ID : MRU_ 441921 | Date : Feb, 2026 | Pages : 248 | Region : Global | Publisher : MRU

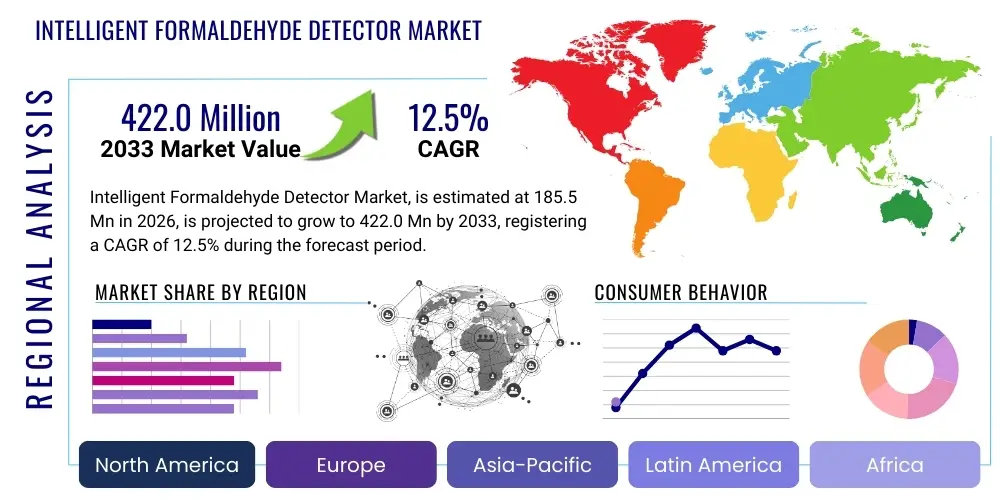

The Intelligent Formaldehyde Detector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at $185.5 Million in 2026 and is projected to reach $422.0 Million by the end of the forecast period in 2033.

The Intelligent Formaldehyde Detector Market encompasses devices designed for the accurate, continuous, and often remote monitoring of formaldehyde (HCHO) levels in indoor environments. Formaldehyde, a volatile organic compound (VOC) commonly released from building materials, furniture, and household products, poses significant health risks, necessitating sophisticated detection methods. These intelligent detectors move beyond basic sensor technology by integrating advanced features such as IoT connectivity, cloud data processing, and predictive analytics, enabling real-time alerts, historical data logging, and seamless integration with smart home or building management systems (BMS). The primary function is to safeguard occupant health by providing actionable insights into air quality dynamics.

Intelligent formaldehyde detectors are rapidly gaining traction across diverse applications, ranging from residential smart homes and new construction projects to complex industrial settings like chemical plants, laboratories, and specialized commercial spaces such as hospitals and schools. The core benefits derived from these advanced systems include superior measurement accuracy, reduced false alarms through enhanced calibration algorithms, long-term operational stability, and the ability to link detection events directly to remedial actions, such as activating integrated ventilation systems. This transition from passive monitoring to active, data-driven air quality management defines the market’s current trajectory.

Market expansion is primarily fueled by escalating global health consciousness regarding indoor air quality (IAQ) and the tightening of regulatory standards pertaining to VOC emissions in consumer products and building materials. Furthermore, the proliferation of Internet of Things (IoT) platforms and the increasing affordability of highly sensitive sensor technologies, notably electrochemical and photoionization detector (PID) sensors miniaturized for consumer use, are critical driving factors. These technological convergence points facilitate the deployment of robust, user-friendly, and network-enabled detection solutions that meet both consumer demand for personal health protection and institutional requirements for regulatory compliance and building optimization.

The Intelligent Formaldehyde Detector Market is currently defined by a strong emphasis on technological integration, moving toward comprehensive Indoor Air Quality (IAQ) platforms rather than standalone detection units. Key business trends include strategic partnerships between hardware manufacturers and AI/software developers to enhance data interpretation capabilities and reduce sensor drift, a persistent challenge in VOC detection. The market is experiencing aggressive product differentiation based on sensor longevity, connectivity protocols (especially Wi-Fi 6 and 5G readiness), and integration potential with existing infrastructure like HVAC systems and building automation platforms. Furthermore, sustainability mandates and green building certification standards (such as LEED and WELL) are creating significant demand pull in the commercial sector, driving vendors to develop solutions with minimal energy footprints and maximal lifespan.

Geographically, the Asia Pacific (APAC) region, spearheaded by China and India, represents the largest and fastest-growing segment, driven by rapid urbanization, substantial construction activities, and heightened governmental focus on urban air pollution mitigation strategies. European markets demonstrate strong adoption propelled by strict adherence to IAQ standards and a high consumer propensity for premium, certified health technology. North America remains a significant market, characterized by mature smart home ecosystems and strong regulatory enforcement by agencies like the EPA, demanding highly reliable and certified detection instruments. Regional trends also reveal varying degrees of acceptance for cloud-based vs. edge processing, depending on data privacy concerns and infrastructure maturity.

Segmentation trends highlight the increasing dominance of IoT-enabled detectors over standalone variants, reflecting a market shift towards connected ecosystems. By application, the residential sector, fueled by direct-to-consumer health gadget sales, and the specialized commercial sector (healthcare, education) are the most dynamic segments. Technology-wise, while electrochemical sensors dominate due to their cost-effectiveness and good specificity, Photoionization Detectors (PIDs) are gaining momentum in professional and industrial high-precision applications. Overall, the market trajectory is characterized by fierce competition centered on achieving the golden standard of detection: high accuracy, rapid response time, and minimal total cost of ownership (TCO) through reduced maintenance requirements.

User queries regarding AI's influence in the Intelligent Formaldehyde Detector market predominantly revolve around three critical themes: improving sensor reliability, enabling predictive health modeling, and optimizing energy use through smart ventilation control. Users frequently question if AI can overcome the inherent limitations of conventional VOC sensors, such as cross-sensitivity to other gases and calibration drift over time. There is high expectation that AI algorithms will enhance data fidelity by filtering noise, correlating formaldehyde readings with environmental factors (temperature, humidity), and validating measurements against historical trends or external air quality indices. Furthermore, consumers and facility managers are keenly interested in how AI can move beyond simple threshold alerts to provide predictive warnings about potential air quality deterioration and autonomously adjust remediation measures, thereby transforming reactive monitoring into proactive air quality management.

The practical application of Artificial Intelligence (AI) algorithms, specifically machine learning (ML) models, significantly elevates the performance ceiling of intelligent formaldehyde detectors. ML models trained on vast datasets encompassing sensor readings, usage patterns, external environmental data, and known chemical interference profiles can execute sophisticated drift compensation and enhance the specificity of low-cost sensors, thereby bridging the performance gap between consumer-grade and expensive analytical equipment. This capability drastically reduces the operational expenditure associated with manual calibration and maintenance cycles, while simultaneously instilling greater user confidence in the accuracy of the reported data. AI also facilitates personalized alert systems, learning the baseline air quality signature of a specific environment and only flagging deviations that are statistically relevant, reducing alarm fatigue.

Beyond improving raw detection accuracy, AI is pivotal in enabling the strategic integration of formaldehyde detection with broader smart building infrastructure. Advanced analytics platforms use collected HCHO data to inform Building Management Systems (BMS) and HVAC controllers, optimizing ventilation rates based not solely on CO2 levels, but also on real-time VOC contamination. This predictive ventilation strategy minimizes energy consumption by only increasing air exchanges when genuine pollutant threats are detected, offering significant operational cost savings for commercial property owners. This convergence of detection, prediction, and automated action solidifies the intelligent formaldehyde detector's role as a key component in comprehensive, energy-efficient smart building solutions, driving substantial long-term market value.

The Intelligent Formaldehyde Detector Market dynamics are shaped by a complex interplay of influential factors summarized by Drivers, Restraints, and Opportunities (DRO), which are magnified by broader Impact Forces. Primary drivers are rooted in public health concerns and tightening regulatory frameworks globally. The widespread acknowledgement of formaldehyde as a potent carcinogen and a major contributor to Sick Building Syndrome (SBS) mandates its effective monitoring, particularly in high-density or sensitive environments like schools and hospitals. Concurrently, the robust growth of the global smart home ecosystem provides a ready infrastructure for connected IAQ devices, transforming luxury technology into perceived necessity. Restraints primarily involve the technical limitations inherent in current sensor technology, such as persistent issues with sensitivity drift, high cross-sensitivity to common household chemicals, and the perceived high initial investment cost relative to simple, non-intelligent detectors. Furthermore, consumer education gaps regarding the difference between intelligent and basic detectors sometimes impede premium market penetration.

Opportunities abound, centering on technological innovation and market expansion. The integration of advanced Micro-Electro-Mechanical Systems (MEMS) sensors promises higher performance at smaller sizes and lower manufacturing costs, potentially mitigating the current restraints related to cost and size. Significant potential exists in embedding detection capabilities directly into consumer electronics, smart furniture, and HVAC systems, moving from external devices to integrated components. Moreover, the growth of the data monetization economy presents an opportunity for vendors to offer recurring subscription services based on advanced analytical reports, predictive modeling, and remote diagnostic services, thereby creating long-term revenue streams beyond the initial hardware sale. The rising global demand for verifiable Green Building certifications ensures continuous demand in the commercial sector.

The overall impact forces driving the market are dominated by stringent regulatory pressure, global environmental health initiatives, and the accelerating pace of IoT technological convergence. Governments worldwide are consistently lowering permissible exposure limits (PELs) for formaldehyde, requiring businesses and consumers to adopt highly accurate, certified monitoring solutions. This regulatory force acts as a major market accelerator. Simultaneously, competition is intensified by the rapid adoption of AI and ML in data processing, forcing existing market players to continuously invest in R&D to maintain accuracy leadership and integration superiority. These impact forces necessitate a continuous focus on miniaturization, connectivity standardization, and achieving maximum data reliability under diverse environmental conditions.

The Intelligent Formaldehyde Detector market is segmented to analyze growth patterns, adoption rates, and competitive intensity across different dimensions, including technology type, application environment, connectivity level, and detection principle. Understanding these segments is crucial for strategic planning, allowing manufacturers to tailor product specifications—such as sensor lifespan, data output format, and enclosure robustness—to meet the unique demands of specific end-user categories. The market exhibits distinct characteristics between the high-volume residential sector, which prioritizes ease of use and aesthetics, and the low-volume, high-value industrial sector, which demands unparalleled accuracy, robustness, and compliance certification.

Segmentation by technology is critical, distinguishing between devices based on electrochemical cells, which offer good selectivity and low power consumption, and Photoionization Detectors (PIDs), favored for their ultra-high sensitivity and wide dynamic range, although typically reserved for professional-grade instruments due to higher cost and maintenance. The market also segments heavily based on connectivity, differentiating between standalone devices and advanced IoT-enabled systems that communicate via Wi-Fi, Zigbee, or LoRaWAN. This connectivity criterion fundamentally dictates the product's intelligence, integration capability, and the potential for real-time remote monitoring, which is a key driver in both commercial building management and multi-unit residential complexes.

Application segmentation remains pivotal, categorizing demand generated by residential users (driving miniaturization and consumer aesthetics), commercial buildings (requiring seamless BMS integration and certification adherence), and industrial/HVAC sectors (demanding rugged enclosures, continuous operation, and Modbus/BACnet compatibility). The highest growth is observed in the segment combining IoT-enabled technology with residential and specialized commercial applications, reflecting the dual trends of increasing consumer health investment and mandated commercial IAQ verification. Strategic focus is currently placed on developing multi-gas detectors that include specialized formaldehyde detection, providing comprehensive IAQ monitoring solutions rather than single-pollutant devices, optimizing installation complexity and overall cost for the end-user.

The value chain for the Intelligent Formaldehyde Detector Market begins with the highly specialized upstream segment, dominated by key suppliers of core sensor technologies, microcontrollers, and communication chips. Upstream activities involve complex R&D focused on material science to improve sensor longevity and chemical selectivity, particularly for overcoming the cross-sensitivity challenges associated with common VOC sensors. Key upstream players are typically specialized chemical sensor manufacturers and semiconductor giants, which dictates the pace of technological innovation and cost structures for the entire downstream market. The successful integration of MEMS technology at this stage is crucial for achieving cost reduction and miniaturization, which directly impacts the product's competitiveness in consumer markets.

The midstream segment involves the detector manufacturers, where the integration of hardware, firmware, and proprietary AI algorithms takes place. This stage is characterized by high value addition, focusing on industrial design, user interface optimization, quality assurance testing (crucial for regulatory compliance), and the development of cloud platforms for data aggregation and remote management. Manufacturers often dedicate significant resources to developing machine learning models for calibration management and false positive reduction, establishing intellectual property crucial for market differentiation. Effective supply chain management and modular design are paramount in the midstream to ensure rapid assembly and scalability to meet fluctuating demand, particularly during seasonal spikes in air quality awareness.

The downstream activities involve distribution, sales, installation, and after-sales services. Distribution channels are bifurcated into direct sales to large commercial and industrial clients, often involving system integrators (SIs) and HVAC specialists, and indirect channels relying on e-commerce platforms, consumer electronics retailers, and specialized health technology outlets for residential sales. Direct channels necessitate strong technical support and consultancy services to ensure seamless integration into existing building management systems (BMS). Indirect channels prioritize simplified installation and mass-market reach. The profitability of the downstream segment is increasingly linked to subscription revenues generated from enhanced cloud monitoring services and extended maintenance contracts, shifting the economic model from purely transactional hardware sales to service-oriented partnerships.

The market for intelligent formaldehyde detectors is characterized by a broad spectrum of potential customers, segmented based on their primary motivation: regulatory compliance, personal health protection, or operational efficiency. Primary end-users in the residential sector include homeowners and apartment dwellers, particularly those with new furniture, recent renovations, or vulnerable populations (children, elderly) residing within, where the motivation is immediate, personal health assurance and integration into a smart living environment. This segment demands user-friendly interfaces, aesthetically pleasing designs, and robust app connectivity for remote monitoring and notification, often procured through direct-to-consumer e-commerce channels or big-box retailers specializing in smart home technology.

In the commercial domain, potential customers include commercial real estate developers, facility managers of corporate offices, and operators of specialized facilities like hospitals, schools, and daycare centers. For these institutional buyers, the motivation is strictly compliance with IAQ standards, mitigating legal liability related to Sick Building Syndrome, and achieving premium building certifications (e.g., WELL, LEED). These customers require industrial-grade, highly reliable systems that can communicate using standard industry protocols (Modbus, BACnet) and provide traceable, continuous data logs for auditing purposes. System integrators and HVAC contractors act as critical intermediaries in this segment, managing the procurement and installation process.

A specialized, yet high-value, customer group consists of industrial enterprises involved in the manufacture of formaldehyde-containing products, such as resins, paints, adhesives, and composite wood panels. Within this context, intelligent detectors are used for occupational safety and environmental monitoring, ensuring compliance with OSHA and local environmental agency exposure limits. Government agencies, including environmental protection bureaus and occupational safety regulators, also represent significant bulk buyers for mobile and fixed intelligent detectors used in urban air quality assessment and enforcement activities. Their focus is on accuracy, portability (for mobile checks), and standardized data output compatible with national monitoring networks.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $185.5 Million |

| Market Forecast in 2033 | $422.0 Million |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., Thermo Fisher Scientific Inc., Aeroqual Ltd., RAE Systems (by Honeywell), Airthings AS, 3M Company, TSI Incorporated, Testo SE & Co. KGaA, Drägerwerk AG & Co. KGaA, PCE Instruments, ESI Technologies, Forensics Detectors, Sensepoint, Nest Labs (Google), Awair. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape in the Intelligent Formaldehyde Detector market is defined by rapid advancements in sensor miniaturization and chemical selectivity enhancement, coupled with sophisticated data processing capabilities. The backbone of intelligent detection remains advanced electrochemical sensors, which are highly preferred due to their relatively low power consumption, affordability, and reasonable specificity for HCHO compared to broad-spectrum VOC sensors. However, significant R&D efforts are focused on improving the stability and lifespan of these chemical cells, often through novel electrode materials and improved electrolyte formulations, aiming to meet commercial standards requiring 5-7 years of maintenance-free operation. Photoionization Detector (PID) technology, while offering superior sensitivity (ppb level) and rapid response, remains restricted mainly to high-end industrial and scientific applications due to higher cost and susceptibility to humidity interference, though miniaturization efforts are attempting to broaden its applicability.

Intelligence in these devices is critically driven by connectivity and data analytics infrastructure. The transition to IoT-enabled detectors utilizing Wi-Fi, Bluetooth Low Energy (BLE), and specialized low-power wide-area network (LPWAN) protocols like LoRaWAN ensures seamless integration into residential and enterprise networks. This connectivity facilitates real-time data transmission to cloud platforms, enabling remote monitoring, historical trend analysis, and over-the-air (OTA) firmware updates essential for maintaining sensor accuracy throughout the product lifecycle. The reliance on cloud computing allows for the implementation of complex machine learning algorithms that perform necessary environmental normalization, filtering out interference from common household items and recalibrating sensor readings automatically, a process that is technically infeasible on local hardware.

A burgeoning technological trend involves the development and deployment of Micro-Electro-Mechanical Systems (MEMS) based sensors for VOC detection, including formaldehyde. MEMS technology promises radical reductions in sensor size, manufacturing cost, and power requirements, paving the way for ubiquitous integration into diverse consumer products and wearable technology. Although MEMS sensors currently face challenges related to selectivity and stability compared to traditional electrochemical types, ongoing innovation in functionalized coating materials and integration with sophisticated temperature and humidity compensation circuits are expected to make MEMS a disruptive force within the forecast period. Furthermore, advancements in data visualization and API development are simplifying the integration of raw HCHO data into comprehensive Building Energy Management Systems (BEMS) and smart home dashboards, enhancing the detector's utility from a simple monitor to an active control node.

Regional variations in the Intelligent Formaldehyde Detector Market are highly pronounced, reflecting differences in construction standards, regulatory stringency, population density, and technological adoption rates. North America, particularly the United States and Canada, presents a mature market characterized by high consumer awareness regarding IAQ and robust enforcement of environmental regulations by state and federal bodies. The demand in this region is primarily driven by sophisticated smart home ecosystems demanding seamless integration and a high propensity among commercial entities to invest in certified, high-accuracy monitoring systems to mitigate litigation risk and ensure tenant safety. Market growth is sustained by continuous technological upgrades, pushing consumers to replace older, less accurate devices with connected, AI-optimized solutions.

Europe represents another key region, exhibiting strong growth fueled by proactive environmental policies, stringent indoor air quality directives set by the European Union, and a cultural emphasis on sustainable and healthy living spaces, exemplified by the proliferation of passive house and Green Building certifications. Countries such as Germany, the UK, and Scandinavian nations show high adoption rates, favoring detectors that are certified under various European standards (e.g., VDA, Eurofins). The market here is sensitive to sensor life cycle assessments and data privacy regulations (GDPR), which often necessitate regional cloud hosting solutions and transparency in data usage. The trend favors integrated, multi-sensor devices that offer holistic reporting on various pollutants alongside formaldehyde.

The Asia Pacific (APAC) region stands out as the highest growth engine globally, driven by unprecedented rates of urbanization, massive new construction projects, and escalating public outcry over pollution, both ambient and indoor. China, in particular, is a dominant market due to the widespread use of composite wood products in construction and furniture manufacturing, resulting in chronic formaldehyde issues in newly built homes and offices. Regulatory efforts in countries like China, South Korea, and Japan are rapidly catching up to Western standards, translating into substantial procurement by governmental bodies for public monitoring programs and mandatory installation requirements for new buildings. This region is highly competitive, focusing on balancing cost-effectiveness with acceptable performance, often seeing faster adoption of locally developed sensor technologies.

Intelligent detectors integrate IoT connectivity, cloud data processing, and machine learning algorithms for continuous, remote monitoring, automated calibration adjustments, and the integration of detection data with Building Management Systems (BMS) or smart home platforms. Standard detectors typically offer basic, localized measurements without network connectivity or advanced analytical capabilities.

AI, through machine learning models, enhances accuracy by executing complex sensor drift compensation, correlating HCHO readings with ambient environmental factors (like humidity and temperature), and filtering out cross-interference from other Volatile Organic Compounds (VOCs), significantly reducing false positives and extending the functional life of the sensor.

Electrochemical sensors currently dominate the market, especially in consumer and mid-range commercial applications, due to their favorable balance of cost, power efficiency, and reasonable specificity for formaldehyde. However, Photoionization Detectors (PID) are utilized in specialized industrial and high-accuracy professional monitoring segments.

The primary commercial drivers include regulatory compliance in newly constructed buildings, specialized monitoring in healthcare facilities (hospitals and labs), educational institutions (schools), and achieving coveted Green Building certifications like LEED and WELL, which mandate continuous IAQ verification.

Long-term opportunities center on seamless integration into HVAC systems for automated, energy-optimized ventilation control and the transition towards subscription-based service models offering predictive air quality analysis, remote diagnostics, and detailed compliance reporting.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.