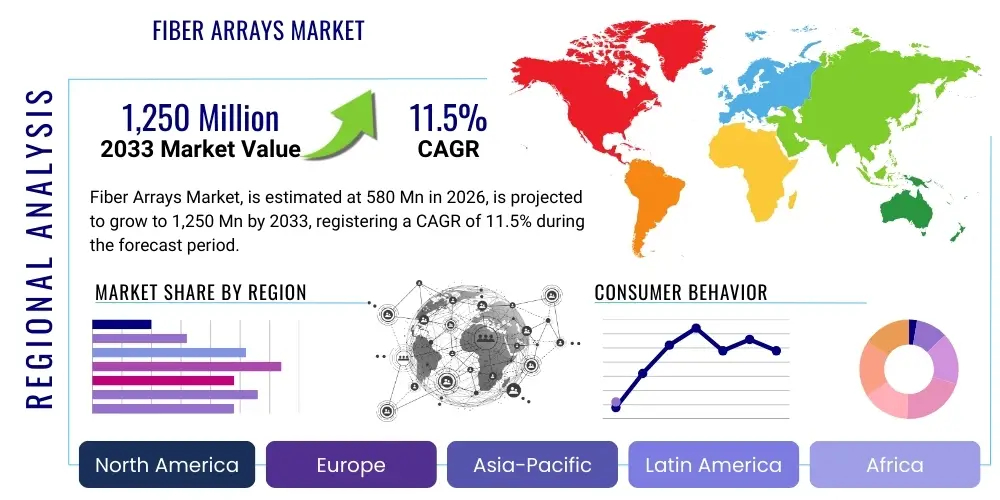

The Fiber Arrays Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at USD 580 Million in 2026 and is projected to reach USD 1,250 Million by the end of the forecast period in 2033.

The Fiber Arrays Market encompasses the manufacturing and distribution of precision optical components designed to accurately align and interface multiple optical fibers with other components, such as planar lightwave circuits (PLCs), waveguides, or integrated photonic chips. These components are critical for achieving high-density optical coupling and efficient light transmission in complex optical systems. Fiber arrays typically consist of V-grooves etched into a substrate material like glass or silicon, which precisely hold the fibers in place, ensuring sub-micron alignment accuracy necessary for high-performance applications. The demand for these components is intrinsically linked to the relentless growth in data consumption and the subsequent need for faster, higher-capacity optical communication networks. As data centers scale up and adopt 400G and 800G transmission standards, the role of precisely manufactured fiber arrays becomes increasingly vital for reliable connectivity.

Key applications driving this market include high-speed data transmission modules (transceivers), optical sensing devices, medical imaging equipment (such as Optical Coherence Tomography or OCT), and high-power laser systems used in industrial and defense sectors. The product description centers on customizability; fiber arrays vary widely based on fiber count (from 2 to 64 or more), pitch (distance between fibers), and termination requirements. The principal benefits of utilizing fiber arrays are superior coupling efficiency, reduction in assembly time and complexity, and enhanced thermal stability, which is crucial for maintaining performance in stringent operational environments. Precision alignment ensures minimal insertion loss, maximizing the overall efficiency of the photonic system.

The primary driving factors accelerating market expansion include the massive investments in 5G infrastructure deployment globally, which requires dense wavelength division multiplexing (DWDM) capabilities reliant on precise array interfaces. Furthermore, the rising adoption of silicon photonics technology—where fiber arrays serve as the crucial optical-to-electrical conversion interface—is fueling market growth. Technological advancements in fabrication techniques, particularly in highly precise etching and polishing processes for V-grooves, are enabling the production of lower-cost, higher-channel-count arrays, further broadening their applicability across emerging fields like quantum computing and autonomous vehicle LiDAR systems. The convergence of these technological and market demands positions the Fiber Arrays Market for sustained and significant expansion throughout the forecast period.

The Fiber Arrays Market is experiencing robust expansion, primarily driven by transformative business trends focusing on high-capacity data transfer and miniaturization of optical components. The shift from traditional copper infrastructure to all-optical networks across metro, long-haul, and particularly intra-data center environments mandates the use of precision coupling components like fiber arrays. Key business trends include aggressive mergers and acquisitions among components manufacturers seeking vertical integration or specialized niche technology acquisition, along with a focus on automating the manufacturing process to meet stringent quality requirements at higher volumes. The increasing adoption of co-packaged optics (CPO) by hyperscale cloud providers represents a paradigm shift, where fiber arrays become integral structural elements within the ASIC packaging itself, necessitating tighter tolerances and innovative thermal management solutions.

Regionally, Asia Pacific (APAC) stands out as the highest growth area, fueled by massive government investments in optical communication infrastructure, notably in China, South Korea, and Japan, to support industrial digitalization and 5G rollout. North America, while a mature market, remains the largest consumer in terms of value, driven by the concentration of hyperscale data centers and leading photonic technology research institutions. European market growth is steady, emphasizing specialized applications in medical diagnostics and high-power industrial lasers. Segments trends highlight a strong transition towards 2D Matrix Fiber Arrays and Polarization-Maintaining (PM) Fiber Arrays, reflecting the growing complexity and demands for coherent communication and advanced sensor applications. Simultaneously, the single-mode fiber array segment continues to dominate revenue due to its indispensable role in long-distance high-speed data transmission and data center interconnects.

The market outlook is highly positive, underpinned by sustained capital expenditure in telecom and IT sectors. Companies are strategically investing in advanced silicon photonics coupling techniques, moving beyond simple V-groove arrays toward integrated lensing and micro-optics solutions to improve efficiency and reduce form factor. The market success hinges on providers’ ability to deliver highly customized, thermally stable, and reliable products at competitive prices, particularly for mass deployment in pluggable transceivers operating at 400G and above. Supply chain resilience, especially concerning specialized raw materials like UV-curable epoxies and high-purity silica glass, remains a critical operational consideration as global demand intensifies.

Analysis of common user questions regarding AI's influence on the Fiber Arrays Market reveals key themes centered around manufacturing efficiency, quality control, and the enabling role of AI infrastructure. Users frequently inquire about whether AI can reduce the sub-micron alignment time during array assembly, how AI-driven machine vision systems enhance the inspection of V-groove structures, and what role fiber arrays play in supporting the high-bandwidth requirements of large AI model training clusters. The overriding concern is how component suppliers can leverage AI/ML to drastically improve yield rates and reduce the labor-intensive aspects of precision manufacturing, while the primary expectation is that the exponential data growth generated by AI applications will necessitate an even greater volume and complexity of high-performance fiber array components.

AI is transforming the manufacturing processes within the fiber array sector by introducing superior levels of automation and precision that surpass human capabilities. Specifically, machine learning algorithms are being integrated into optical alignment machinery to predict and compensate for thermal drift and material variations in real time, drastically optimizing the passive alignment process and achieving faster cycle times. Furthermore, advanced predictive maintenance models, powered by sensor data collected from manufacturing equipment, allow companies to anticipate equipment failure, minimizing downtime and ensuring continuous high-volume production crucial for scaling up infrastructure deployment. This shift towards smart manufacturing ensures tighter quality tolerances and better cost management, particularly vital for suppliers catering to high-volume transceivers needed for hyperscale data centers.

From an application perspective, AI acts as a major market accelerator. The sheer computational demands of AI training, including deep learning and generative models, necessitate massive, high-speed optical interconnects to link thousands of GPUs/TPUs within data center clusters. Fiber arrays are the fundamental optical component enabling these high-density optical connections (e.g., using multi-fiber push-on/pull-off, or MPO, connectors which rely on fiber arrays), supporting the unprecedented bandwidth requirements of AI workloads. Consequently, the proliferation of AI infrastructure directly correlates with an increased demand for high-channel-count, low-loss 2D fiber arrays capable of supporting complex mesh topologies required for massive AI model training and inference servers.

The Fiber Arrays Market dynamics are characterized by a strong push from technology adoption balanced against technical complexity and high initial investment. The primary drivers include the global expansion of high-speed communication networks, rapid growth in hyperscale data centers demanding 400G and 800G connectivity, and the technological breakthrough of silicon photonics requiring precise interfacing components. These forces propel market growth by creating an inescapable need for reliable, high-density optical coupling solutions. Conversely, the market faces restraints rooted in the extreme precision required for manufacturing, leading to high production costs, and the technical challenge of achieving perfect thermal stability across dense arrays. Opportunities lie in developing low-cost, high-yield manufacturing processes, leveraging integrated optics, and expanding applications into emerging fields like quantum communication and advanced LiDAR systems for autonomous vehicles. These combined forces dictate the pace and direction of technological innovation and market penetration.

Drivers: The explosive demand for bandwidth, driven by video streaming, cloud computing, and the IoT ecosystem, is the foundational driver. Specifically, the widespread deployment of 5G networks necessitates vast upgrades in core and metro networks, where optical transport infrastructure relies heavily on array technology for multiplexing and switching. Furthermore, the commercial maturity of technologies utilizing high-channel count MPO connectors, which are essentially housed fiber arrays, in modern data center fabrics ensures sustained volume demand. The migration towards silicon photonics, allowing for high integration density and lower power consumption, inherently requires highly accurate interface components to couple light from the fiber into the on-chip waveguide structure efficiently. This technology transition compels device manufacturers to adopt precision fiber array solutions.

Restraints: The most significant restraint is the manufacturing complexity required to achieve sub-micron dimensional tolerances. V-groove etching, polishing, and precise epoxy dispensing are delicate processes that require expensive, specialized equipment and highly skilled labor, contributing to high production costs and relatively lower yield rates compared to standard components. Additionally, ensuring long-term reliability and stability, particularly in harsh environments (e.g., high humidity or extreme temperatures) or under high-power laser irradiation, poses a technical constraint. Insertion loss sensitivity due to environmental fluctuations or minor misalignment requires constant design optimization, increasing R&D overhead. The reliance on highly customized designs for specific applications (like specialized sensing or high-power laser delivery) also hinders mass standardization, limiting economies of scale.

Opportunities: Significant growth opportunities exist in addressing the emerging need for 2D (matrix) fiber arrays, particularly for advanced sensor arrays and complex photonic integrated circuits (PICs). Developing innovative bonding techniques and materials that offer better thermal management and environmental protection would unlock new revenue streams in demanding industrial and aerospace applications. The convergence of optics and electronics (co-packaged optics) presents a massive future opportunity, where fiber arrays will be integrated directly onto electronic chips, revolutionizing server architecture. Furthermore, the increasing adoption of Fiber Bragg Grating (FBG) sensors in structural health monitoring and the medical sector’s reliance on OCT systems create diverse niche markets that can be served by specialized, highly customizable fiber arrays.

The Fiber Arrays Market is comprehensively segmented based on Type, Fiber Type, Application, and End-User, reflecting the diverse technical requirements across the optical industry. Segmentation by Type, focusing on the structural configuration, is essential as it dictates the array's complexity and channel count, ranging from simple single-row configurations to highly complex 2D matrix arrays. The Fiber Type distinction, primarily between single-mode (SM) and multi-mode (MM) fibers, is critical because it determines the transmission characteristics (bandwidth, distance) and, consequently, the target application (long-haul vs. short-reach interconnects). Application segmentation illustrates where the core demand lies, with Data Centers and Telecom consistently leading, followed by specialized industrial and medical uses, while End-User categorization clarifies the primary purchasing entities, typically module manufacturers, system integrators, and research facilities.

The most lucrative segment, currently, is the V-Groove Fiber Array based on Type, due to its established reliability, high precision, and cost-effectiveness in high-volume applications like transceiver manufacturing. However, the fastest growth is anticipated in the 2D Fiber Array segment, driven by new technologies that require complex, spatially organized beam steering or coupling, such as advanced LiDAR and integrated photonic chip testing. Within the Fiber Type segment, Single-Mode Fiber Arrays account for the largest revenue share, fundamentally supporting all modern high-speed long-distance communication links, including hyper-scale data center interconnects and metro networks operating at 400G and beyond. Multi-mode arrays, while having a smaller market share, remain vital for specific short-reach, high-bandwidth legacy data center environments and specialized sensor systems.

The Application segment is dominated by the Telecommunications and Data Communication sector, which serves as the backbone consumer for both high-end and standard fiber arrays. This segment's growth is directly correlated with global internet traffic and cloud infrastructure expansion. Emerging applications like High-Power Laser systems and Medical Devices (e.g., surgical lasers and advanced diagnostics) offer higher profit margins but lower volume, requiring custom-engineered solutions that demand extremely stringent performance specifications regarding material purity and thermal handling. Successful market participants must maintain a diversified product portfolio capable of addressing the mass-market demands of telecom while retaining the expertise needed for highly specialized, precision-engineered industrial and medical solutions.

The value chain of the Fiber Arrays Market is characterized by a high degree of specialization and technical precision across all stages, beginning with specialized raw material procurement and culminating in complex system integration. Upstream analysis highlights the critical role of material suppliers providing high-purity glass, silicon wafers (for V-groove etching), specialized optical fibers (SM, MM, PM), and highly controlled UV-cured epoxies. The quality and consistency of these raw materials directly impact the final array performance, particularly concerning thermal stability and light transmission characteristics. Due to the stringent quality requirements, the upstream supply base is relatively concentrated, often involving collaborations between component manufacturers and material science firms to ensure specifications are met, particularly for next-generation products requiring extremely low coefficient of thermal expansion (CTE).

The core manufacturing process involves highly advanced fabrication steps: V-groove etching (typically wet chemical or dry plasma etching of silicon or glass), precision fiber insertion and passive alignment (often using sophisticated robotic systems under optical guidance), and meticulous end-face polishing to achieve low reflection and minimum loss. This midstream segment is dominated by specialized fiber optic component manufacturers who possess the proprietary etching and alignment technologies. Downstream analysis focuses on the integration of the finished fiber array into higher-level optical components, such as pluggable transceivers (QSFP, OSFP), optical switches, or specialized sensor heads. Transceiver manufacturers are the largest direct buyers, integrating the array components into modules before selling them to hyperscale data center operators and telecom carriers.

Distribution channels for fiber arrays are bifurcated into direct sales and indirect representation. Direct sales are predominantly used for high-volume orders placed by major transceiver OEMs and large system integrators, allowing for customized specifications and closer quality control collaboration. Indirect channels involve distributors and value-added resellers (VARs) who cater to smaller volume buyers, research institutions, and niche industrial customers, providing technical support and localized inventory management. The efficiency of the distribution channel is critical for time-sensitive market deployment, especially during rapid network upgrade cycles. Given the technical complexity, technical support and post-sales calibration services form an essential part of the value proposition, particularly in markets like high-power laser delivery and aerospace where reliability is paramount.

The potential customer base for the Fiber Arrays Market spans several high-technology sectors, but the largest volume purchasers are manufacturers involved in data communication and telecommunications infrastructure. Specifically, these include Original Equipment Manufacturers (OEMs) specializing in optical transceivers, such as those producing QSFP-DD, OSFP, and CFP modules, which require precise, high-channel count fiber arrays for coupling light between the external fiber cable and the internal photonic components (like lasers, modulators, and photodetectors). These customers operate under intense pressure to minimize insertion loss and maximize bandwidth in their products, making the quality and precision of the fiber array a critical differentiator. Hyperscale data center operators, while often buying the final transceiver product, heavily influence component specification due to their massive deployment scale and need for energy-efficient, robust interconnects.

Beyond traditional telecom, a rapidly expanding segment of buyers includes producers of advanced sensing systems, particularly those involved in medical imaging (Optical Coherence Tomography or OCT systems) and autonomous navigation technology (LiDAR systems). These end-users require highly customized, often 2D matrix arrays or specialized Polarization-Maintaining (PM) arrays to handle complex beam shaping and polarization control. In the medical sector, precision is necessary for non-invasive high-resolution imaging, while in LiDAR, the array facilitates precise coupling to laser sources and detector arrays for accurate distance and velocity mapping. These niche buyers prioritize customized dimensions, high reliability under varying conditions, and low unit volume but often offer higher profit margins due to the specialized nature of the product.

A third major category of potential customers includes industrial laser system manufacturers and research institutions. Industrial applications, such as high-power cutting and welding lasers, utilize specialized fiber arrays for efficient beam delivery, requiring components that can withstand extremely high optical power without degradation or thermal runaway. Research institutions, particularly those engaged in quantum communication, integrated photonics research, and next-generation computing architectures, represent an important segment for experimental and low-volume, ultra-high-precision arrays. For all segments, purchasing decisions are heavily influenced by the supplier’s ability to meet stringent geometric specifications (pitch, angular alignment), demonstrated reliability data (MTBF), and competitive pricing relative to the achieved precision level.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 580 Million |

| Market Forecast in 2033 | USD 1,250 Million |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Suntec Fiber Optics, Sanwa Components, Fiber Optic Center Inc. (FOC), Chiral Technologies, Fiberlabs Inc., US Conec, Santec Corporation, Molex, SCHOTT AG, Precision Micro-Optics, SENKO Advanced Components, Adamant Namiki Precision, Coherent Corp., Corning Incorporated, DiCon Fiberoptics, Amphenol Corporation, Fujikura, Huber+Suhner, Gooch & Housego, Sumitomo Electric Industries. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Fiber Arrays Market is defined by the continual pursuit of higher precision, greater integration density, and improved cost efficiency, largely driven by the demands of next-generation optical communication (400G/800G) and silicon photonics. The foundational technology remains the precision V-groove fabrication, utilizing advanced micro-machining and etching techniques on substrates like silicon, glass, or polymer. Silicon V-groove arrays are particularly dominant due to the established reliability and scalability of silicon processing techniques, allowing for sub-micron fiber alignment accuracy (typically 0.5 µm or less). Recent technological innovations focus on improving the yield and consistency of these etching processes, employing deep reactive ion etching (DRIE) for better aspect ratio control and smoothness, crucial for minimizing light scattering and insertion loss. Furthermore, the development of specialized optical epoxies that exhibit ultra-low shrinkage and robust thermal properties is critical for maintaining alignment integrity across wide operating temperature ranges.

A major technological frontier is the transition towards advanced coupling mechanisms to facilitate interfaces with Photonic Integrated Circuits (PICs). Edge coupling and grating coupling are two primary approaches impacting fiber array design. Edge coupling requires highly precise arrays positioned perpendicularly to the PIC waveguide, demanding extremely low profile designs and complex angle polishing. Grating coupling, conversely, allows for surface coupling but requires the fiber array to be precisely angled and positioned over the integrated grating structure. The fiber arrays designed for these applications often integrate micro-lenses (lens arrays) directly onto the fiber tips or the array substrate to improve mode field diameter matching between the fiber and the PIC waveguide, thereby significantly boosting coupling efficiency and tolerance to alignment errors. The integration of such micro-optics is a key area of differentiation among leading manufacturers.

Another crucial technological advancement involves 2D Fiber Arrays (Matrix Arrays), necessary for emerging applications like optical switching fabrics, quantum computing interfaces, and advanced active sensing. Manufacturing 2D arrays introduces higher complexity in both substrate design and passive alignment, requiring sophisticated robotic pick-and-place systems and specialized bonding techniques to ensure positional accuracy across multiple rows and columns. Furthermore, Polarization-Maintaining (PM) Fiber Array technology is gaining traction, necessary for coherent optical transmission and fiber optic gyroscopes. PM arrays require specialized assembly processes to ensure that the polarization axis of the stress-applying parts within the PM fiber is accurately aligned across the entire array, a process monitored using real-time polarization measurement systems. Overall, the market is shifting toward automated, highly repeatable, and thermally robust assembly technologies to meet the stringent performance metrics of future optical networks.

The exponential growth in data traffic and the massive deployment of 400G and 800G optical transceivers in hyperscale data centers are the primary drivers. These high-speed interconnects necessitate high-density components like 16-channel, 32-channel, or 64-channel fiber arrays to manage parallel optical signal transmission efficiently.

Silicon Photonics requires Fiber Arrays with extremely high precision (sub-micron accuracy) for robust passive alignment. Designs must incorporate specialized features, such as micro-lenses or angled surfaces, to efficiently couple light between the fiber and the small mode-field diameter of the on-chip waveguide structures, minimizing insertion loss.

For high-performance applications, particularly in single-mode systems interfacing with integrated circuits, the alignment tolerance required for V-grooves and fiber pitch is typically ultra-tight, often demanding precision better than 0.5 micrometers (µm) to ensure low insertion loss and reliable coupling efficiency over the product lifespan.

The Asia Pacific (APAC) region, led by China and South Korea, is experiencing the fastest growth. This is due to accelerated 5G infrastructure development, government-backed digitalization initiatives, and large-scale manufacturing capacity for optical communication modules serving global markets.

Single-row arrays align fibers linearly (e.g., 4 or 8 fibers in a straight line) primarily for standard MPO connections. 2D Matrix arrays arrange fibers in a grid (e.g., 8x8 or 16x16) for more complex spatial applications like advanced optical switching, specialized sensing, and interfacing with large-scale photonic components.

The technological foundation of fiber arrays, specifically the reliance on precision etching techniques like Deep Reactive Ion Etching (DRIE) for creating accurate V-groove geometries in silicon or glass substrates, remains a cornerstone of the market. This manufacturing precision is fundamental because any deviation from the required fiber pitch or height can dramatically increase insertion loss, thereby degrading system performance. As bandwidth demands increase and systems transition to higher data rates (e.g., 1.6T), the requirements for these physical tolerances become increasingly stringent. Market leaders are continuously investing in proprietary processes to minimize process variation, which is essential for scaling up production while maintaining quality consistent with Telcordia and other industry standards.

The push for miniaturization and integration in optical modules necessitates innovation in packaging and assembly. Co-Packaged Optics (CPO), which integrates optical engines directly within the same package as the ASIC, is driving the need for fiber arrays that are significantly smaller, lighter, and capable of operating under higher ambient temperatures close to the heat-generating electronics. This paradigm shift requires specialized low-CTE materials and new methods for secure, high-precision bonding that can withstand prolonged thermal cycling. Manufacturers are exploring passive alignment enhancement techniques, often utilizing UV-cured index-matching epoxies that offer superior environmental protection and long-term stability, critical for achieving the required Mean Time Between Failures (MTBF) targets set by hyperscale operators.

Furthermore, the increasing use of specialized fiber types, such as Polarization-Maintaining (PM) fibers and specialty large-mode-area (LMA) fibers for high-power lasers, introduces additional manufacturing complexities. PM fiber arrays must align the fiber’s internal polarization axes with extreme accuracy, a process that demands active alignment using specialized monitoring equipment rather than relying solely on passive V-groove placement. Similarly, LMA fiber arrays require highly precise mechanical tolerances and optimized end-face geometries to prevent power degradation and potential damage when handling high-power laser output in industrial or defense applications. These specialized technologies represent premium segments of the market where intellectual property and manufacturing know-how are significant competitive advantages.

The core value proposition delivered by fiber array manufacturers resides in their ability to bridge the gap between delicate optical fibers and highly rigid planar optical or electronic components. Upstream material selection directly influences the array's robustness; for example, using quartz glass or high-purity fused silica substrates ensures excellent optical transparency and minimal thermal expansion, vital for high-reliability components. The sourcing of specialty optical fibers, especially for multi-core or PM applications, also dictates the product's final capability. Given the global nature of fiber optic component supply chains, strategic relationships with specialized raw material providers are paramount for securing supply and managing quality control effectively, especially during periods of high demand growth driven by global network upgrades.

The midstream value chain, where the actual array assembly occurs, involves highly capital-intensive manufacturing facilities. Key activities here include not only the V-groove fabrication but also the complex process of fiber placement, fixation, and precision polishing. Automation is increasingly deployed in this phase to maintain the sub-micron accuracy required at scale. Machine learning and robotic vision systems are utilized to inspect groove quality and perform highly repeatable fiber insertion and bonding procedures, significantly reducing reliance on manual labor for alignment, which historically has been a bottleneck. Companies that invest heavily in automated manufacturing and superior cleanroom environments are better positioned to capture large-volume orders from top-tier transceiver manufacturers.

Downstream activities are characterized by intense collaboration between array suppliers and optical engine integrators. Since fiber arrays are custom-designed components tailored to specific transceiver architectures or sensor packages, the distribution channel often involves dedicated technical support teams working closely with the customer’s R&D department. The performance verification and testing protocols applied post-manufacturing are extensive, covering insertion loss, return loss, polarization extinction ratio (for PM arrays), and thermal cycling performance. For high-volume markets like data centers, efficient logistics and just-in-time inventory management are crucial, whereas for niche markets like aerospace or medical, the emphasis shifts entirely to quality documentation, traceability, and long-term supply stability.

Within the potential customer ecosystem, the segment comprising Transceiver and Module Manufacturers (such as Cisco, Lumentum, Innolight, etc.) represents the highest volume of consumption. Their procurement cycles are closely tied to the capital expenditure cycles of hyperscale cloud providers (Amazon, Google, Microsoft). Fiber arrays are purchased as critical, often custom-specified, components for mass-produced products like 400G and 800G QSFP/OSFP modules, forming the backbone of cloud networking infrastructure. These buyers demand stringent quality specifications, highly competitive pricing, and assurance of scalable production capacity, making suppliers' manufacturing capability a primary selection criterion.

A secondary, yet highly influential, customer group consists of providers of advanced test and measurement (T&M) equipment, particularly those specializing in characterizing optical components, integrated circuits, and high-speed networks. T&M applications require fiber arrays with exceptional stability and reliability, often used to create permanent precision interfaces in complex testing rigs. These arrays might have specialized features, such as integrated beam collimators or specific numerical aperture requirements, demanding bespoke engineering. While the volume purchased by T&M companies is lower than telecom OEMs, these customers often require the absolute highest level of geometric precision available in the market.

The continuous growth in advanced sensing applications, including fiber optic gyroscopes (FOGs) used in inertial navigation systems and sophisticated structural health monitoring systems, expands the customer base beyond conventional communication. FOG manufacturers require specialized PM fiber arrays for maintaining signal integrity and accuracy under dynamic conditions. Similarly, the integration of fiber arrays into complex sensor heads, such as those used in large infrastructure monitoring or environmental surveillance, requires array designs that are extremely ruggedized and resistant to environmental ingress, broadening the supplier engagement beyond typical cleanroom specifications into industrial-grade requirements.

The dominance of North America in terms of market value is sustained not only by the immense volume of data center deployment but also by its leadership in next-generation photonic research and development. This region often dictates the earliest adoption of advanced technologies like silicon photonics integration and Co-Packaged Optics. Consequently, fiber array suppliers serving this market must possess robust R&D capabilities and the ability to rapidly prototype and scale complex, highly customized 2D and lensed fiber array solutions. Intellectual property protection and joint development agreements between array manufacturers and U.S. technology giants are common in this environment, focusing on solving critical challenges related to thermal management and passive alignment efficiency for future 1.6T systems.

Conversely, the Asia Pacific market's volume growth is driven by the sheer scale of manufacturing and infrastructure projects. While APAC includes high-tech leaders like Japan, which focuses on precision industrial and medical fiber array applications, the majority of the volume demand stems from the mass production of transceivers in China and its surrounding supply chain. Manufacturers in this region prioritize efficiency and cost optimization. The ability to supply vast quantities of standard, highly reliable V-groove arrays used in FTTH and standard MPO products at competitive prices is key to capturing market share in this dominant growth territory. Strategic investment in high-throughput automation is essential for sustaining competitiveness in the APAC region.

The Fiber Arrays Market is highly consolidated, with a few key players dominating the high-precision, customized segment due to proprietary manufacturing techniques and long-standing supplier relationships with major transceivers OEMs. These market leaders, such as US Conec and Sanwa Components, maintain high barriers to entry by controlling critical patents related to V-groove fabrication, polishing techniques, and MPO connector interfaces. However, specialized smaller firms often thrive by focusing on niche, high-margin applications like aerospace, defense, or customized medical arrays, where unit volume is low but technical specification complexity is extremely high, requiring bespoke engineering solutions and specialized material sourcing. The competitive landscape is increasingly characterized by a race to automate the assembly process to reduce labor costs and improve yield, a necessary step for meeting the high-volume demands of the future optical communication market.

Technological integration remains the core differentiator. Beyond simple V-groove etching, leading companies are exploring novel materials, such as ceramic and polymer substrates, to offer alternative solutions that balance precision with cost-effectiveness and flexibility. Polymer waveguides, for instance, can be manufactured faster and cheaper than silicon, although they currently face challenges in meeting the thermal stability requirements of high-power or high-temperature environments. Furthermore, active alignment techniques, where laser light is used during the assembly process to optimize fiber position relative to the target component before permanent bonding, are increasingly being applied to achieve the absolute lowest coupling loss, particularly in ultra-high-performance R&D and specialized products, despite the higher initial cost associated with this process.

The need for faster product development cycles is also shaping the technological landscape. As optical standards evolve quickly (e.g., from 100G to 400G in rapid succession), fiber array suppliers must shorten their design-to-production time frames. This has led to the integration of advanced simulation tools (e.g., finite element analysis) into the design phase to predict thermal stress, mechanical performance, and optical loss before expensive prototyping begins. This commitment to front-loaded engineering and simulation capability helps suppliers quickly adapt their array designs to meet the evolving interface requirements of new generations of optical engines and transceivers, ensuring they remain relevant in the fast-paced optical communication ecosystem.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.