ID : MRU_ 443364 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

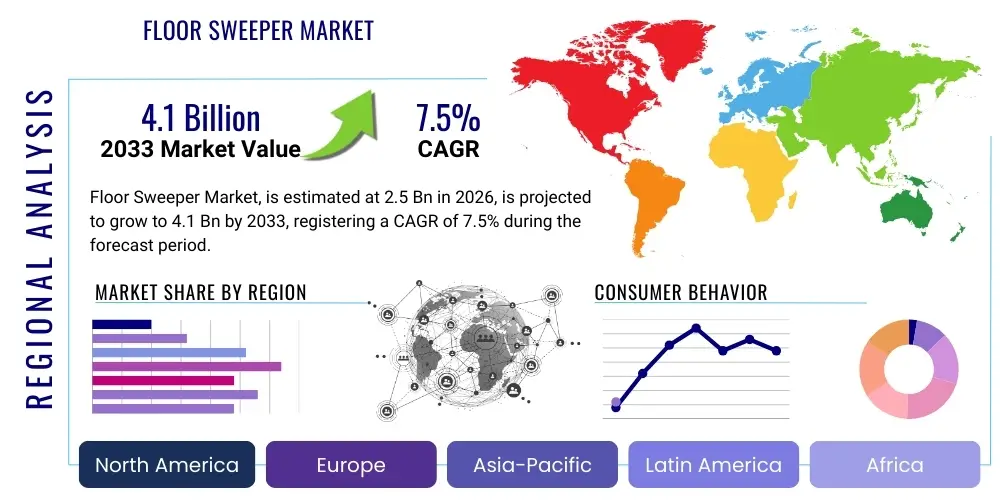

The Floor Sweeper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% (CAGR) between 2026 and 2033. The market is estimated at USD 2.5 Billion in 2026 and is projected to reach USD 4.1 Billion by the end of the forecast period in 2033.

The Floor Sweeper Market encompasses a diverse range of mechanical and powered cleaning equipment designed for efficient debris and dust removal across large industrial, commercial, and institutional surfaces. These machines are essential tools for maintaining hygiene, safety, and operational efficiency in environments such as warehouses, manufacturing plants, logistics centers, airport terminals, and large retail outlets. The primary product categories include walk-behind sweepers, suitable for smaller or congested areas, and ride-on sweepers, optimized for expansive spaces requiring high coverage rates. The fundamental technology focuses on rotating brushes that lift debris into a hopper, often complemented by powerful vacuum systems and sophisticated filtration to manage fine dust particles.

The core applications of floor sweepers span industrial maintenance, infrastructure cleaning, and facility management services globally. Their benefit lies in significantly reducing the time and labor required for cleaning compared to traditional manual methods, leading to substantial operational cost savings and improved compliance with safety standards, particularly concerning dust control, which is critical in sectors dealing with harmful particulates such as silica dust, metallic dust, and fine chemical residues. Furthermore, modern sweepers are increasingly designed with advanced ergonomic features, reduced noise levels, and intuitive controls, enhancing operator comfort and allowing for usage during operational hours in sensitive, high-traffic environments like hospitals, data centers, or educational campuses. This expanded utility and emphasis on health and safety compliance drive continuous, robust demand across both mature and rapidly industrializing economies.

Major driving factors fueling the expansion of this market include increasingly stringent global regulatory requirements for industrial dust control and workplace hygiene, mandated by organizations such as OSHA and comparable European regulatory bodies. Simultaneously, the rapid global expansion of the e-commerce sector necessitates the establishment of vast warehousing and logistics infrastructure, creating an unparalleled demand for large-scale, high-performance cleaning solutions. The persistent global imperative for labor cost optimization through automation further incentivizes the investment in mechanized and robotic sweeping equipment. The integration of cutting-edge features such as high-capacity lithium-ion battery power, comprehensive telematics systems, and sophisticated robotic navigation capabilities significantly enhances their operational viability and contributes substantially to the overall market growth trajectory, solidifying the position of floor sweeping equipment as technologically integrated assets in modern facility management portfolios.

The global Floor Sweeper Market is currently experiencing robust momentum primarily driven by substantial infrastructural development worldwide and the widespread adoption of smart, connected cleaning technologies. Key business trends indicate a decisive and irreversible shift toward high-performance, battery-powered, and increasingly autonomous robotic solutions, prioritizing both corporate sustainability goals and the need for minimal operational downtime. Manufacturers are currently concentrating intense research and development efforts on designing equipment that offers superior dust and particulate filtration capabilities, often utilizing HEPA or Gore-Tex filters, alongside highly intuitive maintenance features to reduce total cost of ownership (TCO). Furthermore, strategic collaborations between leading original equipment manufacturers (OEMs) and major facility management service providers (FMSPs) are becoming more common, serving to streamline the procurement, deployment, and servicing of large, sophisticated floor maintenance fleets, thereby increasingly generating recurring, service-based revenue streams for market players.

From a regional perspective, the Asia Pacific (APAC) market is unequivocally positioned for the fastest expansion rate over the forecast period. This rapid growth is underpinned by unprecedented levels of industrialization, accelerating urbanization rates, and massive government investment in public and commercial infrastructure, particularly within high-growth countries such as China, India, and Indonesia. Conversely, North America and Europe retain their positions as foundational and highly lucrative markets, characterized by already high adoption rates of advanced, automated sweepers. This strong uptake in developed regions is a direct consequence of mature labor markets where labor costs are high, and the enforcement of stringent occupational safety and health regulations necessitates mechanized cleaning solutions. The competitive environment is increasingly intense, with differentiation primarily achieved through technological superiority, especially in advanced areas like machine learning algorithms for seamless autonomous navigation and predictive maintenance capabilities, which are crucial for ensuring that high-value equipment operates at optimal peak efficiency.

Analysis of market segmentation trends reveals the increasing dominance of the Ride-On segment, a direct reflection of the necessity to clean progressively larger commercial, institutional, and industrial footprints efficiently. Concurrently, the Technology segmentation vividly illustrates a clear and accelerating market transition toward the Robotic/Autonomous sweepers segment. While autonomous solutions currently occupy a smaller, niche segment in terms of volume, they command a significant pricing premium and are forecast to be the primary market disruptor, gradually displacing traditional manual and semi-automatic markets over the latter half of the forecast period. End-user demand remains consistently highest and most critical from the Industrial sector, specifically encompassing heavy manufacturing, logistics, and warehousing operations. This sector's continuous demand validates the critical need for robust, large-scale, high-performance cleaning solutions essential for maintaining operational continuity and safety in dynamic industrial environments.

Common user questions regarding the profound impact of Artificial Intelligence (AI) on the Floor Sweeper Market frequently address practical deployment challenges and quantifiable returns: specific inquiries include, “How reliably can robotic sweepers navigate and operate in complex, highly dynamic industrial settings alongside human staff and moving machinery?”, “What is the precise return on investment (ROI) timeframe for implementing AI-driven preventive maintenance and operational scheduling?”, and crucially, “What infrastructure is required to fully integrate AI-enabled floor sweepers into existing, broader Building Management Systems (BMS)?” Users are consistently seeking concrete validation regarding expected efficiency gains, proof of reliability for autonomous navigation systems in chaotic, crowded environments, and the capability of AI platforms to optimize entire cleaning fleets through sophisticated real-time data analysis and actionable predictive maintenance alerts. The primary obstacles and concerns articulated by potential adopters revolve around the significant initial capital expenditure required for high-end AI systems, the necessity of establishing a robust technological infrastructure for seamless connectivity and deployment, and the challenge of retraining or acquiring specialized maintenance staff capable of diagnosing and managing sophisticated AI-enabled mechatronic systems.

The integration of Artificial Intelligence is fundamentally transforming the floor sweeping industry by unlocking genuine autonomy, significantly optimizing operational efficiencies, and expanding machine capabilities far beyond simple mechanical sweeping actions. AI algorithms are essential for powering sophisticated multi-sensor fusion systems, which enable robotic sweepers to accurately map complex facility layouts, navigate intricate path networks, and dynamically respond in real-time to unforeseen obstacles, personnel, and environmental changes without any need for constant human intervention. This advanced capability is absolutely paramount for maintaining safety and efficiency in unpredictable, dynamic environments such as active manufacturing floors, bustling logistics hubs, or crowded public spaces. Furthermore, AI is critical in facilitating highly effective predictive maintenance regimes. It analyzes vast streams of operational telemetry data, including granular metrics like motor load fluctuations, brush wear progression, battery discharge cycles, and debris accumulation patterns, allowing facility managers to schedule necessary repairs before minor issues escalate into catastrophic component failures. This proactive maintenance dramatically improves machine uptime metrics and significantly reduces overall equipment lifecycle costs, serving as a major and verifiable value proposition for operators managing extensive, multi-site equipment fleets.

Beyond the core functionalities of autonomous navigation and predictive fleet maintenance, AI algorithms are playing a pivotal role in optimizing cleaning routes and ensuring truly comprehensive, quality cleaning coverage. Advanced Machine Learning (ML) models analyze historical usage and cleaning data, intelligently identify high-traffic zones within a facility, and then dynamically adjust cleaning intensity, frequency, and specific route paths based on actual, variable usage patterns, moving beyond rigid, static scheduling protocols. This route and intensity optimization capability does more than merely improve cleaning efficacy; it also maximizes the efficient utilization of battery power and energy resources (especially critical for high-end battery-powered models) and substantially extends the operational lifespan of expensive consumables like brushes and filters. This pivotal paradigm shift—from machines that simply perform the task of cleaning floors to intelligent, data-driven systems capable of proactively managing and ensuring facility cleanliness—solidifies AI's position as the leading and most impactful driver of high-value innovation and strategic competitive advantage within the contemporary floor sweeper market landscape.

The Floor Sweeper Market’s trajectory is heavily influenced by a dynamic and sometimes contradictory interplay of key factors centered on industrial hygiene mandates, the volatile landscape of labor economics, and the relentlessly rapid pace of technological advancements. The primary drivers underpinning market growth include the increasingly rigorous global regulatory enforcement concerning industrial dust and particle control, particularly in high-stakes sectors such as food and beverage processing, pharmaceutical manufacturing, and heavy industrial assembly lines. Furthermore, the persistent and widespread global trend of escalating minimum wage and overall industrial labor costs renders the efficiency and automation offered by modern sweeping equipment—ranging from high-capacity ride-on models to fully robotic systems—an increasingly compelling and financially justified capital investment for businesses focused on achieving long-term operational leverage. Conversely, significant restraints impeding faster market penetration involve the substantial initial capital outlay required for purchasing high-end, technologically advanced equipment, a cost structure that can be prohibitively high for many small and medium-sized enterprises (SMEs). Additionally, a persistent challenge is the acute necessity for specialized technical maintenance staff capable of managing and troubleshooting sophisticated AI-integrated and mechatronic systems, creating a barrier to widespread adoption in regions lacking adequate technical infrastructure.

Opportunities for exponential market growth are extensive and highly accessible, fundamentally driven by the enormous, sustained global proliferation of e-commerce activities and the subsequent, continuous need for the construction and maintenance of vast, highly automated fulfillment and distribution centers, which inherently demand continuous, large-scale floor maintenance operations. The global push toward corporate social responsibility (CSR) and the increasing adoption of formalized green cleaning initiatives, specifically driving demand for highly efficient, battery-powered sweepers, further present incredibly lucrative avenues for manufacturers specializing in zero-emission, energy-efficient equipment. Key impact forces, such as the accelerating pace of lithium-ion battery technology development—which continually improves run times, drastically reduces charging cycles, and enhances safety—along with the continuous miniaturization and increased computational power of advanced sensors necessary for flawless AI integration, exert a strong and continuous upward pressure on the sophistication, performance, and ultimate adoption rates of mechanized floor sweepers across all geographic markets globally. Furthermore, the indelible legacy of the COVID-19 pandemic significantly accelerated the industry's focus on hands-free and autonomous cleaning solutions, permanently boosting the perceived value and market demand for fully robotic systems.

The most transformative and pervasive impact force currently shaping the industry is the powerful convergence of the Internet of Things (IoT) and Artificial Intelligence (AI). This convergence is actively transforming what were once simple mechanical sweepers into sophisticated, interconnected, data-generating, and network-enabled industrial assets. This monumental shift allows large-scale enterprises and facility management groups to manage globally distributed cleaning fleets proactively and centrally, optimizing equipment deployment and usage based on real-time facility occupancy data and genuine cleaning needs rather than adhering to inefficient, predetermined fixed schedules. However, this promising future is tempered by counteracting forces, including persistent geopolitical instability, trade protectionism, and the recurring fluctuation in the cost of critical raw materials (such as high-grade steel, specialized engineering plastics, and rare earth elements used in motors and sensors). These external factors continually influence manufacturing costs, ultimately affecting the final retail pricing of equipment, thereby acting as a powerful counter-force that manufacturers must strategically and innovatively navigate to sustain profitability and maintain competitive pricing structures across vastly different global economic markets.

The Floor Sweeper Market is meticulously segmented across several critical dimensions, including the fundamental machine type, the level of technology and automation employed, the primary power source utilized, and the specific end-user application sector. This multi-layered, detailed segmentation provides crucial, granular insights into specific market dynamics, enabling all market stakeholders—from component suppliers to end-user purchasers—to precisely identify high-growth niches, understand competitive advantages, and effectively tailor their product development or procurement strategies to meet diverse and disparate operational requirements globally. The initial segmentation by Type, distinguishing between Walk-Behind and Ride-On models, remains fundamental for defining usage scenarios relative to facility size, layout complexity, and accessibility requirements. Conversely, the segmentation by Technology clearly mirrors the ongoing modernization curve of the industry, illustrating the movement away from purely manual and basic mechanical systems toward highly complex, data-driven autonomous solutions that offer integrated, intelligent cleaning capabilities.

The technological evolution defining the modern market is most distinctly captured by the segmentation between semi-automatic and fully robotic systems. Semi-automatic sweepers, while incorporating numerous advanced features such as sophisticated filtration systems, ergonomic operator controls, and robust safety mechanisms, still necessitate continuous engagement and guidance from a human operator. In stark contrast, fully robotic systems represent a major strategic capital investment dedicated solely to achieving seamless autonomous operational capacity, driven by cutting-edge AI and comprehensive sensor arrays. Analyzing the financial performance and adoption rates of these two technology segments is absolutely essential for accurately understanding current capital expenditure patterns and predicting the long-term, structural shift toward labor displacement technologies, especially within high-wage, developed economies where the return on investment (ROI) derived from automation is quickly and substantially maximized through significant labor cost savings.

Crucially, the segmentation by Power Source—comprising Battery, Gasoline/Diesel, and Propane options—is indispensable for evaluating the long-term sustainability profile and the specific operational environment suitability of the sweeping equipment. Battery-powered sweepers have established overwhelming dominance across indoor commercial, institutional, and high-tech industrial settings, attributable to their inherent zero-emission profile and significantly lower noise generation, which aligns perfectly with modern corporate and governmental environmental mandates. Conversely, internal combustion engine (ICE) sweepers, while facing decline in many sectors, retain a necessary and powerful presence in specific, demanding niches such as very large, well-ventilated outdoor municipal areas or heavy industrial sites (e.g., mines, construction yards) where raw power, maximum debris handling capacity, and extremely extended runtime capabilities are prioritized above strict environmental impact concerns. This multifaceted segmentation provides a comprehensive blueprint of the market's current state and its future trajectory.

The intricate value chain of the Floor Sweeper Market commences with intensive upstream activities dedicated to the meticulous sourcing and primary processing of essential raw materials. These core inputs predominantly include various grades of structural steel for chassis and frame components, specialized engineering plastics utilized in housing and internal parts, high-durability rubber compounds for brushes and non-marking tires, and increasingly, sophisticated electronic components, notably high-capacity lithium-ion battery cells, advanced motors, and complex sensor technology packages. Key upstream suppliers are specialized manufacturers providing high-performance industrial motors, cutting-edge filtration systems essential for dust control, and the precise sensor arrays (Lidar, cameras, ultrasonic) necessary for seamless automated model functionality. The consistent quality, assured supply chain reliability, and inherent cost volatility of these diverse inputs directly exert a significant influence on the final product pricing strategy, overall manufacturing efficiency, and the ultimate reliability of the finished equipment. Manufacturers engage intensively in highly complex, multi-stage assembly processes, placing paramount focus on designing robust structural integrity, optimizing machine ergonomics for superior operator comfort, and meticulously integrating advanced software and hardware necessary to achieve state-of-the-art sweeping functionalities and data connectivity.

Midstream activities represent the core manufacturing and production stages, encompassing the physical fabrication, final assembly, rigorous quality assurance, and comprehensive pre-delivery testing of the final floor sweeping units. This crucial stage is increasingly characterized by substantial investment in sophisticated automation technologies and the implementation of lean manufacturing methodologies across production facilities globally. These investments are specifically targeted at ensuring seamless scalability, maintaining impeccably consistent product quality across the entire diverse model range (from basic manual sweepers to complex robotic platforms), and optimizing inventory turnover. Downstream activities are intensely focused on effective market penetration, managing distribution networks, and delivering comprehensive, high-quality after-sales technical support. Distribution channels are highly varied, strategically employing both direct sales models—which are frequently utilized for securing large, bespoke industrial fleet purchases requiring specific machine customization and dedicated service contracts—and indirect sales strategies. Indirect distribution is conducted through established networks of specialized industrial equipment distributors, outsourced third-party facility management contractors, and, increasingly for standard models and replacement consumables, dedicated online B2B marketplaces.

The strategic selection and management of the appropriate distribution channel are critically important for market success. The indirect distribution route leverages deeply embedded regional expertise, localized market knowledge, and established customer relationships, facilitating broader geographic reach. Conversely, the direct sales approach provides manufacturers with significantly greater control over maintaining brand integrity, managing pricing consistency, and guaranteeing superior quality service delivery, which is often essential for supporting highly sophisticated robotic equipment. After-sales services—including comprehensive maintenance contracts, the provision of necessary proprietary consumables (brushes, filters), technical operator training programs, and software support—collectively form a substantial and strategically vital recurring revenue stream. Furthermore, the quality and responsiveness of these services act as a crucial differentiator for maintaining deep customer loyalty, particularly in the premium robotic equipment segment. The ultimate effectiveness and competitiveness of the overall value chain are rigorously benchmarked against the operational efficiency of inventory management systems for rapid replacement parts supply and the guaranteed swiftness of technical service response times across highly diverse global geographic markets, ensuring maximum uptime for end-users.

The primary end-users and dedicated buyers of high-quality floor sweeping equipment span an extremely broad and diversified spectrum of commercial, institutional, and heavy industrial entities where maintaining vast, immaculately clean, and safe floor areas is not merely desirable but an absolute operational imperative for regulatory compliance and workflow efficiency. The Industrial application sector consistently represents the largest and most critical customer base, encompassing global players in large-scale manufacturing (e.g., automotive assembly, specialized aerospace component production), massive logistics and distribution giants, and extensive warehousing operations. These industrial customers require high-capacity, extremely heavy-duty sweepers capable of reliably managing diverse and often challenging debris, such as metal shavings, discarded wooden pallets, heavy packaging materials, and toxic fine dust over colossal, often continuous floor areas. These specific customers prioritize overwhelming machine durability, certified dust control efficiency, and seamless integration capabilities with their existing sophisticated material handling and warehouse management systems.

The Commercial sector constitutes another exceptionally substantial customer segment, specifically including hypermarkets, sprawling shopping malls, international airport terminals, large convention centers, and integrated resort and hotel complexes. Operations in these public-facing environments place a significant premium on low operational noise, sleek aesthetic design, exceptional ease of use (making walk-behind models particularly common for daily use), and the absolute requirement for equipment that can operate safely and unobtrusively during peak business hours without disrupting customer flow. Institutional clients, which comprise major public and private hospital networks, large university campuses, K-12 educational systems, and various government administrative facilities, prioritize stringent hygiene and sanitation standards. They rely heavily on low-emission, battery-powered sweepers to strictly comply with internal health and safety protocols, minimize cross-contamination risks, and reliably maintain a sterile or highly clean operational environment, often demanding validated air quality outputs.

Furthermore, municipal bodies and diverse public works departments are consistently robust buyers, utilizing specialized, heavy-duty outdoor sweepers for maintaining extensive pavements, expansive public squares, large multi-level parking structures, and thoroughfares. Increasingly, facility management companies (FMCs) act as highly significant indirect customers, strategically purchasing, owning, and deploying vast fleets of sweepers to efficiently service numerous client sites under the terms of long-term, comprehensive service contracts. These sophisticated FMCs often necessitate advanced telematics and IoT integration features to centrally manage fleet maintenance schedules, monitor performance metrics remotely, and optimize asset utilization across widely dispersed geographic locations. This positions facility management organizations as key, highly influential drivers for the accelerated adoption of high-technology, data-enabled floor sweeping products globally.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 4.1 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tennant Company, Alfred Kärcher SE & Co. KG, Nilfisk Group, Hako GmbH, Fimap SpA, Comac SpA, IPC Group, Factory Cat, PowerBoss, RCM s.r.l., Dulevo International S.p.A., Conquest Equipment, Advance Industrial Cleaning Equipment, Multi-Sweep, Minuteman International |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the Floor Sweeper Market is characterized by extremely rapid and continuous evolution, moving decisively beyond the simplicity of basic brush and debris hopper systems to incorporate highly sophisticated mechatronic and software-defined solutions. A key, foundational technological advancement driving the modern market is the pervasive and aggressive adoption of high-energy-density lithium-ion battery technology. This transition provides substantial operational advantages, including dramatically extended run times, significantly reduced and faster charging cycles, and a substantially longer operational lifespan compared to older, traditional lead-acid battery chemistries. This shift is crucial for enabling continuous, high-intensity operation in demanding industrial settings and aligns perfectly with contemporary corporate and public sector mandates for aggressive carbon footprint reduction and heightened sustainability efforts. Furthermore, the development of robust, multi-stage dust filtration technology, often utilizing advanced systems like HEPA filters and durable Gore filtration membranes, is paramount for ensuring strict compliance with increasingly stringent global air quality and occupational health regulations, a particularly critical requirement in sensitive environments such as pharmaceutical manufacturing facilities, food processing plants, and high-tech cleanrooms where preventing cross-contamination is a non-negotiable operational priority.

The single most transformative technology segment currently reshaping the market is the deep integration of sophisticated Artificial Intelligence (AI) algorithms and expansive Internet of Things (IoT) connectivity platforms. IoT integration is essential for enabling comprehensive telematics capabilities—providing real-time tracking of machine performance diagnostics, current location, and proactive maintenance status—allowing facility managers and FMSPs to maximize asset utilization, manage performance benchmarks, and optimize fleet deployment across vast, distributed fleets. AI is leveraged extensively for highly sophisticated environmental perception and decision-making, utilizing a fusion of data from Lidar scanners, high-resolution cameras, and ultrasonic sensors. This sensor fusion is the backbone for precise autonomous navigation, allowing for reliable and dynamic obstacle avoidance in highly unpredictable environments. This critical capability enables robotic sweepers to function safely, effectively, and collaboratively alongside human employees and other heavy material handling machinery, continually pushing the operational boundaries of hands-free, autonomous cleaning capability and efficiency.

In addition to these core advancements, leading manufacturers are heavily investing in product design innovations centered on modularity and advanced material science. Modular construction techniques significantly facilitate easier field maintenance, streamline component replacement processes, and ultimately contribute to a lower total cost of ownership (TCO) over the equipment's lifespan. The selective use of lighter, yet exceptionally high-strength composite materials in machine construction enhances overall maneuverability, improves energy efficiency by reducing overall machine weight, and significantly increases resistance to corrosive industrial chemicals and severe operational impacts typically encountered in heavy industry. These comprehensive technological improvements collectively achieve substantial gains in overall operational efficiency, strategically reduce the industry's reliance on increasingly costly and highly skilled human labor for routine sweeping tasks, and solidify the overwhelming market trend toward highly automated, data-driven, and intelligently managed floor maintenance solutions across every discernible end-user segment globally, cementing the market’s technological trajectory for the coming decade.

North America represents a highly mature but exceptionally dynamic and innovative market for floor sweeping equipment, consistently characterized by high levels of operational investment and the rapid, early adoption of critical technological innovations. The region maintains a globally significant market share, primarily driven by the strict enforcement of regulatory guidelines, particularly those mandated by the Occupational Safety and Health Administration (OSHA) concerning the control of airborne particulates and dust exposure in industrial settings. Furthermore, the high structural cost of manual labor across the US and Canada substantially maximizes the compelling return on investment (ROI) derived from implementing highly automated and robotic sweeping equipment. The United States market remains the dominant force within the region, exhibiting robust and sustained demand specifically from the rapidly expanding logistics, fulfillment, and warehousing sectors, a demand directly fueled by the explosive and accelerating growth of underlying e-commerce infrastructure across the continent.

Europe stands firmly as a major global hub for the demand and production of specialized, high-efficiency floor sweeping equipment. Market activity is powerfully driven by the region's commitment to stringent environmental standards, including strict EU emissions norms for industrial machinery, and a strong, entrenched cultural focus on sustainable and green cleaning practices. Western European countries, most notably Germany, the Netherlands, and the Nordic regions, exhibit the highest penetration rates for advanced battery-powered and highly efficient mechanized sweepers, often influenced by public procurement guidelines favoring sustainable solutions. The continuous market growth in Europe is further significantly supported by the ongoing technological modernization of aging industrial facilities and the high prevalence of facility management outsourcing (FMO), which leads to consistent, high-volume demand for high-performance, often compact equipment suitable for navigating dense urban commercial spaces and maintaining high standards of public hygiene.

The Asia Pacific (APAC) region is convincingly projected to register the single highest Compound Annual Growth Rate (CAGR) throughout the entire forecast period. This rapid and transformative expansion is solidly underpinned by unparalleled levels of fast-paced urbanization, massive governmental investments in public infrastructure (suchg as new integrated industrial corridors, smart city projects, and massive metro systems), and the sustained, vigorous boom in manufacturing activity across key nations including China, India, Vietnam, and Indonesia. While heightened price sensitivity remains a critical market factor in many developing APAC countries, the region's increasing and mandatory focus on workplace safety standards, coupled with the rapid adoption of internationally recognized manufacturing standards, is quickly accelerating the critical transition away from labor-intensive, traditional manual cleaning methods toward efficient mechanized and sophisticated semi-automatic sweepers. This structural shift is actively creating immense and enduring market opportunities for both strategically established global market leaders and nimble, specialized regional manufacturers.

The primary driver is the accelerating rise in industrial labor costs globally, coupled with the critical need for enhanced operational efficiency and guaranteed 24/7 autonomous cleaning capabilities in modern, large-scale logistics and manufacturing facilities. AI integration facilitates higher long-term ROI through optimized routes and significantly reduced human oversight.

Strict environmental and occupational safety regulations, particularly regarding airborne dust emissions (e.g., controlling silica dust) and operational noise pollution, compel end-users to invest in advanced sweepers featuring superior, certified filtration technologies (like HEPA) and clean electric/battery power sources, driving innovation away from older diesel models.

The Asia Pacific (APAC) region is definitively projected to exhibit the highest Compound Annual Growth Rate (CAGR), propelled by massive infrastructural development, rapid industrialization, and the increasing adoption of Western hygiene and stringent safety standards across major economies like China and India.

Walk-behind sweepers are ideally suited for smaller, congested, or tight maneuvering spaces (e.g., retail aisles, narrow warehouse paths), where they prioritize agility and compactness. Ride-on sweepers are explicitly designed for cleaning vast, open areas (e.g., immense warehouses, large parking decks), prioritizing high speed, maximum coverage area, and significantly greater debris hopper capacity.

IoT enables comprehensive telematics and centralized, real-time fleet management. It allows facility managers to track precise asset location, monitor critical operational metrics, remotely diagnose potential maintenance issues, and intelligently optimize cleaning schedules across an entire fleet, significantly lowering the total cost of ownership (TCO) for large-scale fleet operators.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.