ID : MRU_ 443488 | Date : Feb, 2026 | Pages : 241 | Region : Global | Publisher : MRU

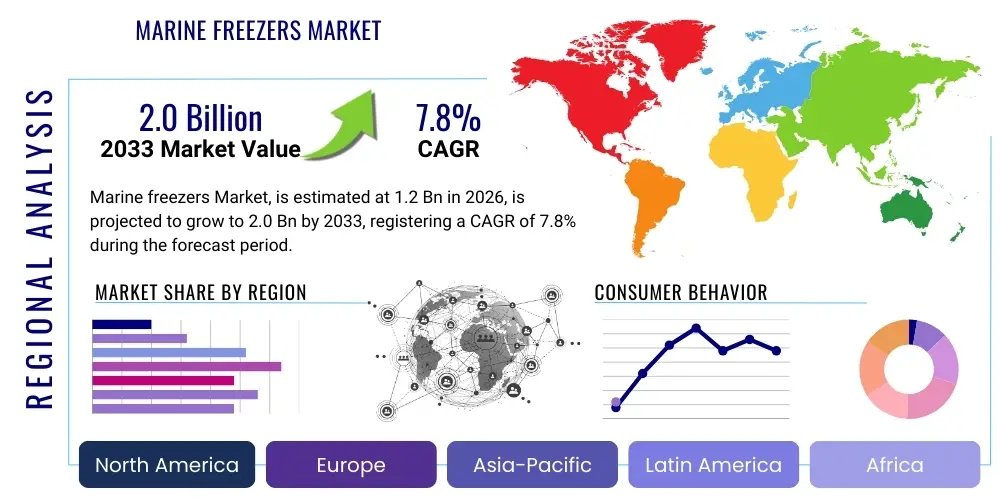

The Marine freezers Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at $1.2 Billion in 2026 and is projected to reach $2.0 Billion by the end of the forecast period in 2033.

The Marine Freezers Market encompasses the specialized segment of refrigeration equipment designed specifically for use in maritime environments, ranging from small recreational yachts to large commercial fishing vessels and naval fleets. These highly specialized units are engineered to withstand the unique and particularly harsh operating conditions encountered at sea, including constant exposure to salt spray, high ambient temperatures and humidity levels, continuous mechanical vibration and pitching/rolling motion, and fluctuating power supplies. To ensure operational longevity and reliability, marine freezers necessitate robust construction using corrosion-resistant materials, superior energy efficiency metrics, and components certified for maritime safety standards. Unlike standard domestic freezers which rely purely on stable AC power and benign climate conditions, marine freezers often incorporate features vital for sea use such as positive latching mechanisms to prevent doors from opening during heavy weather, sophisticated multi-zone insulation techniques, and the critical capability to operate effectively and efficiently on both AC (shore power or generator) and low-voltage DC (battery) electricity. This duality of power input capability, managed by advanced electronic controllers, is a fundamental characteristic differentiating marine refrigeration equipment from terrestrial counterparts and driving innovation within the sector.

Major applications for marine freezers span across several economically significant maritime sectors, dictating design specifications and capacity needs. In the vital commercial fishing industry, freezers are absolutely critical for preserving valuable catches, such as high-grade tuna or specialized seafood, immediately upon harvesting. This rapid freezing process is essential not only for maximizing product quality and market value before the vessel reaches port, but also for ensuring strict compliance with increasingly stringent global cold chain management and food safety regulations (such as HACCP certification). For the burgeoning market of recreational boaters, luxury yacht owners, and long-range cruisers, high-performance marine freezers significantly enhance the vessel’s endurance and cruising capabilities by allowing for extended, safe storage of high volumes of perishable provisions. Furthermore, highly specialized segments, including military/naval applications, offshore energy platforms, and scientific research vessels, rely on heavy-duty, often redundant, marine refrigeration solutions designed to maintain long-term, stable food supplies for personnel operating in highly remote, extreme, or extended-duration deployment missions, where reliability is non-negotiable.

Key benefits that are driving the accelerated market adoption include the scientifically measurable enhancement of food preservation quality, which translates directly into reduced spoilage and waste; significantly extended operational range and endurance for all types of vessels; and markedly improved overall operational efficiency achieved by minimizing the frequency and time required for essential restocking operations. Underlying driving factors propelling market expansion are the robust global expansion of recreational boating activity, especially in affluent regions; the continually increasing worldwide demand for high-quality, ethically sourced frozen seafood, necessitating efficient onboard preservation; the implementation of stringent international regulations regarding safe food preservation at sea; and perhaps most critically, continuous technological advancements focused squarely on improving energy consumption profiles and enhancing overall system reliability. This latter point is primarily achieved through the rapid adoption of highly efficient variable-speed compressors, advanced insulation compounds, and enhanced smart monitoring systems that provide real-time diagnostic feedback to operators and fleet managers globally.

The Marine Freezers Market is currently experiencing a trajectory of consistent, measured growth, intrinsically linked to the global economic stability affecting consumer leisure spending and the fundamental demands of international food trade logistics. Key business trends indicate a definitive market shift toward integrated, modular refrigeration solutions designed for maximum spatial optimization and ease of installation within standardized vessel designs. Furthermore, there is an escalating focus among major manufacturers on utilizing lighter, yet structurally more durable, materials to optimize onboard space utilization and critically reduce the vessel’s total power draw, thereby improving overall fuel efficiency. Leading market manufacturers are aggressively incorporating IoT and telematics capabilities, enabling centralized fleet management, remote performance monitoring, and rapid temperature deviation alerts. This connectivity appeals significantly to sophisticated, high-value commercial fishing operations and large yacht management firms seeking enhanced operational predictability and proactive predictive maintenance scheduling, minimizing costly non-scheduled downtime.

From a geographical perspective, established maritime economies in North America and Europe retain the largest share of the market, primarily driven by substantial historical investment in recreational marine infrastructure, high disposable incomes supporting luxury yachting, and mature commercial fishing industries requiring cyclical equipment replacement and technological upgrades. However, the Asia Pacific (APAC) region is strategically positioned to register the fastest growth rate over the forecast period. This acceleration is underpinned by the unprecedented expansion of the regional aquaculture sector, substantial growth in commercial fishing fleets—especially in nations like Vietnam, Indonesia, and India—and significant budgetary allocations towards naval fleet expansion and modernization programs across the region. This dynamic regional expansion is fueling robust demand not only for high-standard OEM equipment necessary for new vessel construction but also for aftermarket units utilizing the latest energy-efficient technologies tailored specifically for the challenges posed by tropical and sub-tropical operational environments.

Analyzing key segmentation trends reveals a notable preference evolution within the recreational segment towards highly accessible drawer-style and extremely compact portable freezers, which maximize ergonomic use and minimize intrusion in limited cabin and cockpit spaces. Conversely, the commercial sector is seeing simultaneous demand acceleration at both ends of the capacity spectrum: small, specialized deep-freeze units for artisanal or specific high-value catches, and massive, customized industrial freezing systems designed for rapid blast freezing of significant daily yields. Technologically, the defining trend continues to be the overwhelming shift towards DC-powered variable-speed compressor units, which offer vastly superior energy efficiency and performance stability compared to older, more rudimentary plate-style or eutectic cooling methodologies. This industry-wide emphasis on optimized energy performance is a direct reflection of the global push toward more sustainable, battery-optimized vessel operations, profoundly influencing the entire design and engineering philosophy of new marine refrigeration products.

Analysis of common user questions regarding AI's application in marine refrigeration systems demonstrates a focused desire for enhanced operational predictability and dynamic energy optimization. Users frequently query how sophisticated AI can effectively mitigate the risk of catastrophic system failures during extended, isolated voyages, where immediate repair is impossible. They are keenly interested in whether AI-driven systems possess the capability to autonomously adjust crucial cooling cycles in real-time, factoring in variables such as fluctuating ambient air and water temperatures, immediate vessel power availability (especially crucial for solar or hybrid vessels), and historical usage patterns. Furthermore, there is strong expectation regarding the potential for AI to implement fully autonomous, continuous fault detection and complex diagnostic routing. The overriding theme derived from user inquiries is the necessity of moving marine freezers beyond simple temperature control and establishing them as active, intelligent, and predictive components within the larger integrated vessel management system, ensuring maximal thermal stability, reducing operational expenditure, and eliminating the need for constant human oversight or manual adjustments.

The application of sophisticated Artificial Intelligence methodologies within high-end marine freezers focuses primarily on developing highly accurate predictive maintenance algorithms and achieving unparalleled levels of energy consumption optimization. AI systems are programmed to continuously analyze multiple real-time data streams—including data points such as the compressor’s mechanical performance signature, minute internal temperature fluctuation rates, external ambient temperature and humidity, condenser water inlet/outlet temperatures, and input power stability—to identify subtle, often imperceptible deviations that serve as precursors to pending equipment failure. This crucial diagnostic capability empowers vessel engineering staff or remote fleet operators to schedule proactive, non-emergency maintenance interventions while the vessel is still underway or during routine port calls. This preemptive approach is vital for preventing major breakdowns that would severely compromise stored goods, which is a financial necessity for high-value commercial seafood catches and a logistical imperative for long-duration naval or research missions operating far from repair facilities.

Furthermore, the integration of AI technologies enables extraordinarily complex load forecasting and optimized inventory management for large-scale marine installations, especially prominent on industrial fishing trawlers or large cruise ships. On a commercial fishing vessel, for instance, a machine learning model can correlate instantaneous freezing activity with current catch rates, subsequent volumetric storage density, and the required pull-down temperature schedule. This optimization ensures that temperature requirements are consistently met without generating excessive, detrimental peak loads on the vessel's often sensitive electrical grid. This precision in load management significantly improves the unit's overall energy footprint, directly reducing the required fuel consumption linked to auxiliary power generation, translating immediately into tangible operational cost savings. As marine communications infrastructure continues to mature, the foundational role of machine learning in providing centralized, multi-vessel fleet management diagnostics, anomaly detection, and operational benchmarking is rapidly evolving from a niche feature into a standardized expectation for leading marine freezer system providers globally.

The Marine Freezers Market is strategically positioned at the intersection of powerful economic and technological forces that dictate its long-term growth and structural evolution. The primary drivers underpinning market expansion are inherently linked to globalized trade dynamics, specifically the continually increasing international flow of highly perishable goods, particularly premium seafood, which necessitates meticulous, reliable cold chain logistics from the specific point of harvest to the final consumer market. Simultaneously, the sustained global expansion of the luxury recreational yachting sector, propelled by rising global affluence and increased leisure expenditure in both developed and rapidly emerging economies, generates consistent demand for compact, aesthetically advanced, highly energy-efficient, and structurally integrated onboard refrigeration and freezing systems. Furthermore, ongoing technological breakthroughs, particularly concerning the widespread availability of high-efficiency variable-speed DC compressors (such as those supplied by dominant players like Secop and Danfoss) and the innovative application of advanced insulation materials (like space-saving vacuum insulated panels), serve as crucial market enablers by drastically reducing the vital power draw of the equipment—an absolute necessity on any marine vessel where energy conservation is prioritized.

Conversely, several significant constraints impose limitations on the market’s pace of proliferation. The exceptionally high initial capital expenditure associated with purchasing and installing specialized, certified marine-grade freezers remains the most significant impediment. This cost differential, often several times that of equivalent standard domestic units, strongly restricts adoption among smaller-scale independent vessel owners or commercial operations working under strict capital budget constraints. Operational challenges further compound these restraints, including the inherent reliance on a perfectly stable, high-quality power supply—which is frequently challenging to guarantee in underdeveloped ports or during generator failures—and the highly specialized nature of the maintenance required for complex refrigerant systems while operating hundreds or thousands of miles offshore. Additionally, the corrosive marine environment itself acts as a profound structural restraint; constant exposure to high salinity, severe humidity, and relentless structural vibration accelerates the degradation of even the highest quality components, necessitating significantly more frequent and costly replacements, thereby substantially inflating the long-term Total Cost of Ownership (TCO) for operators.

Significant growth opportunities for manufacturers are concentrated primarily in aggressive emerging market penetration, particularly within developing coastal nations actively scaling up their indigenous commercial fishing capacity, modernizing their existing fleets, and investing heavily in naval readiness. These nations present vast, untapped avenues for high-volume sales of highly durable, fundamentally reliable, and cost-effective commercial units. A major future opportunity lies in aligning with the accelerating trend towards sustainable and ‘green’ boating initiatives. This offers manufacturers a clear pathway to capture a premium market segment by developing and aggressively marketing freezers that utilize environmentally benign, natural refrigerants (such as R290 propane or R600a isobutane) and are engineered for seamless integration with renewable energy generation systems like advanced solar arrays and next-generation high-capacity lithium battery banks. Critical external impact forces include the ongoing threat of technological substitution from increasingly effective alternative preservation technologies (e.g., specialized chilling methods or high-pressure processing), the binding influence of stringent international maritime environmental protocols (specifically those mandating the swift phase-out of high Global Warming Potential F-Gas refrigerants), and the economic volatility inherent in the global shipbuilding and luxury yachting sectors, which have a direct, measurable correlation with the demand for new marine refrigeration installations.

The Marine Freezers Market exhibits a complex segmentation framework, categorized rigorously based on fundamental design type, total cooling capacity, specialized intended maritime application, and primary power source utilized, effectively reflecting the highly specialized and diverse operational requirements of the global maritime community. Detailed analysis across these distinct segments is fundamentally vital for manufacturers, enabling them to finely tune their product development pipelines, optimize supply chain logistics, and precisely target marketing efforts, ensuring that highly specialized refrigeration solutions are effectively matched to the distinct needs of recreational cruisers versus industrial-scale commercial freezing operations. For example, segmentation by Type clearly differentiates robust chest models—overwhelmingly preferred in the commercial sector for their superior thermal retention and massive internal volume—from integrated drawer or sleek upright models which are mandated by luxury yacht designers for maximizing ergonomic integration and aesthetic appeal within confined living quarters. Capacity segmentation determines applicability, ranging widely from ultra-compact, highly portable units sufficient for short day trips to mammoth, purpose-built, permanent deep-freeze systems engineered for processing and storing thousands of kilograms of frozen catch daily.

The overall market structure is primarily defined by its two principal purchasing avenues: the Original Equipment Manufacturer (OEM) segment and the dynamic Aftermarket segment. The OEM channel involves direct supply to shipyards and major vessel builders who integrate the freezers as standard components during the initial construction of new vessels, often requiring highly specific custom engineering and extensive technical partnership support throughout the vessel design process. The Aftermarket segment, conversely, provides a vital pathway for replacement units, technological upgrades, and refit projects on existing vessels, capitalizing on the cyclical nature of marine equipment lifespan. Technological categorization further refines the market, distinguishing between legacy AC-powered systems (often reserved for high-power fixed installations), the increasingly dominant, highly efficient DC-powered units utilizing advanced variable-speed compressors, and specialized systems like eutectic or plate-based freezing methods that are deployed in specific, often smaller commercial or dedicated backup scenarios requiring passive cooling capability.

The market dynamics within each detailed segment are intrinsically influenced by regional differences in maritime traditions (e.g., Asian vs. European fishing techniques), prevailing governmental fishing quotas, the stringency of the local environmental and safety regulatory environment, and, critically, the fluctuating global economic health and investment levels within the heavy shipbuilding and leisure yachting industries. Continuous innovation is pushing convergence, particularly in the mid-range capacity segment, where manufacturers are striving to produce highly durable, efficiently insulated units that satisfy both the stringent power constraints of long-distance cruising yachts and the rugged reliability demands of smaller, independent commercial fishing operators. This pressure for multi-functional, high-performance units is reshaping material science applications within the sector, prioritizing lightness, structural strength, and unparalleled thermal performance.

The Marine Freezers Market value chain initiates with intensive upstream analysis and strategic component procurement, which is critically dependent upon specialized industrial inputs. This phase involves sourcing crucial, high-technology components, including the supply of high-efficiency variable-speed DC compressors (dominated by specialized firms such as Secop and Danfoss, whose technological roadmaps heavily influence final product performance), procurement of advanced insulation materials, notably the growing use of Vacuum Insulated Panels (VIPs) alongside specialized high-density polyurethane foams, and durable marine-grade stainless steel (316L or higher) or advanced, corrosion-resistant composite polymer casings. Upstream operations face continuous challenges in securing a reliable, cost-effective global supply of these highly specialized, certified components that must consistently meet exceptionally stringent maritime durability, electromagnetic compatibility (EMC), and vibration resistance standards. Establishing and maintaining deep, strategic sourcing relationships with these core component suppliers is absolutely essential for manufacturers to rigorously maintain quality control, effectively manage volatile global cost structures, and ensure the rapid integration of the newest energy-saving and compliance-related technologies into the final product assemblies.

The midstream segment involves the meticulous manufacturing, complex assembly, and rigorous testing of the final marine freezer units. Given the demanding operational context, assembly processes transcend standard manufacturing; they require advanced techniques such as vacuum-assisted polyurethane foaming for insulation integrity, robust hermetic sealing to prevent moisture intrusion, precise thermal mapping, and extensive, continuous vibration and shock testing simulating prolonged sea conditions. Manufacturers operating in this stage must strictly adhere to multiple international certification standards, including ISO protocols, CE conformity markings, specific maritime safety agency approvals (e.g., ABYC, USCG), and stringent environmental regulations pertaining to refrigerant handling and disposal. Distribution channels then diverge into two primary streams: Direct and Indirect. The Direct channel predominantly caters to large Original Equipment Manufacturers (OEMs), who embed the freezers directly into high-volume new vessel construction projects. This often necessitates bespoke design modifications, substantial logistical coordination, and dedicated technical application support throughout the long, complex shipbuilding lifecycle, usually secured via multi-year, strategic supply contracts.

Downstream activities are concentrated on efficiently reaching the vast and geographically dispersed end-user base through the aftermarket channel. The Indirect distribution structure relies heavily on a comprehensive network of specialized marine equipment distributors, globally accessible online retail platforms, and localized marine supply stores (chandleries) situated strategically near major marinas and fishing ports. This channel is primarily focused on supplying high-margin replacement units, offering performance upgrades, and executing complex refit projects. Post-sale support, crucially encompassing robust warranty services, guaranteed global availability of specialized spare parts, and responsive technical assistance, constitutes a highly valued and essential part of the downstream value proposition, particularly because many commercial vessels operate in highly remote locations globally. The effectiveness and speed of this intricate distribution and service network directly correlates with end-user satisfaction metrics and fosters crucial brand loyalty, especially given that any delay in repairing critical marine cooling equipment can immediately translate into catastrophic financial losses of perishable goods for commercial operators.

Potential customers for high-performance marine freezers are remarkably broad and structurally segmented, spanning the entirety of the commercial maritime, governmental, and global leisure sectors, with each group imposing distinct performance criteria and compliance obligations. The most volumetrically significant commercial segment consists of global fishing fleet operators, including large-scale industrial trawlers, specialized factory ships, purse seiners, and long-liners. These customers require systems capable of reliable blast freezing and stable long-term deep storage for multi-ton daily catches. Their core purchasing priorities center on massive capacity, maximized energy efficiency under sustained heavy load conditions, extreme structural robustness to endure relentless operational vibration and heavy seas, and unwavering compliance with stringent international cold chain standards, such as those mandated by the FAO or governing export bodies. Procurement decisions in this sector are driven almost exclusively by the system’s longevity, verifiable reliability track record, and the long-term Total Lifecycle Cost (TLC), as equipment failure poses an immediate and direct threat of inventory loss.

The high-end leisure segment, encompassing owners of luxury superyachts, performance sailing yachts, and long-range motor cruisers, represents the highest margin customer base. These affluent consumers demand refrigeration systems that are aesthetically refined, feature extremely low noise profiles, offer superior spatial efficiency (often requesting integrated drawer designs), and boast advanced digital connectivity that must flawlessly integrate with the vessel's centralized electronics (NMEA 2000 or proprietary bus systems). These discerning customers frequently commission premium, highly customized, polished stainless steel or glass-fronted refrigeration units, prioritizing user-centric design, absolute energy autonomy (optimized DC power draw for battery endurance), and unmatched material quality over maximum storage volume. The sustained growth of this segment is intrinsically linked to global wealth creation trends, the popularity of extended international cruising routes, and continuous expansion and sophistication of high-end marine tourism infrastructure in destinations like the Caribbean and the Mediterranean.

Institutional and governmental entities form a highly specialized but consistently stable segment, encompassing national naval fleets, coast guard agencies, vessels supporting scientific research (e.g., polar vessels, oceanographic surveyors), and auxiliary support ships for offshore oil and gas infrastructure. These critical users require freezers built to withstand extreme environmental stress, often demanding military-specification robustness, shock resistance, redundant systems, and mandatory adherence to highly prescriptive regulatory certifications, including potential nuclear or hazard-zone safety compliance. The procurement cycles for these entities are characteristically lengthy, emphasizing meticulous custom engineering, guaranteed decades-long spare parts and logistics support, and units specifically designed for maximum survivability and operational reliability during high-stakes, protracted missions far from logistical hubs.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.2 Billion |

| Market Forecast in 2033 | $2.0 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Dometic Group, Norcold, Engel, Isotherm (Webasto), Vitrifrigo, Waeco (Dometic), Indel Webasto Marine, U-Line Corporation, Whynter, Koolatron, Vetus, Danfoss, Sea Frost, Technautics, Nova Kool, SunDanzer, National Luna, SnoMaster, isotherm, Isotherm Marine Systems, Snomaster, Frigoboat, Seafrost, Glacier Bay. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The contemporary technology landscape for the marine freezer market is fundamentally defined by the strategic pivot towards high-efficiency refrigeration architectures, primarily centered around sophisticated variable-speed DC compressors. These advanced compressors, often produced under license or proprietary technology from industry leaders like Secop and Danfoss, represent the foundational engine of modern marine cooling. Their core functional advantage lies in their capability to modulate the cooling output speed continuously and precisely based on the detected thermal load and the immediately available power input. This sophisticated modulation dramatically reduces the transient power peaks and overall energy consumption footprint compared to older, less flexible fixed-speed AC systems. This technological shift is critically important for all vessels that rely extensively on finite battery banks, solar arrays, or small generators, as it ensures consistent, stable freezing performance while minimizing the detrimental impact on the vessel’s complex, distributed power budget. In parallel, significant technological refinement has occurred in the deployment of advanced heat exchange systems, encompassing specialized water-cooled condensers that offer superior thermal dissipation in high ambient temperature marine environments, a key factor for maintaining efficiency in tropical cruising regions.

A secondary, but equally vital, technology defining market capability involves groundbreaking advancements in insulation science and structural marine construction methodologies. The industry is rapidly adopting cutting-edge insulation materials, most notably the Vacuum Insulated Panels (VIPs), which deliver thermal performance orders of magnitude superior to traditional insulation methods, allowing manufacturers to achieve required temperature stability with significantly thinner wall profiles. This innovation provides the crucial benefit of maximizing internal storage capacity while minimizing the external footprint—an extremely valuable consideration where every centimeter of space onboard a vessel is utilized. These advanced insulation components are encapsulated within robust, purpose-designed marine-grade enclosures, typically fabricated from high-grade 316 stainless steel or specialized, UV and corrosion-resistant composite polymers. These design elements collectively ensure that the units maintain absolute resistance to continuous exposure to salt water, high moisture content air, and severe mechanical vibration, consequently extending the operational service life far beyond the expectations of standard commercial appliances and ensuring compliance with stringent marine classification society requirements.

The emerging technological front is decisively focused on next-generation connectivity and integrated smart vessel management. Key developments include robust implementation of Internet of Things (IoT) protocols that enable comprehensive remote diagnostics, real-time performance tracking, and the delivery of prophylactic maintenance alerts directly via satellite or cellular links to shore-based fleet management centers. This remote capability is transforming maintenance logistics for large commercial operations. Moreover, regulatory pressure, primarily driven by international agreements such as the Montreal Protocol and Europe’s F-Gas regulation, is accelerating the transition toward refrigerants with ultra-low Global Warming Potential (GWP), particularly natural refrigerants like R290 (propane) or R600a (isobutane). These fluids provide not only compliance advantages but also often deliver marginal improvements in thermodynamic efficiency. Full network integration is also becoming standard, utilizing protocols such as NMEA 2000, which allows centralized digital control and simultaneous monitoring of the freezer system alongside other crucial navigational and operational ship systems, enhancing the vessel’s overall automation, safety, and operational efficiency profile.

Marine freezers are engineered for extreme resilience, featuring specialized components designed to withstand intense corrosion, mechanical vibration, continuous motion, and high humidity prevalent at sea. Crucially, they utilize high-efficiency DC compressors and thick, proprietary insulation, enabling reliable operation primarily on battery power (12V/24V), unlike standard AC household units that require stable shore power.

The predominant and most impactful technology is the variable-speed DC compressor. These advanced components adjust their cooling output speed precisely based on the immediate thermal load and available electrical input, drastically reducing average power draw and maximizing the endurance of onboard battery banks for prolonged off-grid cruising.

IoT and AI systems provide crucial predictive maintenance capabilities by continuously analyzing real-time operational data (e.g., compressor pressures, power consumption anomalies, temperature stability trends). This allows fleet managers to receive proactive, remotely generated alerts about potential component failures, enabling efficient scheduled repairs during planned downtime and preventing costly cargo loss at sea.

Future market growth is primarily polarized between the high-value Luxury Recreational Boating segment in North America and Europe, demanding integrated, silent, and aesthetically superior units, and the high-volume Commercial Fishing segment in the Asia Pacific (APAC) region, which drives demand for robust, high-capacity blast and deep-freeze systems.

The key regulatory pressure stems from international environmental mandates, specifically directives aimed at phasing down high Global Warming Potential (GWP) refrigerants (HFCs). This forces manufacturers to invest heavily in redesigning systems to safely and efficiently use low-GWP, natural refrigerants like R290 (propane) and R600a (isobutane) to ensure future market compliance.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.