ID : MRU_ 443773 | Date : Feb, 2026 | Pages : 248 | Region : Global | Publisher : MRU

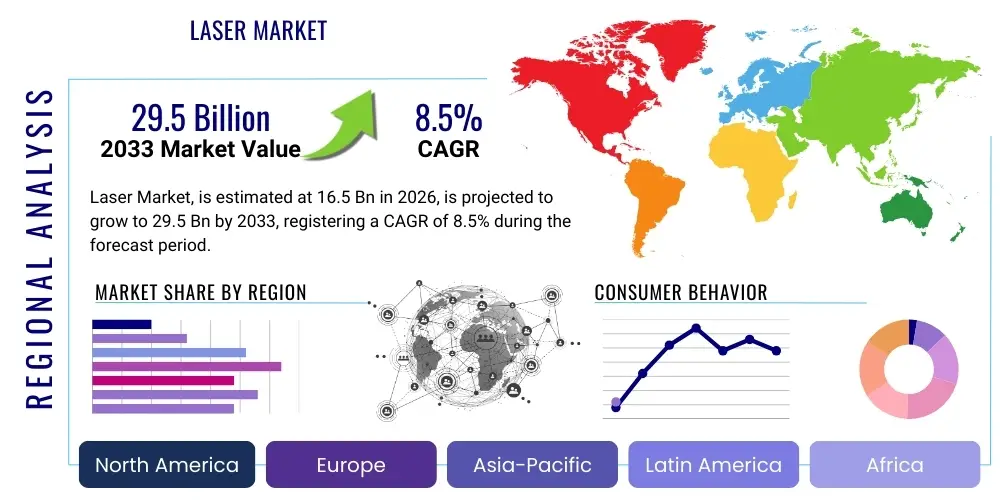

The Laser Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 16.5 Billion in 2026 and is projected to reach USD 29.5 Billion by the end of the forecast period in 2033. This robust expansion is primarily driven by escalating demand across advanced manufacturing sectors, particularly in microelectronics, and the continuous integration of high-power fiber lasers in material processing applications, which require precision and speed unobtainable through conventional methods. Furthermore, the increasing adoption of laser technologies in minimally invasive surgical procedures and sophisticated diagnostic tools within the healthcare industry contributes significantly to this upward trajectory, solidifying the laser market's critical role in technological advancement globally.

The forecasted growth trajectory reflects substantial investments in research and development aimed at improving laser efficiency, reducing operational costs, and expanding wavelength versatility. Emerging economies, notably in the Asia Pacific region, are rapidly adopting advanced laser systems for industrial automation and infrastructure development, thereby providing a major impetus for market expansion. Competitive dynamics emphasize strategic mergers and acquisitions among key players to consolidate technological expertise and secure intellectual property related to next-generation laser sources, such as ultrafast and quantum cascade lasers, ensuring sustained growth throughout the forecast period and beyond.

The Laser Market encompasses the manufacturing, distribution, and application of various coherent light sources across a multitude of industries. Lasers, characterized by their monochromatic, directional, and highly focused light output, serve as fundamental tools in modern technology. Product descriptions span several types, including Solid-State Lasers (e.g., Nd:YAG, DPSS), Gas Lasers (e.g., CO2, Excimer), Fiber Lasers, and Semiconductor Lasers (Diode Lasers), each offering unique performance characteristics tailored to specific requirements such as power output, pulse duration, and wavelength. Major applications are diverse, ranging from high-precision material processing (cutting, welding, marking) in automotive and aerospace sectors, to advanced communication technologies (fiber optics), scientific research (spectroscopy, quantum computing), and therapeutic and cosmetic treatments in healthcare.

The primary benefits derived from laser technology include unparalleled precision, non-contact processing capabilities, high energy efficiency, and operational speed, leading to enhanced productivity and reduced waste in manufacturing environments. Driving factors underpinning the market expansion include the miniaturization trend in electronics necessitating precise micro-processing tools, the increasing global demand for high-speed internet infrastructure requiring advanced optical communication systems, and the rising prevalence of chronic diseases demanding sophisticated medical laser devices. Moreover, technological advancements focusing on higher beam quality and increased power scalability, especially in the fiber laser segment, are continually opening new application avenues. Regulatory frameworks supporting the use of lasers in industrial safety and medical device standards further bolster market confidence and adoption rates across developed nations.

The Laser Market exhibits robust growth propelled by synergistic business trends, favorable regional expansion, and diversified segment performance. Key business trends include the shift toward higher power, higher efficiency laser systems, particularly fiber and ultrafast lasers, which are replacing traditional manufacturing methods due to their superior performance characteristics and lower total cost of ownership. Strategic alliances focusing on vertically integrated supply chains, from crystal growth to final system integration, are becoming common among industry leaders to secure raw material access and maintain competitive pricing. Additionally, significant investments in software and control systems that enable precise automation of laser processes are enhancing overall productivity and expanding the scope of laser applicability in Industry 4.0 environments.

Regional trends indicate that the Asia Pacific (APAC) region remains the dominant growth engine, driven by massive investments in consumer electronics manufacturing, automotive production, and expanding telecommunications infrastructure in China, South Korea, and Japan. North America and Europe continue to be crucial markets, characterized by high adoption rates of advanced medical lasers and specialized industrial applications, alongside robust government funding for scientific research utilizing high-end spectroscopic and imaging laser systems. Segment trends reveal that the Material Processing application segment holds the largest market share, fueled by the demand for precision cutting and additive manufacturing (3D printing). Concurrently, the Fiber Laser segment is experiencing the fastest growth rate due to its efficiency, reliability, and scalability across numerous industrial tasks.

Analysis of common user questions regarding the intersection of Artificial Intelligence (AI) and the Laser Market reveals significant thematic focuses centered on optimization, automation, and predictive maintenance. Users frequently inquire about how AI algorithms can enhance laser beam steering accuracy, optimize process parameters in real-time for complex materials (e.g., in welding or additive manufacturing), and predict component failure, such as diode aging, within high-power laser systems. The key concerns revolve around the cybersecurity risks associated with integrating smart, connected laser systems and the need for standardized data protocols to facilitate effective machine learning training. Expectations are high regarding AI’s ability to unlock new levels of precision and efficiency, fundamentally transforming quality control and throughput in laser-based manufacturing environments, moving the industry toward fully autonomous operation.

AI's influence extends deeply into the development cycle and operational efficiency of laser systems. In material processing, AI-driven machine vision systems are increasingly used for defect detection and real-time adjustment of laser power based on material feedback, maximizing quality and minimizing material waste. Furthermore, in medical applications, AI assists in image processing for laser surgery guidance and treatment planning, improving outcomes and patient safety. This integration requires significant collaboration between laser manufacturers and specialized software developers to embed sophisticated algorithms directly into the laser control hardware.

The dynamics of the Laser Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities, which collectively constitute the Impact Forces influencing market growth and direction. Key drivers include the global expansion of the microelectronics industry, particularly the production of advanced semiconductors and displays, which heavily rely on excimer and ultrafast lasers for precise patterning and annealing processes. Furthermore, the strong push toward industrial automation and the adoption of Industry 4.0 paradigms mandate the deployment of sophisticated laser systems for high-throughput manufacturing. However, the market faces restraints such as the high initial investment cost associated with advanced high-power laser systems and the stringent regulatory hurdles, particularly in the medical device sector, which mandate extensive testing and certification processes, potentially delaying product launch and market entry for smaller innovators.

Opportunities are abundant, particularly in emerging technological domains. The development of quantum cascade lasers (QCLs) offers significant opportunities in sensing and spectroscopy for environmental monitoring and security applications, leveraging their mid-infrared wavelength capabilities. The growing market for electric vehicles (EVs) also presents a major opportunity, requiring specialized high-power laser welding techniques for battery manufacturing and structural joining. The impact forces are generally weighted toward growth drivers, given the irreplaceable nature of laser technology in high-precision, high-speed applications. The rapid advancement in fiber laser technology has mitigated some cost restraints by offering increased energy efficiency and reliability compared to older laser types, thus accelerating overall market penetration across diverse industrial sectors globally.

The Laser Market is extensively segmented based on Type, Application, and End-Use Industry, reflecting the diverse technological landscape and specialized requirements across sectors. This structured segmentation allows market participants to identify niche opportunities and tailor product development strategies effectively. The 'Type' segmentation distinguishes between the fundamental technologies employed (e.g., Solid-State, Gas, Fiber), while the 'Application' segmentation delineates the functional use cases (e.g., Material Processing, Communications, Medical). The 'End-Use Industry' view categorizes buyers based on their primary operational sector, such as Automotive, Telecommunications, or Healthcare. Understanding these segment dynamics is crucial, as performance requirements—such as power output in industrial manufacturing versus beam quality in scientific research—vary significantly, influencing product design and market pricing strategies.

The dominance of Fiber Lasers is a prominent trend within the Type segmentation, largely owing to their superior efficiency, compact size, and maintenance-free operation compared to conventional CO2 or solid-state lasers in high-power applications. Meanwhile, the Application segmentation is heavily skewed towards Material Processing, which includes complex processes like laser ablation, micromachining, and laser marking, essential for modern production lines. Geographically, market behavior and segment preferences differ; for instance, semiconductor lasers find maximum penetration in the Communication and Data Storage segments globally, driven by infrastructure demands, whereas high-power industrial lasers are concentrated in regions with robust heavy manufacturing bases.

The Laser Market value chain is intricate, commencing with highly specialized upstream activities involving the sourcing and processing of critical raw materials. Upstream analysis focuses on key components such as specialized rare earth elements (for fiber doping), gain media crystals (like Nd:YAG or Yb:YAG), semiconductor wafers for diode manufacturing, and high-purity gases for gas lasers. Component manufacturers (suppliers of pump diodes, optics, beam delivery systems, and power supplies) hold significant leverage, as the quality and performance of these components directly determine the final laser system's efficiency and reliability. Vertical integration is increasingly utilized by large laser manufacturers to mitigate supply chain risks and control component quality, enhancing overall profitability and competitive positioning in the global market.

The midstream involves the core manufacturing and assembly of the laser sources and systems, requiring advanced cleanroom facilities, complex optical alignment, and thermal management expertise. Downstream analysis focuses on the integration and distribution channels, where systems integrators customize laser modules for specific industrial machines or medical devices. Distribution channels are bifurcated into direct sales for high-volume, standardized industrial systems and indirect channels utilizing regional distributors and value-added resellers (VARs) who provide localized installation, maintenance, and application support. The shift toward software-defined laser processes has also introduced independent software vendors (ISVs) as a crucial part of the downstream value delivery.

The profitability across the value chain is highest in the upstream component manufacturing and the specialized systems integration/software development segments, where intellectual property and technological know-how create significant barriers to entry. Direct distribution channels are prevalent for major Tier 1 manufacturers dealing with large industrial clients (e.g., automotive OEMs), ensuring tight control over service and relationship management. Conversely, indirect channels are vital for penetrating geographically dispersed small and medium-sized enterprises (SMEs) and specialized scientific research institutions, offering necessary local support and rapid turnaround times for specialized configurations.

Potential customers for the Laser Market are broadly categorized by their end-use industry, reflecting the technology's versatile utility. The largest segment of end-users are within the Industrial Manufacturing sector, comprising automotive companies, aerospace manufacturers, electronics producers, and heavy machinery fabricators. These entities procure high-power and ultrafast lasers for precision cutting, welding of complex materials (including dissimilar metals), marking/engraving for traceability, and advanced additive manufacturing processes. The driving factor for this customer base is the necessity for repeatable, high-quality output and increased production throughput mandated by global competitiveness and stringent quality standards.

Another crucial customer segment is the Telecommunications and IT infrastructure industry, which relies extensively on semiconductor lasers (VCSELs, edge-emitting lasers) for fiber optic communication, data transmission across data centers, and optical storage devices. The continual explosion of data traffic worldwide mandates ongoing upgrades and expansion of optical networking infrastructure, ensuring consistent demand for high-performance, cost-effective semiconductor laser components. Furthermore, the Healthcare sector represents a rapidly growing customer base, including hospitals, specialized clinics (dermatology, ophthalmology), and medical device manufacturers, purchasing diverse laser systems for surgical procedures, diagnostics, and aesthetic treatments, driven by the demand for less invasive and more precise medical interventions.

The Defense and Scientific Research sectors also serve as significant high-value customers. Military applications include laser targeting, directed energy weapons, and advanced surveillance systems, while research institutions and universities purchase high-end, complex laser systems (e.g., tunable lasers, femtosecond lasers) for fundamental physics research, quantum studies, and advanced material analysis. These customers prioritize performance, stability, and customization, often requiring bespoke solutions from specialized suppliers. The diversity of these end-user segments underscores the laser market's stability and resilience against economic fluctuations in any single industrial domain.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 16.5 Billion |

| Market Forecast in 2033 | USD 29.5 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Coherent Corp., IPG Photonics, TRUMPF, Lumentum Holdings, MKS Instruments (Newport), Novanta Inc., Jenoptik, Han's Laser Technology Industry Group Co., Ltd., Maxphotonics Co., Ltd., Raycus Fiber Laser Technologies Co., Ltd., nLight, Inc., 3D Systems, Laserline GmbH, II-VI Incorporated, Rofin-Sinar Technologies (now part of Coherent/TRUMPF), CY Laser SRL, GSI Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Laser Market's technological landscape is characterized by rapid innovation focused primarily on enhancing beam quality, increasing power efficiency, and achieving shorter pulse durations. Fiber laser technology stands as a cornerstone, dominating the industrial segment due to its excellent beam confinement, superior thermal management, and high wall-plug efficiency. Recent advancements in fiber lasers involve the development of single-mode high-power sources exceeding 10kW, enabling faster and deeper penetration welding critical for the electric vehicle and aerospace industries. Furthermore, wavelength diversification is a key trend, with significant R&D dedicated to developing green and UV fiber lasers for processing highly reflective materials like copper and gold, which are essential in electronics manufacturing.

Ultrafast lasers, including femtosecond and picosecond systems, represent the technological vanguard, moving from specialized research tools to mainstream industrial applications. Their ability to deliver high peak power over extremely short durations enables "cold ablation," minimizing thermal damage and providing exceptional precision for micro-machining complex substrates such as glass, sapphire, and advanced composites used in consumer electronics displays and medical implants. This high-precision capability ensures that the market for ultrafast lasers will continue to expand rapidly, particularly as costs decrease due to optimized manufacturing processes and component standardization.

Another critical area of technological focus is the development of Vertical-Cavity Surface-Emitting Lasers (VCSELs). While lower power, VCSEL arrays offer high integration density, excellent reliability, and low manufacturing costs, making them indispensable in 3D sensing, facial recognition systems, LiDAR, and high-speed data communications within data centers. Their semiconductor-based architecture allows for wafer-level mass production, which is crucial for meeting the scalability requirements of the consumer electronics and automotive safety markets. Continuous improvements in VCSEL power efficiency and temperature stability are driving their broader adoption across numerous sensing and illumination applications.

The primary factor is the widespread adoption of Industry 4.0 and industrial automation, demanding high-precision, high-speed, and non-contact material processing solutions like fiber and ultrafast lasers for cutting, welding, and micromachining in sectors such as automotive and electronics manufacturing, enhancing productivity and quality control globally.

Fiber laser technology exhibits the fastest growth rate due to its exceptional efficiency, superior beam quality, high reliability, and low maintenance requirements. Its scalability in power output makes it ideal for replacing older CO2 and solid-state systems across various demanding industrial applications, offering better lifetime operational cost efficiency.

AI integration significantly enhances operational efficiency by enabling real-time process monitoring, automated quality inspection through machine vision, and predictive maintenance capabilities. This leads to optimized laser parameters, minimized material waste, higher throughput, and reduced unplanned system downtime in critical manufacturing environments.

The Asia Pacific (APAC) region dominates the consumption of laser technologies. This dominance is attributed to the massive scale of manufacturing operations in countries like China and South Korea, particularly in consumer electronics, semiconductor fabrication, and expanding electric vehicle production, requiring high volumes of sophisticated laser systems.

The main restraints include the substantial initial capital investment required for high-power or ultrafast laser systems, the need for specialized technical expertise for installation and maintenance, and complex regulatory compliance procedures, particularly for highly specialized medical laser devices entering new markets.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.