ID : MRU_ 443211 | Date : Feb, 2026 | Pages : 245 | Region : Global | Publisher : MRU

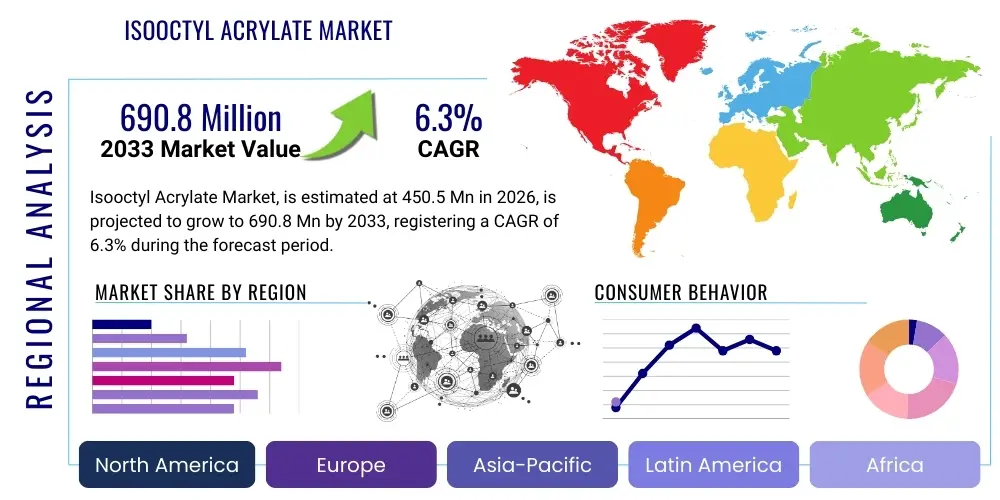

The Isooctyl Acrylate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.3% between 2026 and 2033. The market is estimated at $450.5 Million in 2026 and is projected to reach $690.8 Million by the end of the forecast period in 2033.

Isooctyl Acrylate (IOA) is a clear, colorless liquid monomer characterized by its low volatility, excellent flexibility, and high reactivity, making it a pivotal chemical intermediate across numerous industrial sectors. Chemically, it is an acrylic ester derived from isooctyl alcohol and acrylic acid, possessing a single acrylic unsaturation that readily undergoes polymerization reactions, forming polymers with specific desirable characteristics such as low glass transition temperature (Tg) and superior adhesion properties. This chemical profile positions IOA as a crucial component in high-performance formulations where elasticity and strong bonding are paramount, notably in specialized adhesive tapes, pressure-sensitive adhesives (PSAs), and architectural coatings. The versatility of IOA allows it to be copolymerized with other monomers, enabling formulators to fine-tune the resulting polymer properties, thereby expanding its utility in advanced material science.

The primary applications driving the demand for Isooctyl Acrylate center around its role in pressure-sensitive adhesives used extensively in packaging, medical devices (such as transdermal patches), and industrial assembly, where its contribution to tackiness and shear strength is irreplaceable. Furthermore, in the coatings industry, IOA is valued for enhancing the weathering resistance, flexibility, and impact strength of paints and protective films, particularly those used in automotive finishes and exterior architectural applications. The inherent low toxicity and stability of IOA derivatives also make them suitable for sensitive applications like specialty ink formulations and cosmetic ingredients, ensuring broad market penetration across diverse end-user industries.

Key driving factors accelerating the Isooctyl Acrylate market expansion include the sustained growth of the global packaging industry, driven by e-commerce proliferation and the increasing requirement for robust, reliable adhesive solutions. The rising demand for eco-friendly, solvent-free coating technologies, particularly UV-cured and waterborne systems, significantly boosts IOA consumption due to its compatibility with these modern chemistries. Additionally, rapid urbanization and infrastructure development in emerging economies are fueling the construction and automotive sectors, both heavy consumers of IOA-based sealants and coatings. Regulatory landscapes favoring low-VOC (Volatile Organic Compound) materials further solidify IOA's market position, as it offers performance benefits while complying with increasingly stringent environmental standards, making it a critical chemical building block for future sustainable materials.

The Isooctyl Acrylate market is characterized by robust business trends driven primarily by shifts toward high-performance, sustainable chemical solutions and the expanding industrial application base in Asia Pacific. Segment trends indicate that the Pressure-Sensitive Adhesives (PSA) application segment maintains market dominance, bolstered by increasing consumption of specialty tapes, labels, and protective films across logistics and consumer electronics manufacturing. Furthermore, the market is witnessing technological refinement focused on producing high-purity IOA suitable for specialized medical and electronic applications, demanding tighter quality control and sophisticated polymerization techniques. Strategic initiatives among key manufacturers revolve around capacity expansion, particularly in regions offering competitive feedstock prices and proximity to burgeoning end-use markets, aiming to secure long-term supply stability and optimize distribution logistics for bulk chemicals.

Regionally, Asia Pacific commands the largest market share and is expected to exhibit the highest growth rate throughout the forecast period, primarily fueled by the massive growth in China, India, and Southeast Asian nations' manufacturing, construction, and automotive industries. This regional surge is attributed to substantial domestic industrial output, favorable government policies supporting manufacturing excellence, and the relocation of global production bases to these areas. North America and Europe, while representing mature markets, show consistent demand driven by stringent regulatory frameworks necessitating the adoption of low-VOC coatings and specialized industrial adhesives. These mature markets focus heavily on innovation, demanding Isooctyl Acrylate derivatives optimized for advanced UV-cured formulations and specialized medical adhesive applications, ensuring stable, high-value consumption.

Overall, the market dynamic is a complex interplay of feedstock volatility (linked to crude oil pricing), regulatory pressures favoring green chemistry, and unparalleled demand from the adhesives and coatings sectors. The future trajectory of the IOA market relies heavily on managing supply chain disruptions, successfully transitioning towards bio-based or renewable feedstock alternatives to mitigate environmental impact, and capitalizing on the rapid digitalization across industries that necessitate advanced labeling and flexible electronic materials. Successful market participation requires companies to balance operational efficiency and competitive pricing with continuous innovation in product quality and purity, effectively navigating both bulk chemical supply complexities and niche specialty application requirements.

User queries regarding the intersection of Artificial Intelligence (AI) and the Isooctyl Acrylate market primarily center on optimizing chemical synthesis processes, predicting feedstock price volatility, and enhancing quality control in polymerization. Key themes include the implementation of predictive analytics for supply chain resilience, utilizing machine learning algorithms to discover novel acrylic co-polymers with enhanced performance characteristics (such as improved thermal stability or accelerated curing times), and automating quality checks to ensure consistent purity levels required for high-end applications like medical adhesives. Concerns also frequently arise regarding the capital investment needed to integrate AI infrastructure into existing chemical production facilities and the requirement for specialized data science expertise within traditional chemical manufacturing organizations. Users anticipate that AI will fundamentally transform R&D efficiency and maintenance schedules, leading to significant cost reductions and faster time-to-market for new IOA-based products.

The most immediate impact of AI is observed in production optimization and predictive maintenance. Advanced AI algorithms can analyze vast datasets from reactors, including temperature, pressure, reaction kinetics, and catalyst concentration, to fine-tune reaction parameters in real-time. This dynamic adjustment capability minimizes off-spec product batches, reduces energy consumption per unit produced, and significantly improves overall operational efficiency, which is critical in the cost-sensitive bulk chemical market. Furthermore, predictive models can anticipate equipment failure with high accuracy, allowing maintenance teams to intervene proactively, thus minimizing costly unplanned downtime and maximizing asset utilization, which directly influences the overall capacity and pricing stability of Isooctyl Acrylate.

Beyond manufacturing, AI is revolutionizing the research and development pipeline for Isooctyl Acrylate applications. Machine learning is increasingly utilized for virtual screening of potential copolymer blends, drastically reducing the need for expensive and time-consuming laboratory experiments. By simulating interactions between IOA and various co-monomers, AI can identify promising formulations for new adhesives or coatings that meet specific regulatory requirements or performance benchmarks, such as improved durability or enhanced biodegradability. This accelerated material discovery process is crucial for maintaining competitiveness in fast-evolving sectors like electronics and specialty packaging, where demand for customized, high-performance IOA derivatives is constant.

The Isooctyl Acrylate market dynamics are governed by a complex set of Drivers, Restraints, and Opportunities (DRO), underpinned by significant external impact forces. Key drivers include the exponential growth in demand for high-performance Pressure Sensitive Adhesives (PSAs) in electronics, automotive assembly, and medical applications, where the monomer's characteristic flexibility and strong bonding capabilities are highly valued. Furthermore, the global shift towards environmentally preferred coating systems, such as UV-curable and waterborne coatings, substantially boosts the consumption of IOA due to its reactive nature and ability to impart desired performance attributes in solvent-free systems. Restraints predominantly revolve around the inherent volatility and price fluctuations of petrochemical feedstocks, specifically acrylic acid and isooctyl alcohol, which introduce significant cost uncertainty for manufacturers and downstream consumers. Additionally, increasing environmental scrutiny and evolving regulations regarding chemical handling and disposal pose ongoing challenges, demanding continuous investment in safer manufacturing processes and compliance protocols.

Opportunities for market growth are vast and largely tied to innovation and geographical expansion. The development of bio-based Isooctyl Acrylate alternatives presents a major opportunity to mitigate feedstock reliance and appeal to increasingly sustainability-conscious industries, positioning manufacturers favorably for future regulatory environments. Geographically, expansion into rapidly industrializing regions of Asia Pacific, particularly countries strengthening their domestic manufacturing and construction sectors, provides significant untapped market potential. The continuous development of specialized, high-margin applications, such as optically clear adhesives (OCA) for display technologies and advanced materials for renewable energy infrastructure (e.g., specialized sealants for solar panels), offers avenues for premium pricing and technological leadership.

External impact forces, including Porter’s Five Forces analysis, indicate moderate competitive rivalry, driven by capacity expansions among major Asian producers and the relatively high capital intensity required for monomer production. The bargaining power of suppliers is moderate to high, largely dependent on the integration level of the manufacturers, as the raw materials are globally traded commodities tied to crude oil markets. The threat of substitutes, while present from other acrylate monomers (such as 2-Ethylhexyl Acrylate, 2-EHA) and alternative non-acrylate adhesive systems (like polyurethanes or silicones), is somewhat mitigated by the unique performance profile of IOA, especially in applications demanding low Tg and specific adhesion profiles. Overall market stability is maintained by sustained demand from critical infrastructure sectors, although sudden spikes in raw material costs or restrictive environmental policies could swiftly alter the operating landscape.

The Isooctyl Acrylate market is meticulously segmented to provide granular insights into consumer behavior, technological adoption, and application maturity across various industrial landscapes. Segmentation is primarily structured based on Purity Level, acknowledging the distinct quality requirements for specialized applications versus bulk uses; Application Method, focusing on the formulation type; and the End-Use Industry, highlighting the diverse sectoral demand drivers. This framework allows market participants to tailor their product offerings, sales strategies, and R&D efforts to target high-growth or high-margin niches, such as the need for ultra-high purity IOA in sophisticated medical adhesives or high-volume IOA for general-purpose construction coatings. Understanding the interplay between these segments is crucial for forecasting regional demand patterns and anticipating technological shifts within the supply chain.

The application segmentation, covering adhesives, coatings, and sealants, provides the clearest delineation of demand concentration, with adhesives consistently holding the dominant share due to the proliferation of PSA technology globally. Within the purity segment, standard industrial grade (99.0%) accounts for the largest volume consumption, primarily serving traditional coatings and sealants markets, whereas higher purity grades (99.5% and above) command significant price premiums and are directed toward sensitive applications like specialized medical packaging, pharmaceutical labels, and advanced electronic bonding agents. Furthermore, the end-use industry segmentation validates the market's dependence on global macroeconomic trends in construction and automotive manufacturing, which require substantial volumes of protective and functional IOA-based chemistries for durability and aesthetic purposes, confirming IOA's status as a foundational building block chemical.

The value chain for the Isooctyl Acrylate market begins with the Upstream Analysis, which is highly integrated and capital-intensive, focusing on the procurement and processing of key petrochemical feedstocks: acrylic acid and isooctyl alcohol. Acrylic acid is primarily derived from the catalytic oxidation of propylene, a derivative of crude oil refining or natural gas processing, introducing significant vulnerability to volatile energy market prices. Isooctyl alcohol is often sourced through oxo synthesis processes. Major chemical producers typically operate integrated facilities, allowing them to capture value through in-house production of these precursors. The efficiency and reliability of this upstream stage, including process optimization and feedstock hedging strategies, directly determine the profitability of IOA manufacturing.

The core manufacturing process involves the esterification reaction between acrylic acid and isooctyl alcohol to yield Isooctyl Acrylate monomer. This midstream process requires specialized continuous reactors, stringent temperature and pressure control, and effective purification techniques (such as distillation) to achieve the required industrial or specialty purity grades. Manufacturers in this stage must prioritize operational scale to achieve cost competitiveness, while simultaneously investing in quality assurance protocols necessary for specialized markets like medical devices. Differentiation is achieved through process technology licensing, ensuring consistent quality, and managing inventory levels effectively to respond to fluctuating downstream demand without compromising product stability, as IOA must be stabilized against premature polymerization during storage and transit.

Downstream analysis encompasses the formulation and end-use application of IOA. The distribution channel is bifurcated into direct sales for large bulk consumers (e.g., major coating companies or PSA manufacturers) and indirect distribution through chemical distributors and agents, serving smaller specialty formulators. Direct channels offer cost efficiency and tighter supply management, while indirect channels provide market reach and technical support for specialized small-volume users. The ultimate buyers transform the IOA monomer into finished products—adhesives, protective coatings, sealants, or specialty polymer resins—which are then utilized across high-growth sectors such as high-speed labeling in logistics, structural bonding in modern construction, and high-performance films in electric vehicle battery components, completing the value flow from petroleum derivatives to advanced functional materials.

Potential customers for Isooctyl Acrylate are diverse multinational corporations and specialized formulators primarily operating within the high-performance materials sector, where the monomer's flexibility and adhesion promotion qualities are indispensable. The largest cohort of potential buyers includes major adhesive and sealant manufacturers specializing in Pressure Sensitive Adhesives (PSAs), especially those producing tapes, labels, and graphic films for consumer electronics, automotive interior parts, and general industrial assembly. These companies require bulk quantities of high-purity IOA to serve as the foundational polymer backbone for their solvent-based, water-based, or UV-curable adhesive formulations, valuing suppliers who can guarantee stable supply, consistent quality, and competitive bulk pricing through reliable logistics networks spanning major industrial hubs.

Another significant customer base exists within the global coatings industry, encompassing large paint and resin producers focusing on industrial maintenance coatings, protective automotive topcoats, and durable architectural paints. These end-users incorporate IOA into their formulations to enhance the coating's elasticity, impact resistance, and weatherability, ensuring longevity and performance, particularly in extreme environments. The shift towards low-VOC and solvent-free systems means that formulators are increasingly seeking IOA and its derivatives compatible with these environmentally stringent systems, thus positioning customers who are pioneering UV-curable and electron-beam curing technologies as key high-value targets for IOA suppliers. These customers often engage in extensive R&D collaboration with IOA producers to develop customized monomer blends.

Furthermore, specialized segments such as medical device manufacturers and the rapidly growing electronics sector represent high-growth, high-margin potential customers. Medical buyers utilize ultra-high purity IOA for applications requiring biocompatibility and skin adhesion, such as transdermal drug delivery patches and surgical tapes, demanding rigorous quality control and certification from suppliers. Electronics companies use IOA-based optically clear adhesives (OCAs) and protective films for display screens, battery assemblies, and flexible circuits, prioritizing suppliers who can deliver monomers with minimal impurities and precise compositional consistency to prevent defects in high-tech manufacturing processes, driving demand for specialized, premium-grade products.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $450.5 Million |

| Market Forecast in 2033 | $690.8 Million |

| Growth Rate | 6.3% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Dow Chemical Company, Arkema SA, Mitsubishi Chemical Corporation, Nippon Shokubai Co., Ltd., Evonik Industries AG, LG Chem, Formosa Plastics Corporation, SIBUR Holding PJSC, Wanhua Chemical Group Co., Ltd., China Petroleum & Chemical Corporation (Sinopec), CNPC, Kowa Group, Taizhou Suning Chemical Co., Ltd., Fushun Petrochemical Company, Sanmu Group, Nipro Corporation, KH Neochem Co., Ltd., Hexion Inc., and Specialty Chemical Company X. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Isooctyl Acrylate market is characterized by continuous refinement in two primary areas: optimizing the synthesis process and advancing stabilization and purification techniques to meet the increasing demand for high-purity grades. The synthesis of IOA typically relies on direct esterification catalyzed by strong acids, but modern advancements focus on enzymatic esterification or reactive distillation techniques. These newer methods offer significant environmental benefits by reducing energy consumption, minimizing waste byproduct formation, and often increasing reaction selectivity, leading to higher monomer yield and reduced purification complexity. Furthermore, the utilization of continuous flow reactor technology, as opposed to traditional batch processing, is gaining traction among leading producers, allowing for better process control, enhanced safety, and greater consistency in product quality, which is vital for specialty applications.

A critical technological focus area involves stabilizing the IOA monomer against premature polymerization during storage, transport, and processing. Acrylate monomers are highly reactive, and technological innovations center on developing and implementing highly effective, yet regulatory-compliant, polymerization inhibitors. Research is actively exploring non-phenolic and low-migration inhibitors that maintain stability without negatively impacting the performance of the final polymer or the subsequent curing processes, particularly in UV-cured systems where initiator interactions are critical. Advanced monitoring systems, often incorporating AI and IoT sensors, are also being deployed within storage tanks and logistics networks to maintain optimal conditions and prevent thermal runaway incidents, thereby enhancing supply chain reliability and ensuring monomer integrity upon delivery to the end-user formulators.

Furthermore, technology related to downstream application methods is significantly influencing IOA demand. The widespread adoption of UV-curing technology in coatings and adhesives necessitates IOA grades optimized for fast reaction rates and minimal yellowing. Manufacturers are developing IOA derivatives and specialized co-monomers that integrate seamlessly into these fast-paced, high-throughput curing lines. The innovation in polymerization technology is also leading to the production of specialized IOA oligomers and prepolymers, which offer formulators enhanced control over final product properties, such as viscosity, adhesive tack, and peel strength, catering directly to the bespoke requirements of the medical, aerospace, and high-end automotive sectors. The ability to customize the molecular weight distribution and functional groups via controlled polymerization techniques is a core competitive technological advantage in this market.

The demand for IOA is overwhelmingly driven by the Pressure-Sensitive Adhesives (PSAs) industry for manufacturing high-performance tapes, labels, and protective films, where its low glass transition temperature ensures superior flexibility and tack. Secondary drivers include specialized architectural and automotive coatings, and sealant formulations requiring elasticity and durability.

IOA production relies heavily on petrochemical derivatives, specifically acrylic acid and isooctyl alcohol. Volatility in crude oil and natural gas prices directly translates to fluctuating production costs for IOA manufacturers, leading to price instability for end-users and often prompting manufacturers to implement sophisticated hedging strategies and long-term supply contracts.

Asia Pacific (APAC), particularly driven by industrial expansion in China and India, represents the region with the highest consumption volume and fastest projected growth rate. This surge is fueled by rapid urbanization, substantial growth in domestic manufacturing, and increasing infrastructure development projects.

Key technological advancements include the adoption of continuous flow reactors for enhanced efficiency and consistency, development of highly effective non-phenolic polymerization inhibitors for product stability, and ongoing research into sustainable bio-based synthesis routes to mitigate reliance on fossil fuel feedstocks and meet green chemistry standards.

The primary difference lies in the Purity Level. Industrial grade (typically 99.0%) is used for high-volume applications like general coatings and sealants. Specialty grade (99.5% and higher) is mandatory for sensitive applications such as medical adhesives and optically clear adhesives (OCAs) in electronics, demanding stringent impurity controls and often commanding a significant price premium due to specialized purification processes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.