ID : MRU_ 443840 | Date : Feb, 2026 | Pages : 249 | Region : Global | Publisher : MRU

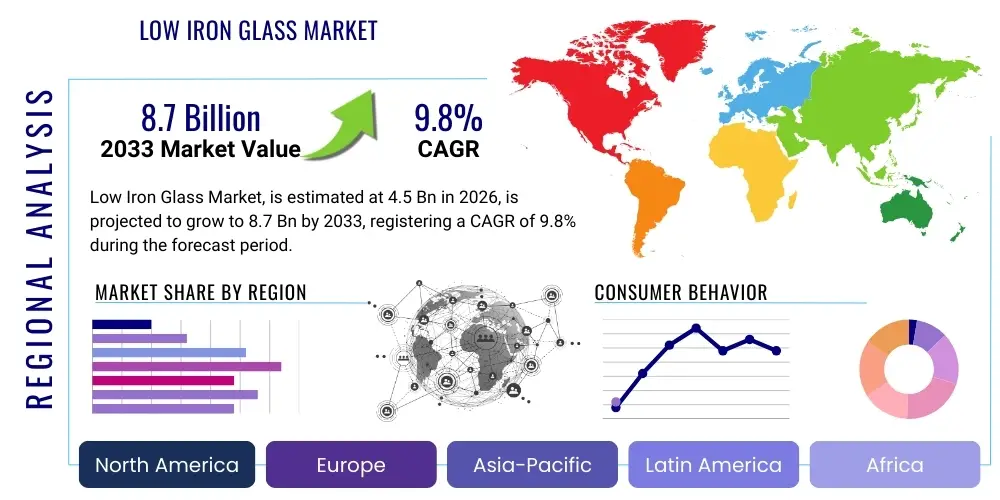

The Low Iron Glass Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 8.7 Billion by the end of the forecast period in 2033. This robust expansion is predominantly fueled by the global shift towards renewable energy infrastructure, particularly the burgeoning demand within the photovoltaic (PV) solar panel manufacturing sector, where high transparency and maximum light transmission are critical for efficiency optimization. Simultaneously, the architectural design industry's increasing preference for aesthetically superior, ultra-clear glass in high-end commercial and residential construction projects further bolsters market valuation, positioning low iron glass as a premium construction material essential for modern sustainable design.

The Low Iron Glass Market encompasses the production and distribution of highly transparent glass characterized by a significantly reduced iron oxide content compared to standard float glass. This reduction minimizes the green tint typically visible in thicker glass panels, thereby enhancing light transmission rates—often exceeding 91%—and offering superior clarity. Low iron glass, often referred to as ultra-clear glass, is manufactured using specialized raw materials and refined melting processes, which are pivotal in achieving its distinct optical properties. Its superior clarity makes it indispensable across various high-precision and high-performance applications where maximizing light entry and minimizing color distortion are paramount.

Major applications of low iron glass span key industrial and commercial sectors. In the renewable energy sector, it is the standard material for solar photovoltaic modules and thermal collectors, where even marginal increases in light transmittance translate directly into higher energy output efficiency, driving significant demand across major solar manufacturing hubs in Asia Pacific. Within the architectural and construction industries, low iron glass is extensively utilized in facades, skylights, interior partitions, display cases, and curtain walls, providing structures with unparalleled visual lightness and clarity, meeting stringent aesthetic requirements for modern, minimalist designs. The material’s high durability and potential for further processing (such as tempering, laminating, and coating) ensure its versatility across demanding environments.

The primary driving factors sustaining the market's rapid growth include supportive governmental policies promoting solar energy adoption and green building standards worldwide. Furthermore, continuous advancements in glass manufacturing technology, particularly in the large-format glass production necessary for utility-scale solar farms and expansive architectural installations, are improving cost-effectiveness and accessibility. The product's inherent benefits—including enhanced solar heat gain (when required), superior visual quality, and UV light blocking capabilities (when coated)—solidify its position as a critical material for sustainable and high-performance building envelopes and energy generation solutions, ensuring sustained market penetration throughout the forecast period.

The Low Iron Glass Market is currently defined by robust business trends, primarily stemming from the exponential growth of the global solar energy market, which constitutes the largest end-use segment and dictates pricing stability and technological advancements within the sector. Key business trends include the ongoing capacity expansion by major manufacturers, particularly in APAC, aiming to meet the scale requirements of large utility projects and capitalizing on the economies of scale. Furthermore, a rising trend involves strategic partnerships between glass producers and solar module integrators to ensure a stable, quality supply chain for advanced bifacial and thin-film solar technologies, necessitating glass with stringent optical tolerances and mechanical strength.

Regionally, the market exhibits strong bifurcation, with the Asia Pacific region dominating both production capacity and consumption, driven by massive domestic investments in renewable energy, notably in China and India, alongside accelerated urbanization requiring sophisticated architectural glass. North America and Europe, while possessing smaller manufacturing bases, represent high-value markets characterized by stringent quality specifications and a strong focus on high-performance building certifications (e.g., LEED, BREEAM), where low iron glass justifies its premium pricing through energy efficiency contributions. Emerging markets in Latin America and MEA are increasingly adopting the technology, propelled by new infrastructure projects and governmental goals related to diversification away from fossil fuels, contributing to a diversified global demand profile.

In terms of segmentation trends, the market for low iron tempered glass is expected to maintain leadership due to its mandated use in safety applications, particularly solar panel encapsulation and structural architecture. However, the laminated low iron glass segment is showing the fastest growth rate, fueled by its enhanced security features and acoustic insulation properties essential for high-rise buildings and noise-sensitive urban environments. Application-wise, while construction remains crucial, the solar application segment is anticipated to expand its market share significantly, driven by global energy transition mandates and the diminishing cost gap between solar power and conventional electricity sources, cementing low iron glass as a foundational material for future energy grids.

Common user inquiries concerning the impact of Artificial Intelligence (AI) on the Low Iron Glass Market center predominantly on optimizing complex manufacturing processes, ensuring ultra-high quality control, and improving supply chain resilience in a commodity-sensitive market. Users frequently ask how AI can reduce the inherently high cost of low iron glass production, specifically focusing on minimizing material waste during the highly technical float process and detecting microscopic defects that compromise optical clarity or mechanical integrity. Furthermore, there is significant interest in AI's role in predicting shifts in raw material prices (like high-purity silica sand) and optimizing complex logistics networks serving global solar manufacturing hubs. The overarching expectation is that AI integration will lead to higher production throughput, enhanced energy efficiency during glass melting, and a measurable reduction in the overall carbon footprint of glass manufacturing.

AI is already beginning to revolutionize several aspects of low iron glass manufacturing. In the initial batch preparation stage, machine learning algorithms analyze raw material purity data in real-time, adjusting batch compositions to maintain consistent iron oxide levels and chemical stability, which is vital for achieving the ultra-clear specification. During the high-temperature melting and float phases, predictive modeling uses sensor data (temperature, viscosity, thickness) to anticipate process anomalies hours before they occur, allowing operators to make proactive adjustments, thereby reducing scrap rates and ensuring continuous, optimized operation. This transition from reactive quality control to proactive process management is instrumental in addressing the inherent challenges of large-scale, high-quality glass production.

The most significant visible impact of AI is in quality assurance and defect detection. Traditional quality checks often rely on human visual inspection or basic machine vision, which can miss subtle internal defects or minute surface imperfections crucial for solar applications. AI-powered inspection systems, utilizing deep learning models trained on vast datasets of defect patterns, can instantly identify, classify, and map defects such as bubbles, stones, or microscopic scratches with far greater precision and speed than conventional methods. This rapid, automated defect detection ensures that only the highest quality glass, suitable for high-efficiency PV modules and premium architectural facades, reaches the end-user, drastically improving product consistency and reducing post-production failure rates, thereby enhancing the market's reliability and reputation.

The Low Iron Glass Market is highly influenced by a complex interplay of Drivers, Restraints, Opportunities, and broader Impact Forces that shape its trajectory and competitive landscape. The market’s primary impetus is the global commitment to sustainable development and the accelerated deployment of solar power generation capacity, which directly mandates the use of low iron glass for maximizing panel efficiency. Counterbalancing this strong demand are significant restraints, primarily the higher capital expenditure required for specialized manufacturing facilities and the resultant premium pricing compared to standard glass, which occasionally limits its adoption in budget-sensitive construction projects. Opportunities for growth lie mainly in integrating low iron glass into high-value applications such as smart glass technology and advanced automotive sunroofs, alongside exploring emerging thin-film solar technologies.

Drivers: The fundamental driver is the ongoing energy transition, where low iron glass is crucial for maximizing the efficiency of solar photovoltaic (PV) modules, a priority for governments aiming to achieve net-zero carbon goals. Supporting regulatory frameworks, such as feed-in tariffs and tax credits for renewable energy installations, create favorable investment climates for solar projects, subsequently driving bulk orders for ultra-clear glass. Furthermore, in the construction sector, increasing consumer and developer preference for aesthetically appealing, structurally sound, and high-performance building materials contributes substantially to market demand. Modern architectural trends emphasize natural light integration and transparency, making low iron glass an essential element of high-end commercial and residential designs.

Restraints: The most prominent constraint is the specialized and costly manufacturing process. Achieving extremely low iron content requires highly refined raw materials (low iron silica sand) and meticulous control over the float process, leading to higher operational expenses. This translates into a substantial price premium (often 20% to 40% higher) compared to conventional clear glass, presenting an affordability barrier for mass-market construction applications. Moreover, the production process is energy-intensive, and any volatility in global energy prices or raw material supply chains (which are concentrated geographically) can introduce significant operational risk and price instability, potentially hindering broader market accessibility and consistent supply.

Opportunities: Significant untapped potential exists in next-generation applications. The integration of low iron glass into smart glass technology—allowing for switchable privacy, dimming, or energy harvesting capabilities—opens up lucrative avenues in premium architectural and automotive segments. The demand for lightweight, durable low iron glass in thin-film solar applications, Building-Integrated Photovoltaics (BIPV), and advanced greenhouse glazing (optimizing specific light wavelengths for crop growth) represents diverse opportunities for technological differentiation and market penetration. Furthermore, geographical expansion into rapidly developing economies in Africa and Southeast Asia, where large-scale infrastructure and energy projects are commencing, offers new high-volume consumption centers.

Impact Forces: The market is subject to powerful external impact forces. Regulatory stringency regarding building codes (e.g., energy performance mandates and daylighting requirements) compels architects and engineers to specify high-transparency glass. Global trade dynamics, including anti-dumping duties or tariffs imposed on glass imports, particularly involving major Asian producers, significantly alter regional pricing structures and competitive strategies. Finally, the macro-economic stability of key consuming nations, particularly concerning government expenditure on renewable infrastructure and housing construction, directly correlates with market performance. Technological disruptions, such as the emergence of superior glass alternatives or cheaper manufacturing routes, pose a long-term transformative risk, requiring constant innovation from established market players.

The Low Iron Glass Market is comprehensively segmented based on Type, Application, and End-Use, reflecting the diverse requirements and technological specifications across various consuming industries. The segmentation is critical for understanding specific market dynamics, price points, and competitive intensity within niche areas. Low iron glass products are primarily categorized by their post-processing characteristics, determining their suitability for safety and structural functions. The application segmentation clearly delineates the market into the dominant energy sector and the rapidly evolving construction segment, each driven by distinct regulatory and technological needs. Geographic clustering of demand and manufacturing capacity also plays a crucial role in strategic planning and supply chain optimization for industry stakeholders, ensuring specialized products meet stringent regional standards.

The Type segment is crucial as it reflects the required performance characteristics, distinguishing between basic ultra-clear glass sheets and those modified for enhanced strength or security. Low iron tempered glass holds a commanding market share because of its mandatory use in solar panels (for impact resistance) and various architectural safety applications (doors, railings). The laminated segment, utilizing an interlayer like PVB or SentryGlas Plus, is gaining momentum due to its superior safety benefits, acoustic performance, and enhanced UV protection, essential for premium residential and commercial structures in densely populated areas. Furthermore, coated low iron glass, often applied with low-emissivity (Low-E) or anti-reflective (AR) coatings, represents a high-growth category, optimized specifically to balance solar heat gain and maximum light transmission, particularly for highly efficient building envelopes.

The Application segment highlights the disparity in demand volume and value contribution. The Solar Energy sector accounts for the largest share by volume, driven by utility-scale installations, requiring vast quantities of standardized, high-quality, ultra-clear glass cover sheets. Conversely, the Construction and Architecture segment often commands higher value per square meter, driven by customization, complex fabrication, and the integration of highly processed products (curved, insulated, or digitally printed low iron glass). The Display and Appliance segment, encompassing museum display cases, high-definition monitors, and premium white goods, while smaller, demands the highest level of optical clarity and finish, often utilizing thin-film low iron glass. Understanding these varied demands is essential for manufacturers tailoring their capacity and product mix effectively.

The value chain of the Low Iron Glass Market begins with rigorous upstream activities focused on securing and processing specialized raw materials. Unlike standard glass, low iron glass production necessitates high-purity silica sand, limestone, and soda ash with minimal iron content. Raw material sourcing involves specialized mining operations and advanced beneficiation processes to ensure the iron oxide concentration is consistently below the 0.01% threshold. The procurement stage is critical, as the quality of these raw materials directly dictates the final optical clarity and manufacturing yield. Manufacturers often establish long-term contracts with specialized suppliers to secure stable sourcing and maintain stringent quality specifications, mitigating the volatility often associated with high-ppurity minerals.

The core manufacturing stage involves the capital-intensive float glass process, where the molten mixture is floated onto a bath of molten tin to achieve uniform thickness and flawless surface finish, followed by annealing and cutting. This stage requires significant technological expertise and energy input. Post-processing activities, including tempering (heat treatment for strength), lamination (combining multiple layers with interlayers for security), coating (applying anti-reflective or low-E films), and edge work, add substantial value and customize the product for specific end-use applications like solar panels or structural facades. Efficiency in this midstream section is optimized through continuous process improvements and automation, often leveraging AI and advanced robotics to manage large, delicate glass sheets.

Downstream analysis focuses on distribution channels and the final consumption sectors. Due to the fragility and specialized nature of low iron glass, distribution relies heavily on specialized logistics providers equipped to handle large, oversized glass panels safely. Direct distribution channels are prevalent when supplying major photovoltaic manufacturers or large-scale architectural projects, involving direct negotiations and just-in-time delivery schedules to minimize storage costs and breakage risk. Indirect channels utilize specialized glass distributors and fabricators who perform cutting, etching, and installation services before reaching the final end-users in residential or commercial construction. The installer and fabricator segments hold considerable power in the downstream chain, as proper handling and integration are essential for the glass to perform according to its specifications.

The primary potential customers and end-users of low iron glass are broadly categorized into entities involved in large-scale energy production, high-end construction, and specialized display manufacturing, each valuing the material's unique optical properties for different functional requirements. Solar module manufacturers represent the single largest volume buyer segment, as the efficiency of their photovoltaic panels is directly correlated with the light transmittance of the cover glass, making low iron glass a non-negotiable component for achieving competitive power output ratings and meeting industry standards for utility-scale solar farms globally. These manufacturers typically seek jumbo-sized sheets, consistent quality, and long-term supply agreements to ensure cost-effective, continuous production.

Another major customer base includes commercial and high-end residential developers, architectural firms, and specialized glass fabricators. These customers specify low iron glass for premium applications such as structural glazing, expansive curtain walls, museum display cases, and interior partitions where minimizing color distortion and maximizing natural light are primary design objectives. Architectural clients value the superior aesthetics, demanding highly processed forms, including curved, laminated, or complex insulated glass units (IGUs). The decision-making process for these customers is influenced less by cost minimization and more by the material's aesthetic contribution, structural performance, and compliance with stringent energy efficiency and daylighting requirements in modern building codes.

Furthermore, specialized industrial buyers, including automotive manufacturers, are increasingly utilizing low iron glass for panoramic sunroofs and specialized instrumentation displays where high clarity and resistance to discoloration are vital for luxury and safety. The greenhouse agriculture sector is also a growing potential customer base, seeking optimized low iron glass solutions that transmit the specific light spectrum necessary for accelerated or enhanced crop growth, presenting a niche but high-value segment focusing on yield improvement and energy management within controlled environment agriculture (CEA) systems. These specialized customers require customized coating applications and specific thickness tolerances, often in smaller, tailored batches.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 8.7 Billion |

| Growth Rate | 9.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AGC Inc., Guardian Glass LLC, Saint-Gobain, Pilkington (NSG Group), Euroglas GmbH, Taiwan Glass Industry Corporation, China Glass Holdings Limited, Xinyi Solar Holdings Limited, Flat Glass Group Co. Ltd., Sisecam, Central Glass Co. Ltd., Schott AG, Jinjing Group Co., Vitro Architectural Products, CSG Holding Co., Nippon Sheet Glass (NSG), Kibing Group, AVIC Glass Co., Interpane Glas Industrie AG, Shanghai Yaohua Pilkington Glass Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing of low iron glass is deeply rooted in sophisticated advancements of the standard float glass process, requiring specialized technological applications to achieve exceptional clarity. The primary technological prerequisite involves highly controlled batch preparation using meticulously sourced, high-purity raw materials. Innovations in melt technology, specifically optimizing furnace design and fuel efficiency, are essential to maintain extremely stable, low-oxygen melting conditions necessary to prevent residual iron from converting into color-imparting compounds. Advanced sensor technology and process control systems are deployed throughout the float line to ensure precise temperature profiles and uniform ribbon formation, which minimizes optical distortion and ensures consistent thickness across large formats, critical for modern jumbo-sized architectural and solar applications.

The technology landscape is increasingly defined by post-processing and value-addition techniques. Chemical and thermal tempering processes are continuously being refined to enhance the mechanical strength and durability of ultra-clear glass without compromising its optical transmission capabilities. Laminating technology has evolved with the introduction of high-performance interlayers (e.g., SGP ionoplast interlayers) that offer superior rigidity and tear resistance, enabling the use of low iron laminated glass in demanding structural applications such as glass fins and bomb-blast resistant facades. This reliance on robust lamination technology is expanding the architectural scope for large, safe, and transparent structures, pushing the boundaries of material science in construction.

Furthermore, advanced coating technologies represent a high-growth technological area. Anti-reflective (AR) coatings, typically applied through vacuum deposition methods, are crucial for solar applications to maximize light capture and minimize surface reflection, often boosting PV panel efficiency by 2-3%. Simultaneously, sputtering technology is utilized to apply highly customized Low-E coatings onto the low iron substrate for energy-efficient building applications. These technological layers are engineered to selectively manage solar radiation, allowing visible light entry while reflecting specific infrared wavelengths, thereby reducing HVAC load and improving building sustainability performance. The convergence of glass chemistry, precision engineering, and surface modification techniques defines the competitive edge in the current low iron glass technology landscape.

Regional dynamics heavily influence the Low Iron Glass Market, driven by differential rates of solar adoption, governmental construction investments, and varying regulatory standards concerning energy efficiency and building materials.

Low iron glass, also known as ultra-clear glass, contains significantly less iron oxide (typically below 0.01%) than standard clear glass. This reduction eliminates the greenish tint, allowing low iron glass to achieve superior visible light transmittance, often exceeding 91%, making it ideal for solar panels and high-clarity architectural applications where color neutrality is essential.

The Solar Energy sector, particularly the manufacturing of photovoltaic (PV) modules, drives the highest volume demand for low iron glass. Its use is mandated in high-efficiency solar panels because maximizing light capture directly increases energy generation, offering a critical performance advantage over standard glass.

Manufacturers mitigate high production costs primarily through achieving massive economies of scale, particularly in the Asia Pacific region, and by implementing advanced manufacturing techniques such as AI-driven process optimization and superior defect detection systems that minimize waste (scrap rate) and improve energy efficiency during the intensive melting process.

Key technological advancements include the development of highly durable Anti-Reflective (AR) coatings, specifically for solar efficiency gains, and innovations in lamination technology (e.g., SGP interlayers) to create stronger, lighter, and safer structural glass units for complex, high-rise architectural facades.

Yes, low iron glass is crucial for sustainability. While its production is energy-intensive, its primary environmental contribution is through enhancing the efficiency and longevity of renewable energy systems (solar PV), which significantly offsets carbon emissions. Its use in green buildings also reduces lighting and heating loads, contributing directly to global energy conservation and net-zero targets.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.