ID : MRU_ 443476 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

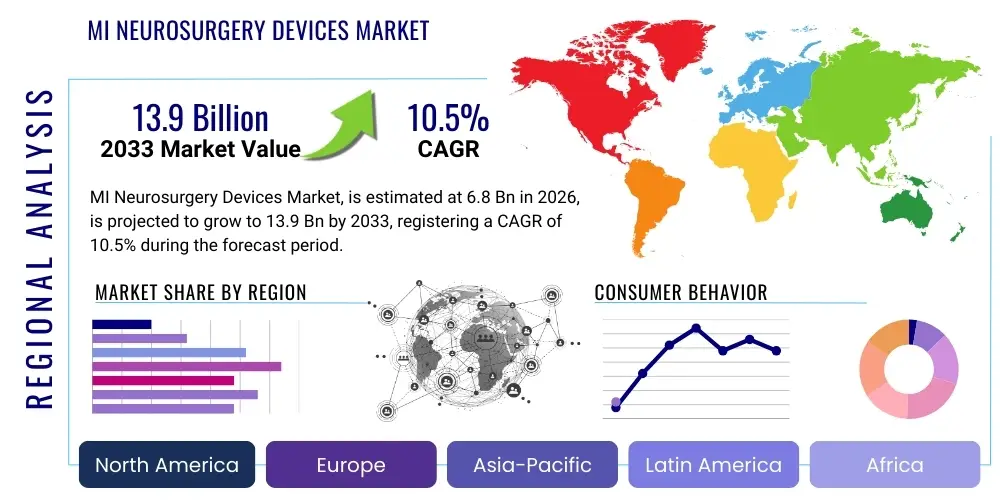

The MI Neurosurgery Devices Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.5% between 2026 and 2033. The market is estimated at USD 6.8 Billion in 2026 and is projected to reach USD 13.9 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the increasing global incidence of neurological disorders, coupled with technological advancements that enhance precision and reduce recovery times associated with surgical procedures.

The Minimally Invasive (MI) Neurosurgery Devices Market encompasses a highly specialized category of medical instruments and systems designed to facilitate neurosurgical procedures through smaller incisions, minimizing damage to surrounding healthy tissue. These devices are central to modern neurosurgical practice, offering significant advantages over traditional open surgery, including reduced patient trauma, lower risk of infection, decreased hospitalization duration, and superior cosmetic outcomes. The core product categories include neuro-endoscopes, specialized high-definition visualization systems, robotic and navigation platforms, and advanced intraoperative monitoring tools essential for complex procedures such involving brain tumors, vascular malformations, and intricate spinal conditions.

Major applications of MI neurosurgery devices span oncological procedures, such as transsphenoidal removal of pituitary tumors and biopsy of deep-seated brain lesions; functional neurosurgery, including deep brain stimulation (DBS) electrode placement; and spinal neurosurgery, targeting herniated discs and spinal instability. The fundamental benefits—enhanced precision via navigation technology, real-time feedback through imaging systems, and reduced blood loss—are making these techniques the standard of care globally. The integration of advanced optics and precision mechanical components ensures that surgeons can operate in sensitive neural environments with unprecedented control, transforming the prognosis for many patients with critical neurological conditions.

Key driving factors propelling the adoption of MI neurosurgery devices include the rapid expansion of the aging population worldwide, which increases the prevalence of age-related neurological disorders such as Alzheimer's, Parkinson's disease, and stroke-related complications. Furthermore, continuous innovation in high-resolution imaging (like intraoperative MRI and CT) and the increasing capability of robotic assistance systems to perform intricate maneuvers are widening the scope of treatable conditions. The growing demand for cost-effective healthcare solutions that accelerate patient discharge also favors minimally invasive approaches, solidifying their market position.

The MI Neurosurgery Devices Market is characterized by intense technological innovation and shifting clinical paradigms favoring less invasive treatments. Business trends show a distinct move toward strategic collaborations between technology developers and neurosurgical centers of excellence to rapidly prototype and integrate advanced robotic and AI-enhanced navigation systems. Key industry players are focusing on miniaturization, enhanced ergonomics, and the development of integrated operating room solutions that streamline workflows and improve real-time data accessibility during complex operations. Furthermore, sustained venture capital interest in specialized device manufacturers focused on laser interstitial thermal therapy (LITT) and focused ultrasound technology underscores a broader trend toward non-ablative and targeted therapeutic interventions.

Regional trends indicate North America currently dominates the market, driven by high healthcare expenditure, established reimbursement frameworks, and the early adoption of cutting-edge technologies like sophisticated neuro-navigation and robotic surgery platforms. However, the Asia Pacific (APAC) region is projected to exhibit the fastest growth over the forecast period, fueled by expanding healthcare infrastructure, increasing medical tourism, and rising public awareness regarding the benefits of minimally invasive procedures, particularly in China and India. Europe maintains a strong position, bolstered by government investments in centralized neuroscience research and well-developed regulatory pathways facilitating market entry for new devices.

Segment trends highlight the dominance of the neuro-endoscopy and neuro-navigation systems segments due to their indispensable role in precision surgery. Within applications, the cranial procedures segment, particularly for complex tumor resections, commands the largest market share, while the spinal segment demonstrates accelerating growth, spurred by the increasing incidence of degenerative disc diseases and the shift toward outpatient spinal interventions utilizing specialized instrumentation. End-user trends show that specialized hospital neurosurgery departments remain the primary purchasers, but Ambulatory Surgical Centers (ASCs) are emerging as significant growth centers, especially for routine spinal and peripheral nerve procedures, driven by cost efficiency and patient preference for non-hospital settings.

User inquiries regarding Artificial Intelligence (AI) in MI neurosurgery overwhelmingly center on enhanced precision, automation potential, and implications for surgical training. Common questions address how AI can reduce surgical time, improve tumor margin detection, and integrate predictive analytics into navigation systems to mitigate operative risks. Users are highly interested in the role of machine learning in optimizing preoperative planning (e.g., segmenting critical structures from imaging data), and the expected timeframe for widespread adoption of fully autonomous robotic assistance systems. A significant theme is the expected synergy between AI algorithms and existing high-definition neuro-endoscopy and robotic platforms, focusing on how AI provides real-time guidance and potentially automates repetitive or highly standardized surgical steps, ultimately aiming to democratize complex procedures and improve consistency in outcomes across different healthcare settings.

AI's primary influence is moving neurosurgery towards hyper-personalization and predictive safety. By analyzing vast datasets derived from pre-operative MRI/CT scans, intraoperative monitoring data, and surgical video feeds, AI models can construct highly accurate 3D surgical maps, anticipate potential complications (such as microvascular damage or tissue shift), and provide actionable, real-time feedback to the operating surgeon. This integration enhances the performance of MI devices, transforming standard navigation systems into intelligent, adaptive guidance tools. Furthermore, AI is crucial in simulating complex scenarios for surgical training, allowing novice surgeons to practice high-stakes procedures in a safe, repeatable, and quantifiable environment, thereby accelerating skill acquisition and ensuring higher proficiency before entering the operating room.

The integration of deep learning models into image-guided surgery (IGS) systems significantly boosts the market value proposition of MI neurosurgery devices. AI enhances the clarity and utility of multimodal imaging fusion, ensuring that the critical neural pathways and pathological tissues are accurately differentiated in real-time, even when anatomical shifts occur during surgery (known as "brain shift"). This enhanced accuracy allows surgeons utilizing MI devices, such as flexible endoscopes and precision robotics, to achieve maximal resection with minimal functional morbidity. The long-term trajectory of AI involvement includes developing smart tools that can independently verify surgical targets and optimize device trajectories, further cementing AI as a foundational technology for the next generation of minimally invasive neurosurgical platforms.

The market for Minimally Invasive Neurosurgery Devices is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), all contributing to distinct Impact Forces shaping its competitive landscape and adoption rates. A crucial driver is the increasing global elderly population, inherently susceptible to neurological ailments requiring surgical intervention, thus fueling sustained demand for low-trauma procedures. Simultaneously, the rapid evolution of technology, particularly in high-definition imaging, surgical robotics, and specialized instrumentation that enables access to previously unreachable brain regions, provides continuous upward momentum. Regulatory bodies, recognizing the patient benefits, are also gradually streamlining approval processes for proven innovative MI technologies, accelerating market access.

However, significant restraints temper this expansion. The substantial initial capital investment required for high-end MI neurosurgery systems, such as advanced neuro-navigation units and dedicated robotics, often presents a barrier to adoption, particularly in developing economies or smaller healthcare facilities. Furthermore, the steep learning curve and the necessity for specialized training for neurosurgeons and support staff to effectively utilize these complex devices can limit their rapid diffusion. Product recalls, although infrequent, and the inherent risks associated with penetrating the Central Nervous System (CNS) require stringent quality control and slow down innovation cycles due to rigorous regulatory scrutiny.

Opportunities for growth are abundant, primarily centered around expanding applications in emerging economies through public-private partnerships designed to subsidize equipment costs and provide necessary training infrastructure. The growing trend toward hybrid operating rooms (ORs) that seamlessly integrate imaging, navigation, and robotic technologies offers manufacturers a fertile ground for integrated system sales. Moreover, the development of disposable or single-use MI instruments addressing infection control concerns and reducing sterilization burdens represents a niche but highly lucrative opportunity. The major impact forces are technological obsolescence risk, demanding continuous R&D investment, and favorable patient outcomes data, which significantly drives clinical acceptance and positive reimbursement decisions globally.

The Minimally Invasive Neurosurgery Devices market is broadly segmented based on Product Type, Application, and End-User, reflecting the diverse technologies and clinical areas where these devices are utilized. Understanding these segment dynamics is critical for market participants to tailor their strategic focus, whether targeting the burgeoning demand for specialized neuro-endoscopes in cranial procedures or addressing the volume-driven needs of the spinal segment. The segmentation underscores the move toward highly specialized tools that enhance precision and procedural efficiency, differentiating high-value capital equipment from high-volume consumable instruments. Analyzing the interplay between these segments reveals that technological convergence, especially between advanced imaging and robotic platforms, is currently the most significant factor driving growth across all categories.

The market composition is heavily influenced by the Product Type segment, where advanced visualization and neuro-navigation systems account for the largest revenue share due to their fundamental role in virtually all MI neurosurgical operations, requiring continuous hardware and software upgrades. Application-wise, the complexity and severity of cranial procedures (e.g., complex tumor ablation and ventricular procedures) ensure its financial dominance, though the increasing frequency of outpatient spinal procedures is rapidly enhancing the spinal segment's contribution. End-user analysis highlights the centrality of large, tertiary hospitals and specialized neuroscience centers, which possess the necessary expertise and financial resources to acquire and maintain state-of-the-art MI systems, acting as primary demand drivers for premium products.

The value chain for MI Neurosurgery Devices is complex, starting with high-precision raw materials and culminating in specialized surgical intervention within a clinical setting. Upstream analysis focuses on specialized component manufacturing, including sophisticated optics, miniature sensors, high-strength biocompatible polymers, and specialized micro-machinery required for robotic joints and precision instrument tips. Suppliers in this phase must adhere to stringent quality standards (ISO 13485) and often engage in long-term partnerships with device manufacturers to ensure consistency and technological compatibility. Innovation at this stage, particularly in materials science (e.g., lightweight, radio-translucent materials), directly impacts the safety and efficacy of the final device, creating a high barrier to entry for new component suppliers.

The mid-stream segment involves the core manufacturing, assembly, and rigorous testing of complex systems like neuro-navigation platforms and surgical robots. Key manufacturers invest heavily in R&D to integrate software (AI, machine learning) with hardware, ensuring seamless system performance and user interface reliability. Following manufacturing, the distribution channel becomes critical. Due to the high value and required specialized service, direct distribution models are prevalent for capital equipment (robots, navigation systems), allowing manufacturers to maintain tight control over installation, training, and maintenance. Conversely, consumable instruments and standard endoscopy components often utilize indirect channels, relying on specialized medical device distributors or Group Purchasing Organizations (GPOs) to reach a wider network of hospitals and clinics efficiently.

Downstream analysis involves the direct interaction with end-users—primarily highly specialized neurosurgery departments in hospitals and, increasingly, specialized ASCs. These facilities serve as the final point of purchase, driven by clinical efficacy data, total cost of ownership, and comprehensive service agreements provided by the manufacturer. The transition to minimally invasive techniques necessitates ongoing training and technical support, making after-sales service a crucial component of the value proposition. Direct distribution ensures that manufacturers maintain deep relationships with key opinion leaders (KOLs) and clinical decision-makers, driving product feedback loops essential for continuous improvement and market positioning.

The primary consumers and end-users of MI Neurosurgery Devices are sophisticated healthcare institutions requiring specialized infrastructure and highly trained personnel to perform complex neurological procedures. Large-scale tertiary and quaternary hospitals, particularly those affiliated with academic medical centers, represent the largest customer segment. These institutions handle the highest volume of complex neurological pathologies, including difficult-to-reach tumors, cerebral aneurysms, and severe spinal cord injuries, mandating the use of cutting-edge technology such as surgical robotics and intraoperative imaging systems. Their purchasing decisions are heavily influenced by clinical outcomes, research grants, and the ability to attract top-tier neurosurgeons, positioning them as the key buyers for premium, high-capital equipment.

Ambulatory Surgical Centers (ASCs) constitute the fastest-growing customer segment, particularly in North America, for streamlined and lower-risk procedures. As MI techniques become standardized for certain spinal procedures (like single-level discectomies) and peripheral nerve surgeries, ASCs offer a cost-effective alternative to traditional hospital settings, attracting patients focused on swift recovery and reduced costs. Although ASCs typically procure less expensive, portable systems compared to large hospitals, their increasing volume of procedures makes them critical buyers for specialized consumables, high-definition endoscopes, and simplified neuro-navigation tools tailored for outpatient environments. This shift necessitates manufacturers to develop more compact, user-friendly, and cost-efficient product lines to meet the ASC demand.

Furthermore, specialized neuroscience centers and focused trauma centers are significant purchasers, often integrating a comprehensive suite of MI devices to offer holistic care. These centers are frequently early adopters of new technologies, such as advanced laser ablation systems (LITT), as they strive to offer the most advanced treatment options for intractable epilepsy or difficult-to-treat deep brain lesions. Government and military hospitals, especially those specializing in neurological trauma care, also represent a stable customer base, focusing procurement on robust, reliable, and easily deployable navigation and imaging systems capable of functioning across varied clinical environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 13.9 Billion |

| Growth Rate | CAGR 10.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic plc, Stryker Corporation, B. Braun Melsungen AG, Karl Storz SE & Co. KG, Olympus Corporation, Johnson & Johnson (DePuy Synthes), Zimmer Biomet Holdings, Inc., Integra LifeSciences Holdings Corporation, Brainlab AG, Renishaw plc, Stereotaxis Inc., Boston Scientific Corporation, InMode Ltd., ConMed Corporation, Synaptive Medical Inc., Mizuho OSI, Intuitive Surgical Inc., Leica Microsystems, Accuray Incorporated, Natus Medical Incorporated. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the MI Neurosurgery Devices market is characterized by a rapid fusion of advanced imaging, precision robotics, and computational guidance systems aimed at minimizing invasiveness while maximizing surgical accuracy. Neuro-navigation systems, utilizing optical or electromagnetic tracking, have become standard of care, offering real-time correlation between pre-operative imaging and the patient's anatomy during surgery. Recent innovations focus on integrating intraoperative imaging modalities, such as mobile CT and MRI, directly into the navigation workflow to correct for "brain shift"—the anatomical displacement that occurs once the skull is opened, thereby maintaining high fidelity of the navigational guidance throughout the procedure. This continuous technological refinement is essential for performing intricate procedures through keyhole approaches.

Robotics and flexible instrumentation represent another critical area of technological advancement. Robotic systems are increasingly being utilized not just for guiding stereotactic devices (like DBS electrodes), but also for performing complex microsurgical maneuvers, offering enhanced stability, tremor filtration, and controlled force application far exceeding human physiological limits. Simultaneously, high-definition neuro-endoscopy has evolved significantly, incorporating 4K and 3D visualization capabilities, along with channel irrigation and suction features, to provide superior operative field clarity and maneuverability within confined spaces like ventricles and the skull base. This technological sophistication necessitates robust networking and data management infrastructure within the operating room.

Furthermore, therapeutic ablation technologies are transforming the treatment of certain neurological conditions. Laser Interstitial Thermal Therapy (LITT) and High-Intensity Focused Ultrasound (HIFU) represent non-invasive or minimally invasive alternatives for treating conditions like drug-resistant epilepsy and specific brain tumors. LITT, for instance, uses MRI-guided fiber optics to deliver thermal energy precisely to target tissue, resulting in minimal collateral damage. This shift from resection to highly targeted ablation highlights the market’s pivot towards technologies that facilitate immediate and localized treatment with minimal systemic impact. These advanced technologies collectively drive higher investment in specialized training and infrastructure upgrading across major neurosurgical centers globally.

The primary driver is the accelerating prevalence of neurological disorders globally, coupled with continuous technological advancements in neuro-navigation and surgical robotics, which significantly enhance procedural precision and minimize patient recovery time.

AI is used for complex pre-operative planning, real-time image segmentation, and surgical simulation, while robotics provide enhanced stability, tremor reduction, and precise instrument manipulation for highly delicate procedures like Deep Brain Stimulation (DBS) and tumor ablation.

The Neuro-navigation Systems segment currently holds the largest revenue share due to its critical and mandatory role in virtually all advanced MI neurosurgical procedures, ensuring high spatial accuracy and safety throughout the operation.

The most significant restraint is the extremely high initial capital cost associated with acquiring advanced systems, such as neuro-navigation platforms, specialized robotic units, and integrated intraoperative imaging equipment, alongside the specialized training requirements.

The Asia Pacific (APAC) region is projected to exhibit the highest CAGR, propelled by rapid investments in healthcare infrastructure, increasing access to advanced medical care, and rising public awareness regarding the benefits of minimally invasive surgical techniques in countries like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.