ID : MRU_ 442642 | Date : Feb, 2026 | Pages : 253 | Region : Global | Publisher : MRU

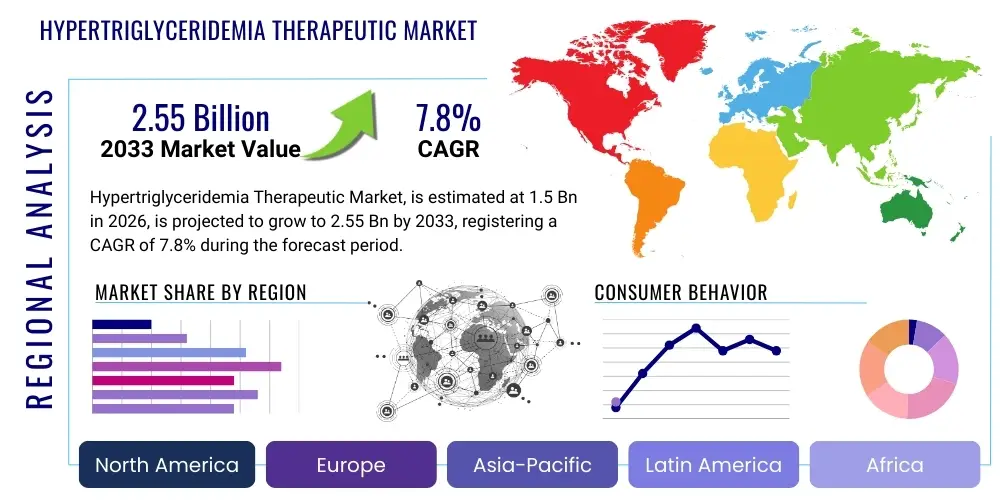

The Hypertriglyceridemia Therapeutic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 2.55 Billion by the end of the forecast period in 2033. This growth trajectory is significantly influenced by the escalating global prevalence of lifestyle-related metabolic disorders, including obesity, diabetes mellitus, and metabolic syndrome, all of which are primary drivers of elevated triglyceride levels. Furthermore, continuous advancements in lipid-lowering pharmacological agents, specifically the introduction of highly effective and targeted novel therapies, are contributing substantially to market expansion, enabling better management of high-risk patient populations.

Hypertriglyceridemia, characterized by abnormally elevated levels of triglycerides in the bloodstream, is a critical risk factor for cardiovascular diseases (CVD) and acute pancreatitis. The Hypertriglyceridemia Therapeutic Market encompasses a wide spectrum of pharmacological and nutritional interventions aimed at lowering these lipid levels and mitigating associated health risks. Key product descriptions within this market include established treatments such as fibrates (e.g., fenofibrate, gemfibrozil), niacin (nicotinic acid), high-dose omega-3 fatty acid preparations, and increasingly, novel therapeutics like antisense oligonucleotides (ASOs) and lipoprotein lipase enhancers. These treatments primarily target the reduction of circulating very-low-density lipoproteins (VLDL) and chylomicrons.

Major applications of these therapeutic agents are centered on primary and secondary prevention strategies. Primary prevention involves treating individuals with isolated, severe hypertriglyceridemia to prevent pancreatitis, while secondary prevention focuses on reducing residual cardiovascular risk in patients already undergoing statin therapy for hypercholesterolemia. The benefits associated with effective treatment include a marked reduction in the incidence of fatal and non-fatal cardiovascular events, a lower risk of acute pancreatitis, and overall improvement in patient quality of life. The increasing awareness among healthcare providers regarding the independent prognostic value of hypertriglyceridemia, even in normocholesterolemic patients, is widening the treatment eligibility pool and consequently boosting market dynamics.

Driving factors for this market are multi-faceted. The foremost factor is the dramatic increase in the global incidence of metabolic syndrome, driven by sedentary lifestyles and poor dietary habits in developed and developing nations alike. This epidemiological shift necessitates aggressive lipid management strategies. Furthermore, the advent of proprietary, highly purified omega-3 formulations, which demonstrate superior efficacy and better side-effect profiles compared to generic fish oil supplements, has reinvigorated interest in this class of drugs. Regulatory endorsements and favorable clinical trial outcomes proving the cardiovascular risk reduction benefit of these purified agents are crucial catalysts for market growth, encouraging greater clinical adoption and payer reimbursement.

The Hypertriglyceridemia Therapeutic Market is currently experiencing a profound transition driven by evolving treatment guidelines and the introduction of advanced pharmacological modalities. Business trends indicate a significant shift in research and development investment away from traditional fibrates and niacin towards high-potency, targeted biologic therapies such as antisense oligonucleotides and monoclonal antibodies aimed at specific metabolic pathways (e.g., ANGPTL3 inhibition). This investment is catalyzed by the search for treatments that offer superior efficacy and reduced interaction complexity compared to existing oral agents. Key strategic movements include mergers, acquisitions, and licensing agreements between large pharmaceutical firms and specialized biotechnology companies, particularly those developing gene-silencing therapies for genetic forms of hypertriglyceridemia.

From a regional perspective, North America maintains market dominance, primarily attributable to high healthcare expenditure, established clinical guidelines promoting early and aggressive lipid management, and rapid market access for premium-priced novel therapeutics. However, the Asia Pacific region is poised for the most rapid growth, driven by an expanding middle class adopting Westernized diets, increasing prevalence of diabetes, and improving healthcare infrastructure facilitating access to diagnostic and therapeutic resources. European markets are characterized by stringent health technology assessment (HTA) procedures, leading to slower but more systematic adoption of newer, higher-cost treatments, emphasizing cost-effectiveness data.

Segment trends reveal that the Omega-3 Fatty Acids category, particularly prescription-grade icosapent ethyl, is dominating the revenue share due to robust clinical evidence demonstrating cardiovascular risk reduction beyond simple triglyceride lowering. Conversely, the segment of novel therapeutics, while currently smaller in volume, is projected to exhibit the highest Compound Annual Growth Rate (CAGR) as pipelines mature and agents like volanesorsen and other targeted injectables gain regulatory approval for specific severe patient populations. The distribution channel analysis highlights the continued significance of retail and specialty pharmacies, reflecting the outpatient nature of hypertriglyceridemia management, although hospital pharmacies remain crucial for the initiation of expensive injectable or infused therapies for severe familial cases.

Common user questions regarding the impact of Artificial Intelligence (AI) in the hypertriglyceridemia therapeutics space frequently revolve around its potential to revolutionize drug target identification, optimize clinical trial design, and enhance personalized treatment protocols. Users are keen to understand how AI algorithms can screen large genomic and proteomic datasets to uncover novel lipid metabolism pathways that are currently untargeted by existing drugs. Furthermore, significant interest lies in AI’s capability to predict patient response to various lipid-lowering agents, thereby minimizing trial-and-error treatment approaches and reducing healthcare costs. Concerns often center on the validation and transparency of AI-driven drug discovery outputs and the ethical implications of using predictive models for patient stratification, especially in vulnerable populations with severe or familial forms of the disorder. The consensus expectation is that AI will streamline R&D cycles, potentially leading to faster market entry for more effective and safer therapeutic options.

The Hypertriglyceridemia Therapeutic Market is shaped by a complex interplay of Drivers, Restraints, and Opportunities, collectively forming the key Impact Forces. A major driver is the accelerating epidemic of non-communicable diseases (NCDs), particularly Type 2 Diabetes Mellitus and obesity, which serve as primary underlying causes of secondary hypertriglyceridemia. Global population aging also contributes to the disease burden, as lipid metabolism often deteriorates with age, necessitating therapeutic intervention. Furthermore, the publication of compelling outcomes data from large-scale cardiovascular outcome trials (CVOTs) involving high-dose Omega-3 derivatives has established a new standard of care, driving prescribing behavior towards proven risk-reducing agents.

However, the market faces significant restraints. High drug costs, particularly associated with novel agents like antisense oligonucleotides, limit access and adherence, especially in healthcare systems sensitive to budget constraints. Poor patient adherence to chronic medication regimens, a persistent challenge in preventive cardiology, often compromises therapeutic efficacy, hindering optimal market performance. Additionally, the fragmented and often delayed diagnosis of moderate hypertriglyceridemia, which is frequently asymptomatic until severe complications arise, restricts the early application of therapeutics, thereby limiting the total addressable market in earlier disease stages.

Opportunities within this therapeutic landscape are substantial, primarily driven by innovations in genetic and precision medicine. The development of gene therapy and gene-editing techniques targeting Mendelian disorders of lipid metabolism (such as familial chylomicronemia syndrome, which causes severe hypertriglyceridemia) represents a paradigm shift toward curative treatments. Furthermore, the expansive emerging markets in Asia and Latin America, characterized by rapid urbanization and increasing disposable income, present untapped potential for branded lipid-lowering drugs. Strategic alliances focusing on combination therapies that simultaneously address both hypercholesterolemia and hypertriglyceridemia offer enhanced therapeutic profiles and promising commercial avenues.

The Hypertriglyceridemia Therapeutic Market is strategically segmented across several critical dimensions, including the type of Drug Class, the Route of Administration, and the Distribution Channel. Drug class segmentation is fundamental, reflecting the diverse pharmacological mechanisms employed to lower circulating triglycerides. This segmentation highlights the competitive landscape between established generic therapies and proprietary, high-efficacy formulations. The route of administration dictates patient compliance and accessibility, distinguishing between widely used oral agents and specialized injectable treatments reserved for severe or refractory cases. Analyzing the distribution channels reveals the primary points of dispensing and their influence on market pricing and accessibility, with hospital and retail pharmacies forming the core structure.

The Drug Class segment currently sees dominance from Omega-3 Fatty Acids, specifically high-purity, prescription-strength formulations, following definitive clinical evidence of their cardiovascular benefits. Fibrates maintain a stable, albeit slower, growth trajectory, primarily utilized in countries with cost-sensitive healthcare systems or in combination therapies. The fastest-growing segment is Novel Therapies, encompassing agents like ASOs (e.g., volanesorsen) and small interfering RNAs (siRNA), which offer unprecedented efficacy by directly interfering with genetic expression pathways crucial for triglyceride synthesis, addressing previously unmet clinical needs in high-risk patients. Market dynamics within these segments are continuously reshaped by pipeline progression and shifts in international clinical guidelines.

The value chain for the Hypertriglyceridemia Therapeutic Market begins with rigorous Upstream Analysis centered on R&D and Active Pharmaceutical Ingredient (API) manufacturing. Research activities are intensely focused on discovering new molecular entities that modulate lipid metabolism, often leveraging genomic and proteomic data. API manufacturing involves highly specialized chemical synthesis for small molecules (like fibrates) or complex bioprocessing for large molecules and biologics (like ASOs and monoclonal antibodies). Maintaining stringent quality control and achieving economies of scale in API production are crucial factors influencing the final cost of the therapeutic agent, particularly for high-purity omega-3 derivatives which require sophisticated purification technologies.

The Midstream component involves manufacturing and formulation, where APIs are converted into finished dosage forms (tablets, capsules, or sterile injectable solutions). This stage includes critical regulatory approvals from bodies like the FDA and EMA. Downstream Analysis encompasses marketing, sales, and distribution. Distribution channels are predominantly categorized into direct and indirect methods. Direct distribution involves large pharmaceutical companies supplying specialized treatments directly to large hospital systems or specialty pharmacy networks, often necessitated by complex storage requirements or patient support programs for novel injectables. Indirect distribution relies on established wholesale intermediaries that supply the broader network of retail and independent pharmacies for high-volume oral medications.

Potential conflicts and optimization points in the value chain often arise at the distribution and pricing level. Payers (insurance companies and government entities) exert significant pressure on pricing, impacting profit margins across the chain. The shift toward personalized medicine requires tighter integration between diagnostic companies and therapeutic providers. The efficacy of the market depends heavily on effective physician and patient education, ensuring compliance and correct usage of both oral maintenance therapies and specialized injectable biologicals, thereby realizing the full therapeutic and commercial potential of these lipid-lowering agents.

The primary consumers and end-users of hypertriglyceridemia therapeutic products are a diverse group of healthcare practitioners and institutions directly involved in cardiovascular risk management and metabolic disorder treatment. Cardiologists and endocrinologists represent the most critical prescribers, as hypertriglyceridemia is intimately linked with cardiovascular disease progression and insulin resistance often observed in Type 2 Diabetes. General practitioners and internal medicine specialists also constitute a substantial customer base, particularly for routine screening and maintenance therapy using widely available oral agents such as fibrates and statins.

From an institutional perspective, major buyers include large hospital systems and specialized clinics that manage high-risk patient populations, especially those requiring complex or novel injectable therapies for severe familial hypertriglyceridemia. Government procurement agencies and national health services (e.g., NHS in the UK, various health ministries in Europe and Asia) are pivotal customers in bulk purchasing generic and essential lipid-lowering drugs for national formularies, profoundly influencing regional market volumes and pricing strategies. Furthermore, individual patients, through out-of-pocket payments or insurance co-pays, are the ultimate beneficiaries and purchasers of these chronic medications dispensed via retail pharmacy networks.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.55 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amgen Inc., Pfizer Inc., Takeda Pharmaceutical Company Limited, AstraZeneca PLC, GlaxoSmithKline PLC, Novartis AG, Sanofi S.A., Ionis Pharmaceuticals, Inc., Akcea Therapeutics (Ionis Subsidiary), Kowa Company, Ltd., Bristol-Myers Squibb Company, Eli Lilly and Company, Merck & Co., Inc., Catabasis Pharmaceuticals, Inc., Acasti Pharma Inc., North American BioSciences, Inc., Esperion Therapeutics, Inc., Regeneron Pharmaceuticals, Inc., Matinas BioPharma Holdings, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Hypertriglyceridemia Therapeutic Market is currently undergoing significant technological transformation, moving beyond traditional small-molecule interventions toward advanced biological and genetic approaches. A crucial technology driving this innovation is gene silencing, exemplified by the use of Antisense Oligonucleotides (ASOs) and small interfering RNA (siRNA). These technologies allow for the targeted inhibition of gene expression responsible for the overproduction of triglyceride-rich lipoproteins (e.g., ApoCIII). ASOs, such as volanesorsen, represent a breakthrough in treating severe, genetically linked hypertriglyceridemia, offering profound and sustained triglyceride reduction that conventional drugs cannot achieve. The development focus is on improving delivery mechanisms, reducing injection frequency, and minimizing hepatic and renal toxicity associated with these nucleic acid-based therapies.

Another pivotal technological area is the development of next-generation monoclonal antibodies targeting key regulatory proteins in lipid metabolism. Specifically, research into inhibiting Angiopoietin-like 3 (ANGPTL3) shows immense promise. ANGPTL3 is a circulating protein that inhibits lipoprotein lipase and endothelial lipase, thus elevating triglyceride levels. By blocking ANGPTL3 with a dedicated antibody, researchers can achieve substantial reductions in both triglycerides and LDL cholesterol. Evinacumab is a prime example of this technology, showcasing the potential for highly effective, targeted therapies that address complex dyslipidemias simultaneously. These biologic agents often require highly sophisticated bioprocessing and sterile manufacturing capabilities, demanding high initial capital investment.

Furthermore, the integration of advanced diagnostic technologies, particularly comprehensive lipidomic analysis and genetic sequencing, plays a critical role in supporting the therapeutic market. Lipidomics allows for the detailed profiling of various lipid classes and subclasses, providing deeper insight into the patient’s metabolic phenotype beyond standard lab panels. This precision diagnostic capability enables physicians to select the most appropriate targeted therapy, moving the field towards truly precision medicine. The convergence of these technological advancements – genetic therapies, targeted antibodies, and high-resolution diagnostics – is creating a complex but highly effective therapeutic landscape for patients with severe or refractory hypertriglyceridemia, ensuring sustained high growth in the novel therapeutics segment.

The Hypertriglyceridemia Therapeutic Market exhibits significant regional disparities influenced by varying healthcare policies, disease prevalence rates, and market access strategies.

North America is the dominant region, commanding the largest market share due to the highest per capita healthcare spending globally, a high prevalence of obesity and metabolic syndrome, and well-defined clinical guidelines that favor aggressive lipid management. The U.S. market, in particular, benefits from robust reimbursement mechanisms for high-cost, branded novel therapies and prescription-grade omega-3 formulations, such as those proven effective in cardiovascular outcome trials. Early and rapid adoption of cutting-edge technologies like ASOs and ANGPTL3 inhibitors ensures sustained regional leadership, alongside a highly competitive environment among pharmaceutical manufacturers.

The European market presents a diverse landscape, characterized by centralized government procurement and stringent Health Technology Assessment (HTA) procedures in major markets like Germany, France, and the UK. While the overall prevalence of hypertriglyceridemia is high, particularly in Eastern Europe, market growth is often tempered by cost-effectiveness requirements, favoring the utilization of established, generic therapies (fibrates, low-cost niacin). However, Western European nations are demonstrating increasing uptake of specialty biologicals for severe familial cases, driving segmentation toward higher-value products, despite longer approval times compared to the U.S.

The APAC region is projected to experience the fastest market growth during the forecast period. This rapid expansion is fueled by drastic changes in dietary habits, increasing urbanization, and subsequent rise in NCDs, notably diabetes and related dyslipidemias, across India, China, and Southeast Asia. Improving economic conditions and increasing government investments in healthcare infrastructure enhance patient access to treatment. While generic drugs currently dominate volume sales, the emerging middle class and expanding private insurance markets are accelerating the adoption of premium branded and novel therapies, making it a critical strategic focus area for global pharmaceutical companies.

The LATAM market, including Brazil and Mexico, exhibits steady growth driven by demographic factors and increasing prevalence of metabolic diseases. Market access is often variable, influenced by localized government funding and economic stability. There is a strong demand for affordable generic alternatives, though pharmaceutical companies are increasingly targeting the high-net-worth segment with branded products through private healthcare facilities. Regulatory harmonization remains a challenge, impacting the speed of new product introductions.

The MEA region shows nascent but focused growth, particularly in the Gulf Cooperation Council (GCC) states (Saudi Arabia, UAE) where high incidence of lifestyle diseases and substantial government healthcare investment create demand for advanced therapeutic options. In contrast, parts of Africa face immense challenges regarding infrastructure and affordability, limiting the market primarily to essential, cost-effective generic lipid-lowering drugs.

The primary factor is the soaring global prevalence of metabolic disorders, specifically obesity and Type 2 Diabetes Mellitus, which are directly responsible for the increasing incidence of elevated blood triglyceride levels and associated cardiovascular risks.

Novel therapeutics like ASOs and gene silencing agents are revolutionizing the treatment of severe, often genetically driven, hypertriglyceridemia by offering highly targeted, substantial, and sustained triglyceride reduction through specific interference with metabolic genes, addressing patients refractory to traditional oral agents.

The Omega-3 Fatty Acids drug class, specifically high-purity, prescription-grade icosapent ethyl, holds the largest market share due to robust clinical trial evidence demonstrating significant cardiovascular risk reduction in addition to lipid lowering, leading to widespread adoption in established markets like North America.

The key challenge in Europe is the presence of stringent Health Technology Assessment (HTA) requirements and centralized price negotiations, which prioritize cost-effectiveness, leading to slower market access and greater pressure on the pricing of high-cost, branded biological therapies compared to the US market.

AI is crucial for enhancing precision medicine by enabling the rapid identification of new drug targets, optimizing clinical trial patient selection, and developing personalized dosing strategies based on complex patient genetic and metabolic profiles, streamlining the development of next-generation therapies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.