ID : MRU_ 444144 | Date : Feb, 2026 | Pages : 242 | Region : Global | Publisher : MRU

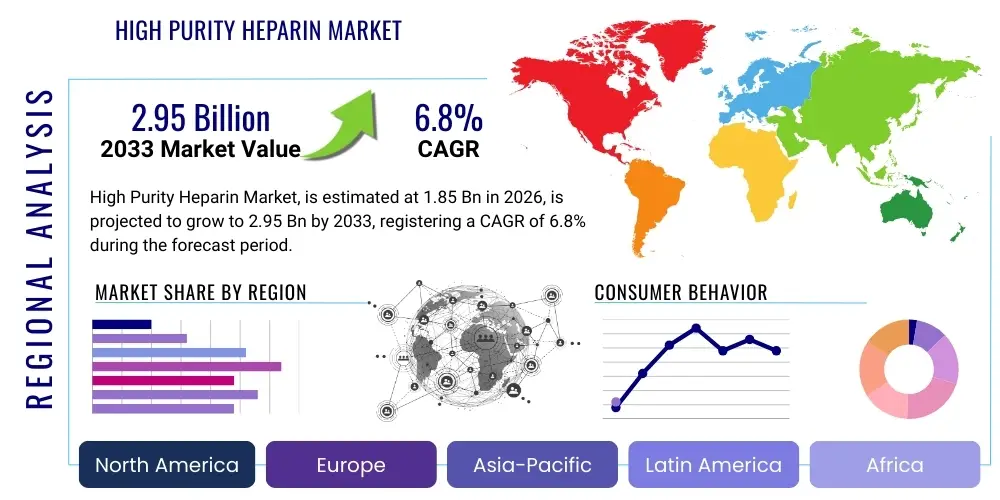

The High Purity Heparin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 2.95 Billion by the end of the forecast period in 2033.

The High Purity Heparin Market encompasses the global trade and utilization of pharmaceutical-grade heparin, a crucial anticoagulant derived primarily from porcine intestinal mucosa. This complex glycosaminoglycan is renowned for its potent ability to prevent blood clot formation, a characteristic that makes it indispensable in numerous medical applications. As a product, high purity heparin distinguishes itself through stringent manufacturing processes that ensure minimal impurities, consistent molecular weight distribution, and adherence to pharmacopeial standards, thereby guaranteeing its safety and efficacy in therapeutic settings. Its robust anticoagulant activity is attributed to its unique structure, which binds to antithrombin III, accelerating its inhibitory action on various coagulation factors, particularly thrombin and Factor Xa. The market's foundational strength lies in its long-standing history of clinical use and its essential role in preventing and treating thrombotic disorders across a broad spectrum of patient populations.

Major applications of high purity heparin span critical areas within healthcare, including the prophylaxis and treatment of deep vein thrombosis (DVT) and pulmonary embolism (PE), anticoagulation during cardiac surgery, percutaneous coronary interventions, and extracorporeal circulation procedures such as hemodialysis. Furthermore, it plays a vital role in maintaining the patency of intravenous and arterial catheters, preventing clot formation in blood samples for diagnostic purposes, and in various other medical conditions where thromboprophylaxis is paramount. The benefits of high purity heparin are extensive, offering rapid onset of action, dose adjustability, and a reversible effect with protamine sulfate, making it a highly versatile and controllable anticoagulant. Its established efficacy and relatively lower cost compared to some newer anticoagulants continue to cement its position as a first-line therapy in many clinical guidelines, highlighting its indispensable nature in modern medicine and healthcare systems worldwide.

The market for high purity heparin is significantly driven by several interconnected factors. A primary driver is the global increase in the prevalence of cardiovascular diseases (CVDs), including conditions such as myocardial infarction, stroke, and peripheral artery disease, which frequently necessitate anticoagulant therapy. The rising number of surgical procedures, particularly those involving cardiovascular, orthopedic, and abdominal interventions, invariably increases the demand for perioperative thromboprophylaxis, where heparin is a standard choice. Moreover, the expanding aging population globally is more susceptible to thrombotic events, further fueling the need for effective anticoagulants. Advances in diagnostic capabilities leading to earlier and more accurate detection of thrombotic conditions also contribute to increased heparin prescriptions. Furthermore, the growing awareness among healthcare professionals regarding evidence-based guidelines for thromboprophylaxis, coupled with the need for safe and reliable anticoagulants in critical care settings, continuously underpins the demand for high purity heparin, driving its sustained market growth.

The High Purity Heparin Market is characterized by dynamic business trends, evolving regional demands, and significant segmentation shifts. Currently, business trends are focusing on supply chain resilience and transparency, largely in response to past supply disruptions and quality concerns. Pharmaceutical manufacturers are investing in advanced purification technologies to meet increasingly stringent regulatory standards set by agencies like the FDA and EMA, ensuring product consistency and safety. There is also a notable trend towards strategic partnerships and collaborations among raw material suppliers, API manufacturers, and finished product distributors to secure supply and expand market reach. Furthermore, the market is experiencing consolidation, with larger players acquiring smaller specialized firms to enhance their product portfolios and technological capabilities, aiming to streamline production and achieve economies of scale. The emphasis on sustainable sourcing and ethical practices concerning animal welfare is also gaining traction, influencing procurement strategies and brand reputation within the industry.

Regionally, the market exhibits diverse growth patterns. North America and Europe continue to represent mature markets with stable demand driven by established healthcare infrastructures, high incidence of chronic diseases, and advanced surgical practices. However, the Asia Pacific (APAC) region is emerging as the fastest-growing market, propelled by rapidly expanding healthcare expenditures, increasing medical tourism, a burgeoning aging population, and improvements in healthcare access and infrastructure, particularly in countries like China and India. Latin America and the Middle East & Africa (MEA) are also showing promising growth potential, albeit from a smaller base, attributed to rising awareness of thrombotic disorders, increasing investments in healthcare facilities, and government initiatives aimed at improving public health. These regions offer significant untapped market opportunities for heparin manufacturers and distributors looking to diversify their geographical footprint, though they often present unique regulatory and logistical challenges that require tailored market entry strategies and localized distribution networks to navigate effectively.

Segmentation trends within the High Purity Heparin Market reveal a continued dominance of therapeutic applications, specifically in the management of deep vein thrombosis and pulmonary embolism, as well as critical care settings. The demand for low molecular weight heparin (LMWH) derivatives is steadily growing due to their improved pharmacokinetic profiles, greater bioavailability, and reduced need for monitoring compared to unfractionated heparin, driving innovation in this sub-segment. Hospitals remain the largest end-user segment, consistently driving substantial demand for both unfractionated and LMWH products for a wide array of procedures and patient treatments. However, there's an observable increase in demand from ambulatory surgical centers and home healthcare settings, particularly for LMWH, as healthcare delivery models shift towards outpatient care and patient self-administration becomes more common. The market also sees a steady demand from diagnostic laboratories for reagents and from research institutions exploring new applications and synthetic alternatives, highlighting the diverse utility and persistent clinical relevance of high purity heparin across the entire healthcare ecosystem.

User inquiries regarding AI's impact on the High Purity Heparin market predominantly revolve around optimizing manufacturing processes, enhancing supply chain resilience, and improving drug discovery and development, particularly for novel anticoagulant agents or heparin alternatives. Users are keen to understand how AI can address historical challenges such as raw material sourcing vulnerabilities, quality control inconsistencies, and the complexities of purification. There's also significant interest in AI's potential to personalize anticoagulant therapy, predict patient responses, and minimize adverse events, thereby enhancing patient safety and treatment efficacy. Overall, the community expects AI to drive efficiency, reduce costs, and foster innovation within this mature but critical pharmaceutical segment, transitioning from traditional methods to data-driven decision-making in various operational facets.

The High Purity Heparin Market is significantly influenced by a confluence of driving forces, inherent restraints, and emerging opportunities, all subject to various impact forces that shape its trajectory. Key drivers propelling the market include the escalating global burden of cardiovascular diseases (CVDs) and other thrombotic conditions such as deep vein thrombosis (DVT) and pulmonary embolism (PE), necessitating effective anticoagulant therapies. The expanding geriatric population, inherently more susceptible to these conditions, further intensifies demand. Furthermore, the increasing number of complex surgical procedures, including cardiac interventions, orthopedic surgeries, and organ transplants, invariably requires perioperative anticoagulation, solidifying heparin's role. The established clinical efficacy, rapid onset of action, and reversibility of heparin, coupled with its cost-effectiveness compared to many newer anticoagulant alternatives, continue to make it a preferred choice among clinicians and healthcare systems worldwide, ensuring a stable and growing demand curve. Additionally, advancements in diagnostic technologies leading to earlier and more accurate detection of thrombotic risks contribute to proactive treatment initiation, augmenting heparin utilization.

Despite robust demand, the market faces notable restraints. A significant challenge is the inherent reliance on animal-derived raw materials, primarily porcine intestinal mucosa. This dependence creates vulnerabilities in the supply chain, making it susceptible to outbreaks of animal diseases, geopolitical tensions affecting trade, and ethical concerns regarding animal sourcing. The infamous 2008 heparin contamination crisis highlighted the critical need for stringent quality control and supply chain transparency, leading to heightened regulatory scrutiny and increased compliance costs for manufacturers. Furthermore, the advent and growing adoption of novel oral anticoagulants (NOACs), while not direct substitutes for all heparin applications, do offer an alternative for certain patient populations, posing a competitive threat. Price volatility of raw materials, coupled with intense competition among generic heparin manufacturers, can exert downward pressure on profit margins. The complex and expensive purification processes required to produce high purity, pharmaceutical-grade heparin also present a significant barrier to entry for new players, limiting market dynamism and potentially hindering innovation in certain areas.

Amidst these challenges, several opportunities present themselves within the High Purity Heparin Market. The development and implementation of advanced purification technologies, such as improved chromatography and filtration techniques, offer the potential to enhance yield, reduce impurity profiles, and bolster safety, thereby addressing past quality concerns and meeting evolving regulatory requirements. Exploration into alternative non-animal sources for heparin or synthetic heparin mimetics represents a long-term opportunity to mitigate supply chain risks and cater to ethical considerations, though significant research and development investments are required. The growing demand for biosimilar low molecular weight heparins (LMWHs) offers a cost-effective alternative to originator products, expanding patient access in developing economies. Furthermore, geographical expansion into underserved markets with rapidly developing healthcare infrastructures, particularly in Asia Pacific and Latin America, presents substantial growth avenues. Enhanced supply chain traceability leveraging digital technologies like blockchain, coupled with robust quality assurance protocols, can rebuild trust and strengthen the market's reputation, unlocking further growth potential. The market is also impacted by forces such as the bargaining power of buyers (large hospital groups, PBMs), the bargaining power of suppliers (raw material providers), the threat of new entrants (due to high capital and regulatory barriers), the threat of substitutes (NOACs, synthetic mimetics), and intense competitive rivalry among established players.

The High Purity Heparin market is meticulously segmented to provide a comprehensive understanding of its diverse applications, product types, and end-user demands. This segmentation allows for a detailed analysis of market dynamics across various categories, highlighting key growth areas and competitive landscapes. By breaking down the market into these distinct components, stakeholders can better identify specific opportunities, tailor product development, and refine market entry strategies. The divisions reflect the clinical utility of different heparin formulations, the various medical settings in which they are employed, and the underlying therapeutic needs they address, offering a granular view of the market's structure and operational intricacies. Understanding these segments is crucial for forecasting future trends and strategic planning.

The value chain for the High Purity Heparin market is complex and multi-layered, beginning with critical upstream activities that dictate the quality and availability of the foundational raw material. The process initiates with the meticulous sourcing of porcine intestinal mucosa, primarily from slaughterhouses globally. This initial stage involves rigorous inspection and collection protocols to ensure the biological material is free from contaminants and meets specified health standards. Following collection, crude heparin is extracted from the mucosa through enzymatic digestion and precipitation processes, often performed by specialized raw material processors. These upstream activities are highly sensitive to animal health, geopolitical factors affecting livestock trade, and stringent regulatory oversight concerning animal welfare and product safety. Ensuring a consistent, high-quality supply of crude heparin is paramount, as it directly impacts the subsequent purification stages and the final product's efficacy and safety profile. Any disruption or quality lapse at this foundational level can have cascading effects throughout the entire value chain, highlighting the critical importance of robust supplier relationships and transparent sourcing practices in this segment of the pharmaceutical industry.

Moving downstream, the crude heparin undergoes a series of sophisticated purification and manufacturing processes to transform it into pharmaceutical-grade high purity heparin. This stage involves advanced techniques such as chromatography (e.g., ion-exchange chromatography, affinity chromatography), filtration, and ultrafiltration, aimed at removing impurities, proteins, nucleic acids, and other contaminants to achieve the desired purity profile and molecular weight distribution. Strict quality control measures, including analytical testing using methods like Nuclear Magnetic Resonance (NMR), High-Performance Liquid Chromatography (HPLC), and mass spectrometry, are employed at various steps to ensure compliance with pharmacopeial standards (e.g., USP, EP, JP) and regulatory requirements. Once purified, the high purity heparin active pharmaceutical ingredient (API) is formulated into various finished dosage forms, such as injectable solutions of unfractionated heparin or low molecular weight heparin (LMWH), followed by sterile filling, packaging, and labeling. This transformation phase is capital-intensive and requires highly skilled personnel, advanced manufacturing facilities, and adherence to Good Manufacturing Practices (GMP) to ensure the stability, sterility, and therapeutic integrity of the final product, ready for distribution to healthcare providers and ultimately, patients.

The distribution channel for high purity heparin is multifaceted, encompassing both direct and indirect sales approaches to reach its diverse end-users. Direct distribution typically involves pharmaceutical manufacturers supplying large volumes of heparin directly to major hospital networks, group purchasing organizations (GPOs), and governmental healthcare procurement agencies, often through long-term contracts. This approach allows for closer relationships, better control over pricing, and more efficient communication regarding supply and demand. Indirect distribution, which forms a significant portion of the market, relies on a network of wholesalers, third-party logistics (3PL) providers, and specialized pharmaceutical distributors. These intermediaries are crucial for reaching a broader range of end-users, including smaller hospitals, clinics, ambulatory surgical centers, dialysis centers, and pharmacies. They manage warehousing, inventory, and last-mile delivery, ensuring that products are delivered efficiently and compliantly across diverse geographical regions. The choice between direct and indirect channels often depends on market penetration goals, regulatory landscapes in different countries, and the scale of operations. Effective management of these distribution channels is vital for ensuring timely access to this life-saving medication, navigating complex logistics, and maintaining product integrity throughout its journey from manufacturing site to patient administration, underscoring the importance of a robust and resilient supply chain for the high purity heparin market.

The primary potential customers and end-users of high purity heparin are diverse institutions within the global healthcare ecosystem, all requiring a reliable and high-quality anticoagulant for patient care. Hospitals, particularly large tertiary and quaternary care centers, constitute the largest segment of end-users. Within hospitals, heparin is extensively used across various departments, including intensive care units (ICUs), cardiology, surgery (cardiac, orthopedic, general), emergency rooms, and internal medicine wards for conditions ranging from acute coronary syndromes and deep vein thrombosis to maintaining catheter patency. Their demand is consistently high due to the critical nature of patient conditions requiring immediate and continuous anticoagulation, as well as the sheer volume of surgical procedures performed. Hospitals also rely on high purity heparin for their pharmacy compounding needs and for various diagnostic procedures that require blood sample handling. The need for bulk purchasing and consistent supply makes hospitals pivotal customers for heparin manufacturers and distributors, shaping procurement strategies and supply chain capacities in the market.

Beyond hospitals, other significant end-users include clinics and ambulatory surgical centers, which cater to a growing number of outpatient procedures and less severe thrombotic conditions. These facilities often administer low molecular weight heparins (LMWHs) for thromboprophylaxis in patients undergoing minor surgeries or those who require bridge therapy before or after oral anticoagulation. Dialysis centers represent another crucial customer segment, as heparin is routinely used to prevent clotting in the extracorporeal circuits during hemodialysis sessions, ensuring the smooth and efficient removal of waste products from patients with renal failure. Diagnostic laboratories also utilize small quantities of heparin as an anticoagulant for blood collection tubes and in various laboratory assays where clot formation must be prevented to obtain accurate results. Additionally, pharmaceutical and biotechnology companies are potential customers, as they may purchase high purity heparin API for further formulation into proprietary drug products or for use in research and development of new heparin-derived therapies or drug-device combinations. The growing trend towards home healthcare also creates a segment of potential customers, as LMWHs are increasingly prescribed for self-administration in chronic conditions or post-discharge thromboprophylaxis, requiring distribution through retail pharmacies and specialized home care providers.

Furthermore, academic and research institutes represent a distinct but vital segment of potential customers. These institutions utilize high purity heparin for a broad spectrum of preclinical and clinical research activities, including studies on coagulation mechanisms, drug discovery for novel anticoagulants, tissue engineering, and cell culture applications. The demand from this segment is driven by the continuous pursuit of scientific understanding and medical innovation, requiring highly specific grades of heparin for experimental integrity. Government health organizations and public health initiatives, especially in developing countries, can also be significant customers as they aim to improve access to essential medicines and implement national programs for the prevention and treatment of thrombotic diseases. The pharmaceutical supply chain for high purity heparin also includes distributors and wholesalers who act as intermediaries, purchasing from manufacturers and then reselling to the various end-user segments. These intermediaries are crucial for efficient market penetration and ensuring widespread availability of the product across diverse geographic regions and healthcare settings, making them indirect but highly influential customers in the overall market landscape. The evolving landscape of healthcare delivery, with a shift towards value-based care and outpatient settings, continues to expand the potential customer base for high purity heparin, albeit with varying product specifications and volume requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 2.95 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Fresenius Kabi AG, Baxter International Inc., Sanofi S.A., Aspen Pharmacare Holdings Limited, Pfizer Inc., Dr. Reddy's Laboratories Ltd., Leo Pharma A/S, Opko Health Inc., B. Braun Melsungen AG, Celsus Inc., GlaxoSmithKline plc, Teva Pharmaceutical Industries Ltd., Hikma Pharmaceuticals PLC, United Therapeutics Corporation, Meitheal Pharmaceuticals, Inc., Scientific Protein Laboratories LLC (SPL), Changzhou Qianhong Bio-pharma Co., Ltd., Shenzhen Hepalink Pharmaceutical Group Co., Ltd., Pharma Action, Nanjing King-friend Biochemical Pharmaceutical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The production of high purity heparin relies on a sophisticated technology landscape that spans from initial raw material processing to advanced analytical validation, ensuring product safety, efficacy, and regulatory compliance. At the core are separation and purification technologies, predominantly various forms of chromatography. Ion-exchange chromatography, for instance, is critical for separating heparin from other glycosaminoglycans and impurities based on charge differences. Affinity chromatography, utilizing specific ligand binding, provides highly selective purification capabilities, essential for achieving the extremely high purity required for pharmaceutical applications. Membrane filtration techniques, including ultrafiltration and diafiltration, are employed for molecular weight fractionation and removal of larger contaminants, concentrating the heparin solution and further enhancing its purity profile. These technologies are continuously refined to improve yield, reduce processing time, and minimize the use of harsh chemicals, aligning with green chemistry principles and sustainable manufacturing practices, while simultaneously meeting ever-increasing regulatory demands for a safer and more consistent product profile. The precision and efficiency of these purification steps are paramount in determining the quality and therapeutic effectiveness of the final high purity heparin API.

Beyond purification, robust quality control and analytical technologies form a crucial part of the heparin market's technological backbone. Nuclear Magnetic Resonance (NMR) spectroscopy, particularly 1H-NMR and 13C-NMR, is indispensable for structural elucidation, confirming the integrity of the heparin molecule, and detecting specific contaminants or adulterants that could compromise patient safety, as famously highlighted during past contamination crises. High-Performance Liquid Chromatography (HPLC) is extensively used for molecular weight profiling and quantifying various heparin components, ensuring consistency across batches. Mass spectrometry, often coupled with liquid chromatography (LC-MS), provides highly sensitive detection of impurities, including oversulfated chondroitin sulfate (OSCS) or other harmful substances. Biological assays, such as anti-Factor Xa and anti-thrombin activity assays, are vital for measuring the anticoagulant potency of heparin preparations, directly correlating to their therapeutic efficacy. These analytical technologies are continuously advanced to provide higher resolution, faster detection times, and improved quantification limits, allowing manufacturers to meet stringent pharmacopeial requirements and regulatory guidelines (e.g., USP, EP) for impurity thresholds and biological activity, thereby safeguarding public health and maintaining confidence in the product. The integration of automation and robotics in these analytical processes further enhances throughput and reduces human error, ensuring consistency in quality assessments.

Furthermore, the technology landscape extends to innovative approaches aimed at enhancing supply chain transparency, exploring alternative sources, and optimizing manufacturing processes. Blockchain technology is emerging as a powerful tool for supply chain traceability, providing an immutable ledger of every step in the heparin production, from the animal source to the final product. This distributed ledger technology can significantly improve accountability, combat counterfeiting, and rebuild trust in a supply chain previously vulnerable to adulteration. While high purity heparin is primarily derived from animal sources, ongoing research in biotechnological methods explores the feasibility of synthetic heparin mimetics or recombinant production, which could potentially offer a more controlled and sustainable supply independent of animal sourcing. Such developments involve complex molecular biology and fermentation technologies. Process Analytical Technology (PAT) and real-time monitoring systems are increasingly being integrated into manufacturing lines. These systems use sensors and in-line analytical tools to monitor critical process parameters, enabling real-time adjustments and ensuring consistent product quality throughout the manufacturing run. This shift towards data-driven manufacturing optimizes efficiency, reduces batch variability, and significantly contributes to the overall robustness and reliability of the high purity heparin production process, ultimately benefiting both manufacturers and healthcare consumers by ensuring a safer and more dependable supply of this essential medication.

High purity heparin is a pharmaceutical-grade anticoagulant derived primarily from animal tissue, used to prevent blood clot formation. It is essential due to its rapid action, established efficacy in treating and preventing thrombotic disorders (like DVT, PE), and critical role in surgical procedures, dialysis, and maintaining catheter patency, making it a life-saving medication in various clinical settings.

The market is primarily driven by the increasing global prevalence of cardiovascular diseases and other thrombotic conditions, the rising number of surgical procedures, and the expanding aging population, which is more susceptible to such conditions. Its proven efficacy, cost-effectiveness, and established clinical guidelines further fuel its sustained demand.

Key challenges include reliance on animal-derived raw materials, leading to supply chain vulnerabilities and ethical concerns. Stringent regulatory scrutiny following past contamination crises, competition from novel oral anticoagulants (NOACs), and price volatility of raw materials also pose significant restraints on market growth and stability.

AI is influencing the market by optimizing purification processes for higher yield and purity, enhancing supply chain resilience through predictive analytics, and improving quality control by rapid detection of contaminants. AI also holds potential for personalized dosing and accelerated development of synthetic alternatives, making production more efficient and safer.

North America and Europe are mature markets with stable demand due to established healthcare systems and high disease prevalence. The Asia Pacific region is the fastest-growing, driven by expanding healthcare infrastructure, rising disposable incomes, and a large aging population. Latin America and MEA are emerging with significant growth potential as healthcare access improves.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.