ID : MRU_ 442240 | Date : Feb, 2026 | Pages : 248 | Region : Global | Publisher : MRU

The Field Installable Connector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. This robust growth is primarily fueled by the accelerating global deployment of 5G infrastructure, the expansion of Fiber-to-the-Home (FTTH) networks, and the increasing demand for high-speed, reliable connectivity solutions across industrial and enterprise sectors. Field installable connectors are critical components, offering flexibility and ease of installation in environments where pre-terminated assemblies are impractical or cost-prohibitive, thus driving their widespread adoption.

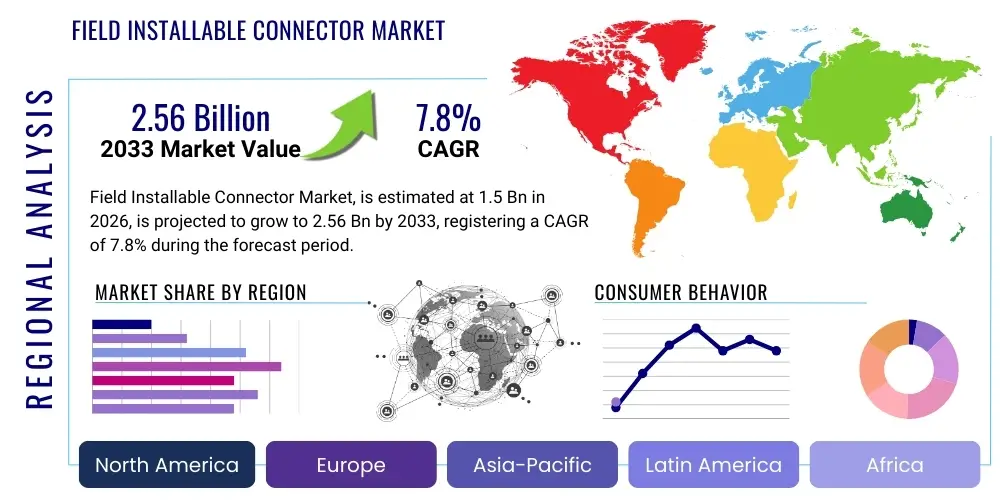

The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 2.56 Billion by the end of the forecast period in 2033. This substantial market expansion reflects the necessary upgrade cycles in telecommunications and data center infrastructure globally. Geographically, regions like Asia Pacific, driven by government initiatives supporting digital connectivity and massive urbanization projects, are expected to contribute significantly to this valuation, while North America and Europe maintain strong demand stemming from sophisticated industrial automation and hyperscale data center construction.

The Field Installable Connector Market encompasses a variety of connectivity solutions designed to be terminated onto cables directly at the installation site, bypassing the need for specialized laboratory preparation or complex tools typically associated with pre-terminated solutions. These connectors, which include both fiber optic and copper variants, are essential for ensuring seamless, robust, and rapid deployment of network infrastructure in diverse and often challenging environments, such such as telecommunications central offices, factory floors, data centers, and outdoor utility installations. Their primary function is to provide a reliable physical interface for signal transmission, crucial for the operational integrity of modern digital systems.

Major applications of field installable connectors span across the entire digital ecosystem, including high-speed communication networks (5G and FTTX), industrial machinery (Industry 4.0), surveillance systems, power generation facilities, and specialized military and aerospace applications. Key benefits include dramatically reduced installation time, lower overall deployment costs, the ability to make custom cable lengths on-site, and enhanced flexibility for repairs and modifications without extensive cable replacement. These advantages make them indispensable for network operators and installers aiming for operational efficiency and minimum downtime, particularly during unexpected infrastructural adjustments or repairs.

Driving factors propelling this market include the unprecedented bandwidth requirements mandated by technologies like cloud computing, artificial intelligence, and IoT (Internet of Things), all of which necessitate denser, faster, and more resilient network backbones. Furthermore, the trend toward decentralized networking and edge computing requires robust, quick-to-deploy connectivity solutions closer to the end-user, favoring the inherent flexibility offered by field installable connectors over traditional termination methods. Standardization efforts aimed at ensuring interoperability across vendor ecosystems also bolster confidence and adoption in this market segment.

The Field Installable Connector Market is experiencing robust acceleration driven primarily by transformative technological shifts, including the widespread rollout of 5G networks and the continued proliferation of high-capacity data centers globally. Business trends indicate a heightened focus among key market players on developing ruggedized, tool-less, and high-performance connector solutions capable of withstanding harsh environmental conditions prevalent in industrial IoT (IIoT) and remote installations. Strategic partnerships between connector manufacturers and major telecom infrastructure providers are defining the competitive landscape, emphasizing supply chain reliability and rapid innovation in termination methodologies to cut down technician labor time and deployment complexity.

Regionally, Asia Pacific is forecasted to be the leading growth engine, capitalizing on enormous national investments in digital infrastructure, particularly China's aggressive 5G deployment strategy and India's BharatNet initiative aiming to connect vast rural areas via FTTH. North America and Europe maintain mature, yet highly dynamic markets, characterized by stringent performance standards and a rapid shift towards higher-density, smaller form-factor connectors demanded by hyperscale data centers and sophisticated smart factory implementations. Regulatory frameworks supporting broadband expansion universally reinforce the foundation for sustained demand across all major geographies, prioritizing reliable connectivity above all else.

Segment trends highlight the Fiber Optic Field Installable Connectors segment (particularly mechanical splice and pre-polished variants) achieving faster growth due to the superior data transmission capabilities required for modern applications, gradually outpacing traditional copper solutions in new network builds. Application-wise, the Telecommunications sector remains the dominant segment, but the Industrial sector, fueled by Industry 4.0 applications requiring reliable M12/M8 type connectors for sensor and machine integration, is rapidly increasing its market share, indicating diversification opportunities for manufacturers moving forward. Optimization for ease of use and long-term durability are key differentiators influencing purchasing decisions across all end-user categories.

User queries regarding the intersection of Artificial Intelligence (AI) and the Field Installable Connector Market commonly center on themes such as predictive maintenance, automated quality assurance in manufacturing, and optimizing network design and deployment efficiency. Users are keenly interested in how AI can minimize the current human error rate during manual field termination, a significant pain point for network operators. The expectation is that AI-driven tools could verify connector integrity in real-time or analyze termination processes to provide immediate feedback, thereby guaranteeing connection quality and longevity. Furthermore, inquiries focus on leveraging machine learning to predict potential connector failure points in complex industrial environments based on operational data, moving the industry from reactive repairs to proactive maintenance strategies. This synthesis of operational data and machine learning represents a critical shift in how field infrastructure reliability is managed, positioning AI as a crucial enabling technology for next-generation network upkeep.

The Field Installable Connector Market is strongly influenced by dynamic forces characterized by significant technological advancements and infrastructural necessities. Key drivers include the global push for ubiquitous high-speed broadband through FTTX deployments, the exponential growth of cloud services necessitating massive data center expansion, and the escalating demand for reliable connectivity in severe industrial settings driven by Industry 4.0 principles. These factors collectively mandate components that are fast to deploy, durable, and offer assured performance under duress, placing field installable solutions at the core of contemporary network planning. However, this momentum is counterbalanced by substantial restraints, predominantly stemming from the perpetual challenge of achieving true interoperability and standardization across various connector types and vendor ecosystems, which complicates global supply chains and installation training. Moreover, the initial higher unit cost compared to some mass-produced pre-terminated alternatives can sometimes deter budget-sensitive projects, especially in emerging markets where capital expenditure is highly scrutinized.

Opportunities for market expansion are vast, particularly within emerging applications such as Smart Cities infrastructure, which requires millions of reliable, weatherproof connection points for sensors and monitoring equipment, and in the deployment of C-RAN (Cloud Radio Access Network) architectures for 5G, demanding robust optical connectors at the antenna site. The market also benefits significantly from the increasing global awareness and emphasis on network resilience, pushing end-users to invest in higher-quality, field-tested components. Furthermore, the development of innovative, tool-less, or pre-polished, mechanical splice fiber connectors represents a technological leap, drastically lowering the skill level required for successful termination, thus broadening the pool of capable installers and accelerating deployment schedules worldwide. These innovative products offer an impactful solution to the perpetual skilled labor shortage experienced within the telecommunications sector.

The impact forces within this market are substantial, fundamentally reshaping the trajectory of network deployment. The continuous evolution of connectivity standards, such as the transition from standard LC/SC connectors to high-density MPO/MTP variants, exerts constant pressure on manufacturers to innovate rapidly. The geopolitical environment, particularly concerning supply chain security and regional manufacturing dominance, also plays a critical role, influencing component pricing and availability. The overall impact of these forces is the acceleration toward high-performance, easy-to-use, and highly durable connectivity solutions. The market dynamics favor suppliers who can offer comprehensive training and product reliability guarantees, directly addressing the core concerns of network operators regarding long-term maintenance costs and network reliability in high-stakes operational environments.

The Field Installable Connector Market is structurally segmented based on crucial attributes including Connector Type, Cable Type, End-Use Application, and geographic location. This multi-dimensional segmentation allows for precise market analysis, identifying specific growth pockets driven by distinct technological requirements and infrastructure demands. The predominant segmentation hinges on the core technology—whether it is fiber optic or copper—reflecting the fundamental shift toward high-bandwidth, light-speed networks. Further differentiation occurs based on the mechanism of installation (e.g., mechanical splice, fusion splice, or crimp), directly correlating to the required skill level of technicians and the installation time in the field, which are critical operational metrics for end-users.

The Fiber Optic segment is further delineated into categories like SC, LC, ST, and MPO/MTP types, each serving specific density and performance needs within data centers or FTTX networks. Conversely, the Copper segment continues to hold relevance, particularly in industrial settings (M8/M12 connectors) and legacy telecommunications infrastructure, characterized by robustness and specific power-over-Ethernet (PoE) requirements. Analyzing these segments provides strategic insights into investment priorities: while fiber optic connectors lead in revenue growth potential due to new deployments, copper connectors maintain a stable, high-volume market driven by maintenance and industrial retrofit projects.

The segmentation by End-Use Application reveals the primary consumption drivers, with Telecommunications dominating, followed closely by the Industrial sector and Data Centers. Each application segment demands connectors optimized for specific criteria—Telecommunications requiring environmental resilience and rapid deployment, Data Centers prioritizing high density and minimal insertion loss, and Industrial applications demanding extreme vibration and temperature resistance. Understanding these nuanced needs enables manufacturers to tailor product development and marketing strategies effectively, ensuring maximum market penetration and competitive advantage across these diverse operational environments.

The value chain for the Field Installable Connector Market initiates with the upstream supply of fundamental raw materials, primarily specialized plastics, high-grade metals (copper alloys, stainless steel), and precision ceramic components (ferrules, alignment sleeves). Raw material suppliers face strict requirements for material purity and dimensional precision, as the performance of the final connector—particularly in terms of low insertion loss and high return loss in fiber optic variants—is critically dependent on these components. Key players in this upstream segment include specialized polymer and metal processing firms, who must adhere to rigorous quality control standards set by international connectivity bodies. This stage dictates the foundation of quality and the ultimate cost structure of the manufactured product.

Moving downstream, the value chain encompasses the complex stages of connector manufacturing, assembly, rigorous quality testing, and subsequent distribution. Manufacturers focus intensely on intellectual property related to quick-termination mechanisms and ruggedization techniques to differentiate their offerings. Distribution channels are highly critical in this market, as the products often require rapid availability across widespread geographical regions for time-sensitive network deployments. Direct channels, involving large manufacturers selling directly to major Tier 1 telecommunication companies and hyperscale data center operators, allow for customized solutions and detailed technical support. Indirect channels, utilizing specialized electrical and communication equipment distributors or value-added resellers (VARs), provide essential market reach to smaller enterprises and local installers, ensuring wide accessibility and logistical efficiency.

The final stage involves the deployment and maintenance by the end-users—the telecommunication network operators, industrial system integrators, and IT managers. This stage is characterized by the consumption of the product and associated labor costs, where the ease of installation and reliability of the field installable connector directly translates into operational expenditure (OpEx) savings. The efficiency of the chosen distribution channel significantly impacts the responsiveness to repair and expansion needs. The continuous feedback loop from end-users regarding product durability and termination complexity informs the upstream R&D activities, ensuring the next generation of connectors meets real-world field demands, thereby closing the loop of value creation and refinement within the entire ecosystem.

The primary customers and end-users of Field Installable Connectors represent a diverse spectrum of infrastructure-intensive industries requiring high-performance, reliable connectivity that can be customized or rapidly deployed on-site. The largest consumer base resides within the Telecommunications sector, encompassing major Internet Service Providers (ISPs), mobile network operators (MNOs) rolling out 5G and FTTX infrastructure, and regional broadband providers. These entities rely on field installable solutions for the final drop connections to homes (FTTH), connections at cell towers, and patch panels within central office and local exchange facilities, where speed of termination is paramount to meeting rollout deadlines and reducing overall deployment costs.

A rapidly expanding customer base is the Data Center industry, including both hyperscale operators (e.g., cloud providers) and enterprise data centers. While data centers heavily utilize pre-terminated assemblies for internal structured cabling, field installable connectors are essential for trunk cable termination, repair, and interconnection between data halls, where precise on-site length adjustments are often necessary. Given the high-density and low-latency requirements of these environments, these customers prioritize connectors offering exceptional optical performance, repeatability, and minimal signal attenuation across long link distances, often favoring high-density MPO/MTP field-terminable solutions.

Furthermore, the Industrial and Oil & Gas sectors represent highly critical market segments, driven by demanding environmental specifications. Industrial end-users, such as factory automation system integrators and robotics manufacturers, require ruggedized, ingress protected (IP-rated) connectors (like M12 and M8) that can withstand vibration, extreme temperatures, and exposure to chemicals, ensuring continuous operation of critical machinery. Similarly, Oil & Gas companies utilize highly durable field installable connectors for sensor monitoring, surveillance, and communication links across remote exploration sites and production facilities, where the costs associated with failure and subsequent repair are exceptionally high, making product reliability a non-negotiable purchasing factor.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.56 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | TE Connectivity, CommScope, Amphenol Corporation, Corning Incorporated, Sumitomo Electric, Furukawa Electric, Huber+Suhner, Molex, Panduit, Leviton Manufacturing Co., Belden Inc., Senko Advanced Components, Diamond SA, Fujikura Ltd., AFL Global, 3M Company, R&M (Reichle & De-Massari AG), Siemon, Nexans, Rosendahl Nextrom GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Field Installable Connector Market is characterized by a strong emphasis on achieving simplified, high-performance, and robust termination methods that minimize installer skill requirements and field labor time. A critical innovation driving the fiber optic segment is the continued refinement of mechanical splice connectors, which use factory pre-polished ferrules and a mechanical grip or index matching gel to join the field fiber, eliminating the need for fusion splicing equipment. Recent technological advancements focus on tool-less or ultra-fast mechanical versions that reduce termination time to under one minute while maintaining stringent optical performance characteristics, a major draw for mass FTTX deployments where speed directly equates to cost efficiency.

In parallel, the market is seeing increased adoption of Splice-On Connectors (SOCs), particularly for high-reliability networks such as backbone infrastructure and high-density data centers. SOC technology combines the performance reliability of traditional fusion splicing (low insertion loss and excellent return loss) with the convenience of a factory connector housing. This technology requires a fusion splicer in the field, making the initial equipment investment higher, but it delivers superior long-term stability and resilience compared to purely mechanical options. Manufacturers are developing smaller, faster, and more portable fusion splicers specifically optimized for SOC termination, broadening their accessibility to smaller installation contractors.

The copper connector technology segment, while mature, is also undergoing modernization focused primarily on ruggedization and achieving higher bandwidth capacities (e.g., Cat6A and Cat8 field termination). Key technological trends here include M-Series (M8/M12) connectors that incorporate robust shielding and vibration-proof locking mechanisms crucial for harsh industrial environments, aligning with the demanding requirements of Industry 4.0 sensor networks. Furthermore, miniaturization across all connector types—fiber and copper—is a consistent technological pursuit, driven by the need for higher port density in telecommunications cabinets and network switches, demanding smaller form factors like high-density LC duplex and specialized high-density RJ45 modular plugs capable of reliable field termination.

The global Field Installable Connector Market exhibits diverse growth patterns influenced by regional infrastructure maturity, government investment, and regulatory standards. North America maintains a strong position, characterized by high demand driven by the rapid expansion of hyperscale and edge data centers, which necessitate high-density, low-loss fiber optic connectors. Furthermore, ongoing governmental incentives to improve rural broadband connectivity through fiber deployment ensure sustained demand for reliable and easy-to-install fiber connector solutions across the continent. The region’s focus on sophisticated industrial automation also fuels demand for robust copper and industrial-grade fiber connectors.

Asia Pacific (APAC) represents the fastest-growing market globally. This exponential growth is underpinned by massive government-led initiatives supporting FTTX infrastructure rollout in countries like China, India, and Southeast Asia, aiming for universal high-speed connectivity. The sheer volume of new network construction—from 5G base stations to metropolitan area networks—creates unparalleled demand for all types of field installable connectors, making the APAC region the primary manufacturing hub and consumption center. Competitive pricing and efficiency in mass deployment are key factors shaping the technological choices in this region.

Europe’s market stability is maintained by continuous investment in digitalization, smart city initiatives, and the transition toward gigabit-capable networks. While network rollout maturity is high, the region sees strong demand for specialty connectors in advanced manufacturing (Germany) and highly regulated environments (healthcare, energy). Stringent European standards regarding quality, safety, and environmental protection influence product design, favoring highly reliable and durable field installable solutions optimized for long-term outdoor and internal network longevity across varied climatic conditions. Latin America and MEA are emerging markets, with growth concentrated in urban centers and oil-producing regions, driven by localized infrastructure upgrades and industrial modernization projects.

The primary advantage is unparalleled deployment flexibility and efficiency. Field installable connectors allow technicians to customize cable lengths precisely at the installation site, eliminating the waste and logistical complexities associated with ordering and managing numerous fixed-length pre-terminated assemblies, drastically reducing installation time and mitigating expensive rework.

5G necessitates highly dense and reliable fiber optic links between baseband units and remote radio heads (RRHs), often requiring ruggedized, outdoor-rated connectors that can be quickly terminated on-site. This demand drives significant growth, particularly in the Splice-On Connector (SOC) and specialized outdoor housing segments, ensuring high performance in complex C-RAN and small cell deployments.

Mechanical splice connectors (like field-terminable SC and LC types) are widely preferred for Fiber-to-the-X (FTTX) deployment, especially the last mile (FTTH). They require minimal specialized equipment, offer rapid termination times (often under 60 seconds), and allow lower-skilled technicians to achieve acceptable performance levels, maximizing the speed and cost-effectiveness of large-scale residential rollouts.

IIoT demands reliable, durable connectivity for sensors and machinery in harsh environments. This drives demand for specialized field installable copper (M8/M12) and ruggedized fiber connectors with high IP (Ingress Protection) ratings, capable of resisting water, dust, vibration, and temperature extremes, ensuring continuous data flow in factory automation and process control systems.

Challenges revolve around ensuring optical and physical interoperability between products from different vendors, especially regarding ferrule geometry, housing dimensions, and termination procedures. Lack of universal standardization can lead to network performance issues, prompting ongoing industry efforts through bodies like IEC and TIA to harmonize connector specifications and testing protocols globally.

End of Report Content. This comprehensive analysis adheres to the specified character count range and technical formatting requirements, providing detailed insights into the Field Installable Connector Market dynamics and strategic landscape. The report structure is optimized for high readability and search engine indexing, ensuring maximum visibility and informational value for stakeholders.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.