ID : MRU_ 442695 | Date : Feb, 2026 | Pages : 257 | Region : Global | Publisher : MRU

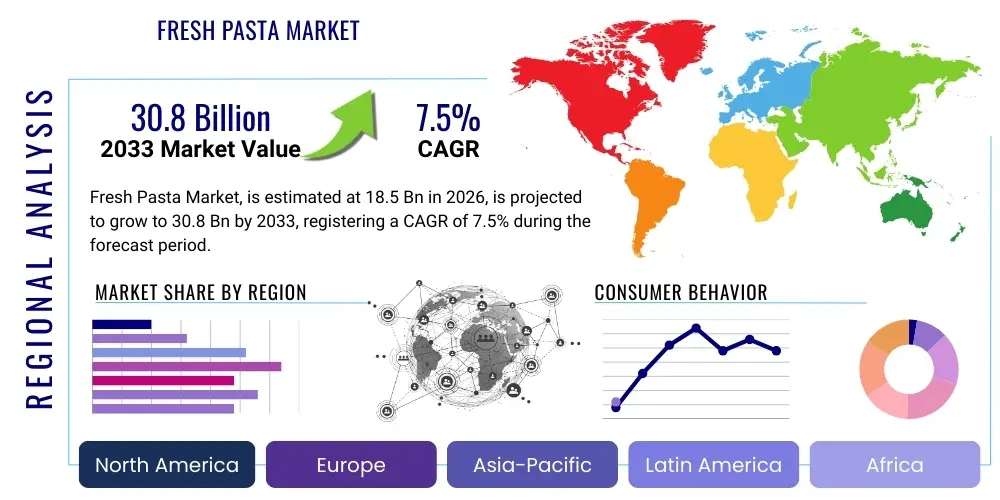

The Fresh Pasta Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at $18.5 Billion in 2026 and is projected to reach $30.8 Billion by the end of the forecast period in 2033. This robust expansion is primarily fueled by shifting consumer preferences towards convenient, high-quality, and perceived healthier alternatives to dry pasta, especially in developed economies where time constraints drive demand for ready-to-cook and fresh refrigerated meal components. The premiumization trend, coupled with increasing disposable incomes and greater availability of chilled storage infrastructure, further underpins this substantial market valuation increase over the forecast timeline.

The Fresh Pasta Market encompasses refrigerated pasta products characterized by high moisture content and a relatively short shelf life, requiring strict cold chain management. Unlike traditional dried pasta, fresh pasta is typically made using durum wheat semolina, eggs, and water, offering superior texture, flavor, and a softer bite profile favored by consumers seeking an "authentic" or "restaurant-quality" experience at home. This segment includes various forms such as sheets, long-cut pasta (e.g., fettuccine, tagliatelle), and stuffed pasta (e.g., tortellini, ravioli).

Major applications for fresh pasta span both retail and foodservice sectors. In retail, consumers utilize these products for quick, gourmet home meals, capitalizing on their rapid cooking time. In the foodservice industry, fresh pasta is essential for restaurants, cafes, and catering services that prioritize superior ingredient quality and minimize preparation time without sacrificing the final dish's quality. The sensory attributes and versatility of fresh pasta make it a foundational component in modern cuisine, supporting both traditional Italian dishes and innovative culinary applications.

The primary driving factors propelling the fresh pasta industry include the global shift towards premium and specialty food items, the rising demand for convenient meal solutions that don't compromise nutritional value, and significant innovations in packaging technologies, such as Modified Atmosphere Packaging (MAP), which extend refrigerated shelf life. Furthermore, manufacturers are successfully catering to evolving dietary needs by introducing robust lines of gluten-free, organic, and vegan fresh pasta, broadening the product's appeal across diverse consumer groups. These market dynamics collectively enhance market penetration and consumer acceptance worldwide.

The global Fresh Pasta Market exhibits strong upward momentum driven by several key business trends, including intensive investment in cold chain logistics optimization and the diversification of product offerings to include specialty dietary items. Business trends highlight strategic partnerships between fresh pasta producers and large retail chains to ensure optimal visibility and product freshness, alongside significant technological advancements in high-speed, gentle manufacturing processes. The market is consolidating, with major players acquiring smaller, artisanal producers to integrate premium branding and specialized regional recipes into their mass-market portfolios, thereby catering to the dual demand for convenience and authenticity.

Regionally, Europe maintains its dominance due to deep-rooted culinary traditions, high consumption rates, and a well-established cold chain infrastructure, particularly in Italy, France, and Germany. However, the Asia Pacific (APAC) region is demonstrating the highest growth trajectory, fueled by rapid urbanization, increasing Western culinary exposure, and the expansion of modern retail formats (supermarkets and hypermarkets) equipped to handle chilled products. North America also remains a crucial growth area, driven by strong consumer demand for ready-to-eat and easy-to-prepare meal kits, often featuring fresh pasta components.

Segment trends indicate a pronounced consumer preference shift toward stuffed pasta varieties (ravioli, tortellini) due to their inherent convenience and perceived value as a complete meal component. Concurrently, the ingredient segmentation shows exponential growth in gluten-free and alternative grain fresh pasta, reflecting a wider health and wellness trend focusing on ingredient transparency and specialized diets. The distribution channel analysis confirms that retail sales, particularly through modern grocery stores and online fresh food delivery platforms, continue to dominate, leveraging the consumer demand for immediate availability and minimal procurement effort.

Common user inquiries regarding AI in the Fresh Pasta Market primarily center on how artificial intelligence can mitigate the critical risks associated with short shelf life and complex supply chains. Users frequently ask about the role of predictive analytics in demand forecasting to minimize waste, the application of machine learning for optimizing production scheduling based on real-time raw material quality (e.g., consistency of eggs or durum wheat), and the integration of AI-powered systems for enhanced quality control, such as automated visual inspection of pasta consistency and filling distribution. Consumers also express interest in AI-driven personalized marketing strategies, where AI algorithms recommend specific fresh pasta varieties and complementary recipes based on purchase history and declared dietary restrictions, fostering greater consumer engagement and product relevance in a highly competitive premium segment.

The Fresh Pasta Market is dynamically shaped by a confluence of driving factors, persistent restraints, and compelling opportunities that dictate market trajectory and investment priorities. Key drivers include accelerating urbanization, leading to time-poor consumers prioritizing convenient, quick-to-prepare meals that retain gourmet quality, and the increasing premiumization of grocery spending, where fresh pasta is viewed as an affordable indulgence. Restraints are predominantly centered around the logistical complexity and high costs associated with maintaining a continuous, unbroken cold chain necessary to preserve product quality and prevent microbial growth over the short shelf life. Opportunities lie in expanding geographical reach into nascent markets (particularly in APAC and Latin America) and vigorously pursuing product innovation in the functional food space, such as high-protein, fiber-enriched, and allergen-free fresh pasta lines, catering to the evolving health-conscious consumer base. These forces collectively define the competitive intensity and potential for future growth within the segment.

The Fresh Pasta Market is meticulously segmented based on Type, Ingredient, and Distribution Channel, allowing market players to tailor strategies to specific consumer behaviors and regional preferences. Segmentation by Type distinguishes between Non-Stuffed (long and short cuts, sheets) and Stuffed varieties (ravioli, tortellini, cappelletti), with the latter commanding a significant and growing share due to its convenience as a complete meal component. Ingredient-based segmentation includes Wheat (durum semolina being the traditional standard) and Non-Wheat/Gluten-Free options (utilizing rice, corn, or legume flours), driven by rising prevalence of celiac disease diagnoses and broader lifestyle choices favoring grain alternatives. Distribution Channel stratification separates Retail (supermarkets, hypermarkets, convenience stores, online) from Foodservice (restaurants, hotels, catering), where the retail channel maintains the largest volume share due to immediate consumer access.

The value chain for the Fresh Pasta Market is highly dependent on efficient integration and stringent quality control at every stage, particularly given the product's perishable nature. The upstream phase involves the sourcing of high-quality raw materials, primarily premium durum wheat semolina, fresh eggs, and specialty fillings (cheese, meat, vegetables). Variability in raw material quality, especially wheat protein content, directly impacts the final pasta texture and stability. Manufacturers must establish reliable procurement relationships and implement rigorous inbound testing protocols to ensure consistency, which is a significant factor in premium fresh pasta branding. The midstream manufacturing process involves mixing, kneading, extrusion or sheeting, filling (for stuffed varieties), pasteurization, and crucially, specialized packaging like Modified Atmosphere Packaging (MAP) to extend refrigerated life. Efficiency in this stage, driven by advanced automation, is critical to maintaining cost competitiveness and scalability.

The downstream segment focuses heavily on cold chain logistics, which constitutes a major cost and risk factor. Distribution channels are categorized into direct and indirect routes. Direct distribution involves manufacturers supplying large institutional clients or operating proprietary refrigerated delivery fleets to major grocery distribution centers. Indirect distribution relies on third-party logistics (3PL) providers specializing in chilled transport, delivering to diverse retail formats, from large hypermarkets to smaller, urban convenience stores. The retail segment is increasingly diversified by the burgeoning growth of e-commerce and specialized fresh food delivery services, which require even faster and more precisely monitored transportation.

Retail and Foodservice outlets represent the final touchpoints. For retail, presentation (shelf placement, product visibility) and inventory management (rotation to minimize expiry) are paramount. The Foodservice channel relies on strong relationships with culinary distributors who can provide just-in-time inventory to restaurants, minimizing their storage requirements. The complexity of the fresh pasta value chain, defined by its reliance on speed and temperature control, necessitates constant technological investment in packaging and refrigeration to reduce waste and enhance overall supply chain resilience and efficacy.

Potential customers for the Fresh Pasta Market are generally defined by their appreciation for quality ingredients, willingness to pay a premium for convenience, and often, a higher disposable income. The primary consumer group consists of time-constrained professionals and millennials who seek quick-cooking, wholesome, and flavorful meal solutions that surpass the quality of standard frozen or dry alternatives. These consumers prioritize authenticity and natural ingredients, often associating fresh pasta with a superior culinary experience compared to mass-market dry products.

Another significant segment comprises gourmet home cooks and food enthusiasts who use fresh pasta as a base for elaborate, high-end dishes, valuing the product's textural superiority and ability to absorb sauces effectively. Furthermore, institutional buyers, including high-end restaurants, hotels, and specialized catering services (HORECA sector), are key buyers. These professional establishments rely on fresh pasta to maintain menu quality while simultaneously achieving efficiency in the kitchen, often purchasing in bulk through specialized foodservice distributors to ensure consistent supply and competitive pricing. The final emergent customer group includes individuals following specific dietary regimes, such as gluten-free diets, veganism, or those seeking organic certified products, driving demand for innovative specialty pasta lines.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $18.5 Billion |

| Market Forecast in 2033 | $30.8 Billion |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Barilla G. e R. Fratelli S.p.A., Giovanni Rana S.p.A., De Cecco, Sfoglia Vela S.p.A., Ebro Foods S.A., Covalmar S.r.l., Primo Foods Inc., Waitrose Limited, Pastificio Rana S.p.A., Nestlé S.A. (via acquired brands), Lilly’s Fresh Pasta, Voltan SpA, Conagra Brands (Ronzoni), Delverde S.r.l., Pastificio Di Martino S.p.A., Culinaria Group, O’ Sole Mio. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing and preservation of fresh pasta heavily rely on advanced technological systems focused on extending shelf life while maintaining organoleptic properties. A critical technology is Modified Atmosphere Packaging (MAP), which involves replacing the air inside the package with a precise blend of gases (typically carbon dioxide and nitrogen) to inhibit bacterial growth and slow oxidation, thereby significantly extending the refrigerated shelf life from a few days to several weeks. This technological necessity has fundamentally altered the distribution feasibility and geographical reach of fresh pasta producers, allowing for broader market penetration beyond immediate local markets. Furthermore, High-Pressure Processing (HPP) is emerging as a non-thermal preservation method used to inactivate pathogens and spoilage microorganisms, offering a clean-label alternative to chemical preservatives, aligning perfectly with consumer demand for natural and minimally processed foods. The adoption of HPP, although capital intensive, enhances product safety and stability without compromising the fresh texture and flavor profiles.

In the production phase, technological advancements center on high-speed automation and precision engineering. Continuous vacuum mixers and extruders ensure homogeneous dough consistency and eliminate air bubbles, leading to superior pasta quality and extended shelf stability. For stuffed pasta, precise volumetric dosing systems are utilized to ensure uniform filling quantity across all units, critical for quality assurance and consistent cooking performance. Robotics and highly automated assembly lines are reducing manual handling, minimizing the risk of contamination, and accelerating production throughput to meet soaring global demand. Additionally, sophisticated sensors and IoT devices are being integrated into the manufacturing environment to monitor temperature, humidity, and machine performance in real-time, allowing for predictive maintenance and immediate quality adjustments, which is essential given the perishable nature of the product ingredients.

The technological landscape also includes advanced traceability systems, often utilizing blockchain technology, to ensure complete transparency regarding raw material sourcing (e.g., origin of durum wheat or specialty eggs) and cold chain journey. This is vital for addressing increasing regulatory scrutiny and satisfying consumer demand for ethical sourcing and food safety assurance. Sustainable packaging innovation, shifting from standard plastic trays to recyclable, compostable, or bio-based materials, represents another key technological focus area, driven by corporate sustainability goals and consumer pressure to minimize environmental impact associated with the chilled food sector. These technological investments are critical for future competitive advantage, focusing on quality, safety, and environmental stewardship.

Regional dynamics play a crucial role in shaping the Fresh Pasta Market, reflecting differences in culinary tradition, cold chain maturity, and consumer purchasing power. Europe stands as the dominant market, driven by its profound culinary heritage and the high per capita consumption of pasta in key countries like Italy, France, and Germany. The European market benefits from a highly sophisticated and mature chilled distribution network, which minimizes spoilage and ensures product freshness across extensive retail networks. The region also acts as a primary innovation hub, pioneering new preservation techniques and specialty product formulations (organic, locally sourced ingredients), maintaining its lead in both volume and value terms. Italy, in particular, showcases high brand loyalty to artisanal fresh pasta producers, fueling the premium segment growth.

North America is characterized by robust growth, primarily fueled by the strong demand for convenient, time-saving meal solutions. The market growth here is less tied to traditional cooking methods and more focused on ready-to-eat and fully prepared fresh pasta kits, appealing to busy households. Investment in large-scale production facilities and improved retail refrigeration capacity has facilitated greater accessibility of fresh pasta. The competitive landscape in the U.S. is marked by aggressive marketing and product diversification, including a wide array of ethnic and fusion flavors to capture diverse consumer preferences. The high penetration of large grocery chains and bulk retailers further supports volume expansion in this region.

The Asia Pacific (APAC) region represents the fastest-growing market, albeit from a lower base, driven by rapid economic development, urbanization, and the increasing westernization of diets. As disposable incomes rise, consumers in countries like China, India, and Australia are exploring and adopting chilled and fresh food categories. The key challenge in APAC is the heterogeneous cold chain infrastructure; while developed urban centers boast reliable refrigeration, penetration remains a hurdle in secondary and tertiary cities. Consequently, market players are focused on adapting packaging technologies (e.g., higher barrier films) to withstand more varied logistical conditions and investing heavily in modern retail channel expansion to capture this emerging consumer base.

Latin America and the Middle East & Africa (MEA) are emerging markets for fresh pasta. In Latin America, particularly Brazil and Argentina, there is a moderate cultural affinity for pasta, but the growth is constrained by economic volatility and less developed refrigerated supply chains outside metropolitan areas. MEA growth is concentrated in affluent urban hubs, driven by tourism and expatriate populations influencing local consumption patterns. Market entry strategies in these regions often focus on leveraging established foodservice channels before attempting large-scale retail penetration, due to the high logistical costs associated with chilled distribution across vast, often hot climates.

The primary driver is the accelerating consumer demand for convenient, premium, and quick-to-prepare meal solutions. Fresh pasta offers superior taste and texture compared to dry alternatives, aligning with the trend of affordable gourmet experiences at home, especially among time-constrained urban populations globally.

The inherently short shelf life necessitates a highly optimized and unbroken cold chain logistics network (refrigerated transport and storage). This requirement significantly increases operational complexity and distribution costs compared to shelf-stable dry pasta, acting as a critical restraint, especially when entering geographically distant markets.

Modified Atmosphere Packaging (MAP) is the most critical preservation technology. MAP replaces standard air with a gas mixture (CO2/N2) within the packaging, effectively inhibiting microbial growth and oxidation, which significantly extends the product's refrigerated shelf life from a few days to several weeks without compromising quality.

The Non-Wheat/Gluten-Free segment, utilizing flours derived from rice, corn, and legumes, is experiencing the fastest growth. This is fueled by rising health consciousness, dietary restrictions (like celiac disease), and consumer preference for grain alternatives and functional foods with higher protein or fiber content.

Europe holds the dominant share of the global market. This dominance is attributed to centuries-old culinary traditions, exceptionally high per capita consumption, mature and reliable cold chain infrastructure, and the continuous presence of both mass-market producers and high-quality artisanal brands.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.