ID : MRU_ 443809 | Date : Feb, 2026 | Pages : 251 | Region : Global | Publisher : MRU

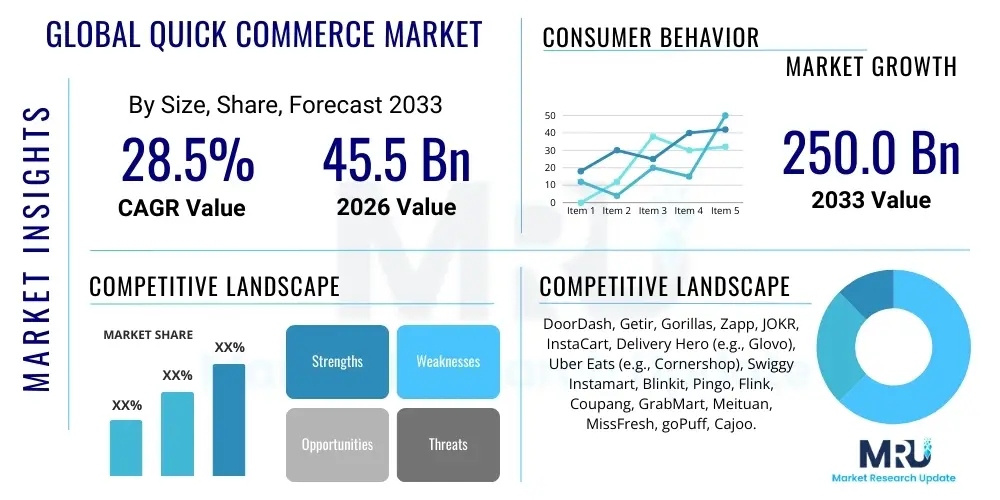

The Global Quick Commerce Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 28.5% between 2026 and 2033. This exponential growth trajectory is fundamentally driven by shifting consumer expectations towards instant gratification and the continuous optimization of hyper-local logistics infrastructure worldwide. The intense competitive landscape and heavy venture capital investment in rapid expansion models further solidify this high growth forecast, transforming traditional retail supply chains into agile, technology-driven networks designed for speed.

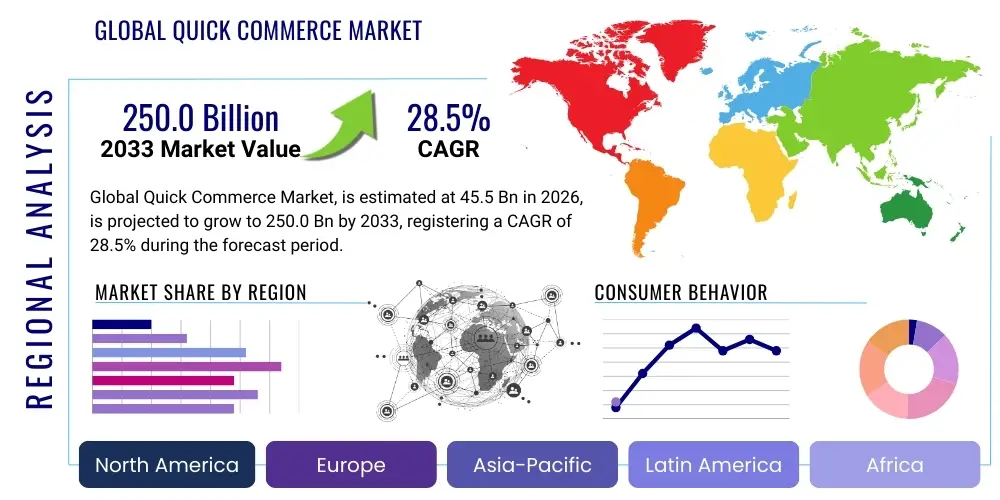

The market is estimated at USD 45.5 Billion in 2026, reflecting the massive consumer adoption spurred by pandemic-related demand shifts and subsequent investments in 'dark store' operations and automated fulfillment centers. This valuation incorporates revenue generated across various models, including dedicated inventory-based services and marketplace facilitators focusing exclusively on ultra-fast delivery promises, typically under 30 minutes, often aiming for 10-15 minutes.

By the end of the forecast period in 2033, the global quick commerce sector is projected to reach USD 250.0 Billion. This significant escalation in market value will be fueled by geographic penetration into Tier 2 and Tier 3 cities, diversification beyond grocery into pharmaceutical and general merchandise categories, and the integration of advanced technologies like AI-driven demand forecasting and drone or robotic delivery systems, ensuring scalability and profitability in high-density urban areas.

The Global Quick Commerce (Q-Commerce) Market encompasses the business model focused on the swift delivery of retail goods, typically groceries, convenience items, and pharmaceuticals, characterized by delivery times ranging from 10 to 30 minutes. This segment differentiates itself from conventional e-commerce by prioritizing speed and convenience through specialized hyper-local fulfillment infrastructures, predominantly utilizing 'dark stores' or micro-fulfillment centers strategically located within densely populated urban zones. Q-Commerce platforms employ sophisticated logistics software, coupled with dedicated fleets of riders, to meet stringent time constraints, effectively transforming the consumer purchasing experience from planning-based to immediate necessity fulfillment.

Major applications of quick commerce span essential consumer needs, including emergency grocery restocking, prepared meals, over-the-counter medication delivery, and impulse purchases. The primary benefits driving market acceptance include unparalleled convenience, substantial time savings for consumers, and the ability to minimize stock-outs by accessing proximal inventory. Q-Commerce enhances urban mobility efficiency by consolidating deliveries and reducing individual consumer trips to retail locations.

Key driving factors accelerating the market’s expansion involve surging urbanization rates, increasing digital literacy coupled with high smartphone penetration, and the persistent desire among Millennial and Generation Z consumers for instantaneous service. Furthermore, significant capital injections from institutional investors continue to fund aggressive geographic expansion and technological innovation, particularly in route optimization and inventory management systems, enabling platforms to achieve the required speed and reliability metrics necessary to sustain consumer loyalty and competitive advantage.

The Quick Commerce market is experiencing transformative growth, underpinned by dynamic business trends such as the consolidation of regional players, the pivot towards profitability through optimized fulfillment metrics, and the strategic integration of private label products to enhance margin structures. Operators are increasingly leveraging data analytics to refine dark store placement, ensuring proximity to high-demand clusters while minimizing real estate overheads. The dominant trend involves transitioning from high cash burn models, focused solely on market share acquisition, to sustainable operational frameworks emphasizing customer lifetime value (CLV) and delivery unit economics, often involving subscription models and premium service tiers.

Regionally, Asia Pacific and Europe exhibit the most intense competitive landscapes and the highest adoption rates. Asia Pacific's growth is propelled by vast, densely populated mega-cities and established networks of two-wheeler delivery riders, making quick commerce highly scalable. Europe, particularly Western Europe, is characterized by sophisticated digital infrastructure and high consumer willingness to pay for convenience, though it faces stricter labor regulations and high urban rental costs. North America, while having massive potential, faces unique challenges related to sprawl and lower population density in many areas, requiring alternative fulfillment strategies like integrating with existing large retail footprints or specialized micro-warehouses.

Segmentation trends indicate that the Grocery segment remains the undisputed leader, accounting for the largest share of market revenue, driven by high purchase frequency and low barriers to consumer adoption. However, the Pharmaceuticals and Health & Wellness segments are poised for rapid acceleration, pending regulatory navigation, as consumers seek rapid fulfillment for non-prescription and prescription needs. The inventory-based model (dark stores) currently dominates due to its superior control over stock and fulfillment speed, although the marketplace model remains critical for platforms entering fragmented markets or providing supplementary specialty items.

User inquiries concerning AI's influence on Quick Commerce heavily concentrate on automation efficiency, profitability, and personalization. Consumers and industry stakeholders frequently question how AI can transition Q-Commerce from a costly, labor-intensive model to a streamlined, sustainable business. Specific thematic concerns include AI's role in optimizing delivery routes in real-time to overcome urban congestion, improving hyper-local inventory accuracy to prevent costly cancellations (What is the acceptable level of inventory forecasting error?), and enabling truly predictive shopping experiences rather than simple recommendation engines. The expectation is that AI will be the primary lever for reducing labor costs, enhancing customer experience through hyper-personalization, and ensuring logistical efficiency that justifies the premium cost of speed, ultimately determining the long-term viability of the 10-minute delivery promise.

AI's adoption is viewed as essential for scaling quick commerce operations while maintaining high service levels. Crucially, AI-driven analytics are being deployed to monitor rider behavior, predict demand fluctuations based on external factors like weather and local events, and dynamically price both products and delivery fees to maximize yield and stabilize margins during peak hours. The deployment of generative AI models is also starting to influence customer service, providing instantaneous and highly localized support regarding product availability and delivery status, thereby reducing call center load and improving the overall customer journey experience.

Furthermore, AI algorithms are vital for optimizing dark store layouts and picking processes. By analyzing historical order patterns and product adjacency, AI guides human pickers through the most efficient paths, shaving precious seconds off the internal fulfillment time—a critical metric in quick commerce. The deployment extends into fraud detection and supply chain risk management, ensuring that the intensely fast pace of transactions does not compromise security or reliability, guaranteeing a robust operational backbone for hyper-speed deliveries.

The dynamics of the Global Quick Commerce Market are fundamentally shaped by a complex interplay of high-impact drivers and critical restraining factors, creating a market environment where strategic agility and sufficient capitalization are paramount for survival. The primary driver is the pervasive consumer demand for convenience and instant gratification, cemented by the success of earlier generations of digital services. Coupled with this is the continuous improvement in digital infrastructure, including high-speed mobile connectivity and sophisticated geolocation technologies, which allow for precision logistics. However, the market is severely restrained by intense capital expenditure requirements for establishing and maintaining dense networks of dark stores and micro-fulfillment centers, compounded by persistently high operational costs, particularly last-mile labor expenses and urban real estate rental rates.

Significant opportunities arise from the market's current fragmentation and the potential for consolidation, offering established players a pathway to achieve economies of scale and mitigate high per-order fulfillment costs. Geographic expansion into underserved Tier 2 cities, where competition is nascent but population density is favorable, represents a major growth avenue. Furthermore, vertical integration into adjacent services, such as specialized pharmaceutical delivery or B2B quick supply for small enterprises, provides lucrative diversification possibilities. The most powerful impact forces shaping the industry are the twin pressures of competitive intensity—which forces continual subsidies and promotional pricing—and the regulatory environment, especially concerning urban logistics, labor laws, and licensing for potentially sensitive goods like alcohol or pharmaceuticals.

The critical impact forces often revolve around regulatory changes, specifically those affecting gig economy workers and urban traffic management. A shift towards mandatory employment status for delivery riders in major jurisdictions significantly increases operational expenses, directly challenging the profitability model. Conversely, the successful adoption of automation, such as autonomous vehicles or drone delivery systems, acts as a powerful enabling force that could fundamentally alter unit economics by minimizing dependency on human labor for last-mile delivery. Navigating this landscape requires Q-Commerce platforms to maintain flexibility, focusing on maximizing technological efficiencies to counteract rising labor and infrastructure costs while simultaneously defending market share against well-funded incumbents and agile new entrants.

The Global Quick Commerce Market is comprehensively segmented based on its operational models, the type of products offered, and the nature of the end-user. This segmentation is crucial for understanding the varying degrees of capital intensity, margin profiles, and competitive advantages held by different market players. The primary distinction lies between platforms that maintain their own inventory (inventory-based/dark store models) and those that leverage existing third-party retail stores (marketplace models). Product type segmentation reflects consumer habits and regulatory hurdles, while end-user classification helps platforms tailor their service level agreements and delivery infrastructure, optimizing for residential urgency versus commercial bulk or regularity.

The rapid growth of the quick commerce ecosystem necessitates precision targeting, achieved through detailed segmentation. For instance, the grocery segment demands extremely tight control over chilled/frozen logistics and high inventory turnover, whereas the pharmaceutical segment requires specialized regulatory compliance and handling protocols. Furthermore, operational models significantly influence profitability; inventory-based models offer superior speed and stock control but demand substantial upfront capital, while marketplace models are asset-light but often suffer from variability in product quality and stock visibility, forcing players to strategically choose a model that aligns with their desired market footprint and long-term financial goals.

Analysis confirms that the inventory-based model is currently the most dominant in mature markets, driving the fastest delivery times and highest customer satisfaction, despite higher operational expenses. However, hybrid models—where a marketplace framework integrates dedicated dark stores in critical zones—are gaining traction, offering a balance between market penetration speed and control over the core delivery experience. Understanding these intricate segment dynamics allows investors and operators to correctly allocate resources toward technology development, warehouse footprint expansion, and targeted marketing campaigns essential for achieving sustainable growth in this hyper-competitive sector.

The Quick Commerce value chain is characterized by its high speed and extreme dependence on seamless integration between digital ordering and physical fulfillment, making technology the central nervous system. The upstream analysis focuses on sourcing and procurement, where operators secure high-quality, fresh inventory, often negotiating directly with local suppliers or large distribution centers to maintain competitive pricing and consistent stock levels required for instant fulfillment. This stage necessitates robust supplier management systems and automated quality control to handle high-frequency, smaller-batch procurements, which differ substantially from traditional bulk retail buying. The operational efficiency of this upstream segment directly impacts product availability and margin stability, critical determinants of long-term viability.

The core of the value chain involves the midstream activities: fulfillment and logistics, centered around the dark store network. Products are received, stored, and then rapidly picked and packed (P&P) upon order placement. This phase demands sophisticated Warehouse Management Systems (WMS), AI-driven inventory mapping, and optimized picking routes to minimize the time between click and handover to the rider. Distribution channels are predominantly direct, utilizing proprietary fleets of independent contractors or employed riders for the last-mile sprint. The strategic location and operational synchronization of the dark store with the last-mile fleet are the key differentiators in quick commerce, determining whether the 10-15 minute delivery promise is met consistently.

Downstream analysis focuses on customer acquisition, engagement, and retention, primarily executed through seamless mobile application experiences and real-time communication. The direct distribution channel is almost entirely digital, utilizing indirect marketing (SEO/SEM, social media) for initial customer acquisition, followed by loyalty programs and push notifications to drive repeat orders. Unlike traditional retail, where location dictates access, quick commerce success is tied to data utilization for personalization and predictive stocking, ensuring that the final customer experience—the actual moment of ultra-fast delivery—is flawless and reinforces the perceived value of the speed premium paid by the consumer.

The primary end-users and buyers in the Global Quick Commerce Market are densely concentrated in urban and metropolitan areas, characterized by high disposable incomes and a strong preference for convenience over cost savings associated with traditional grocery shopping or planned purchases. This demographic primarily includes busy working professionals, small households, and individuals utilizing Q-Commerce for impulse buying or emergency restocking of essentials. Quick commerce platforms cater exceptionally well to the 'immediate need' scenario, targeting users who prioritize time savings, particularly in situations where a conventional retail trip is inconvenient, such as late evenings, poor weather conditions, or during peak commuting hours when traveling to a store is inefficient.

A rapidly growing segment of potential customers includes the elderly or those with mobility restrictions, for whom quick commerce provides a vital alternative to physical shopping, offering accessibility and speed for essential goods like non-prescription medication and routine groceries. Furthermore, the commercial end-user segment—comprising small offices, co-working spaces, and boutique businesses—is increasingly relying on quick commerce platforms for instant supplies, such as coffee, office stationery, or immediate catering needs, leveraging the speed advantage to avoid business interruptions and maintain operational flow without dedicated procurement staff.

The market also targets digitally native consumers (Millennials and Gen Z) who have normalized on-demand services across all aspects of life, viewing quick commerce as a baseline utility rather than a luxury. Customer acquisition strategies are heavily weighted towards attracting these frequent users through loyalty programs and seamless app integrations, focusing on maximizing the frequency of small orders rather than the size of the basket. The potential market size is directly correlated with urban density and average order value, driving operators to prioritize expansion in high-rise residential zones and dense city centers worldwide.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 45.5 Billion |

| Market Forecast in 2033 | USD 250.0 Billion |

| Growth Rate | 28.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DoorDash, Getir, Gorillas, Zapp, JOKR, InstaCart, Delivery Hero (e.g., Glovo), Uber Eats (e.g., Cornershop), Swiggy Instamart, Blinkit, Pingo, Flink, Coupang, GrabMart, Meituan, MissFresh, goPuff, Cajoo. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological foundation of the Quick Commerce market is centered on achieving ultra-low latency and hyper-precision in logistics, requiring a sophisticated stack ranging from mobile application interfaces to advanced warehouse automation. Mobile platforms must offer near-instantaneous stock updates, personalized browsing experiences, and seamless checkout processes, utilizing robust cloud infrastructure to handle massive spikes in localized demand efficiently. Crucially, proprietary algorithms govern route planning and batching, leveraging geo-spatial data, real-time traffic analysis, and machine learning to consistently reduce last-mile delivery times, making the difference between success and failure in meeting the 10-15 minute promise.

Fulfillment technology within dark stores is equally vital, characterized by advanced inventory management systems (IMS) integrated with handheld devices for guided picking and packing. Many leading platforms are investing heavily in micro-fulfillment automation (MFA), incorporating elements like automated storage and retrieval systems (AS/RS) or robotic picking assistance for faster turnaround times and reduced reliance on manual labor, which mitigates high operational expenses. This automation aims to transform the internal dark store process from a manual operation into a highly efficient, high-throughput machine capable of processing hundreds of small orders per hour per facility, optimizing the critical first leg of the delivery journey.

Furthermore, data analytics and AI are the core engines driving strategic decisions. Technologies for predictive analytics are deployed to forecast localized demand patterns based on factors such as weather, local events, and time of day, ensuring inventory is positioned optimally to match consumer needs and reduce spoilage of fresh goods. Payment processing infrastructure must also be instantaneous and secure, supporting high volumes of small-value, frequent transactions. The future technology landscape anticipates greater integration of autonomous delivery vehicles (drones or ground robots) in controlled urban environments, potentially revolutionizing the final mile cost structure and significantly enhancing scalability while maintaining or improving speed metrics.

The regional analysis reveals distinct market maturity levels, competitive structures, and regulatory challenges across different geographies, yet all are united by the fundamental drive for instant delivery convenience. Asia Pacific (APAC) dominates the quick commerce landscape in terms of market volume and competitive intensity, particularly in densely populated countries like China, India, and Southeast Asia. This region benefits from a highly advanced digital infrastructure, consumer familiarity with on-demand services, and a vast, cost-effective workforce for last-mile delivery, allowing platforms like Meituan and Swiggy Instamart to scale rapidly, often achieving delivery targets under 15 minutes routinely.

Europe represents a highly fragmented but mature quick commerce market, with major competition occurring in metropolitan hubs such as London, Berlin, and Paris. Western European consumers exhibit high willingness to pay for premium services, fueling the growth of players like Getir, Gorillas, and Flink. However, these markets face substantial regulatory headwinds concerning labor laws, urban planning restrictions on dark store locations, and high real estate costs, often leading to intense financial struggles and subsequent consolidation among key players who are now focusing aggressively on achieving unit profitability rather than pure market share.

North America, led by the United States, presents a unique challenge due to lower urban density compared to Europe or APAC. Quick commerce players like goPuff and DoorDash are adapting by employing larger dark stores covering broader geographic radii or leveraging partnerships with mainstream retailers (e.g., Instacart’s model). Growth here is heavily reliant on technological solutions for route efficiency across longer distances and significant investment in cold chain logistics to serve suburban areas effectively, making the logistical complexity higher but the potential market size enormous, particularly in major coastal cities.

Latin America (LATAM) showcases explosive growth potential, driven by young, digitally savvy populations and a general lack of high-quality traditional retail infrastructure in many areas, creating a vacuum that quick commerce fills effectively. Platforms in Brazil and Mexico are expanding rapidly, capitalizing on high smartphone penetration, though they must navigate challenges related to fragmented distribution networks and significant security risks associated with high-value goods and cash transactions. The Middle East and Africa (MEA) market is still nascent but rapidly developing, fueled by high disposable incomes in Gulf nations and government initiatives promoting digital economies, though scalability remains hindered by infrastructure gaps in some parts of Africa.

Quick Commerce (Q-Commerce) specializes in ultra-fast delivery, typically within 10 to 30 minutes, relying on hyper-local infrastructure like dark stores. Traditional e-commerce focuses on scheduled delivery windows or standard shipping, prioritizing inventory depth and lower logistics cost over instantaneous speed.

Profitability is achieved through optimization strategies including AI-driven route optimization, increased order density within tight geographic zones, higher average order values (AOV) driven by targeted promotions, and leveraging private label goods for superior margin control. Consolidation and scale also help reduce fulfillment costs per order.

Dark stores are small, localized micro-fulfillment centers or warehouses strategically placed in densely populated urban areas, closed to the public. They are essential because they allow Q-Commerce operators to store inventory extremely close to the consumer base, minimizing the distance required for last-mile delivery and enabling the promised speed.

The Asia Pacific (APAC) region is currently leading in terms of absolute market volume and scale of operations, driven by high population density, rapid digitalization, and consumer acceptance of on-demand delivery models in key markets like China and India.

AI is set to revolutionize Q-Commerce logistics by enabling highly accurate predictive demand forecasting, optimizing inventory placement within dark stores, and providing dynamic, real-time route optimization for delivery riders, which is critical for achieving sustainable operational efficiency and cost reduction at scale.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.