ID : MRU_ 442472 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

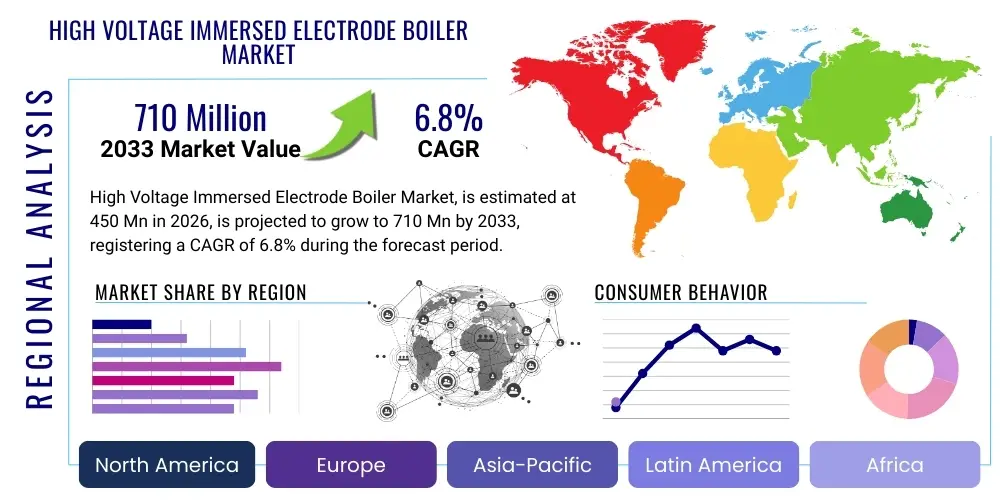

The High Voltage Immersed Electrode Boiler Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 450 million in 2026 and is projected to reach USD 710 million by the end of the forecast period in 2033.

This robust expansion is primarily driven by the global imperative for decarbonization and the increasing integration of intermittent renewable energy sources into the electrical grid. High voltage electrode boilers (HVEBs) provide a highly efficient, scalable solution for utilizing surplus renewable electricity (Power-to-Heat, P2H) to generate industrial process steam or district heating, thus offering essential grid flexibility and thermal storage capabilities. The market valuation reflects significant investment in large-scale industrial applications and utility-managed district heating networks, particularly across Europe and North America where stringent climate policies accelerate the shift away from fossil-fuel-based heating.

The High Voltage Immersed Electrode Boiler Market encompasses systems designed to convert electrical energy directly into thermal energy using the resistance of water (the electrolyte) as current passes between submerged electrodes. These boilers operate efficiently at medium to high voltages (typically above 6 kV) and are predominantly employed in large industrial facilities, utilities, and district heating systems requiring high capacity steam or hot water production. Unlike traditional fuel-fired boilers, HVEBs offer near-instantaneous response times, zero on-site emissions, and exceptionally high thermal efficiency, often exceeding 99%, making them a cornerstone technology in the industrial energy transition and grid balancing initiatives.

Key applications of these advanced boilers span heavy industries such as pulp and paper, chemicals, food and beverage processing, and large-scale urban district heating infrastructure. The product description emphasizes robustness, safety, and operational flexibility, allowing seamless integration with variable renewable energy generation profiles, such as wind and solar power. Major benefits include reduced carbon footprints, lower operational costs due to favorable electricity pricing during off-peak or surplus renewable periods, and significantly simplified regulatory compliance regarding emissions. These systems are crucial for achieving sustainability targets in sectors historically reliant on natural gas or coal for thermal energy.

Driving factors for the market include government incentives supporting electrification and P2H strategies, escalating carbon taxes making fossil fuels uneconomical, and the increasing need for reliable thermal energy storage solutions. Furthermore, advancements in smart grid technologies and utility demand response programs enhance the economic viability of utilizing these high-power consumption devices. The inherent scalability of immersed electrode technology allows deployment across diverse industrial sizes and operational requirements, cementing its role as a foundational technology for industrial decarbonization globally.

The High Voltage Immersed Electrode Boiler Market is poised for significant expansion, driven fundamentally by the convergence of energy transition mandates and industrial operational efficiency demands. Business trends indicate a heightened focus on integrating these boilers with utility-scale Battery Energy Storage Systems (BESS) and sophisticated Energy Management Systems (EMS) to maximize economic returns through arbitrage and participation in ancillary grid services. Manufacturers are increasingly offering modular and containerized solutions, simplifying installation and reducing commissioning times for complex industrial retrofits. Furthermore, strategic partnerships between boiler manufacturers and renewable energy developers are becoming common, targeting fully integrated green heat solutions for large industrial consumers.

Regional trends highlight Europe, particularly the Nordic countries and Germany, as the leading adopters, spurred by mature district heating infrastructure and aggressive decarbonization roadmaps. North America is rapidly accelerating adoption, driven by policy incentives like the Inflation Reduction Act (IRA) in the US, favoring electrification and renewable integration in the industrial sector. Asia Pacific (APAC) represents a burgeoning market, focusing primarily on large industrial complexes in China and India seeking sustainable alternatives to coal-fired processes, though regulatory frameworks supporting P2H require further development compared to Western markets.

Segment trends emphasize the dominance of the Steam segment due to pervasive industrial reliance on high-pressure steam for processes, followed closely by the Hot Water/District Heating segment, reflecting significant utility investments. From an end-user perspective, the Chemical and Petrochemical industry and Pulp and Paper sectors remain the largest consumers, given their immense and constant demand for process heat. The market is also experiencing a notable trend toward digital twin technology integration and remote diagnostics capabilities, enhancing boiler reliability and predictive maintenance schedules, further improving the overall value proposition for end-users seeking maximal uptime.

Common user questions regarding AI’s influence typically revolve around optimizing operational efficiency, predicting maintenance needs, and maximizing profitability through intelligent energy arbitrage. Users frequently inquire about how AI can manage the complex interaction between volatile electricity prices, renewable energy availability, and industrial heat demand fluctuations. Key concerns include data security, the accuracy of predictive models in real-time environments, and the necessary integration depth with existing plant control systems. The overarching expectation is that AI will transform HVEBs from simple heat generators into sophisticated grid assets capable of autonomous, profit-driven operation within dynamic energy markets.

AI's primary role in the HVEB market is optimization. Advanced machine learning algorithms analyze historical operational data alongside real-time inputs such as spot electricity prices, intraday market forecasts, renewable generation curves, and specific industrial thermal requirements. This analysis allows the boiler system to autonomously determine the optimal operating schedule, maximizing the utilization of low-cost renewable energy while ensuring mandated steam or hot water supply is met. This level of predictive control significantly enhances the economic viability of the P2H strategy, allowing industrial users to effectively participate in demand response programs and earn revenue from grid stabilization services.

Furthermore, AI-driven diagnostics revolutionize maintenance practices. By continuously monitoring critical operational parameters, including water conductivity, electrode wear rates, pressure transients, and insulation resistance, AI systems can accurately predict potential failures before they occur. This transition from scheduled maintenance to true predictive maintenance dramatically reduces downtime, lowers spare parts inventory costs, and extends the operational life of the high-voltage components. The application of deep learning models to sensor data ensures unparalleled precision in identifying anomalies, enhancing both safety and system reliability, which is paramount in high-voltage industrial environments.

The High Voltage Immersed Electrode Boiler Market is significantly influenced by powerful global drivers, notably the urgent need for industrial decarbonization and the increasing penetration of volatile renewable energy sources requiring flexible load management. Restraints primarily center on the substantial initial capital investment required for high-voltage infrastructure and the lack of comprehensive P2H regulatory frameworks in several major industrial regions. Opportunities abound in the burgeoning hydrogen economy (where excess electricity can be stored as heat or hydrogen) and the expansion of urban district heating networks. These forces create a dynamic environment where regulatory support is critical for overcoming investment hurdles and unlocking the full potential of P2H technology.

Market drivers include stringent governmental mandates, such as the EU’s Green Deal and various national carbon neutrality goals, compelling industries to seek non-fossil fuel heating solutions. The inherent efficiency (near 100%) and operational cleanliness of HVEBs provide a clear compliance pathway. Furthermore, the economic driver of minimizing exposure to volatile natural gas prices, especially following geopolitical instability, makes fixed-cost electricity consumption an attractive alternative. As grids become greener, the operational carbon intensity of HVEBs diminishes, providing a future-proof thermal energy solution that aligns with long-term ESG strategies of major corporations.

Restraints include the dependency on electricity grid capacity, which may necessitate costly grid upgrades for high-power installations, and the prevailing perception of high upfront costs compared to mature natural gas boiler systems. Impact forces are predominantly regulatory and technological; the impact of rapidly declining renewable energy costs dramatically improves the economics of HVEBs, while evolving global standards for grid resilience and smart energy management dictate the pace and direction of market adoption. The continuous development of superconducting materials and optimized control systems acts as a strong positive impact force, enhancing both the safety and long-term reliability of these high-power installations.

The High Voltage Immersed Electrode Boiler market segmentation is critical for understanding market dynamics and targeting specific customer needs based on output media, operating voltage, and end-user application. The primary segmentation distinguishes between steam boilers, hot water boilers, and dual-purpose systems, reflecting the diverse thermal requirements of industrial and municipal sectors. Further granularity is provided by the segmentation based on operating voltage, generally classifying units into medium voltage (MV) and true high voltage (HV) systems, which correlates directly with the required capacity and connection point to the utility grid.

The segmentation by capacity is perhaps the most defining characteristic, ranging from smaller industrial units (under 20 MW) to massive utility-scale installations (exceeding 100 MW) used for large district heating schemes or large petrochemical facilities. The segmentation highlights the versatility of the technology, capable of serving everything from discrete manufacturing processes to entire municipal heating grids. The industrial segmentation further refines market focus, isolating high-growth sectors such as pharmaceuticals, where cleanliness is paramount, and pulp and paper, which requires enormous quantities of low-cost steam.

This detailed market segmentation allows stakeholders, including manufacturers, investors, and policymakers, to accurately assess potential areas of investment and policy intervention. For instance, the hot water segment is strongly concentrated in European countries with established district heating, whereas the steam segment sees broader global adoption in process industries. Analyzing these segments reveals that the strategic integration of HVEBs with thermal storage (e.g., pressurized water tanks) is a key feature sought by end-users in the highest capacity segment, enabling further decoupling of electricity consumption from heat demand schedules.

The value chain for the High Voltage Immersed Electrode Boiler market begins with raw material sourcing and specialized component manufacturing (upstream analysis), progresses through design and fabrication (midstream), and culminates in distribution, installation, and after-sales service (downstream analysis). Upstream activities are critical, involving sourcing high-quality, corrosion-resistant electrode materials (e.g., nickel alloys or proprietary steels), specialized electrical insulation components suitable for high voltages, and robust pressure vessel steel. The dependence on high-purity components for electrical safety and longevity makes supply chain resilience and material quality assurance paramount. Furthermore, specialized transformer and switching gear manufacturers are key upstream suppliers, dictating the overall high-voltage system performance.

The midstream phase involves complex engineering design tailored to specific customer thermal and electrical requirements, followed by rigorous pressure vessel manufacturing compliant with international standards (ASME, PED). Key manufacturers focus on optimizing the electrode geometry and boiler vessel layout to maximize heat transfer efficiency and minimize standing losses. Direct distribution channels are prevalent, especially for large, customized projects, where the manufacturer directly manages the sales, engineering, and installation process due to the complexity and high value of the equipment. This direct engagement ensures technical specifications are precisely met and allows for comprehensive integration with the client’s existing utility infrastructure.

Downstream activities include specialized installation services, requiring highly skilled technicians proficient in high-voltage electrical connections and high-pressure steam systems. After-sales service, maintenance, and system optimization constitute a significant revenue stream (downstream analysis). Indirect distribution, through engineering procurement and construction (EPC) firms or regional industrial integrators, is utilized for standard or smaller capacity installations, particularly in new geographical markets where the manufacturer lacks a direct operational footprint. The overall value chain is characterized by high technical expertise at every stage, emphasizing quality control and safety standards necessary for operating high-pressure, high-voltage equipment.

Potential customers for High Voltage Immersed Electrode Boilers are predominantly large-scale industrial entities and utility providers characterized by high, consistent demand for thermal energy and access to high-capacity electrical substations. These end-users are typically motivated by dual objectives: achieving significant reductions in operational carbon emissions and capitalizing on the economic opportunity presented by time-of-use electricity tariffs or renewable energy oversupply. Buyers are often the energy management or facilities departments within these large organizations, necessitating solutions that are not only efficient but also compliant with stringent industry safety and operational regulations, driving demand for robust and certified systems.

The largest segment of buyers includes global utility companies and municipal entities managing centralized District Heating (DH) networks. These customers utilize HVEBs as massive thermal batteries, converting surplus wind or solar power into storable hot water, effectively buffering the electricity grid. Their purchasing decisions are heavily influenced by government incentives, long-term infrastructure planning, and the need for reliable, maintenance-friendly heat generation sources. These projects often involve multi-year procurement cycles and require proven track records in high-capacity boiler deployment, emphasizing long-term reliability over marginal cost savings.

Industrial end-users, encompassing the chemical, petrochemical, pulp and paper, and large-scale food processing sectors, represent the other major buying group. These industries have intense, continuous process heat needs, often requiring high-pressure steam (e.g., 10-40 bar). For these buyers, the key metrics are the total cost of ownership (TCO) compared to fossil fuel alternatives, the integration capability with existing steam distribution infrastructure, and the ability of the boiler to handle fluctuations in thermal load without compromising product quality. The strategic advantage of HVEBs is their ability to leverage corporate Power Purchase Agreements (PPAs) for renewable electricity, aligning their operations with sustainability mandates while stabilizing energy inputs.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 million |

| Market Forecast in 2033 | USD 710 million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | PARAT Halvorsen AS, CERTUSS Dampfautomaten GmbH & Co. KG, AC Boiler SpA, SIEMENS AG, Vattenfall AB, ABB Ltd., Danstoker A/S, Thermon Manufacturing Co., STIEBEL ELTRON GmbH & Co. KG, Cochrane Engineering Ltd., Chromalox, Inc., Precision Boilers, Konutherm, Viessmann Group, Indeck Power Equipment Co., Cleaver-Brooks, Inc., Bosch Industriekessel GmbH, Fulton Boiler Works, Inc., Babcock & Wilcox Enterprises, Inc., Miura America Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the High Voltage Immersed Electrode Boiler market is defined by continuous innovation aimed at enhancing operational flexibility, safety, and integration capabilities within complex industrial and utility environments. A core technological focus involves the material science of the electrodes and the associated insulation systems. Manufacturers are developing proprietary electrode alloys that resist corrosion and scaling even under varying water quality conditions and high current densities, ensuring prolonged operational life and consistent heating performance. Advanced control systems utilizing Programmable Logic Controllers (PLCs) and Supervisory Control and Data Acquisition (SCADA) systems are standard, allowing for precise control over steam pressure, temperature, and electricity consumption in real-time, often remotely.

Furthermore, significant technological development is concentrated on enhancing the integration of HVEBs with external energy systems, particularly thermal energy storage (TES) systems. Technologies such as stratified hot water accumulators are crucial components, allowing the boiler to run efficiently during periods of low-cost electricity and store the resulting heat for later use, effectively maximizing the return on investment. The interface technology facilitates rapid ramp-up and ramp-down rates, crucial for participating effectively in fast-response grid balancing markets. This responsiveness is a key differentiator compared to legacy fossil fuel boilers, requiring sophisticated modulation capabilities that are inherent in modern electrode boiler designs.

The safety and regulatory technology stack is also evolving rapidly. High-voltage power conditioning equipment, including sophisticated circuit breakers and protection relays, is standard, ensuring safe operation at grid voltages up to 69 kV. Remote monitoring and IoT integration are standard features, allowing for continuous performance validation and proactive fault detection, often utilizing cloud-based data analytics platforms. The convergence of high-voltage electrical engineering with advanced thermodynamic control and digital connectivity defines the cutting-edge of HVEB technology, driving higher standards for efficiency, reliability, and grid compatibility. The focus is moving towards autonomous systems that require minimal human intervention for optimal energy management.

Europe holds the dominant position in the High Voltage Immersed Electrode Boiler market, driven by comprehensive regulatory frameworks designed to phase out fossil fuel use in heating and power generation. Countries like Denmark, Sweden, and Finland, with extensive, mature district heating networks, utilize HVEBs as primary assets for grid balancing (Power-to-Heat). The region benefits from high penetration of wind and solar power, leading to significant periods of surplus electricity that make the P2H economic case highly compelling. Government incentives, coupled with high carbon pricing mechanisms through the EU Emission Trading System (ETS), accelerate the industrial shift. Germany, focusing on industrial electrification and the integration of large-scale thermal storage, is a key growth hub. The market demand here is characterized by high-capacity units (50 MW+) used by utilities and major industrial campuses aiming for complete carbon neutrality in thermal operations. The regional emphasis on energy independence further bolsters investment in electrification technologies.

The regulatory environment in Northern and Western Europe is exceptionally favorable, often subsidizing grid connection costs for high-load flexibility devices. This support minimizes one of the primary restraints—the initial capital expenditure. Furthermore, the established expertise of local EPC firms and specialized manufacturers in handling high-voltage industrial installations reduces project risk. Demand in Eastern Europe is also rising as modernization efforts focus on replacing inefficient, coal-dependent heating plants with clean, grid-connected solutions. This consistent demand, supported by robust infrastructure and favorable pricing volatility, secures Europe's position as the primary market for advanced HVEB technology throughout the forecast period.

North America, particularly the United States and Canada, is experiencing rapid acceleration in HVEB adoption. This growth is strongly supported by federal incentives, most notably the U.S. Inflation Reduction Act (IRA), which provides substantial tax credits for projects utilizing clean energy technologies for industrial processes. Canadian provinces, such as Quebec and British Columbia, benefit from abundant, low-cost hydroelectric power, making the economics of electric boilers highly attractive compared to natural gas. The market is concentrated in high-demand industrial corridors, including the Gulf Coast petrochemical industry and the pulp and paper mills in the Pacific Northwest.

The North American market is characterized by large, custom-engineered steam boilers required for high-pressure industrial applications. Unlike Europe, the focus here is less on district heating and more on direct industrial process heat substitution. Challenges include diverse state-level regulatory landscapes and the necessity for significant upgrades to local transmission and distribution infrastructure to handle multi-megawatt electrical loads. However, the ongoing expansion of renewable energy generation capacity across the Midwest and Texas creates frequent periods of low-cost electricity, significantly improving the profitability of utilizing HVEBs for large industrial consumers seeking energy cost stability and reduced emissions compliance costs. Manufacturers are aggressively forming localized partnerships to manage installation and integration complexity.

The APAC region represents a high-potential, rapidly emerging market for HVEBs, although adoption rates lag behind Europe and North America. Growth is primarily concentrated in rapidly industrializing nations such as China, India, South Korea, and Japan. These countries face immense pressure to curb industrial air pollution and carbon emissions, necessitating a shift away from coal and heavy oil boilers. China, with its massive industrial base, is investing heavily in utility-scale electrification projects and modernizing urban heating systems, offering significant opportunities for HVEB deployment, particularly in coastal manufacturing zones.

However, the APAC market faces constraints related to the maturity of smart grid infrastructure and, in many areas, the continued dominance of cheaper, though highly polluting, fossil fuels. Adoption is currently spearheaded by multinational corporations operating in the region who enforce global sustainability standards (ESG initiatives). Key demand segments include electronics manufacturing, large pharmaceutical production, and specialized chemical processing requiring clean, precise thermal input. As renewable energy penetration (especially solar) increases across Southeast Asia and India, the economic rationale for P2H will strengthen, paving the way for wider acceptance of high-voltage electric thermal solutions, supported by technology transfer and localized manufacturing partnerships.

The MEA and Latin America markets are characterized by niche, project-specific deployment, primarily driven by mining, petrochemicals, and unique regional energy scenarios. In Latin America, countries with substantial hydroelectric resources (e.g., Brazil, Chile) offer compelling cases for HVEB adoption in industrial parks where electricity is highly reliable and competitively priced. The focus here is on achieving energy security and stable operating costs rather than solely decarbonization mandates, which may be less stringent than in OECD nations.

In the Middle East, while hydrocarbon reliance is high, there is growing interest in HVEBs for decarbonizing ancillary services within large desalination plants and oil/gas processing facilities. These highly regulated environments prioritize safety and reliability. Africa's market remains nascent, focused mainly on specific industrial zones (e.g., South African mining, North African petrochemicals) where reliable high-voltage power is accessible. Market penetration is slow due to fragmented grid infrastructure and prevailing capital constraints, requiring significant governmental or multinational corporate investment to unlock meaningful growth.

The primary economic driver is the ability to leverage low-cost, surplus renewable electricity (Power-to-Heat strategy) during periods of high generation and low demand. HVEBs enable industrial users and utilities to reduce reliance on volatile natural gas prices, utilize grid flexibility payments, and achieve significant operational cost savings through energy arbitrage.

HVEBs are fundamentally safer than traditional fired boilers because they eliminate combustion risk. They operate solely on electricity, removing the need for fuel storage, piping, burners, and associated explosion hazards. Modern systems incorporate advanced high-voltage protection and interlocking systems, ensuring highly controlled and safe industrial operation.

Industrial HVEB installations typically operate at medium voltages (6 kV to 25 kV) or high voltages (above 25 kV, sometimes up to 69 kV), directly connecting to industrial or utility substations. Capacity ranges widely, generally starting from 5 MW for smaller industrial applications and extending up to 150 MW or more for large utility-scale district heating or major industrial complexes like petrochemical refineries.

TES is crucial for decoupling electricity consumption from thermal demand. By storing the heat generated during low-electricity-cost periods (e.g., overnight renewable surplus) in large accumulator tanks, HVEBs can maximize their economic efficiency, ensuring the continuous supply of steam or hot water even when electricity prices are high or renewable generation is low.

Currently, the largest consumers are the Pulp and Paper, Chemical and Petrochemical industries, and Municipal District Heating Utilities, all requiring vast, consistent sources of process heat or steam. Future growth is expected particularly in Pharmaceuticals, Food and Beverage processing, and specialized manufacturing driven by stringent decarbonization targets and the need for extremely clean thermal sources.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.