ID : MRU_ 443755 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

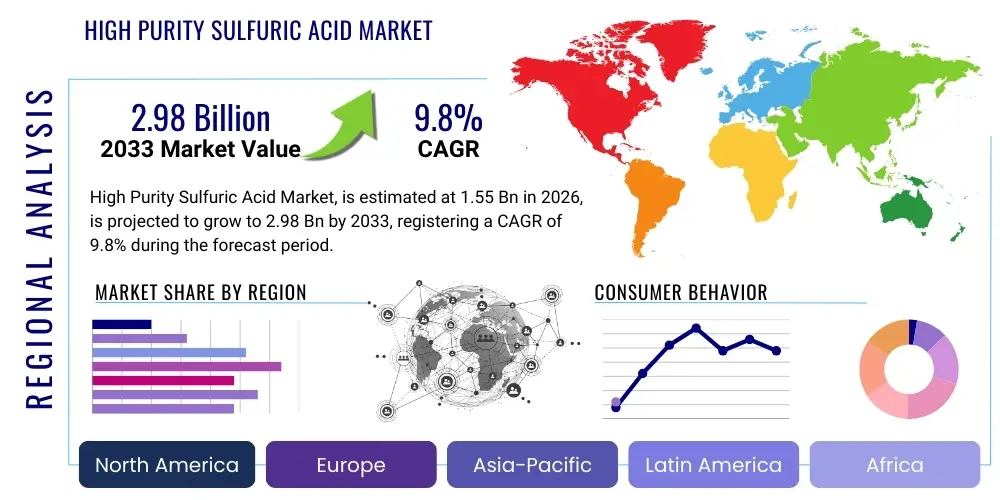

The High Purity Sulfuric Acid Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2026 and 2033. The market is estimated at USD 1.55 Billion in 2026 and is projected to reach USD 2.98 Billion by the end of the forecast period in 2033.

The High Purity Sulfuric Acid (HPSA) market encompasses sulfuric acid grades characterized by extremely low concentrations of metallic impurities and non-volatile residues, often measured in parts per trillion (ppt) or parts per billion (ppb). This specialty chemical is fundamentally distinct from industrial-grade sulfuric acid, being indispensable in highly sensitive manufacturing processes where contamination control is paramount. Its primary function involves cleaning, etching, and oxidation processes, especially within the semiconductor and electronics industries, ensuring the integrity and performance of advanced microelectronic devices.

The product, often categorized into grades like UP (Ultra Pure), UPSS (Ultra Pure Super Grade), and UPSSS (Ultra Pure Super Super Grade), serves as a crucial wet chemical in photolithography and cleaning steps for silicon wafers. The necessity for higher purity levels is directly correlated with the shrinking geometries of integrated circuits (ICs), where even minuscule particulate contamination can lead to significant yield loss and component failure. As device nodes continue to scale down below 10nm, the demand for increasingly purer HPSA grades accelerates, pushing manufacturers toward stringent quality control measures and advanced purification technologies.

Major applications driving market growth include advanced wafer processing, cleaning solutions for display panels (OLED/LCD), specialized laboratory reagents, and certain pharmaceutical processes where regulatory standards demand exceptional chemical purity. The underlying market strength is derived from global digitalization trends, the proliferation of 5G technology, the expansion of data centers, and the sustained innovation within consumer electronics, all of which rely heavily on high-quality semiconductor components manufactured using HPSA.

The High Purity Sulfuric Acid market demonstrates robust growth, primarily propelled by unprecedented global demand for semiconductors and advanced microelectronics. Business trends indicate a strategic shift towards localized manufacturing and enhanced supply chain resilience, particularly in North America and Europe, countering the historical dominance of the Asia Pacific region in production capacity. Key industry players are investing heavily in new purification technologies and expanding Grade 1, 2, and 3 production capabilities to meet the exacting specifications of sub-10nm chip manufacturing. Consolidation and strategic partnerships between chemical suppliers and major semiconductor fabrication plants (fabs) are defining the competitive landscape, aimed at securing long-term supply contracts and ensuring product customization based on specific process requirements.

Regional trends highlight the Asia Pacific (APAC) as the powerhouse of consumption, attributed to the concentration of major semiconductor manufacturers, particularly in Taiwan, South Korea, China, and Japan. However, the anticipated construction and operationalization of new mega-fabs in the United States and Germany, catalyzed by government incentives (such as the CHIPS Act and European Chips Act), are expected to significantly boost market demand in North America and Europe, diversifying the global consumption base. These regional expansions necessitate localized high-purity chemical production facilities to minimize transportation risks and maintain stringent quality controls.

Segmentation trends reveal a strong performance in the UPSS and UPSSS grades, reflecting the industry's migration toward smaller wafer dimensions and higher component density. The semiconductor application segment remains the largest revenue generator, while the display panel manufacturing segment exhibits accelerating growth due to the rollout of high-resolution OLED technology. Furthermore, the market is witnessing increased integration across the value chain, with some suppliers moving upstream into raw material sourcing and downstream into comprehensive chemical management services for end-users, enhancing operational efficiency and lowering the total cost of ownership for high-purity chemicals.

User queries regarding AI's impact on the High Purity Sulfuric Acid (HPSA) market primarily center on how artificial intelligence and machine learning (ML) optimize manufacturing consistency, predict equipment maintenance needs in ultra-clean environments, and enhance quality control to achieve sub-ppt impurity levels. There is significant interest in AI's role in mitigating contamination risks, improving process yields in semiconductor fabrication where HPSA is used, and optimizing complex supply chain logistics for hazardous, high-value chemicals. Users are keen to understand if AI can accelerate R&D for next-generation purification methods and ensure rapid identification of purity deviations that could jeopardize multi-million dollar wafer batches.

The integration of AI/ML models is transforming the operational efficiency of HPSA production facilities. These models are employed to analyze vast streams of sensor data related to temperature, flow rates, pressure, and real-time spectroscopic analysis during the purification process. By establishing baseline purity parameters and identifying minute fluctuations indicative of equipment wear or feedstock inconsistency, AI ensures proactive intervention, maintaining the chemical integrity required for advanced nodes. This predictive quality assurance significantly reduces batch rejection rates, a critical economic factor given the high cost associated with ultra-pure chemical manufacturing.

Furthermore, AI-driven process optimization is crucial for sustainability within the chemical industry. By optimizing reaction kinetics and separation techniques, ML algorithms minimize energy consumption and reduce waste generation during the extensive purification steps needed to achieve electronic grade standards. In the supply chain, AI is utilized for sophisticated demand forecasting, managing inventory of specialized containers, and optimizing routing for time-sensitive, safety-critical delivery to semiconductor fabs, thus improving overall market responsiveness and minimizing logistical risks associated with handling highly corrosive materials.

The High Purity Sulfuric Acid market is governed by powerful demand drivers rooted in the global digital infrastructure buildout, coupled with significant restraints related to stringent regulatory hurdles and high manufacturing complexity. The primary driver is the ceaseless miniaturization of semiconductor chips, which mandates the use of ultra-pure chemicals to prevent defects in smaller geometries, directly tying market growth to capital expenditure cycles in the semiconductor industry. Restraints predominantly involve the intensive capital investment required for building and maintaining contamination-free production facilities and the inherent volatility in the raw material (sulfur) market, which can impact profitability margins. Opportunities are vast, focusing on developing proprietary purification technologies (e.g., advanced ion exchange resins and metal removal systems) to meet the emerging Grade 5 and beyond specifications and capitalizing on regional localization efforts spurred by geopolitical factors.

Impact forces acting on this market are multi-faceted. Technological advancements in wet chemical processing and cleaning protocols continually push the requirements for HPSA purity higher, acting as a pivotal force. The economic impact of semiconductor fab utilization rates directly influences HPSA consumption volumes, creating a cyclical relationship between the electronics economy and the specialty chemical sector. Regulatory forces, particularly environmental and safety standards governing the handling and disposal of corrosive materials, impose significant operational costs and barriers to entry, further concentrating the market among established players capable of meeting these strict compliance mandates. Furthermore, geopolitical tensions emphasizing supply chain security are forcing major semiconductor consuming regions to incentivize domestic HPSA production, reshaping trade dynamics.

The critical impact force remains the technological roadmap set by leading semiconductor manufacturers (like TSMC, Samsung, and Intel). As these companies migrate to 3nm and 2nm nodes, the allowable impurity levels drop drastically, necessitating substantial R&D expenditure by HPSA suppliers to innovate purification techniques capable of achieving these new ultra-low thresholds. The ability of suppliers to maintain consistent quality across large volumes, coupled with reliable global distribution networks capable of handling highly corrosive and sensitive chemicals, dictates market leadership and ensures resilience against economic downturns or supply disruptions.

The High Purity Sulfuric Acid market is critically segmented based on the stringent purity grades required for specific applications, the form in which the acid is supplied, and the end-use industry. Segmentation by grade is the most decisive factor, separating standard electronic grade (SEMI Grade 1 or 2) used in less critical cleaning steps from the ultra-high purity grades (SEMI Grade 3, 4, and 5) that are mandatory for leading-edge photolithography and wafer processing. These higher grades command significant price premiums due to the intensive capital and technological input required for their purification, driving revenue concentration among technologically adept suppliers.

Further analysis of segmentation reveals that the application in wafer cleaning and etching constitutes the largest revenue share. Sulfuric Peroxide Mixture (SPM) cleaning, which utilizes HPSA and hydrogen peroxide, remains a cornerstone process in semiconductor fabrication. Growth is also accelerating in specialized segments, including advanced packaging and 3D NAND manufacturing, which require customized chemical formulations but still rely fundamentally on HPSA as a core component. The trend towards larger wafer sizes (e.g., 300mm and 450mm) also necessitates greater volumes of consistent, high-purity wet chemicals, reinforcing the volume growth within the electronic segment.

Geographically, while demand is focused on high-density manufacturing clusters, the supply side is becoming increasingly localized. Segmentation based on form includes bulk supply via specialized tankers and smaller volume packaging for highly sensitive, custom formulations, tailored to the specific consumption patterns of individual fabs. Overall, successful market participation requires a nuanced understanding of these segmented purity requirements, ensuring that production capabilities align with the evolving technological roadmaps of key consumers in the electronics manufacturing value chain.

The High Purity Sulfuric Acid value chain is distinct due to the rigorous purification steps required, fundamentally separating it from the commodity chemical supply chain. The upstream segment involves the procurement of high-quality sulfur or intermediate industrial-grade sulfuric acid, which must already meet baseline purity standards to minimize subsequent processing complexity. Key upstream activities include securing stable contracts with sulfur mining and smelting operations. The core transformation phase, or midstream, involves complex chemical processing, including catalytic oxidation, absorption, and multi-stage distillation and filtration, often utilizing advanced technologies like ion exchange or membrane separation to strip out trace metallic and organic impurities down to ppt levels.

Downstream activities focus heavily on packaging, specialized logistics, and end-user distribution. Given the extreme corrosiveness and purity sensitivity of HPSA, specialized, non-contaminating packaging (e.g., fluoropolymer-lined containers) is essential. The distribution channel is highly specialized, often relying on dedicated fleets equipped with necessary safety protocols and real-time monitoring to ensure product integrity during transit to semiconductor fabrication plants. Direct distribution is favored by major producers to maintain absolute control over quality and logistics, particularly for Grade 4 and 5 products.

Indirect distribution channels are less common but exist through authorized specialty chemical distributors, particularly for lower-grade electronic applications or in regions where the manufacturer does not maintain a direct physical presence. However, the direct sales model dominates the high-purity segment, allowing for close collaboration between the producer and the fab. This collaboration is vital for just-in-time delivery and integrated chemical management services, where the supplier manages the inventory and disposal/recycling of spent acid, thereby closing the loop and adding significant value to the overall supply chain offering.

The primary and most demanding customer segment for High Purity Sulfuric Acid resides within the semiconductor manufacturing industry, specifically integrated device manufacturers (IDMs) and pure-play foundries. These entities are the largest volume consumers, utilizing HPSA in critical cleaning phases during front-end-of-line (FEOL) and back-end-of-line (BEOL) processing to remove organic residues, particles, and metallic contaminants from silicon wafers. Their purchasing decisions are driven almost exclusively by purity specifications, consistency, and reliability of supply, often demanding multi-year, customized supply agreements.

The second major consumer group includes manufacturers of flat panel displays (FPDs), encompassing companies producing LCD, OLED, and next-generation display technologies. In this sector, HPSA is employed for etching and cleaning substrates to ensure pixel uniformity and device clarity. While the purity requirements may be slightly less stringent than for advanced semiconductor nodes, the volume demands are substantial, tied closely to global consumer electronics cycles and the proliferation of high-end smart devices and large format TVs.

A burgeoning segment of potential customers includes specialized manufacturers in the advanced materials and renewable energy sectors, particularly those involved in high-efficiency solar cells and advanced lithium-ion battery components. In these applications, HPSA is needed for pre-treatment and cleaning processes to ensure optimal material interface quality. Furthermore, regulated specialty chemical laboratories and certain pharmaceutical manufacturers that require ultra-clean reagents for sensitive synthesis and analysis procedures also represent niche, high-value end-users, demanding the highest level of regulatory compliance and product certification.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.55 Billion |

| Market Forecast in 2033 | USD 2.98 Billion |

| Growth Rate | 9.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Kanto Chemical Co., Inc., Moses Lake Industries (TAMA Chemicals), Solvay S.A., Linde plc, Merck KGaA, Avantor, Inc., Asia Union Electronic Chemicals Corp. (AUECC), Mitsubishi Chemical Corporation, PVS Chemicals, Inc., Honeywell International Inc., Iwatani Corporation, INEOS Enterprises, Stella Chemifa Corporation, Trans-Atlantic Chemicals Inc., Chemtrade Logistics Income Fund, CXDC (China Xinneng Development), Cofco (China National Cereals, Oils and Foodstuffs Corporation), FujiFilm Holdings Corporation, Air Liquide S.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The High Purity Sulfuric Acid manufacturing technology landscape is dominated by sophisticated purification techniques aimed at achieving increasingly lower metal and particulate impurity counts. The core technology involves the thermal decomposition and fractional distillation of industrial-grade sulfuric acid, often followed by catalytic oxidation and subsequent absorption. However, the differentiation lies in the secondary and tertiary purification steps. Modern facilities rely heavily on advanced, multi-stage distillation systems that operate under vacuum to lower boiling points and prevent thermal degradation, ensuring volatile organic compounds and other impurities are effectively separated.

The key innovation driver is the integration of proprietary post-distillation purification methods, specifically targeted at removing stubborn metallic ions (such as Fe, Cu, Ni, and Zn) down to single-digit ppt levels. This often involves highly specialized ion exchange resins, advanced filtration membranes (ultrafiltration and nanofiltration), and proprietary chemical chelating agents introduced in the final cleaning loops. Continuous, closed-loop monitoring systems utilizing high-resolution analytical instruments (like ICP-MS) are essential, providing real-time feedback to ensure the product consistently meets the Grade 5 (UPSSS) specification before packaging.

Furthermore, technology related to storage and transport is equally critical. The use of specialized materials for piping, storage tanks, and transportation vessels, such as high-density polyethylene (HDPE) and fluoropolymers (e.g., PFA, PTFE), is mandatory to prevent leaching of contaminants back into the ultra-pure acid. The shift toward higher concentration HPSA (typically 96-98%) also requires precise process control to minimize water content, which can introduce contaminants, and manage the highly exothermic reactions safely throughout the production cycle.

The regional analysis of the High Purity Sulfuric Acid market clearly delineates two phases: consumption dominance and production localization. The Asia Pacific (APAC) region currently holds the largest market share and is projected to maintain its position as the dominant consumption hub throughout the forecast period due to the massive concentration of semiconductor foundries, memory chip manufacturers, and display panel production facilities in countries like China, Taiwan, South Korea, and Japan. The ongoing expansion of manufacturing capacity in these areas, fueled by government industrial policies, ensures sustained, high-volume demand for Grade 3 and Grade 4 HPSA.

North America is anticipated to exhibit the fastest growth rate, a trend largely attributable to substantial government intervention via the CHIPS and Science Act, which is funneling billions into establishing new, advanced semiconductor manufacturing facilities (fabs) across the US. This regional shift requires localized and reliable sources of ultra-pure process chemicals like HPSA to support domestic production goals, driving significant capital expenditure in new chemical manufacturing plants, often in proximity to the new fab clusters in Arizona, Ohio, and Texas.

Europe, driven by the European Chips Act and existing industrial strength in Germany and Ireland, is also demonstrating accelerating demand, albeit starting from a smaller base compared to APAC. European initiatives focus on ensuring technological sovereignty and securing domestic supply for strategic industries. The Middle East and Africa (MEA) and Latin America (LATAM) currently represent smaller markets, primarily driven by specialized industrial or laboratory needs, but are expected to see moderate growth linked to emerging regional electronics assembly and pharmaceutical sectors.

HPSA is predominantly used in critical wet chemical processing steps within semiconductor manufacturing, specifically for cleaning silicon wafers. It is a key component in Sulfuric Peroxide Mixture (SPM) cleaning solutions, essential for removing organic residues, metallic impurities, and particulate contaminants to maximize microchip yield and performance.

Purity grades are typically defined by international standards (like SEMI grades 1 through 5, or UP, UPSS, UPSSS) based on the maximum allowable concentration of metallic impurities, measured in parts per billion (ppb) or parts per trillion (ppt). These grades are crucial because as semiconductor feature sizes shrink (e.g., below 5nm), even minute contamination can cause defects, necessitating Grade 4 or Grade 5 HPSA.

The Asia Pacific (APAC) region currently leads global demand for HPSA due to the dense concentration of global semiconductor foundries (fabs) and advanced display panel manufacturing plants in countries such as Taiwan, South Korea, and China. This region is the primary consumption engine for electronic-grade wet chemicals.

The most significant restraint is the incredibly high capital investment and technical complexity required to build and maintain ultra-clean production facilities capable of consistently delivering sub-ppt purity levels. Stringent regulatory hurdles related to handling hazardous, corrosive materials also increase operational expenditures substantially.

The market is reacting by undertaking significant localization efforts. Driven by geopolitical pressures and government incentives (like the US CHIPS Act), manufacturers are expanding capacity in North America and Europe to ensure regional supply security for key semiconductor fabrication clusters, diversifying the supply base away from traditional Asian hubs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.